Download as pdf or txt

You might also like

- Test Bank Chapter 11Document25 pagesTest Bank Chapter 11leelee0302No ratings yet

- The BettyDocument6 pagesThe Bettymcurel100% (5)

- Unit 5 Centre-State Financial Relations-I1: StructureDocument15 pagesUnit 5 Centre-State Financial Relations-I1: StructureAjay PrakashNo ratings yet

- Centre - State RelationDocument15 pagesCentre - State RelationGopal AeroNo ratings yet

- Unit 5Document15 pagesUnit 5msenthil862706No ratings yet

- Centre State RelationsDocument13 pagesCentre State RelationsBasil JohnNo ratings yet

- Centre State RelationsDocument20 pagesCentre State RelationsRanaRanveerNo ratings yet

- Inter State RelationsDocument4 pagesInter State RelationsMapuii FanaiNo ratings yet

- An Atheist Manifesto - Lewis, JosephDocument41 pagesAn Atheist Manifesto - Lewis, JosephJithin RajNo ratings yet

- Financial Relations Between Centre and State in The Light of ConstitutionDocument11 pagesFinancial Relations Between Centre and State in The Light of Constitutionतेजस्विनी रंजनNo ratings yet

- Financial Relationship Between Union and StateDocument4 pagesFinancial Relationship Between Union and StateABHISHEK SAADNo ratings yet

- Critical Analysis Including Suggestions For ImprovementDocument4 pagesCritical Analysis Including Suggestions For ImprovementAditya DeshmukhNo ratings yet

- Budget 3Document11 pagesBudget 3तेजस्विनी रंजनNo ratings yet

- Barrowing Power of The UnionDocument15 pagesBarrowing Power of The UnionRohit KumarNo ratings yet

- Finance Commission: Summary SheetDocument14 pagesFinance Commission: Summary SheetjashuramuNo ratings yet

- W13T2 State Finance CommissionDocument10 pagesW13T2 State Finance CommissionSantosh Kumar AgastiNo ratings yet

- Dr. Ram Manohar Lohiya National Law University: Economics Project ON Financial Realtions Between Centre and StatesDocument21 pagesDr. Ram Manohar Lohiya National Law University: Economics Project ON Financial Realtions Between Centre and StatestrivendradonNo ratings yet

- Test 11 - Indian Polity - III - Answer Key-Final-10.01.2018Document18 pagesTest 11 - Indian Polity - III - Answer Key-Final-10.01.2018sachinstinNo ratings yet

- Financial Relation Between Centre and StateDocument4 pagesFinancial Relation Between Centre and StateGhazala ShaheenNo ratings yet

- Centre State Inter State Relationship 96Document13 pagesCentre State Inter State Relationship 96ravi kumarNo ratings yet

- Financial Relations Between Centre and State Art 268 To 293Document3 pagesFinancial Relations Between Centre and State Art 268 To 293Narendra GNo ratings yet

- Centre State RelationsDocument3 pagesCentre State RelationsGargi SinhaNo ratings yet

- Ignou Fiscal Federalism 1Document16 pagesIgnou Fiscal Federalism 1luvlickNo ratings yet

- Distribution of Legislative Powers WRT Doctrine of Pith and SubstanceDocument37 pagesDistribution of Legislative Powers WRT Doctrine of Pith and SubstanceSaravna Vasanta100% (1)

- Federal and Fedral Features of Indian ConstitutionDocument7 pagesFederal and Fedral Features of Indian Constitutionurvi solankiNo ratings yet

- Allocation and Share of RSS P-IIDocument18 pagesAllocation and Share of RSS P-IIBharti dubeNo ratings yet

- Essay On The Financial Relationship Between Centre and State - OdtDocument5 pagesEssay On The Financial Relationship Between Centre and State - OdtchanshrNo ratings yet

- L10 Federalism MC Prelims 2024 Lyst2920Document8 pagesL10 Federalism MC Prelims 2024 Lyst2920jankitkhareNo ratings yet

- Fiscal FederalismDocument25 pagesFiscal FederalismAastha AgnihotriNo ratings yet

- Principles of Financial AdministrationDocument301 pagesPrinciples of Financial Administrationahmednor2012No ratings yet

