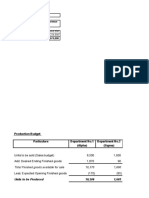

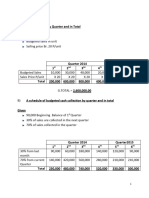

Budgeting Example-Worked Out

Budgeting Example-Worked Out

You might also like

- Universiti Teknologi Mara Final Assessment: Confidential 1 AC/JUL 2022/MAF503Document10 pagesUniversiti Teknologi Mara Final Assessment: Confidential 1 AC/JUL 2022/MAF503Alyn AdnanNo ratings yet

- Harsh Electricals: Analyzing Cost in Search of ProfitDocument11 pagesHarsh Electricals: Analyzing Cost in Search of ProfitSanJana NahataNo ratings yet

- Cma Budget ExcelDocument6 pagesCma Budget ExcelDristi SinghNo ratings yet

- Colin - BookDocument15 pagesColin - BookrizwanNo ratings yet

- 30 Dec COST SHEET - PGDMDocument15 pages30 Dec COST SHEET - PGDMPoonamNo ratings yet

- Hydrochem AnalysisDocument7 pagesHydrochem AnalysisSaransh Kejriwal100% (2)

- Hydrochem PDFDocument7 pagesHydrochem PDFSaransh KejriwalNo ratings yet

- MANAC Pre MidDocument9 pagesMANAC Pre MidAbhay KaseraNo ratings yet

- BA315 Fme Int 005Document29 pagesBA315 Fme Int 005潘伟杰No ratings yet

- Budgetary ControlDocument14 pagesBudgetary ControlCool BuddyNo ratings yet

- Midterm Winter 2020 SolutionDocument5 pagesMidterm Winter 2020 SolutionAya Ben MohamedNo ratings yet

- Worksheet Campar IndustriesDocument11 pagesWorksheet Campar IndustriesRUPIKA R GNo ratings yet

- Kế toán quản trịDocument88 pagesKế toán quản trịHà Mai VõNo ratings yet

- 2m00154 S.y.b.com - Bms Sem Ivchoice Based 78512 Group A Finance Strategic Cost Management Q.p.code53273Document5 pages2m00154 S.y.b.com - Bms Sem Ivchoice Based 78512 Group A Finance Strategic Cost Management Q.p.code53273Navira MirajkarNo ratings yet

- Budgeting Review QuestionDocument5 pagesBudgeting Review QuestionFrankNo ratings yet

- 132 Saqlain ShaikhDocument10 pages132 Saqlain ShaikhCemon FredNo ratings yet

- 04 Akone Joseph Exercise 04 CostDocument4 pages04 Akone Joseph Exercise 04 Costrita tamohNo ratings yet

- Particulars P1 P2Document4 pagesParticulars P1 P2sanket pareekNo ratings yet

- Trout Inc. Prepared The Following Production Report-Weighted AverageDocument4 pagesTrout Inc. Prepared The Following Production Report-Weighted AverageJalaj GuptaNo ratings yet

- P23-1A 1. Sale Budget Quarter 1 2 TotalDocument7 pagesP23-1A 1. Sale Budget Quarter 1 2 TotalVõ Huỳnh BăngNo ratings yet

- Assignment 2 - CMADocument9 pagesAssignment 2 - CMAVivek SharanNo ratings yet

- 05 Atanga Exercise 05Document8 pages05 Atanga Exercise 05rita tamohNo ratings yet

- Exercice 1 - CorrectionDocument5 pagesExercice 1 - CorrectionFagoul JadNo ratings yet

- Narsee Monjee Institute of Management StudiesDocument8 pagesNarsee Monjee Institute of Management StudiesSHIVANGI AGRAWALNo ratings yet

- 06 Tcheutsoua Marie Christelle Exercise 06Document6 pages06 Tcheutsoua Marie Christelle Exercise 06rita tamohNo ratings yet

