Download as pdf or txt

You might also like

- Statement of AdviceDocument23 pagesStatement of AdvicePeter Proksch100% (7)

- Tata Aia Life InsuranceDocument2 pagesTata Aia Life InsurancekotijbNo ratings yet

- OfferletterDocument3 pagesOfferletterAjay Pandey75% (4)

- PP V ManimaranDocument16 pagesPP V ManimaranDheebak Kumaran100% (1)

- Planas vs. ComelecDocument15 pagesPlanas vs. ComelecNxxxNo ratings yet

- Law's Meaning of Life by Ngaire NaffineDocument225 pagesLaw's Meaning of Life by Ngaire NaffineBenjamin Chong100% (1)

- Consumer Credit Insurance: Proposal and Policy ScheduleDocument14 pagesConsumer Credit Insurance: Proposal and Policy ScheduleFaizan FarasatNo ratings yet

- TATA Premium ReceiptDocument1 pageTATA Premium Receiptthetrilight2023No ratings yet

- TATA Premium ReceiptDocument1 pageTATA Premium ReceiptkabuldasNo ratings yet

- Moriarty SFSGDocument1 pageMoriarty SFSGRaul KarkyNo ratings yet

- Mediclaim PolicyDocument2 pagesMediclaim PolicyVikrant AggarwalNo ratings yet

- C320284551-Renewal Premium ReceiptDocument1 pageC320284551-Renewal Premium ReceiptThelu RajuNo ratings yet

- Term Insurance Policy. - CompressedDocument30 pagesTerm Insurance Policy. - Compressedsourabh.khattarNo ratings yet

- Shine Financial Services FSG v3Document9 pagesShine Financial Services FSG v3api-202026441No ratings yet

- Immed 0000 91742569 113978595 20240314Document12 pagesImmed 0000 91742569 113978595 20240314gxawenitulaniNo ratings yet

- Anti Bribery and Anti Corruption Policy - IndiaDocument7 pagesAnti Bribery and Anti Corruption Policy - Indianaveen kumarNo ratings yet

- Group Mediprime Certificate of Insurance: 380-Bsa-Dn188271Document4 pagesGroup Mediprime Certificate of Insurance: 380-Bsa-Dn188271Sangwan ParveshNo ratings yet

- Get IllustrateDocument18 pagesGet IllustrateHitoshi KatoNo ratings yet

- Appraisal LetterDocument7 pagesAppraisal Letterchiraggangwar0007No ratings yet

- Temp20151116092145 PDFDocument66 pagesTemp20151116092145 PDFketian15No ratings yet

- Twenty Six Thousand One Hundred and Twenty Five: A Reliance Capital CompanyDocument1 pageTwenty Six Thousand One Hundred and Twenty Five: A Reliance Capital CompanyDilip UpadhyayNo ratings yet

- Count FSG Jan2020Document10 pagesCount FSG Jan2020mybaggageNo ratings yet

- KOCHI 2/2XYE211550 DHL: Page 1 of 140 Policy No. 2X785169310Document140 pagesKOCHI 2/2XYE211550 DHL: Page 1 of 140 Policy No. 2X785169310Kiran JohnNo ratings yet

- 681 Termination RequestDocument1 page681 Termination RequestDanielNo ratings yet

- Welcome To The World of Aditya Birla Capital!: Mobile NoDocument33 pagesWelcome To The World of Aditya Birla Capital!: Mobile NokumarpramodNo ratings yet

- Broker Appointment (Ita)Document1 pageBroker Appointment (Ita)waynesastarNo ratings yet

- Welcome To The World of Aditya Birla Capital!: Mobile NoDocument39 pagesWelcome To The World of Aditya Birla Capital!: Mobile Nom00162372No ratings yet

- Renewal of Your Optima Restore Floater Insurance PolicyDocument13 pagesRenewal of Your Optima Restore Floater Insurance Policysiddharth.bangani4294No ratings yet

- C301149660-Renewal Premium ReceiptDocument1 pageC301149660-Renewal Premium ReceiptsaivenkateswarNo ratings yet

- Smart Wealth Builder Policy Document Form 17Document29 pagesSmart Wealth Builder Policy Document Form 17Chetanshi Nene100% (1)

- Wa0005.Document37 pagesWa0005.Sumeet AgarwalNo ratings yet

- Policy Schedule - WongaDocument17 pagesPolicy Schedule - Wongawondersipho530No ratings yet

- Trilogy Monthly Income Trust PDS 22 July 2015 WEBDocument56 pagesTrilogy Monthly Income Trust PDS 22 July 2015 WEBRoger AllanNo ratings yet

