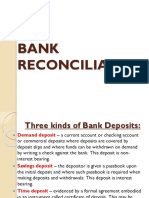

Bank Recon-Tion Statement

Bank Recon-Tion Statement

You might also like

- 1G2 - Outbound Processing For Customer - WMDocument12 pages1G2 - Outbound Processing For Customer - WMsserpsap100% (1)

- BRS Full ChapterDocument16 pagesBRS Full ChapterMumtazAhmad100% (1)

- Monopoly ProjectDocument13 pagesMonopoly Projectapi-311197959No ratings yet

- Risk Management in Banking Sector MainDocument54 pagesRisk Management in Banking Sector MainJahanvi Bansal55% (11)

- Xerox-Case Study Analysi-JhellDocument10 pagesXerox-Case Study Analysi-Jhelljhell de la cruzNo ratings yet

- MODULE 3 - Part 3 Bank ReconciliationDocument16 pagesMODULE 3 - Part 3 Bank ReconciliationShaena Mae50% (2)

- Bank Reconciliation - For LectureDocument3 pagesBank Reconciliation - For LectureCharlene Jane EspinoNo ratings yet

- Hsslive-Chapter 5 BRS 1 PDFDocument2 pagesHsslive-Chapter 5 BRS 1 PDFRam IyerNo ratings yet

- Fundamentas of Accounting I CH 5Document24 pagesFundamentas of Accounting I CH 5israelbedasa3100% (1)

- Bank ReconciliationDocument12 pagesBank ReconciliationJenny Pearl Dominguez CalizarNo ratings yet

- Chapter 2 Bank Reconciliation (Gatdc)Document20 pagesChapter 2 Bank Reconciliation (Gatdc)Joan LeonorNo ratings yet

- Assignment 1571213669 SmsDocument13 pagesAssignment 1571213669 SmsJayasuriya SNo ratings yet

- Bank Reconciliation StatementDocument27 pagesBank Reconciliation Statementkimuli FreddieNo ratings yet

- Intermidiate FA I ChapterDocument28 pagesIntermidiate FA I Chapteryiberta69No ratings yet

- Group - 11 Bank Reconciliation Statement: CIA (Continuous Internal Assessment) 1Document13 pagesGroup - 11 Bank Reconciliation Statement: CIA (Continuous Internal Assessment) 1shriyanshu padhiNo ratings yet

- Chapter 5 - Bank Reconciliation StatementDocument23 pagesChapter 5 - Bank Reconciliation StatementNchumthung JamiNo ratings yet

- Midterm The Banks Functional DepartmentsDocument49 pagesMidterm The Banks Functional DepartmentsB-jay AledonNo ratings yet

- 6 - Bank Reconciliation StatementDocument3 pages6 - Bank Reconciliation StatementNeeraj RaikwarNo ratings yet

- Learning Activity Sheet No. 16 2 Quarter: Grade Level/ Subject Grade 12 - Fundamentals of ABM 2Document13 pagesLearning Activity Sheet No. 16 2 Quarter: Grade Level/ Subject Grade 12 - Fundamentals of ABM 2Yuri GalloNo ratings yet

- Bank Reconciliation Statement Theory and Practice Question From Sir Jawad and Sir Dawood Shahid and Icap TextDocument64 pagesBank Reconciliation Statement Theory and Practice Question From Sir Jawad and Sir Dawood Shahid and Icap TextJahanzaib ButtNo ratings yet

- Bank Reconciliation PDFDocument17 pagesBank Reconciliation PDFJamaica IndacNo ratings yet

- CFAS - Bank ReconciliationDocument5 pagesCFAS - Bank ReconciliationAltessa Lyn ContigaNo ratings yet

- Accounting For CashDocument9 pagesAccounting For CashNatty STAN100% (1)

- Chapter 6 CashDocument15 pagesChapter 6 CashTesfamlak MulatuNo ratings yet

- Chapter-01 Accounting For Banking CompanyDocument26 pagesChapter-01 Accounting For Banking CompanyRabbi Ul Apon100% (1)

- Lesson 8 - Bank Reconciliation StatementDocument5 pagesLesson 8 - Bank Reconciliation StatementUnknownymousNo ratings yet

- Bank Reconciliation StatementDocument4 pagesBank Reconciliation StatementArshad BashirNo ratings yet

