Statistics of Government Revenues From UK Oil and Gas Production July 2019

Statistics of Government Revenues From UK Oil and Gas Production July 2019

You might also like

- DesignProject Part2ESDocument39 pagesDesignProject Part2ESEdgars SilinsNo ratings yet

- General Principles AND National Taxation: As Lectured by Atty. Rizalina LumberaDocument137 pagesGeneral Principles AND National Taxation: As Lectured by Atty. Rizalina LumberaMarvin Marciano DiñoNo ratings yet

- Tutorial 2e Residence StatusDocument2 pagesTutorial 2e Residence StatusnatlyhNo ratings yet

- Tax Planning and ManagementDocument23 pagesTax Planning and ManagementMinisha Gupta100% (19)

- PXP SEC+17Q+report+Q2+2019Document29 pagesPXP SEC+17Q+report+Q2+2019BERNA RIVERANo ratings yet

- HOMERO - Natural Gas Pipeline ProfitsDocument19 pagesHOMERO - Natural Gas Pipeline ProfitsNadjaMenezesNeryNo ratings yet

- North Dakota REV-E-NEWS: Message From The DirectorDocument3 pagesNorth Dakota REV-E-NEWS: Message From The DirectorRob PortNo ratings yet

- Rac Bidco Limited: Interim Report and Financial StatementsDocument27 pagesRac Bidco Limited: Interim Report and Financial StatementsMus ChrifiNo ratings yet

- Barclays Q318 Results AnnouncementDocument49 pagesBarclays Q318 Results AnnouncementAnonymous g7LakmNNGHNo ratings yet

- Press Release Vallourec Reports Third Quarter and First Nine Months 2020 ResultsDocument16 pagesPress Release Vallourec Reports Third Quarter and First Nine Months 2020 ResultsShambavaNo ratings yet

- Saipem: Results For The First Quarter 2019: HighlightsDocument17 pagesSaipem: Results For The First Quarter 2019: HighlightsBert Lester L ElioNo ratings yet

- NE 06-09 - em InglDocument101 pagesNE 06-09 - em InglLightRINo ratings yet

- Australian Petroleum Statistics: Issue 258, January 2018Document40 pagesAustralian Petroleum Statistics: Issue 258, January 2018Alia ShabbirNo ratings yet

- 2021-09-09 Morrisons Interim AnnouncementDocument48 pages2021-09-09 Morrisons Interim AnnouncementBassel HagagNo ratings yet

- OGUK Methane Action PlanDocument22 pagesOGUK Methane Action PlanRoshan KhanNo ratings yet

- Sector Summary ShippingDocument34 pagesSector Summary ShippingVijeya SeelenNo ratings yet

- Petroleum Industry Report 2018 19Document104 pagesPetroleum Industry Report 2018 19ALI ABBASNo ratings yet

- Greencoat UK Wind Half Year Report FINALDocument33 pagesGreencoat UK Wind Half Year Report FINALblackberryxyzNo ratings yet

- UK Offshore Oil and Gas Industry: Briefing PaperDocument44 pagesUK Offshore Oil and Gas Industry: Briefing PaperLegend AnbuNo ratings yet

- Natural ResourcesDocument59 pagesNatural ResourcesSohel BangiNo ratings yet

- India Union Budget 2010Document19 pagesIndia Union Budget 2010jaguarmcsNo ratings yet

- OGRA Petroleum 2019-20Document96 pagesOGRA Petroleum 2019-20Zahid HussainNo ratings yet

- Tax and British Business Making The Case PDFDocument24 pagesTax and British Business Making The Case PDFNawsher21No ratings yet

- Autumn Budget 2018Document106 pagesAutumn Budget 2018edienewsNo ratings yet

- Impact Report of GEO 114/2018 On Romanian Natural Gas & Power MarketsDocument40 pagesImpact Report of GEO 114/2018 On Romanian Natural Gas & Power MarketsOndina OlariuNo ratings yet