- 03 Tadzoa Francis EXO 03 COSTDocument4 pages03 Tadzoa Francis EXO 03 COSTrita tamohNo ratings yet

- Harsh - Electricals - PPTX 2 11Document10 pagesHarsh - Electricals - PPTX 2 11Niya ThomasNo ratings yet

- Gilbert Company-WPS OfficeDocument17 pagesGilbert Company-WPS OfficeTrina Mae Garcia100% (1)

- Salil - Case StudyDocument6 pagesSalil - Case StudySalil DasNo ratings yet

- Shri WCMDocument9 pagesShri WCMIrfan ShaikhNo ratings yet

- Case SolutionsDocument11 pagesCase SolutionsMohit AgrawalNo ratings yet

- Assignment: Table of ContentDocument9 pagesAssignment: Table of ContentAhsanur HossainNo ratings yet

- Revision Class Notes 6 Jun 21Document7 pagesRevision Class Notes 6 Jun 21Rania barabaNo ratings yet

- Round 5 ReprtsDocument29 pagesRound 5 ReprtsrahulNo ratings yet

- CostingDocument46 pagesCostingRaghav KhakholiaNo ratings yet

- MAF Assignment QuestionDocument13 pagesMAF Assignment QuestionKietHuynhNo ratings yet

- 15MBA119 Business PlanDocument6 pages15MBA119 Business PlanhardikgosaiNo ratings yet

- Section - A: Question - 1Document10 pagesSection - A: Question - 1Sameen ShafaatNo ratings yet

- Retain/drop A Segment E12-2Document6 pagesRetain/drop A Segment E12-2Khanh NgocNo ratings yet

- Chapter 6 Short Term BudgetingDocument7 pagesChapter 6 Short Term BudgetingalyNo ratings yet

- Millichem Solution XDocument6 pagesMillichem Solution XMuhammad Junaid100% (1)

- Cost Sheet (Absorption Costing)Document17 pagesCost Sheet (Absorption Costing)Raj singh chouhanNo ratings yet

- Prime Cost 2940000 Conversion Cost Work Cost (Gross) 4140000Document4 pagesPrime Cost 2940000 Conversion Cost Work Cost (Gross) 4140000Shachin ShibiNo ratings yet

- Agamata Chapter 6Document18 pagesAgamata Chapter 6Drama SubsNo ratings yet

- Gloves Price For BuyerDocument4 pagesGloves Price For BuyertopurockNo ratings yet

- Financial Calculation Made by The ClientDocument6 pagesFinancial Calculation Made by The ClientMahnoor RehmanNo ratings yet

- Agamata Chapter 6Document18 pagesAgamata Chapter 6Abigail Faye Roxas100% (1)

- Problem 3 Process Costing AnsDocument2 pagesProblem 3 Process Costing AnsKloie SanoriaNo ratings yet

- Activity 11.6Document4 pagesActivity 11.6scheepersbrNo ratings yet

- Short-Term Budgeting: (Problem 1)Document18 pagesShort-Term Budgeting: (Problem 1)princess bubblegumNo ratings yet

- Ma ExDocument4 pagesMa ExNigussie BerhanuNo ratings yet

- Assignment PDFDocument15 pagesAssignment PDFpavanihirushaNo ratings yet

- Unit 8 - BudgetingDocument8 pagesUnit 8 - Budgetingkevin75108No ratings yet

- PRACTICE-EXERCISES-SOLUTIONS-I_MI1_10.2023Document6 pagesPRACTICE-EXERCISES-SOLUTIONS-I_MI1_10.2023honguyenkimkhanh55No ratings yet

- Add Less Add Add Foh:: Particulars $ $Document18 pagesAdd Less Add Add Foh:: Particulars $ $Saif MughalNo ratings yet

- Romanov MidtermDocument8 pagesRomanov Midterm6ahahahNo ratings yet

- Ch01 Ex AnswersDocument8 pagesCh01 Ex AnswersRana MahmoudNo ratings yet

- PhonePe Statement Nov2023 May2024Document45 pagesPhonePe Statement Nov2023 May2024koshtashubham384No ratings yet

