Download as pdf or txt

You might also like

- Airi Bin Subari - CoEDocument2 pagesAiri Bin Subari - CoES. AiriNo ratings yet

- Xdbs - Offer LetterDocument3 pagesXdbs - Offer LetterAnkit PathakNo ratings yet

- VIVODocument1 pageVIVOMontu ShaniNo ratings yet

- Employment Offer Letter: REF: DTS-OL-C1-122-17Document3 pagesEmployment Offer Letter: REF: DTS-OL-C1-122-17usama hamood100% (3)

- Sample Proposal 1Document8 pagesSample Proposal 1gauravdhawan199180% (5)

- Last Will and Testament - Hannah MabayoDocument3 pagesLast Will and Testament - Hannah MabayoHannah MabayoNo ratings yet

- Sample California Motion For Mandatory Dismissal For Delay in ProsecutionDocument3 pagesSample California Motion For Mandatory Dismissal For Delay in ProsecutionStan Burman100% (1)

- Taxflash: Tax Indonesia / September 2018 / No.10Document4 pagesTaxflash: Tax Indonesia / September 2018 / No.10Jabbaar MohammadNo ratings yet

- Taxflash 2023 02Document3 pagesTaxflash 2023 02Kasuma YeniNo ratings yet

- Taxflash: Tax Indonesia / June 2018 / No.07Document3 pagesTaxflash: Tax Indonesia / June 2018 / No.07Daisy Anita SusiloNo ratings yet

- Taxflash: Tax Indonesia / July 2017 / No.08Document3 pagesTaxflash: Tax Indonesia / July 2017 / No.08Daisy Anita SusiloNo ratings yet

- PWC Indonesia - Tax Flash 2020 #03 PDFDocument4 pagesPWC Indonesia - Tax Flash 2020 #03 PDFfajarNo ratings yet

- Taxflash 2023 06Document3 pagesTaxflash 2023 06yaranami channelNo ratings yet

- Taxflash: Tax Indonesia / July 2017 / No.09Document3 pagesTaxflash: Tax Indonesia / July 2017 / No.09Daisy Anita SusiloNo ratings yet

- FAQs For Bayanihan2Document2 pagesFAQs For Bayanihan2Rave LegoNo ratings yet

- Pradhan Mantri Awas Yojna 2019 (PMAY) प्रधानमंत्री आवास योजना - 2019 स्कीम की पूरी जानकारीDocument20 pagesPradhan Mantri Awas Yojna 2019 (PMAY) प्रधानमंत्री आवास योजना - 2019 स्कीम की पूरी जानकारीAbinash MandilwarNo ratings yet

- Retirement Plans With HIGHEST SAFETY For Indians-VRK100-03012010Document9 pagesRetirement Plans With HIGHEST SAFETY For Indians-VRK100-03012010RamaKrishna Vadlamudi, CFANo ratings yet

- Product Features: Term Loan (Unsecured) Facility in The Form of Personal Loans by Poonawala FinanceDocument2 pagesProduct Features: Term Loan (Unsecured) Facility in The Form of Personal Loans by Poonawala FinanceBALA GNo ratings yet

- Mr. Pankaj L: Insurance Proposal ForDocument6 pagesMr. Pankaj L: Insurance Proposal ForHarish ChandNo ratings yet

- ICAI - Term Loan ProcessDocument2 pagesICAI - Term Loan ProcessRahul KediaNo ratings yet

- Pradhan Mantri Awas YojanaDocument7 pagesPradhan Mantri Awas YojanaMadhu KiniNo ratings yet

- Rad 1 Be 79Document6 pagesRad 1 Be 79Harish ChandNo ratings yet

- Policy Analysis AssignmentDocument6 pagesPolicy Analysis AssignmentAsmitha NNo ratings yet

- Bajet 2023 Tax Mini BriefDocument52 pagesBajet 2023 Tax Mini BriefChun SengNo ratings yet

- Implication of Union Budget 2023Document12 pagesImplication of Union Budget 2023Aditi GuptaNo ratings yet

- Household Durable Scheme: ObjectivesDocument6 pagesHousehold Durable Scheme: ObjectivesNayanNo ratings yet

- Naya Pakistan Housing Scheme: Construction DocumentsDocument3 pagesNaya Pakistan Housing Scheme: Construction DocumentstahaNo ratings yet

- Instabuddy: Institute of Rural Management AnandDocument12 pagesInstabuddy: Institute of Rural Management AnandAnirudh GoelNo ratings yet

- Pradhan Mantri Awas YojanaDocument2 pagesPradhan Mantri Awas YojanaSiksha SharmaNo ratings yet