- The Finance Act 2018 and Statutory Changes in The Income Tax LawsDocument19 pagesThe Finance Act 2018 and Statutory Changes in The Income Tax LawsMd. Arifur RahmanNo ratings yet

- 1.national Budget 2019-20Document21 pages1.national Budget 2019-20ibrahimbdNo ratings yet

- 2017-18 Third Quarter Report Fiscal UpdateDocument18 pages2017-18 Third Quarter Report Fiscal UpdateCTV CalgaryNo ratings yet

- Thaiduong Petrol Joint Stock CompanyDocument15 pagesThaiduong Petrol Joint Stock CompanyMinh PhươngNo ratings yet

- Lloyds Bank PLC Q1 2020 Interim Management Statement 30 April 2020Document9 pagesLloyds Bank PLC Q1 2020 Interim Management Statement 30 April 2020saxobobNo ratings yet

- Release 1Q18 ENGDocument27 pagesRelease 1Q18 ENGPaolo SNo ratings yet

- Facts and Figures On UK's Fiscal Deficit (2000-2010) .Document10 pagesFacts and Figures On UK's Fiscal Deficit (2000-2010) .Aditya NayakNo ratings yet

- DUKES 2020 Annexes E J and Long-Term TrendsDocument33 pagesDUKES 2020 Annexes E J and Long-Term TrendsaravindanjayapalNo ratings yet

- 2nd Annual Sustainability ReportDocument36 pages2nd Annual Sustainability ReportAditya BiswasNo ratings yet

- Joline H. Dela Cruz 12-St - Dominic: Revenue RegulationsDocument2 pagesJoline H. Dela Cruz 12-St - Dominic: Revenue RegulationsJuliaNo ratings yet

- April 2021 (A)Document43 pagesApril 2021 (A)Woody MarcNo ratings yet

- Growth Plan 2022Document42 pagesGrowth Plan 2022Guido Fawkes100% (1)

- 2019 Final Greenhouse Gas Emissions Statistical ReleaseDocument42 pages2019 Final Greenhouse Gas Emissions Statistical ReleaseMohammed S M AlghamdiNo ratings yet

- Adv Tax Assignment 1Document8 pagesAdv Tax Assignment 1Hussain ImranNo ratings yet

- Snapshot of India S Oil Gas Data Apr 2023 UploadDocument39 pagesSnapshot of India S Oil Gas Data Apr 2023 UploadAyush SharmaNo ratings yet

- RGGI Reform PrinciplesDocument5 pagesRGGI Reform PrinciplesalissasusanholtNo ratings yet

- Marks & Spencer:: (CITATION Mar20 /L 1033)Document5 pagesMarks & Spencer:: (CITATION Mar20 /L 1033)Arsal ZucceedNo ratings yet

- Public Finance: Fiscal Trends-Strategies For Achieving Higher Growth and DevelopmentDocument13 pagesPublic Finance: Fiscal Trends-Strategies For Achieving Higher Growth and DevelopmentNazmul HaqueNo ratings yet

- 2018 Operating and Capital Budget - Q1 Transit Commission Status ReportDocument8 pages2018 Operating and Capital Budget - Q1 Transit Commission Status ReportA NonymousNo ratings yet

- KPMG Riesgos Financieros Revelaciones Cuantitativas EngDocument16 pagesKPMG Riesgos Financieros Revelaciones Cuantitativas EngPedroLayaNo ratings yet

- Financial ResourcesDocument14 pagesFinancial ResourcesmanjulashenoiNo ratings yet

- Refineries 2021 Sector ProfileDocument13 pagesRefineries 2021 Sector ProfileanajjarNo ratings yet

- National Budget 2019-20, Income Tax and Amendments in The Income Tax Laws: An OverviewDocument22 pagesNational Budget 2019-20, Income Tax and Amendments in The Income Tax Laws: An OverviewNusrat ShatyNo ratings yet