- Mod 1 FullDocument42 pagesMod 1 FullZAIL JEFF ALDEA DALENo ratings yet

- Ashfaq StockDocument13 pagesAshfaq Stockasadjameel3No ratings yet

- JOURNALIZINGDocument19 pagesJOURNALIZINGJINKY TOLENTINONo ratings yet

- ACCT10001 Assignment 1 Submission Sheet Part One 1361206Document8 pagesACCT10001 Assignment 1 Submission Sheet Part One 1361206jiazhuokNo ratings yet

- The Central ArecanutDocument3 pagesThe Central Arecanutyathinkantramajal9284No ratings yet

- Statement 640xxxx0072 23122023 090630Document20 pagesStatement 640xxxx0072 23122023 090630ganeg1242No ratings yet

- A Guide To Investing in Private CapitalDocument14 pagesA Guide To Investing in Private CapitalJulio CardenasNo ratings yet

- Test Bank For Essentials of Corporate Finance 7th Edition by RossDocument36 pagesTest Bank For Essentials of Corporate Finance 7th Edition by Rossstripperinveigle.7m8qg9100% (52)

- Customer Awareness Regarding Systematic Investment PlanDocument37 pagesCustomer Awareness Regarding Systematic Investment PlanRaja kamal ChNo ratings yet

- WCM ProblemsDocument3 pagesWCM ProblemsAreeba ishaqNo ratings yet

- Mco 05Document12 pagesMco 05Nilanjan GhoshNo ratings yet

- Edward Rosario - TransUnion Personal Credit Report - 20180626Document27 pagesEdward Rosario - TransUnion Personal Credit Report - 20180626Pat MalotNo ratings yet

- e-StatementBRImo 206701008089509 Oct2023 20231218 105159Document3 pagese-StatementBRImo 206701008089509 Oct2023 20231218 105159Nicol IrfansyahNo ratings yet

- SIM ACP 323 Week 4 5Document32 pagesSIM ACP 323 Week 4 5Helga MatiasNo ratings yet

- Dividend PolicyDocument8 pagesDividend PolicyShakti RupiniNo ratings yet

- 202 Corporate Accounting SEM III 1 1Document11 pages202 Corporate Accounting SEM III 1 1Ajay KatkeNo ratings yet

- MPS 08012024 134504Document2 pagesMPS 08012024 134504sukhadevramapure786No ratings yet

- Ebook PDF Cornerstones of Financial Accounting 2nd Canadian Edition PDFDocument41 pagesEbook PDF Cornerstones of Financial Accounting 2nd Canadian Edition PDFcathy.mccann98798% (49)

- Finance Report enDocument1 pageFinance Report enPhương Linh VũNo ratings yet

- Test Bank For Advanced Accounting 12th EditionDocument24 pagesTest Bank For Advanced Accounting 12th EditionLauraWilliamsgqis100% (50)

- Financial Statement Analysis As A Tool For Investment Decisions and Assessment of Companies' PerformanceDocument18 pagesFinancial Statement Analysis As A Tool For Investment Decisions and Assessment of Companies' PerformanceCinta Rizkia Zahra LubisNo ratings yet

- Corporate Financing and Planning Course1Document24 pagesCorporate Financing and Planning Course1edoardozanetta99No ratings yet

- Cash Flow StatementDocument5 pagesCash Flow Statementl201046No ratings yet

- 3 ReceivablesDocument13 pages3 Receivablesjoneth.duenasNo ratings yet

- AFAR 2306 - Home Office, Branch & Agency AcctgDocument5 pagesAFAR 2306 - Home Office, Branch & Agency AcctgDzulija TalipanNo ratings yet