- Centre State RelationsDocument33 pagesCentre State RelationsBadal PanyNo ratings yet

- State Government and AdministrationDocument9 pagesState Government and AdministrationPrasad AkkNo ratings yet

- 3 FINANCIAL SYSTEMS PROCEDURES Sept 2016-1Document60 pages3 FINANCIAL SYSTEMS PROCEDURES Sept 2016-1eduNo ratings yet

- L20 Crux F Center State Disputes 2 1668525005Document11 pagesL20 Crux F Center State Disputes 2 1668525005kunalNo ratings yet

- Federalism (Book-1) Class 11 P.SCDocument3 pagesFederalism (Book-1) Class 11 P.SCNaresh KumarNo ratings yet

- Ci - Unit 2 - Topic 2 - FederalismDocument33 pagesCi - Unit 2 - Topic 2 - FederalismArshia JainNo ratings yet

- 7 FederalismDocument5 pages7 Federalismgokool281378No ratings yet

- The Finance CommissionDocument18 pagesThe Finance CommissionKrishna SankarNo ratings yet

- COI - Module - 5Document42 pagesCOI - Module - 5memeemNo ratings yet

- Module VDocument11 pagesModule VSafalNo ratings yet

- Centre State RelationDocument12 pagesCentre State RelationVasanth Subramanyam100% (1)

- Administrative RelationDocument14 pagesAdministrative RelationSitansi MohantyNo ratings yet

- Constitution II - Centre State Relations AnalysisDocument16 pagesConstitution II - Centre State Relations AnalysisKhushi KothariNo ratings yet

- Center State Financial RelationsDocument15 pagesCenter State Financial RelationsAadi saklechaNo ratings yet

- Distrubution of Financial Powers in India ConstitutionDocument6 pagesDistrubution of Financial Powers in India Constitutionsindhuja singhNo ratings yet

- Centre State Relations Legislative Administrative Financial Aspects Issues During Covid 19 D3e1feb6Document9 pagesCentre State Relations Legislative Administrative Financial Aspects Issues During Covid 19 D3e1feb6Yuseer AmanNo ratings yet

- Centre State RelationsDocument9 pagesCentre State RelationsBuNo ratings yet

- Constitutional Provisions Relating To TaxDocument9 pagesConstitutional Provisions Relating To Taxrakshitha9reddy-1No ratings yet

- Centre State RelationDocument12 pagesCentre State RelationShivam Gupta33% (3)

- Civics, L-2, FederalismDocument13 pagesCivics, L-2, FederalismKrish JainNo ratings yet

- Distribution of Tax RevenuesDocument9 pagesDistribution of Tax RevenuesSahajPuriNo ratings yet

- Constitutional Provisions On BudgetingDocument6 pagesConstitutional Provisions On BudgetingJohn Dx LapidNo ratings yet

- Public Sector Accounting APS 20103 Financial Accounting Systems and ProceduresDocument26 pagesPublic Sector Accounting APS 20103 Financial Accounting Systems and ProceduresAsheequin ZainolNo ratings yet

- Evolution and Development of DecentralizationDocument13 pagesEvolution and Development of DecentralizationVikas JadhavNo ratings yet

- Finance Finance Commission For Rbi Grade B and Sebi Grade A 2019Document12 pagesFinance Finance Commission For Rbi Grade B and Sebi Grade A 2019JJ KNo ratings yet

- INdian Fiscal FederalismDocument21 pagesINdian Fiscal Federalismchoudhary2k8No ratings yet

- The Financial Relation Between The Union and The States in IndiaDocument11 pagesThe Financial Relation Between The Union and The States in IndiaHarsh ShahNo ratings yet

- Centre State Financial RelationsDocument6 pagesCentre State Financial Relationsrashitekwani5No ratings yet

- Tanya SinghDocument23 pagesTanya SinghTanya SinghNo ratings yet

- Cause 03082023Document639 pagesCause 03082023Arun ANNo ratings yet

- Cause 02082023Document657 pagesCause 02082023Arun ANNo ratings yet

- Cause 27072023Document646 pagesCause 27072023Arun ANNo ratings yet

- Unit 333Document16 pagesUnit 333Arun ANNo ratings yet

- Hostile WitnessDocument7 pagesHostile WitnessArun ANNo ratings yet

- Compliance Checklist - HSE-OH-ST07 Cont Welfare MGMTDocument5 pagesCompliance Checklist - HSE-OH-ST07 Cont Welfare MGMTjerinNo ratings yet