- Petroleum Industry Report 2017 18 PDFDocument96 pagesPetroleum Industry Report 2017 18 PDFAamir SamiNo ratings yet

- Tax Burden UKDocument13 pagesTax Burden UKArturas GumuliauskasNo ratings yet

- INTERNAL REPORT 1 - British PetroleumDocument41 pagesINTERNAL REPORT 1 - British PetroleumMohammad Farhan AdbiNo ratings yet

- Chapter-04 (English-2020)Document20 pagesChapter-04 (English-2020)TonmoyNo ratings yet

- Thame and London Quarterly Report To Note Holders 2019 Q4 Final 28.4.20Document49 pagesThame and London Quarterly Report To Note Holders 2019 Q4 Final 28.4.20saxobobNo ratings yet

- Estimated Impacts of A $170 Carbon Tax in Canada: Revised EditionDocument46 pagesEstimated Impacts of A $170 Carbon Tax in Canada: Revised EditionlindaNo ratings yet

- 2017-2021 Plan: in Italy, Completion of TAP Interconnection and CNG Infrastructure DevelopmentDocument4 pages2017-2021 Plan: in Italy, Completion of TAP Interconnection and CNG Infrastructure DevelopmentVinci Cuore AzzurroNo ratings yet

- Final Updated FY 2018-19 Revenue PerformanceDocument8 pagesFinal Updated FY 2018-19 Revenue PerformanceThe Star KenyaNo ratings yet

- Final Report On OIL and Gas INDUSTRYDocument18 pagesFinal Report On OIL and Gas INDUSTRYShefali SalujaNo ratings yet

- F6uk 2011 Dec QDocument12 pagesF6uk 2011 Dec Qmosherif2011No ratings yet

- DMCIHI - 073 SEC 17Q - Second Quarter - Aug 12 PDFDocument61 pagesDMCIHI - 073 SEC 17Q - Second Quarter - Aug 12 PDFRinna Jane Rivera BolandresNo ratings yet

- BIR Revenue Regulations 2018Document4 pagesBIR Revenue Regulations 2018ohoh42No ratings yet

- Mergers and Acquisitions ReportDocument13 pagesMergers and Acquisitions ReportApoorva SaxenaNo ratings yet

- Foundations of Natural Gas Price Formation: Misunderstandings Jeopardizing the Future of the IndustryFrom EverandFoundations of Natural Gas Price Formation: Misunderstandings Jeopardizing the Future of the IndustryNo ratings yet

- BBMP Receipt - 182598430 - 07 - 09 - 2018 PDFDocument1 pageBBMP Receipt - 182598430 - 07 - 09 - 2018 PDFgopalkaushikNo ratings yet

- A To Z of Payroll Guide 2021Document43 pagesA To Z of Payroll Guide 2021melanieNo ratings yet

- Test Bank - Income Taxation-CparDocument5 pagesTest Bank - Income Taxation-CparStephanie Ann TubuNo ratings yet

- Impact of GST On Manufacturer Distributors and RetailersDocument16 pagesImpact of GST On Manufacturer Distributors and RetailersShubham SinhaNo ratings yet

- 1098-T Copy B: Tuition StatementDocument2 pages1098-T Copy B: Tuition StatementJonathan EllisNo ratings yet

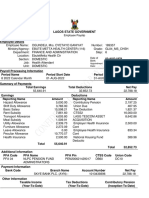

- Httpsmail Lagosstate Gov Ngowaservice svcsGetFileAttachmentid AAMkADFmZmUyMzcxLTQyNWEtNDZmOS1hMjFkLWZhNzg2N2JhNDYzYwBGAADocument3 pagesHttpsmail Lagosstate Gov Ngowaservice svcsGetFileAttachmentid AAMkADFmZmUyMzcxLTQyNWEtNDZmOS1hMjFkLWZhNzg2N2JhNDYzYwBGAADeborah LucridaNo ratings yet

