Download as xlsx, pdf, or txt

You might also like

- (Shared) Day5 Harmonic Hearing Co. - 4271Document17 pages(Shared) Day5 Harmonic Hearing Co. - 4271DamTokyo0% (2)

- CH 03Document67 pagesCH 03Khoirunnisa Dwiastuti100% (2)

- ASSIGNMENT - Jollibee Foods Corp. Financial Forecasting Exercise - by Catherine Rose Tumbali, MBA 2nd Sem, Section 70069Document7 pagesASSIGNMENT - Jollibee Foods Corp. Financial Forecasting Exercise - by Catherine Rose Tumbali, MBA 2nd Sem, Section 70069Cathy Tumbali100% (1)

- Anandam Manufacturing CompanyDocument9 pagesAnandam Manufacturing CompanyAijaz AslamNo ratings yet

- New Heritage Doll Company Case SolutionDocument31 pagesNew Heritage Doll Company Case SolutionSoundarya AbiramiNo ratings yet

- Pacific Grove Spice CompanyDocument3 pagesPacific Grove Spice CompanyLaura JavelaNo ratings yet

- Capital Investment AnalysisDocument5 pagesCapital Investment AnalysisAijaz AslamNo ratings yet

- Directors of Federal Reserve Bank of New York (1914-2014)Document47 pagesDirectors of Federal Reserve Bank of New York (1914-2014)William Litynski100% (1)

- Add Dep Less Tax OCF Change in Capex Change in NWC FCFDocument5 pagesAdd Dep Less Tax OCF Change in Capex Change in NWC FCFGullible KhanNo ratings yet

- Hoa Sen Group OfficialDocument28 pagesHoa Sen Group OfficialBảo TrungNo ratings yet

- Fund Flow Statement - Feb-21Document128 pagesFund Flow Statement - Feb-21Suneet GaggarNo ratings yet

- Kohinoor Chemical Company LTD.: Horizontal AnalysisDocument19 pagesKohinoor Chemical Company LTD.: Horizontal AnalysisShehreen ArnaNo ratings yet

- Eastboro Data - Class - DiscussionDocument11 pagesEastboro Data - Class - Discussionvasuca2007No ratings yet

- NetscapeDocument3 pagesNetscapeulix1985No ratings yet

- Case IDocument20 pagesCase ICherry KanjanapornsinNo ratings yet

- Horizental Analysis On Income StatementDocument21 pagesHorizental Analysis On Income StatementMuhib NoharioNo ratings yet

- Key Operating and Financial Data 2017 For Website Final 20.3.2018Document2 pagesKey Operating and Financial Data 2017 For Website Final 20.3.2018MubeenNo ratings yet

- Puma Energy Results Report q4 2016Document8 pagesPuma Energy Results Report q4 2016KA-11 Єфіменко ІванNo ratings yet

- Ratio Analysis of Engro Vs NestleDocument24 pagesRatio Analysis of Engro Vs NestleMuhammad SalmanNo ratings yet

- Expected Return Risk Free Rate + (Beta Market Risk Premium) Expected Return 3.68% + (0.66 5.05%) Expected Return 7.01%Document16 pagesExpected Return Risk Free Rate + (Beta Market Risk Premium) Expected Return 3.68% + (0.66 5.05%) Expected Return 7.01%Akash GuptaNo ratings yet

- United Tractors TBK.: Balance Sheet Dec-06 DEC 2007 DEC 2008Document26 pagesUnited Tractors TBK.: Balance Sheet Dec-06 DEC 2007 DEC 2008sariNo ratings yet

- DCF 2 CompletedDocument4 pagesDCF 2 CompletedPragathi T NNo ratings yet

- Puma Energy Results Report q3 2016 v3Document8 pagesPuma Energy Results Report q3 2016 v3KA-11 Єфіменко ІванNo ratings yet

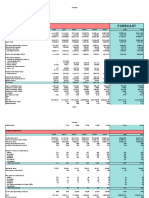

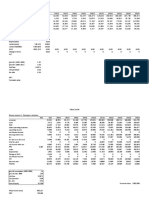

- ABB Power Systems & Automation CompanyDocument13 pagesABB Power Systems & Automation CompanyMohamed SamehNo ratings yet

- Unit: Million VND: Working CapitalDocument12 pagesUnit: Million VND: Working CapitalThảo LinhNo ratings yet

- NetscapeDocument6 pagesNetscapeAnuj BhattNo ratings yet

- DCF 3 CompletedDocument3 pagesDCF 3 CompletedPragathi T NNo ratings yet

- FS AaplDocument20 pagesFS AaplReza FachrizalNo ratings yet

- Supreme Annual Report 2019Document148 pagesSupreme Annual Report 2019adoniscalNo ratings yet

- Tablas Financieras 1Q13Document76 pagesTablas Financieras 1Q13Chavez AznaranNo ratings yet

- Tesla Company AnalysisDocument83 pagesTesla Company AnalysisStevenTsaiNo ratings yet