- A Dissertation On "A Study of Home Loan Industry Growth in India"Document20 pagesA Dissertation On "A Study of Home Loan Industry Growth in India"vaishaliNo ratings yet

- GST Cheque Return LetterDocument6 pagesGST Cheque Return Letterz2824No ratings yet

- Itc-A Few TakeawaysDocument3 pagesItc-A Few TakeawaysApoorva MoonatNo ratings yet

- PGDTP ParnaDocument73 pagesPGDTP ParnaRi ChNo ratings yet

- MSME SchemeDocument9 pagesMSME SchemeNibedita KhatuaNo ratings yet

- Procedure For Private Placement and AllotmentDocument2 pagesProcedure For Private Placement and AllotmentNithya GaneshNo ratings yet

- Loan Policy of Uco Bank For Retail SectorDocument22 pagesLoan Policy of Uco Bank For Retail SectorAnurag BohraNo ratings yet

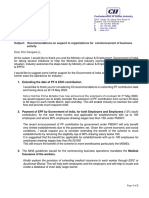

- April 16, 2020: Subject: Recommendations On Support To Organizations For Commencement of Business ActivityDocument2 pagesApril 16, 2020: Subject: Recommendations On Support To Organizations For Commencement of Business ActivityAryanSahniNo ratings yet

- New India Assurance Co. Ltd.Document36 pagesNew India Assurance Co. Ltd.epshitaNo ratings yet

- GHJHJKDocument16 pagesGHJHJKCheGanJiNo ratings yet

- Final Housekeeping Tender 2021Document36 pagesFinal Housekeeping Tender 2021MohakNo ratings yet

- Human Settlement Trainership Programme 2022Document1 pageHuman Settlement Trainership Programme 2022Thandeka NonhlanhlaNo ratings yet

- Assignment On Initiative of Banladesh Goverment For Entrepreneurship DevelopmentDocument11 pagesAssignment On Initiative of Banladesh Goverment For Entrepreneurship DevelopmentBabor PaikNo ratings yet

- Chandrasekar Chigurupati PDFDocument6 pagesChandrasekar Chigurupati PDFraaj mahendraNo ratings yet

- New India Assurance Co LTDDocument30 pagesNew India Assurance Co LTDRachita PrakashNo ratings yet

- FrontlinersDocument5 pagesFrontlinerssdycu74No ratings yet

- DDD DDDD DDDDDocument79 pagesDDD DDDD DDDDSangeetaLakhesarNo ratings yet

- PATROCK BALLAST Final EDITEDDocument35 pagesPATROCK BALLAST Final EDITEDreuben simiyuNo ratings yet

- Income Tax Volume I AY 2022-23Document241 pagesIncome Tax Volume I AY 2022-23PATANJALI ENTERPRISES100% (4)

- LoansDocument17 pagesLoansPia Samantha DasecoNo ratings yet

- Legal Notice of NatrajanDocument7 pagesLegal Notice of NatrajanbhaskardexterNo ratings yet

- Mr. Sandeep: Insurance Proposal ForDocument6 pagesMr. Sandeep: Insurance Proposal ForHarish ChandNo ratings yet

- Mr. Anil Kumar: An Innovative Retirement Solution ForDocument6 pagesMr. Anil Kumar: An Innovative Retirement Solution ForBhanu ANinnocentNo ratings yet

- Wa0052.Document2 pagesWa0052.sujanNo ratings yet

- Offer Letter - M. Zahid - Sr. RNO EngineerDocument1 pageOffer Letter - M. Zahid - Sr. RNO EngineerhmzgNo ratings yet

- Your Policy Details:: Note: 1. The Values Displayed Above Are Exclusive of taxes/GST 2Document2 pagesYour Policy Details:: Note: 1. The Values Displayed Above Are Exclusive of taxes/GST 2sridharanelvagalNo ratings yet

- Concall Transcript Q3 FY 2017Document19 pagesConcall Transcript Q3 FY 2017saurav.kumarNo ratings yet

- Actuary India July Final WebDocument36 pagesActuary India July Final Webyash mallNo ratings yet

- Income TaxDocument60 pagesIncome TaxAnshu LalitNo ratings yet

- SAMPLE Independent Contractor Agreement - v1 0 - 04 May 2022 - Miuki ToginDocument13 pagesSAMPLE Independent Contractor Agreement - v1 0 - 04 May 2022 - Miuki ToginJONATHAN DE GUZMANNo ratings yet

- Truearth Book PDFDocument65 pagesTruearth Book PDFRaymond MachariaNo ratings yet

- Summary 300 LogementDocument8 pagesSummary 300 Logementmariekone79No ratings yet