- Btax - Plq1-Answer KeyDocument6 pagesBtax - Plq1-Answer KeyJohn Victor Mancilla MonzonNo ratings yet

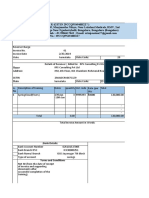

- RPS-PCF-Class - Invoice - 41Document4 pagesRPS-PCF-Class - Invoice - 41Srinivasa HelavarNo ratings yet

- South Delhi Municipal Corporation Tax Payment Checklist For The Year (2019-2020)Document2 pagesSouth Delhi Municipal Corporation Tax Payment Checklist For The Year (2019-2020)Raghvendra ShrivastavaNo ratings yet

- 2015 Bar Examination Question and Suggested Answer in Taxation Law Frequently Asked Articles in Taxation LawDocument16 pages2015 Bar Examination Question and Suggested Answer in Taxation Law Frequently Asked Articles in Taxation LawJan Veah CaabayNo ratings yet

- Deferred Tax Lecture SlidesDocument38 pagesDeferred Tax Lecture Slidesmd salehinNo ratings yet

- ECON 102-Principles of MacroeconomicsDocument48 pagesECON 102-Principles of MacroeconomicsFabio NyagemiNo ratings yet

- Details of Salary Paid and Any Other Income and Tax DeductedDocument3 pagesDetails of Salary Paid and Any Other Income and Tax DeductedAYUSH PRADHANNo ratings yet

- Different Types of Allowances: Presentation By, T. NIKHILA (T-11047) Suraj Kumar SAHU (T-11007)Document16 pagesDifferent Types of Allowances: Presentation By, T. NIKHILA (T-11047) Suraj Kumar SAHU (T-11007)Kumar SurajNo ratings yet

- PSAFDocument920 pagesPSAFReuben GrahamNo ratings yet

- Islamabad Electric Supply Company: Say No To CorruptionDocument1 pageIslamabad Electric Supply Company: Say No To CorruptionSamreen AsmatNo ratings yet

- Bipin Enterprises: GST Tax InvoiceDocument1 pageBipin Enterprises: GST Tax Invoicebipin enterprisesNo ratings yet

- ESIP-CONFERENCE May 23, 2012 - Brussels Vincent Van QuickenborneDocument6 pagesESIP-CONFERENCE May 23, 2012 - Brussels Vincent Van QuickenbornepensiontalkNo ratings yet

- 1702-MX Annual Income Tax Return: Part IV - Schedules InstructionsDocument2 pages1702-MX Annual Income Tax Return: Part IV - Schedules InstructionsVince Alvin DaquizNo ratings yet

- Combined HandoutsDocument224 pagesCombined HandoutsAlexis ParrisNo ratings yet

- Tally 196 Greevani ImpexDocument1 pageTally 196 Greevani Impexpsuraj2808No ratings yet

- Customizing Guide: Withholding Tax Base Amount Accumulation: - For Classic (Non-Condition-Based) Tax CalculationDocument13 pagesCustomizing Guide: Withholding Tax Base Amount Accumulation: - For Classic (Non-Condition-Based) Tax CalculationBruno MerinoNo ratings yet

- Case Study 3 Number 6Document3 pagesCase Study 3 Number 6USD 654No ratings yet

- Taxation: Taxation Is The Supreme Power of A Sovereign State Through Its Law-Making Body, To Impose BurdensDocument6 pagesTaxation: Taxation Is The Supreme Power of A Sovereign State Through Its Law-Making Body, To Impose BurdensTriangular PrismNo ratings yet

- (LECTURE NOTES) TOPIC #6 - Individual Tax Planning and ManagementDocument19 pages(LECTURE NOTES) TOPIC #6 - Individual Tax Planning and Managementcourse shtsNo ratings yet