- Goodyear Indonesia TBK.: Balance SheetDocument20 pagesGoodyear Indonesia TBK.: Balance SheetsariNo ratings yet

- PV OIl Financial Spreadsheet AnalysisDocument32 pagesPV OIl Financial Spreadsheet AnalysisNguyễn Minh ThànhNo ratings yet

- IHH Healthcare BHD Q4 2016 Quarterly Report (Final)Document37 pagesIHH Healthcare BHD Q4 2016 Quarterly Report (Final)Farahain MaizatyNo ratings yet

- Apple V SamsungDocument4 pagesApple V SamsungCarla Mae MartinezNo ratings yet

- Al Fajar WorkingDocument3 pagesAl Fajar WorkingsureniimbNo ratings yet

- Hitung ProyeksiDocument3 pagesHitung ProyeksiDwinanda HarsaNo ratings yet

- Universe 18Document70 pagesUniverse 18fereNo ratings yet

- 1.0 Financial Plan: 1.1. 5-Year Profit & Loss ProjectionDocument3 pages1.0 Financial Plan: 1.1. 5-Year Profit & Loss ProjectionHana AlisaNo ratings yet

- Financial - Analysis (SCI and SFP)Document4 pagesFinancial - Analysis (SCI and SFP)Joshua BristolNo ratings yet

- Astra International TBK.: Balance Sheet Dec-2006 Dec-2007Document18 pagesAstra International TBK.: Balance Sheet Dec-2006 Dec-2007sariNo ratings yet

- Vien Dong Pharmacy Income StatementDocument14 pagesVien Dong Pharmacy Income StatementThảo LinhNo ratings yet

- Horizontal AnalysisDocument1 pageHorizontal AnalysisnazreenNo ratings yet

- Complete Financial Model & Valuation of ARCCDocument46 pagesComplete Financial Model & Valuation of ARCCgr5yjjbmjsNo ratings yet

- Astra Otoparts Tbk. (S) : Balance SheetDocument18 pagesAstra Otoparts Tbk. (S) : Balance SheetsariNo ratings yet

- FIN 422-Midterm AssDocument43 pagesFIN 422-Midterm AssTakibul HasanNo ratings yet

- Excel Files For Case 12 - Value PublishinDocument12 pagesExcel Files For Case 12 - Value PublishinGerry RuntukahuNo ratings yet

- Netflix Spreadsheet - SMG ToolsDocument9 pagesNetflix Spreadsheet - SMG ToolsJohn AngNo ratings yet

- Pro FormaDocument4 pagesPro Formaapi-3710417No ratings yet

- Gildan Model BearDocument57 pagesGildan Model BearNaman PriyadarshiNo ratings yet

- Key Competitors & Inditex Gap H&M Benetton Inditex Operating Results ( Millions)Document1 pageKey Competitors & Inditex Gap H&M Benetton Inditex Operating Results ( Millions)puneetdattaNo ratings yet

- Q3 FY 2024 Metrics FileDocument11 pagesQ3 FY 2024 Metrics Filevighneshsputta2No ratings yet

- Income Statement: USD Millions FY2024 FY2023 FY2022 FY2021Document7 pagesIncome Statement: USD Millions FY2024 FY2023 FY2022 FY2021Vile KushNo ratings yet

- 02 06 BeginDocument6 pages02 06 BeginnehaNo ratings yet

- Fiscal Year Ending December 31 2020 2019 2018 2017 2016Document22 pagesFiscal Year Ending December 31 2020 2019 2018 2017 2016Wasif HossainNo ratings yet

- Blaine Kitchenware: Case Exhibit 1Document15 pagesBlaine Kitchenware: Case Exhibit 1Fahad AliNo ratings yet

- Excel Files For Case 12 Value PublishingDocument12 pagesExcel Files For Case 12 Value PublishingOmer KhanNo ratings yet

- 7-11 MujiDocument15 pages7-11 MujiShiina JarupanichNo ratings yet

- Description Variable 2008: Financial Leverege (Nfo/cse)Document9 pagesDescription Variable 2008: Financial Leverege (Nfo/cse)Nizam Uddin MasudNo ratings yet

- 02 04 EndDocument6 pages02 04 EndnehaNo ratings yet

- ValueInvesting - Io - Financials & Models TemplateDocument66 pagesValueInvesting - Io - Financials & Models TemplatekrishnaNo ratings yet

- United States Census Figures Back to 1630From EverandUnited States Census Figures Back to 1630No ratings yet

- Principles of Cash Flow Valuation: An Integrated Market-Based ApproachFrom EverandPrinciples of Cash Flow Valuation: An Integrated Market-Based ApproachRating: 3 out of 5 stars3/5 (3)

- Running Head: GBADocument8 pagesRunning Head: GBAAijaz AslamNo ratings yet

- Running Head: Johnson Beverages: Finance AssignmentDocument9 pagesRunning Head: Johnson Beverages: Finance AssignmentAijaz AslamNo ratings yet