- Wa 6Document2 pagesWa 6Muhammad nasirNo ratings yet

- Fsav 6e Test Bank Mod13 TF MC 101520Document9 pagesFsav 6e Test Bank Mod13 TF MC 101520pauline leNo ratings yet

Download as xlsx, pdf, or txt

You might also like

- Universiti Teknologi Mara Final Assessment: Confidential 1 AC/JUL 2022/MAF503Document10 pagesUniversiti Teknologi Mara Final Assessment: Confidential 1 AC/JUL 2022/MAF503Alyn AdnanNo ratings yet

- Harsh Electricals: Analyzing Cost in Search of ProfitDocument11 pagesHarsh Electricals: Analyzing Cost in Search of ProfitSanJana NahataNo ratings yet

- Cma Budget ExcelDocument6 pagesCma Budget ExcelDristi SinghNo ratings yet

- Colin - BookDocument15 pagesColin - BookrizwanNo ratings yet

- 30 Dec COST SHEET - PGDMDocument15 pages30 Dec COST SHEET - PGDMPoonamNo ratings yet

- Hydrochem AnalysisDocument7 pagesHydrochem AnalysisSaransh Kejriwal100% (2)

- Hydrochem PDFDocument7 pagesHydrochem PDFSaransh KejriwalNo ratings yet

- MANAC Pre MidDocument9 pagesMANAC Pre MidAbhay KaseraNo ratings yet

- BA315 Fme Int 005Document29 pagesBA315 Fme Int 005潘伟杰No ratings yet

- Budgetary ControlDocument14 pagesBudgetary ControlCool BuddyNo ratings yet

- Midterm Winter 2020 SolutionDocument5 pagesMidterm Winter 2020 SolutionAya Ben MohamedNo ratings yet

- Worksheet Campar IndustriesDocument11 pagesWorksheet Campar IndustriesRUPIKA R GNo ratings yet

- Kế toán quản trịDocument88 pagesKế toán quản trịHà Mai VõNo ratings yet

- 2m00154 S.y.b.com - Bms Sem Ivchoice Based 78512 Group A Finance Strategic Cost Management Q.p.code53273Document5 pages2m00154 S.y.b.com - Bms Sem Ivchoice Based 78512 Group A Finance Strategic Cost Management Q.p.code53273Navira MirajkarNo ratings yet

- Budgeting Review QuestionDocument5 pagesBudgeting Review QuestionFrankNo ratings yet

- 132 Saqlain ShaikhDocument10 pages132 Saqlain ShaikhCemon FredNo ratings yet

- 04 Akone Joseph Exercise 04 CostDocument4 pages04 Akone Joseph Exercise 04 Costrita tamohNo ratings yet

- Particulars P1 P2Document4 pagesParticulars P1 P2sanket pareekNo ratings yet

- Trout Inc. Prepared The Following Production Report-Weighted AverageDocument4 pagesTrout Inc. Prepared The Following Production Report-Weighted AverageJalaj GuptaNo ratings yet

- P23-1A 1. Sale Budget Quarter 1 2 TotalDocument7 pagesP23-1A 1. Sale Budget Quarter 1 2 TotalVõ Huỳnh BăngNo ratings yet

- Assignment 2 - CMADocument9 pagesAssignment 2 - CMAVivek SharanNo ratings yet

- 05 Atanga Exercise 05Document8 pages05 Atanga Exercise 05rita tamohNo ratings yet

- Exercice 1 - CorrectionDocument5 pagesExercice 1 - CorrectionFagoul JadNo ratings yet

- Narsee Monjee Institute of Management StudiesDocument8 pagesNarsee Monjee Institute of Management StudiesSHIVANGI AGRAWALNo ratings yet

- 06 Tcheutsoua Marie Christelle Exercise 06Document6 pages06 Tcheutsoua Marie Christelle Exercise 06rita tamohNo ratings yet

- 03 Tadzoa Francis EXO 03 COSTDocument4 pages03 Tadzoa Francis EXO 03 COSTrita tamohNo ratings yet