- Taxation On Real Estate TransactionsDocument3 pagesTaxation On Real Estate TransactionsGlynda ChanNo ratings yet

- Pay Slip July 2021Document1 pagePay Slip July 2021Chiranjibi BiswalNo ratings yet

Download as pdf or txt

You might also like

- DesignProject Part2ESDocument39 pagesDesignProject Part2ESEdgars SilinsNo ratings yet

- General Principles AND National Taxation: As Lectured by Atty. Rizalina LumberaDocument137 pagesGeneral Principles AND National Taxation: As Lectured by Atty. Rizalina LumberaMarvin Marciano DiñoNo ratings yet

- Tutorial 2e Residence StatusDocument2 pagesTutorial 2e Residence StatusnatlyhNo ratings yet

- Tax Planning and ManagementDocument23 pagesTax Planning and ManagementMinisha Gupta100% (19)

- PXP SEC+17Q+report+Q2+2019Document29 pagesPXP SEC+17Q+report+Q2+2019BERNA RIVERANo ratings yet

- HOMERO - Natural Gas Pipeline ProfitsDocument19 pagesHOMERO - Natural Gas Pipeline ProfitsNadjaMenezesNeryNo ratings yet

- North Dakota REV-E-NEWS: Message From The DirectorDocument3 pagesNorth Dakota REV-E-NEWS: Message From The DirectorRob PortNo ratings yet

- Rac Bidco Limited: Interim Report and Financial StatementsDocument27 pagesRac Bidco Limited: Interim Report and Financial StatementsMus ChrifiNo ratings yet

- Barclays Q318 Results AnnouncementDocument49 pagesBarclays Q318 Results AnnouncementAnonymous g7LakmNNGHNo ratings yet

- Press Release Vallourec Reports Third Quarter and First Nine Months 2020 ResultsDocument16 pagesPress Release Vallourec Reports Third Quarter and First Nine Months 2020 ResultsShambavaNo ratings yet

- Saipem: Results For The First Quarter 2019: HighlightsDocument17 pagesSaipem: Results For The First Quarter 2019: HighlightsBert Lester L ElioNo ratings yet

- NE 06-09 - em InglDocument101 pagesNE 06-09 - em InglLightRINo ratings yet

- Australian Petroleum Statistics: Issue 258, January 2018Document40 pagesAustralian Petroleum Statistics: Issue 258, January 2018Alia ShabbirNo ratings yet

- 2021-09-09 Morrisons Interim AnnouncementDocument48 pages2021-09-09 Morrisons Interim AnnouncementBassel HagagNo ratings yet

- OGUK Methane Action PlanDocument22 pagesOGUK Methane Action PlanRoshan KhanNo ratings yet

- Sector Summary ShippingDocument34 pagesSector Summary ShippingVijeya SeelenNo ratings yet

- Petroleum Industry Report 2018 19Document104 pagesPetroleum Industry Report 2018 19ALI ABBASNo ratings yet

- Greencoat UK Wind Half Year Report FINALDocument33 pagesGreencoat UK Wind Half Year Report FINALblackberryxyzNo ratings yet

- UK Offshore Oil and Gas Industry: Briefing PaperDocument44 pagesUK Offshore Oil and Gas Industry: Briefing PaperLegend AnbuNo ratings yet

- Natural ResourcesDocument59 pagesNatural ResourcesSohel BangiNo ratings yet

- India Union Budget 2010Document19 pagesIndia Union Budget 2010jaguarmcsNo ratings yet

- OGRA Petroleum 2019-20Document96 pagesOGRA Petroleum 2019-20Zahid HussainNo ratings yet

- Tax and British Business Making The Case PDFDocument24 pagesTax and British Business Making The Case PDFNawsher21No ratings yet

- Autumn Budget 2018Document106 pagesAutumn Budget 2018edienewsNo ratings yet

- Impact Report of GEO 114/2018 On Romanian Natural Gas & Power MarketsDocument40 pagesImpact Report of GEO 114/2018 On Romanian Natural Gas & Power MarketsOndina OlariuNo ratings yet