- Liwanag Vs CA Case DigestDocument1 pageLiwanag Vs CA Case DigestVanityHughNo ratings yet

- Financial Management Research Paper Financial Ratios of BritanniaDocument15 pagesFinancial Management Research Paper Financial Ratios of BritanniaShaik Noor Mohammed Ali Jinnah 19DBLAW036No ratings yet

- SculptureDocument59 pagesSculptureJulia Stefanel PerezNo ratings yet

- Uuwi Na Si Udong, Buto't Balat Film AnalysisDocument2 pagesUuwi Na Si Udong, Buto't Balat Film AnalysisJOHN MEGGY SALINASNo ratings yet

- (Write Up) Dear Jesus Album SoundclickDocument2 pages(Write Up) Dear Jesus Album Soundclickapi-3759571No ratings yet

- Bertolt Brecht - WikipediaDocument144 pagesBertolt Brecht - WikipediaJulietteNo ratings yet

- Pros and Cons of Tourism DevelopmentDocument4 pagesPros and Cons of Tourism DevelopmentMusicalNoteNo ratings yet

- 8D Reported QuestionsDocument2 pages8D Reported QuestionsFOR AKKNo ratings yet

- Sigmund Freud: Psychosexual DevelopmentDocument6 pagesSigmund Freud: Psychosexual DevelopmentKarlo Gil ConcepcionNo ratings yet

- A Poison TreeDocument2 pagesA Poison Treedean deanNo ratings yet

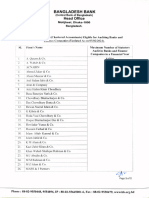

- List of Audit Firms 2024Document2 pagesList of Audit Firms 2024ahibadhaka2020No ratings yet

- SR. NO. Capacity/Descirption of Machine Client: A.C. Generator StatorsDocument5 pagesSR. NO. Capacity/Descirption of Machine Client: A.C. Generator Statorsmtj4uNo ratings yet

- 30 2002 Revenue - Regulations - Implementing - Sections20181220 5466 Ew6q98Document6 pages30 2002 Revenue - Regulations - Implementing - Sections20181220 5466 Ew6q98Milane Anne CunananNo ratings yet

- Battle of Badr - Assignment 1Document3 pagesBattle of Badr - Assignment 1Runa KasiNo ratings yet

- RRB Je Classification + Home WorkDocument46 pagesRRB Je Classification + Home WorkArun KumarNo ratings yet

- LIT 1 EssentialsDocument1 pageLIT 1 Essentialsque zomeNo ratings yet

- Retail Location TheoriesDocument24 pagesRetail Location Theoriesdhruvbarman1100% (1)

- CT PatDocument67 pagesCT Patshadow shadowNo ratings yet

- Themes in Information System DevelopmentDocument14 pagesThemes in Information System DevelopmentMuhammad BilalNo ratings yet

- Vienna Declaration 2022Document6 pagesVienna Declaration 2022Jose Alfredo CedilloNo ratings yet

- Salus Populi Suprema Lex EstoDocument2 pagesSalus Populi Suprema Lex EstoSaad Ahmed100% (3)

- What Are The Different Types of Stocks Available in The Market?Document5 pagesWhat Are The Different Types of Stocks Available in The Market?rachit2383No ratings yet

- Pint and Focused InquiryDocument5 pagesPint and Focused Inquiryjacintocolmenarez7582No ratings yet

- Address Proof Electricity Bill - Jul'21Document2 pagesAddress Proof Electricity Bill - Jul'21Loan LoanNo ratings yet

- Iroquois ConfederacyDocument12 pagesIroquois ConfederacyrideauparkNo ratings yet

- Afi21 103Document123 pagesAfi21 103Rick BradyNo ratings yet

- Governments Should Spend Money On Railways Rather Than RoadsDocument2 pagesGovernments Should Spend Money On Railways Rather Than RoadsHadil Altilbani100% (2)

- M - CV FDocument2 pagesM - CV FYogendra Prawin KumarNo ratings yet