- Bank of AmericaDocument14 pagesBank of AmericaAijaz AslamNo ratings yet

- Airport OperationsDocument19 pagesAirport OperationsAijaz AslamNo ratings yet

- Johnson Beverage CompanyDocument9 pagesJohnson Beverage CompanyAijaz AslamNo ratings yet

- B&K DistributorsDocument12 pagesB&K DistributorsAijaz AslamNo ratings yet

- Suzan LiteratureDocument14 pagesSuzan LiteratureAijaz AslamNo ratings yet

- Alliance ConcreteDocument11 pagesAlliance ConcreteAijaz AslamNo ratings yet

- Sample Mba 510 Final PaperDocument12 pagesSample Mba 510 Final PaperAijaz AslamNo ratings yet

- Dog Treat Budget Planning PaperDocument15 pagesDog Treat Budget Planning PaperAijaz AslamNo ratings yet

- ACCT 221 Report InstructionsDocument4 pagesACCT 221 Report InstructionsAijaz AslamNo ratings yet

- ORDER 23993 - Quantitative Decision MakingDocument4 pagesORDER 23993 - Quantitative Decision MakingAijaz AslamNo ratings yet

- LBO AnalysisDocument7 pagesLBO AnalysisLeonardoNo ratings yet

- Installment SalesDocument4 pagesInstallment Saleskat kaleNo ratings yet

- Journal EntryDocument4 pagesJournal EntryAshish DhakalNo ratings yet

- Chapter 1 Capital Budgeting: Financial Appraisal ofDocument13 pagesChapter 1 Capital Budgeting: Financial Appraisal ofmkspandianNo ratings yet

- Draft Investment ProposalDocument5 pagesDraft Investment ProposalSandeep Borse100% (1)

- FM CHAPTER 3 Definition of Terms and SummaryDocument4 pagesFM CHAPTER 3 Definition of Terms and SummaryJoyceNo ratings yet

- Assumptions: Back To IndexDocument37 pagesAssumptions: Back To IndexSandesh SinghNo ratings yet

- Del Mundo Landscape SpecialistDocument4 pagesDel Mundo Landscape SpecialistKendall JennerNo ratings yet

- Jimmy M. Reed v. Central National Bank of Alva, A Corporation, 421 F.2d 113, 10th Cir. (1970)Document8 pagesJimmy M. Reed v. Central National Bank of Alva, A Corporation, 421 F.2d 113, 10th Cir. (1970)Scribd Government DocsNo ratings yet

- Chapter 30Document5 pagesChapter 30Yusuf HusseinNo ratings yet

- Accounts ReceivableDocument23 pagesAccounts ReceivableAbby MendozaNo ratings yet

- Philippine Commercial International Bank Vs Court of AppealsDocument3 pagesPhilippine Commercial International Bank Vs Court of AppealsfirstNo ratings yet

- 1.unit 1.contract of Indemnity and GuaranteeDocument28 pages1.unit 1.contract of Indemnity and GuaranteeKarthik100% (1)

- Heirs of Tan Eng Kee Vs CADocument2 pagesHeirs of Tan Eng Kee Vs CAJustin LoredoNo ratings yet

- Dawit Abera - Thesis Final 2020Document76 pagesDawit Abera - Thesis Final 2020Biruk FikreselamNo ratings yet

- FinMan Planning Master-BudgetDocument3 pagesFinMan Planning Master-Budgetjim malajatNo ratings yet

- Eugene Fama PHD DissertationDocument5 pagesEugene Fama PHD DissertationCheapPaperWritingServicesCanada100% (1)

- Long-Run Corporate Tax Avoidance: The University of North Carolina at Chapel HillDocument22 pagesLong-Run Corporate Tax Avoidance: The University of North Carolina at Chapel HillHendrawanNo ratings yet

- Moneda Electronică Și PoliticaDocument14 pagesMoneda Electronică Și Politicaadelin matesNo ratings yet

- InfoEdge Annual Report 2023Document1 pageInfoEdge Annual Report 2023Aditya RoyNo ratings yet

- Case 8 Khalid Ibrahim V Bimb - 221227 - 063132Document16 pagesCase 8 Khalid Ibrahim V Bimb - 221227 - 063132abdul rahimNo ratings yet

- Appointment Letter TemplateDocument3 pagesAppointment Letter TemplateManoj KumarNo ratings yet

- Chapter 8 Capital Market TheoryDocument23 pagesChapter 8 Capital Market TheoryEmijiano Ronquillo100% (1)

- Decision Tree Analysis-2Document1 pageDecision Tree Analysis-2Shalmali ShettyNo ratings yet

- Chapter 20 Measuring GDP and Economic GrowthDocument4 pagesChapter 20 Measuring GDP and Economic GrowthAnsonNo ratings yet

- Auburn University Graduate School Thesis FormatDocument4 pagesAuburn University Graduate School Thesis Formatreneedelgadoalbuquerque100% (2)

- Term Paper International EconomicsDocument5 pagesTerm Paper International Economicsafmzkbysdbblih100% (1)

- Penghindaran Pajak-1Document16 pagesPenghindaran Pajak-1putri nurvadilaNo ratings yet