- The Finance Act 2018 and Statutory Changes in The Income Tax LawsDocument19 pagesThe Finance Act 2018 and Statutory Changes in The Income Tax LawsMd. Arifur RahmanNo ratings yet

- 1.national Budget 2019-20Document21 pages1.national Budget 2019-20ibrahimbdNo ratings yet

- 2017-18 Third Quarter Report Fiscal UpdateDocument18 pages2017-18 Third Quarter Report Fiscal UpdateCTV CalgaryNo ratings yet

- Thaiduong Petrol Joint Stock CompanyDocument15 pagesThaiduong Petrol Joint Stock CompanyMinh PhươngNo ratings yet

- Lloyds Bank PLC Q1 2020 Interim Management Statement 30 April 2020Document9 pagesLloyds Bank PLC Q1 2020 Interim Management Statement 30 April 2020saxobobNo ratings yet

- Release 1Q18 ENGDocument27 pagesRelease 1Q18 ENGPaolo SNo ratings yet

- Facts and Figures On UK's Fiscal Deficit (2000-2010) .Document10 pagesFacts and Figures On UK's Fiscal Deficit (2000-2010) .Aditya NayakNo ratings yet

- DUKES 2020 Annexes E J and Long-Term TrendsDocument33 pagesDUKES 2020 Annexes E J and Long-Term TrendsaravindanjayapalNo ratings yet

- 2nd Annual Sustainability ReportDocument36 pages2nd Annual Sustainability ReportAditya BiswasNo ratings yet

- Joline H. Dela Cruz 12-St - Dominic: Revenue RegulationsDocument2 pagesJoline H. Dela Cruz 12-St - Dominic: Revenue RegulationsJuliaNo ratings yet

- April 2021 (A)Document43 pagesApril 2021 (A)Woody MarcNo ratings yet

- Growth Plan 2022Document42 pagesGrowth Plan 2022Guido Fawkes100% (1)

- 2019 Final Greenhouse Gas Emissions Statistical ReleaseDocument42 pages2019 Final Greenhouse Gas Emissions Statistical ReleaseMohammed S M AlghamdiNo ratings yet

- Adv Tax Assignment 1Document8 pagesAdv Tax Assignment 1Hussain ImranNo ratings yet

- Snapshot of India S Oil Gas Data Apr 2023 UploadDocument39 pagesSnapshot of India S Oil Gas Data Apr 2023 UploadAyush SharmaNo ratings yet

- RGGI Reform PrinciplesDocument5 pagesRGGI Reform PrinciplesalissasusanholtNo ratings yet

- Marks & Spencer:: (CITATION Mar20 /L 1033)Document5 pagesMarks & Spencer:: (CITATION Mar20 /L 1033)Arsal ZucceedNo ratings yet

- Public Finance: Fiscal Trends-Strategies For Achieving Higher Growth and DevelopmentDocument13 pagesPublic Finance: Fiscal Trends-Strategies For Achieving Higher Growth and DevelopmentNazmul HaqueNo ratings yet

- 2018 Operating and Capital Budget - Q1 Transit Commission Status ReportDocument8 pages2018 Operating and Capital Budget - Q1 Transit Commission Status ReportA NonymousNo ratings yet

- KPMG Riesgos Financieros Revelaciones Cuantitativas EngDocument16 pagesKPMG Riesgos Financieros Revelaciones Cuantitativas EngPedroLayaNo ratings yet

- Financial ResourcesDocument14 pagesFinancial ResourcesmanjulashenoiNo ratings yet

- Refineries 2021 Sector ProfileDocument13 pagesRefineries 2021 Sector ProfileanajjarNo ratings yet

- National Budget 2019-20, Income Tax and Amendments in The Income Tax Laws: An OverviewDocument22 pagesNational Budget 2019-20, Income Tax and Amendments in The Income Tax Laws: An OverviewNusrat ShatyNo ratings yet