- Bank Reconciliation StatementDocument14 pagesBank Reconciliation StatementMarvie MendozaNo ratings yet

- 206bank Reconcilliation StatementDocument3 pages206bank Reconcilliation StatementRAKESH VARMANo ratings yet

- 8bank Reconciliation StatementDocument12 pages8bank Reconciliation Statementnikita2802No ratings yet

- Chapter Five CashDocument9 pagesChapter Five CashDawit TesfayeNo ratings yet

- Accounting PPT ReportDocument27 pagesAccounting PPT ReportAbdullah AmjadNo ratings yet

- MC1404 - Unit 5Document11 pagesMC1404 - Unit 5Senthil KumarNo ratings yet

- Cash and Cash EquivalentsDocument9 pagesCash and Cash EquivalentsJna MarieNo ratings yet

- Bank Reconciliation StatementDocument10 pagesBank Reconciliation StatementmuniNo ratings yet

- Financial Accounting Handout 2Document49 pagesFinancial Accounting Handout 2Rhoda Mbabazi ByogaNo ratings yet

- BRS Bank Reconcilation StatementDocument15 pagesBRS Bank Reconcilation Statementbabluon22No ratings yet

- Bank ReconciliationDocument7 pagesBank ReconciliationMikaella Adriana GoNo ratings yet

- Managerial Accounting (Banking) Terms For MBA StudentsDocument3 pagesManagerial Accounting (Banking) Terms For MBA StudentsEbunNo ratings yet

- Accounting Lesson 1 Bank Reconciliation NotesDocument9 pagesAccounting Lesson 1 Bank Reconciliation NotesKabelo SefaliNo ratings yet

- Chp1 Bank Bank Recon STMTDocument16 pagesChp1 Bank Bank Recon STMTMichael AsieduNo ratings yet

- Bank Reconciliation: Ninia C. Pauig-Lumauan, MBA, CPA Lyceum of AparriDocument60 pagesBank Reconciliation: Ninia C. Pauig-Lumauan, MBA, CPA Lyceum of AparriTessang OnongenNo ratings yet

- General BankingDocument32 pagesGeneral BankingTaanzim JhumuNo ratings yet

- Chapter-2 Bank Reconciliation StatementDocument10 pagesChapter-2 Bank Reconciliation Statementyisog79636No ratings yet

- Paying and Collecting BankerDocument12 pagesPaying and Collecting BankerartiNo ratings yet

- Bank Reconciliations: Meaning: A Bank Reconciliation Statement Is A Statement That Compares The Cash Book and TheDocument2 pagesBank Reconciliations: Meaning: A Bank Reconciliation Statement Is A Statement That Compares The Cash Book and TheApurvakc KcNo ratings yet

- Notes On Cash and Cash EquivalentsDocument1 pageNotes On Cash and Cash EquivalentsMariz Julian Pang-aoNo ratings yet

- FABM2 Chapter5Document7 pagesFABM2 Chapter5johnleegiba09No ratings yet

- Material 2Document45 pagesMaterial 2Rocky BassigNo ratings yet

- Banking Law & PracticeDocument12 pagesBanking Law & PracticeShams TabrezNo ratings yet

- Bank ReconciliationDocument18 pagesBank ReconciliationJanaica MacaraegNo ratings yet

- Banking Chapter FourDocument13 pagesBanking Chapter FourfikremariamNo ratings yet

- Bank ReconciliationDocument20 pagesBank ReconciliationLoslyn LumacangNo ratings yet

- Ch.4 - Cash and Receivables - MHDocument75 pagesCh.4 - Cash and Receivables - MHSamZhaoNo ratings yet

- CashDocument9 pagesCashHenok EnkuselassieNo ratings yet

- IA 1 Module Week 3-4Document8 pagesIA 1 Module Week 3-4Yamit, Angel Marie A.No ratings yet

- CH 3 - BrsDocument0 pagesCH 3 - BrsHaseeb Ullah KhanNo ratings yet

- Bank Reconciliation TopicDocument11 pagesBank Reconciliation TopicJoanNo ratings yet

- Paying BankerDocument2 pagesPaying BankerwubeNo ratings yet

- Binayak Academy,: Gandhi Nagar 1 Line, Near NCC Office, BerhampurDocument8 pagesBinayak Academy,: Gandhi Nagar 1 Line, Near NCC Office, BerhampurkunjapNo ratings yet