- SIS 2023 11 15 Client Advice RecordDocument6 pagesSIS 2023 11 15 Client Advice Recordnerina.dejager01No ratings yet

- Premarket KnowledgeBrunch Microsec 30.11.16Document5 pagesPremarket KnowledgeBrunch Microsec 30.11.16Rajasekhar Reddy AnekalluNo ratings yet

- PLA Anti Bribery and Corruption Policy (17 Dec 13)Document8 pagesPLA Anti Bribery and Corruption Policy (17 Dec 13)CinCan Poenya PiePieNo ratings yet

- JB503916 Bab2c NB 00 20201209164847 1Document10 pagesJB503916 Bab2c NB 00 20201209164847 1SatishSubramanianNo ratings yet

- Anusha AervaDocument2 pagesAnusha Aervamrcopy xeroxNo ratings yet

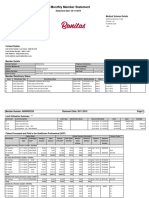

- Member Statement 46900002234Document5 pagesMember Statement 46900002234Charles MutetwaNo ratings yet

- Insurance CoverageDocument50 pagesInsurance Coverage7dwg75s8mgNo ratings yet

- Bonus Notice: Participating Sub-Fund Regular Premium Life Sub-FundDocument2 pagesBonus Notice: Participating Sub-Fund Regular Premium Life Sub-Fundgunat dhanapalNo ratings yet

- Policy Pack - Inward Doc. - 00764794Document22 pagesPolicy Pack - Inward Doc. - 00764794ankur.rdsoNo ratings yet

- Bsa FSGDocument15 pagesBsa FSGtroy.hancoxNo ratings yet

- Intermediary Code CO0000000062 Akshaya Wealth Management PVT - LTD Phone No 080-26535701/02/8026535701 E-Mail Id Services@AkshayaweaDocument4 pagesIntermediary Code CO0000000062 Akshaya Wealth Management PVT - LTD Phone No 080-26535701/02/8026535701 E-Mail Id Services@Akshayaweapushpkant kumarNo ratings yet

- PLAI Company Profile 2024Document11 pagesPLAI Company Profile 2024dizaNo ratings yet

- Volunteer - Anti-Bribery and Corruption Policy V4.0Document5 pagesVolunteer - Anti-Bribery and Corruption Policy V4.0sinongNo ratings yet

- Epolicy - 1022684495Document61 pagesEpolicy - 1022684495Kurt MarfilNo ratings yet

- Extended Manufacturer Warranty Insurance: Proposal & Policy ScheduleDocument21 pagesExtended Manufacturer Warranty Insurance: Proposal & Policy ScheduleFaizan FarasatNo ratings yet

- Amol Kalgonda PatilDocument8 pagesAmol Kalgonda Patilinnovatorsindia91No ratings yet

- Assignment of Policy Form For Corporate PolicyownerDocument3 pagesAssignment of Policy Form For Corporate PolicyownerjedNo ratings yet

- Welcome LetterDocument3 pagesWelcome Letterkhanyadlangalala1507No ratings yet

- 101 Math Short Cuts (WWW - Qmaths.in)Document1 page101 Math Short Cuts (WWW - Qmaths.in)moin khanNo ratings yet

- VishalDocument0 pagesVishalVishal AggawalNo ratings yet

- 18-Oct-2014 MR VVN Murthy Door No 7-75 4Th Mile Nuvalakula Gardens Nellore 524002 Andhrapradesh India Mob No-9966802424 Ph. No-0 Home No - 0Document34 pages18-Oct-2014 MR VVN Murthy Door No 7-75 4Th Mile Nuvalakula Gardens Nellore 524002 Andhrapradesh India Mob No-9966802424 Ph. No-0 Home No - 0Murthy VvnNo ratings yet

- Mots WN 141828420 MDocument18 pagesMots WN 141828420 Mosaelectrical3No ratings yet

- Self Helath Insurance 80D 25000Document1 pageSelf Helath Insurance 80D 25000Santosh Deepak DasariNo ratings yet

- Budget Insurance POLICY NUMBER 778754485Document13 pagesBudget Insurance POLICY NUMBER 778754485suzan moeketsiNo ratings yet

- Preview PDFDocument74 pagesPreview PDFShahrizal Abd MalekNo ratings yet

- IDirect BhartiAirtel QC Mar16Document2 pagesIDirect BhartiAirtel QC Mar16arun_algoNo ratings yet