- Petroleum Industry Report 2017 18 PDFDocument96 pagesPetroleum Industry Report 2017 18 PDFAamir SamiNo ratings yet

- Tax Burden UKDocument13 pagesTax Burden UKArturas GumuliauskasNo ratings yet

- INTERNAL REPORT 1 - British PetroleumDocument41 pagesINTERNAL REPORT 1 - British PetroleumMohammad Farhan AdbiNo ratings yet

- Chapter-04 (English-2020)Document20 pagesChapter-04 (English-2020)TonmoyNo ratings yet

- Thame and London Quarterly Report To Note Holders 2019 Q4 Final 28.4.20Document49 pagesThame and London Quarterly Report To Note Holders 2019 Q4 Final 28.4.20saxobobNo ratings yet

- Estimated Impacts of A $170 Carbon Tax in Canada: Revised EditionDocument46 pagesEstimated Impacts of A $170 Carbon Tax in Canada: Revised EditionlindaNo ratings yet

- 2017-2021 Plan: in Italy, Completion of TAP Interconnection and CNG Infrastructure DevelopmentDocument4 pages2017-2021 Plan: in Italy, Completion of TAP Interconnection and CNG Infrastructure DevelopmentVinci Cuore AzzurroNo ratings yet

- Final Updated FY 2018-19 Revenue PerformanceDocument8 pagesFinal Updated FY 2018-19 Revenue PerformanceThe Star KenyaNo ratings yet

- Final Report On OIL and Gas INDUSTRYDocument18 pagesFinal Report On OIL and Gas INDUSTRYShefali SalujaNo ratings yet

- F6uk 2011 Dec QDocument12 pagesF6uk 2011 Dec Qmosherif2011No ratings yet

- DMCIHI - 073 SEC 17Q - Second Quarter - Aug 12 PDFDocument61 pagesDMCIHI - 073 SEC 17Q - Second Quarter - Aug 12 PDFRinna Jane Rivera BolandresNo ratings yet

- BIR Revenue Regulations 2018Document4 pagesBIR Revenue Regulations 2018ohoh42No ratings yet

- Mergers and Acquisitions ReportDocument13 pagesMergers and Acquisitions ReportApoorva SaxenaNo ratings yet

- Foundations of Natural Gas Price Formation: Misunderstandings Jeopardizing the Future of the IndustryFrom EverandFoundations of Natural Gas Price Formation: Misunderstandings Jeopardizing the Future of the IndustryNo ratings yet

- BBMP Receipt - 182598430 - 07 - 09 - 2018 PDFDocument1 pageBBMP Receipt - 182598430 - 07 - 09 - 2018 PDFgopalkaushikNo ratings yet

- A To Z of Payroll Guide 2021Document43 pagesA To Z of Payroll Guide 2021melanieNo ratings yet

- Test Bank - Income Taxation-CparDocument5 pagesTest Bank - Income Taxation-CparStephanie Ann TubuNo ratings yet

- Impact of GST On Manufacturer Distributors and RetailersDocument16 pagesImpact of GST On Manufacturer Distributors and RetailersShubham SinhaNo ratings yet

- 1098-T Copy B: Tuition StatementDocument2 pages1098-T Copy B: Tuition StatementJonathan EllisNo ratings yet

- Httpsmail Lagosstate Gov Ngowaservice svcsGetFileAttachmentid AAMkADFmZmUyMzcxLTQyNWEtNDZmOS1hMjFkLWZhNzg2N2JhNDYzYwBGAADocument3 pagesHttpsmail Lagosstate Gov Ngowaservice svcsGetFileAttachmentid AAMkADFmZmUyMzcxLTQyNWEtNDZmOS1hMjFkLWZhNzg2N2JhNDYzYwBGAADeborah LucridaNo ratings yet