- How to Reverse Recession and Remove Poverty in India: Prove Me Wrong & Win 10 Million Dollar Challenge Within 60 DaysFrom EverandHow to Reverse Recession and Remove Poverty in India: Prove Me Wrong & Win 10 Million Dollar Challenge Within 60 DaysNo ratings yet

- Fiesta World Mall Vs LinbergDocument3 pagesFiesta World Mall Vs LinbergAmanda ButtkissNo ratings yet

- Alba Patio Vs NLRCDocument9 pagesAlba Patio Vs NLRCJustin HarrisNo ratings yet

- Supreme Court: Republic of The Philippines Manila Second DivisionDocument4 pagesSupreme Court: Republic of The Philippines Manila Second DivisionNikki Joanne Armecin LimNo ratings yet

- Belgica V Ochoa GR 208566Document160 pagesBelgica V Ochoa GR 208566Jeon GarciaNo ratings yet

- Application Under Section 8 of The Arbitration and Conciliation Act, 1996Document13 pagesApplication Under Section 8 of The Arbitration and Conciliation Act, 1996Ananaya Sachdeva100% (1)

- 'Ucsp - Group 9 DiligenceDocument25 pages'Ucsp - Group 9 DiligenceEva Mae TugbongNo ratings yet

- Presentation 43Document11 pagesPresentation 43Mihai 1TAPNo ratings yet

- Manufactured Home Site Tenancy Agreement BetweenDocument6 pagesManufactured Home Site Tenancy Agreement BetweenAnonymous Dk0JJfNo ratings yet

- Workmen Emplyed in Associated Rubber Industries Limited Vs Associated Rubber IndustriesDocument21 pagesWorkmen Emplyed in Associated Rubber Industries Limited Vs Associated Rubber IndustriesShaishavi Kapshikar0% (1)

- Motion For Leave To Travel AbroadDocument2 pagesMotion For Leave To Travel Abroadjessi berNo ratings yet

- DAVID VS. SENATE ELECTORAL TRIBUNAL, G.R. NO. 221538, Sep. 20, 2016Document1 pageDAVID VS. SENATE ELECTORAL TRIBUNAL, G.R. NO. 221538, Sep. 20, 2016Joy DLNo ratings yet

- 26.2.24 Iran Gas PipelineDocument4 pages26.2.24 Iran Gas PipelineIftikharAlamNo ratings yet

- Administrative Law Course OutlineDocument3 pagesAdministrative Law Course OutlinePatricia Pineda100% (2)

- Theories of Law PDFDocument37 pagesTheories of Law PDFaolNo ratings yet

- Peaceful Settlement of DisputesDocument51 pagesPeaceful Settlement of DisputesVivek MenonNo ratings yet

- China Banking Corp V CA and AfpslaiDocument3 pagesChina Banking Corp V CA and AfpslaiPS PngnbnNo ratings yet

- Biristol Case & Mirpuri CaseDocument5 pagesBiristol Case & Mirpuri CaseZen FerrerNo ratings yet

- Maurice B. Moore v. U.S. Bureau of Prisons and United States of America, 129 F.3d 131, 10th Cir. (1997)Document3 pagesMaurice B. Moore v. U.S. Bureau of Prisons and United States of America, 129 F.3d 131, 10th Cir. (1997)Scribd Government DocsNo ratings yet

- Module 1 MGT 209Document9 pagesModule 1 MGT 209Janet T. CometaNo ratings yet

- PBM Employees PRG Vs PBN Co.Document2 pagesPBM Employees PRG Vs PBN Co.claudeNo ratings yet

- Cir Vs Sekisui Jushi PH: Doctrine/SDocument2 pagesCir Vs Sekisui Jushi PH: Doctrine/SIshNo ratings yet

- Daily Time Record Daily Time Record: (NAME) (NAME)Document1 pageDaily Time Record Daily Time Record: (NAME) (NAME)Marven Abello PieraNo ratings yet

- Insurance - Full Text (Concealment-Warranties)Document46 pagesInsurance - Full Text (Concealment-Warranties)Kai TehNo ratings yet

- Odchigue-Bondoc vs. TanDocument1 pageOdchigue-Bondoc vs. TanCarlota Nicolas VillaromanNo ratings yet

- Chapter 29 - Progressivism and The Republican RooseveltDocument4 pagesChapter 29 - Progressivism and The Republican RooseveltloveisgoldenNo ratings yet

- RR 11 2018 - Annex C - Withholding Agent Sworn DeclarationDocument1 pageRR 11 2018 - Annex C - Withholding Agent Sworn DeclarationJames Salviejo PinedaNo ratings yet

- Form 6 BlankDocument4 pagesForm 6 Blankenrique nemenzoNo ratings yet