- Harsh - Electricals - PPTX 2 11Document10 pagesHarsh - Electricals - PPTX 2 11Niya ThomasNo ratings yet

- Gilbert Company-WPS OfficeDocument17 pagesGilbert Company-WPS OfficeTrina Mae Garcia100% (1)

- Salil - Case StudyDocument6 pagesSalil - Case StudySalil DasNo ratings yet

- Shri WCMDocument9 pagesShri WCMIrfan ShaikhNo ratings yet

- Case SolutionsDocument11 pagesCase SolutionsMohit AgrawalNo ratings yet

- Assignment: Table of ContentDocument9 pagesAssignment: Table of ContentAhsanur HossainNo ratings yet

- Revision Class Notes 6 Jun 21Document7 pagesRevision Class Notes 6 Jun 21Rania barabaNo ratings yet

- Round 5 ReprtsDocument29 pagesRound 5 ReprtsrahulNo ratings yet

- CostingDocument46 pagesCostingRaghav KhakholiaNo ratings yet

- MAF Assignment QuestionDocument13 pagesMAF Assignment QuestionKietHuynhNo ratings yet

- 15MBA119 Business PlanDocument6 pages15MBA119 Business PlanhardikgosaiNo ratings yet

- Section - A: Question - 1Document10 pagesSection - A: Question - 1Sameen ShafaatNo ratings yet

- Retain/drop A Segment E12-2Document6 pagesRetain/drop A Segment E12-2Khanh NgocNo ratings yet

- Chapter 6 Short Term BudgetingDocument7 pagesChapter 6 Short Term BudgetingalyNo ratings yet

- Millichem Solution XDocument6 pagesMillichem Solution XMuhammad Junaid100% (1)

- Cost Sheet (Absorption Costing)Document17 pagesCost Sheet (Absorption Costing)Raj singh chouhanNo ratings yet

- Prime Cost 2940000 Conversion Cost Work Cost (Gross) 4140000Document4 pagesPrime Cost 2940000 Conversion Cost Work Cost (Gross) 4140000Shachin ShibiNo ratings yet

- Agamata Chapter 6Document18 pagesAgamata Chapter 6Drama SubsNo ratings yet

- Gloves Price For BuyerDocument4 pagesGloves Price For BuyertopurockNo ratings yet

- Financial Calculation Made by The ClientDocument6 pagesFinancial Calculation Made by The ClientMahnoor RehmanNo ratings yet

- Agamata Chapter 6Document18 pagesAgamata Chapter 6Abigail Faye Roxas100% (1)

- Problem 3 Process Costing AnsDocument2 pagesProblem 3 Process Costing AnsKloie SanoriaNo ratings yet

- Activity 11.6Document4 pagesActivity 11.6scheepersbrNo ratings yet

- Short-Term Budgeting: (Problem 1)Document18 pagesShort-Term Budgeting: (Problem 1)princess bubblegumNo ratings yet

- Ma ExDocument4 pagesMa ExNigussie BerhanuNo ratings yet

- Assignment PDFDocument15 pagesAssignment PDFpavanihirushaNo ratings yet

- Unit 8 - BudgetingDocument8 pagesUnit 8 - Budgetingkevin75108No ratings yet

- PRACTICE-EXERCISES-SOLUTIONS-I_MI1_10.2023Document6 pagesPRACTICE-EXERCISES-SOLUTIONS-I_MI1_10.2023honguyenkimkhanh55No ratings yet

- Add Less Add Add Foh:: Particulars $ $Document18 pagesAdd Less Add Add Foh:: Particulars $ $Saif MughalNo ratings yet

- Romanov MidtermDocument8 pagesRomanov Midterm6ahahahNo ratings yet

- Ch01 Ex AnswersDocument8 pagesCh01 Ex AnswersRana MahmoudNo ratings yet

- PhonePe Statement Nov2023 May2024Document45 pagesPhonePe Statement Nov2023 May2024koshtashubham384No ratings yet