- CO - Surrender or Cancellation of Policy (PPD-08-SURCAN-09-2018v1)Document3 pagesCO - Surrender or Cancellation of Policy (PPD-08-SURCAN-09-2018v1)umairahNo ratings yet

- Securing Your Superannuation Future: How to Start and Run a Self Managed Super FundFrom EverandSecuring Your Superannuation Future: How to Start and Run a Self Managed Super FundNo ratings yet

- Tutorial 1 - Review of ThermodynamicsDocument2 pagesTutorial 1 - Review of ThermodynamicsAdruNo ratings yet

- RA 9717 University CodeDocument10 pagesRA 9717 University CodeKristine CaceresNo ratings yet

- Harden vs. Dir. of Prisons & 7. People vs. DionisioDocument10 pagesHarden vs. Dir. of Prisons & 7. People vs. Dionisiojan lorenzoNo ratings yet

- ADMINISTRATIVE ORDERS Environmental Code La TrinidadDocument12 pagesADMINISTRATIVE ORDERS Environmental Code La TrinidadAlraji rasumanNo ratings yet

- Petitioner vs. vs. Respondents: First DivisionDocument9 pagesPetitioner vs. vs. Respondents: First DivisionVia Rhidda ImperialNo ratings yet

- De Gala Vs Gonzales Compared From Garcia Vs LacuestaDocument10 pagesDe Gala Vs Gonzales Compared From Garcia Vs LacuestaGerald GarcianoNo ratings yet

- CHG MLDocument16 pagesCHG MLKirti GuptaNo ratings yet

- CC Property Transfers 5-12 To 5-23Document2 pagesCC Property Transfers 5-12 To 5-23augustapressNo ratings yet

- Indian Contract Act, 1872 Case Studies On Minor's Agreement: Question No.1Document3 pagesIndian Contract Act, 1872 Case Studies On Minor's Agreement: Question No.1SaloniNo ratings yet

- Torts Digests Beda AlabangDocument3 pagesTorts Digests Beda AlabangLhexor Diapera DobleNo ratings yet

- Tutorial Exercises Logic SolutionsDocument44 pagesTutorial Exercises Logic SolutionsDesmond KcNo ratings yet

- L/Epubltc Tue Lluiltpptnes: QcourtDocument11 pagesL/Epubltc Tue Lluiltpptnes: QcourtThe Supreme Court Public Information OfficeNo ratings yet

- Chapter III: Child in Need of Care and Protection 29. Child Welfare Committee.Document6 pagesChapter III: Child in Need of Care and Protection 29. Child Welfare Committee.monika singhNo ratings yet

- Bangalisan Vs CA Et Al GR No. 124678Document8 pagesBangalisan Vs CA Et Al GR No. 124678John PrimerNo ratings yet

- Legislative Subpoena HomeAway, Inc. 06-06-17Document5 pagesLegislative Subpoena HomeAway, Inc. 06-06-17L. A. PatersonNo ratings yet

- Offer - Letter - RUDRA PRASAD NAHAKDocument6 pagesOffer - Letter - RUDRA PRASAD NAHAKRudra prasad NahakNo ratings yet

- AssignmentsDocument32 pagesAssignmentsNingClaudioNo ratings yet

- ImportantsDocument1 pageImportantsAngelyn C. DazoNo ratings yet

- Henry VIII SummaryDocument6 pagesHenry VIII Summarymoro206hNo ratings yet

- Illegal Elephant Hunting Case 1 18 CR 00238 PABDocument19 pagesIllegal Elephant Hunting Case 1 18 CR 00238 PABJeanLotusNo ratings yet

- Church Quiet TitleDocument119 pagesChurch Quiet Titlejerry mcleodNo ratings yet

- The Legal Framework Issues of PMSC: Indonesian PracticeDocument32 pagesThe Legal Framework Issues of PMSC: Indonesian PracticeMuhammad ArifinNo ratings yet

- International Conflict and Security Law: A Research HandbookDocument1,488 pagesInternational Conflict and Security Law: A Research HandbookOgi NugrahaNo ratings yet

- Ex Post Facto LawsDocument2 pagesEx Post Facto LawsChocolatecham Burstwithsweetness100% (2)

- Cress #179836 v. Palmer - Document No. 4Document14 pagesCress #179836 v. Palmer - Document No. 4Justia.comNo ratings yet

- GensanDocument4 pagesGensanKimiko SyNo ratings yet

- Kelsen - Law As Specific Social Technique PDFDocument24 pagesKelsen - Law As Specific Social Technique PDFcorky01No ratings yet