- Btax - Plq1-Answer KeyDocument6 pagesBtax - Plq1-Answer KeyJohn Victor Mancilla MonzonNo ratings yet

- RPS-PCF-Class - Invoice - 41Document4 pagesRPS-PCF-Class - Invoice - 41Srinivasa HelavarNo ratings yet

- South Delhi Municipal Corporation Tax Payment Checklist For The Year (2019-2020)Document2 pagesSouth Delhi Municipal Corporation Tax Payment Checklist For The Year (2019-2020)Raghvendra ShrivastavaNo ratings yet

- 2015 Bar Examination Question and Suggested Answer in Taxation Law Frequently Asked Articles in Taxation LawDocument16 pages2015 Bar Examination Question and Suggested Answer in Taxation Law Frequently Asked Articles in Taxation LawJan Veah CaabayNo ratings yet

- Deferred Tax Lecture SlidesDocument38 pagesDeferred Tax Lecture Slidesmd salehinNo ratings yet

- ECON 102-Principles of MacroeconomicsDocument48 pagesECON 102-Principles of MacroeconomicsFabio NyagemiNo ratings yet

- Details of Salary Paid and Any Other Income and Tax DeductedDocument3 pagesDetails of Salary Paid and Any Other Income and Tax DeductedAYUSH PRADHANNo ratings yet

- Different Types of Allowances: Presentation By, T. NIKHILA (T-11047) Suraj Kumar SAHU (T-11007)Document16 pagesDifferent Types of Allowances: Presentation By, T. NIKHILA (T-11047) Suraj Kumar SAHU (T-11007)Kumar SurajNo ratings yet

- PSAFDocument920 pagesPSAFReuben GrahamNo ratings yet

- Islamabad Electric Supply Company: Say No To CorruptionDocument1 pageIslamabad Electric Supply Company: Say No To CorruptionSamreen AsmatNo ratings yet

- Bipin Enterprises: GST Tax InvoiceDocument1 pageBipin Enterprises: GST Tax Invoicebipin enterprisesNo ratings yet

- ESIP-CONFERENCE May 23, 2012 - Brussels Vincent Van QuickenborneDocument6 pagesESIP-CONFERENCE May 23, 2012 - Brussels Vincent Van QuickenbornepensiontalkNo ratings yet

- 1702-MX Annual Income Tax Return: Part IV - Schedules InstructionsDocument2 pages1702-MX Annual Income Tax Return: Part IV - Schedules InstructionsVince Alvin DaquizNo ratings yet

- Combined HandoutsDocument224 pagesCombined HandoutsAlexis ParrisNo ratings yet

- Tally 196 Greevani ImpexDocument1 pageTally 196 Greevani Impexpsuraj2808No ratings yet

- Customizing Guide: Withholding Tax Base Amount Accumulation: - For Classic (Non-Condition-Based) Tax CalculationDocument13 pagesCustomizing Guide: Withholding Tax Base Amount Accumulation: - For Classic (Non-Condition-Based) Tax CalculationBruno MerinoNo ratings yet

- Case Study 3 Number 6Document3 pagesCase Study 3 Number 6USD 654No ratings yet

- Taxation: Taxation Is The Supreme Power of A Sovereign State Through Its Law-Making Body, To Impose BurdensDocument6 pagesTaxation: Taxation Is The Supreme Power of A Sovereign State Through Its Law-Making Body, To Impose BurdensTriangular PrismNo ratings yet

- (LECTURE NOTES) TOPIC #6 - Individual Tax Planning and ManagementDocument19 pages(LECTURE NOTES) TOPIC #6 - Individual Tax Planning and Managementcourse shtsNo ratings yet

- Taxation On Real Estate TransactionsDocument3 pagesTaxation On Real Estate TransactionsGlynda ChanNo ratings yet

- Pay Slip July 2021Document1 pagePay Slip July 2021Chiranjibi BiswalNo ratings yet