- Mod 1 FullDocument42 pagesMod 1 FullZAIL JEFF ALDEA DALENo ratings yet

- Ashfaq StockDocument13 pagesAshfaq Stockasadjameel3No ratings yet

- JOURNALIZINGDocument19 pagesJOURNALIZINGJINKY TOLENTINONo ratings yet

- ACCT10001 Assignment 1 Submission Sheet Part One 1361206Document8 pagesACCT10001 Assignment 1 Submission Sheet Part One 1361206jiazhuokNo ratings yet

- The Central ArecanutDocument3 pagesThe Central Arecanutyathinkantramajal9284No ratings yet

- Statement 640xxxx0072 23122023 090630Document20 pagesStatement 640xxxx0072 23122023 090630ganeg1242No ratings yet

- A Guide To Investing in Private CapitalDocument14 pagesA Guide To Investing in Private CapitalJulio CardenasNo ratings yet

- Test Bank For Essentials of Corporate Finance 7th Edition by RossDocument36 pagesTest Bank For Essentials of Corporate Finance 7th Edition by Rossstripperinveigle.7m8qg9100% (52)

- Customer Awareness Regarding Systematic Investment PlanDocument37 pagesCustomer Awareness Regarding Systematic Investment PlanRaja kamal ChNo ratings yet

- WCM ProblemsDocument3 pagesWCM ProblemsAreeba ishaqNo ratings yet

- Mco 05Document12 pagesMco 05Nilanjan GhoshNo ratings yet

- Edward Rosario - TransUnion Personal Credit Report - 20180626Document27 pagesEdward Rosario - TransUnion Personal Credit Report - 20180626Pat MalotNo ratings yet

- e-StatementBRImo 206701008089509 Oct2023 20231218 105159Document3 pagese-StatementBRImo 206701008089509 Oct2023 20231218 105159Nicol IrfansyahNo ratings yet

- SIM ACP 323 Week 4 5Document32 pagesSIM ACP 323 Week 4 5Helga MatiasNo ratings yet

- Dividend PolicyDocument8 pagesDividend PolicyShakti RupiniNo ratings yet

- 202 Corporate Accounting SEM III 1 1Document11 pages202 Corporate Accounting SEM III 1 1Ajay KatkeNo ratings yet

- MPS 08012024 134504Document2 pagesMPS 08012024 134504sukhadevramapure786No ratings yet

- Ebook PDF Cornerstones of Financial Accounting 2nd Canadian Edition PDFDocument41 pagesEbook PDF Cornerstones of Financial Accounting 2nd Canadian Edition PDFcathy.mccann98798% (49)

- Finance Report enDocument1 pageFinance Report enPhương Linh VũNo ratings yet

- Test Bank For Advanced Accounting 12th EditionDocument24 pagesTest Bank For Advanced Accounting 12th EditionLauraWilliamsgqis100% (50)

- Financial Statement Analysis As A Tool For Investment Decisions and Assessment of Companies' PerformanceDocument18 pagesFinancial Statement Analysis As A Tool For Investment Decisions and Assessment of Companies' PerformanceCinta Rizkia Zahra LubisNo ratings yet

- Corporate Financing and Planning Course1Document24 pagesCorporate Financing and Planning Course1edoardozanetta99No ratings yet

- Cash Flow StatementDocument5 pagesCash Flow Statementl201046No ratings yet

- 3 ReceivablesDocument13 pages3 Receivablesjoneth.duenasNo ratings yet

- AFAR 2306 - Home Office, Branch & Agency AcctgDocument5 pagesAFAR 2306 - Home Office, Branch & Agency AcctgDzulija TalipanNo ratings yet

- Wa 6Document2 pagesWa 6Muhammad nasirNo ratings yet

- Fsav 6e Test Bank Mod13 TF MC 101520Document9 pagesFsav 6e Test Bank Mod13 TF MC 101520pauline leNo ratings yet