- Unit 2 LPBDocument9 pagesUnit 2 LPBVeena ReddyNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Hitachi Sa Approval LetterDocument1 pageHitachi Sa Approval LetterMohammad T. KhalafNo ratings yet

- FIN7101 Group Assignment (Plantation) - FINAL (Group 3)Document73 pagesFIN7101 Group Assignment (Plantation) - FINAL (Group 3)Azdzharulnizzam AlwiNo ratings yet

- Start Living in Spain - Spanish Residency Free GuideDocument13 pagesStart Living in Spain - Spanish Residency Free GuideMustaffah KabelyyonNo ratings yet

- Foreign InvestmentDocument12 pagesForeign InvestmentMahmudur RahmanNo ratings yet

- Market Studies: Using Information To Guide Your StrategyDocument12 pagesMarket Studies: Using Information To Guide Your StrategyNicolás Galavis VelandiaNo ratings yet

- The State of CPP Purchase Power - Presentation To Utilities Comm 9-29-2020Document35 pagesThe State of CPP Purchase Power - Presentation To Utilities Comm 9-29-2020Sheehan HannanNo ratings yet

- Solution To Ch14 P13 Build A ModelDocument6 pagesSolution To Ch14 P13 Build A ModelALI HAIDERNo ratings yet

- Working Capital: Estimation and Calculation: de Luna, Regina Carla D. AIME330 - AQ1ArDocument5 pagesWorking Capital: Estimation and Calculation: de Luna, Regina Carla D. AIME330 - AQ1ArRegina De LunaNo ratings yet

- Handouts ACCOUNTING-2Document39 pagesHandouts ACCOUNTING-2Marc John IlanoNo ratings yet

- Tax For Rental Income in The PhilippinesDocument3 pagesTax For Rental Income in The PhilippinesRESIE GALANGNo ratings yet

- Financial Technologies and DeFi A Revisit To The Digital Finance RevolutionDocument3 pagesFinancial Technologies and DeFi A Revisit To The Digital Finance RevolutionAista Putra WisenewNo ratings yet

- Business English-FinalDocument37 pagesBusiness English-FinalLee's WorldNo ratings yet

- Ganning Your Own IndependenceDocument3 pagesGanning Your Own Independenceferreira MBNo ratings yet

- Financial Management-Lecture 7Document26 pagesFinancial Management-Lecture 7TinoManhangaNo ratings yet

- NFIR LecturesDocument9 pagesNFIR LecturesEliNo ratings yet

- Dokumen - Tips Industry Analysis Splash CorpDocument32 pagesDokumen - Tips Industry Analysis Splash CorpJayNo ratings yet

- Block 4Document84 pagesBlock 4Abhinav Ashok ChandelNo ratings yet

- 2 4ms of ProductionDocument31 pages2 4ms of ProductionYancey LucasNo ratings yet

- Comprehensive ExerciseDocument4 pagesComprehensive Exerciseوائل مصطفىNo ratings yet

- Solution Far670 Dec 2019Document5 pagesSolution Far670 Dec 2019Farissa ElyaNo ratings yet

- Case Ocean CarriersDocument2 pagesCase Ocean CarriersMorsal SarwarzadehNo ratings yet

- DSE McSleepersDocument1 pageDSE McSleepersJo FarrellNo ratings yet

- Cons of Global Free TradeDocument4 pagesCons of Global Free TradeGlydel Mae LaidanNo ratings yet

- (Done) Q2 - GenMath WEEK 11 (M1)Document3 pages(Done) Q2 - GenMath WEEK 11 (M1)aespa karinaNo ratings yet

- MSFIN 223 - Case 1 - Du Pont (Cauton, Cortez, Dy, Lui, Mamaril, Papa, Rasco)Document3 pagesMSFIN 223 - Case 1 - Du Pont (Cauton, Cortez, Dy, Lui, Mamaril, Papa, Rasco)Leophil RascoNo ratings yet

- BS 4662Document41 pagesBS 4662hessian123100% (1)

Download as docx, pdf, or txt

You might also like

- 1G2 - Outbound Processing For Customer - WMDocument12 pages1G2 - Outbound Processing For Customer - WMsserpsap100% (1)

- BRS Full ChapterDocument16 pagesBRS Full ChapterMumtazAhmad100% (1)

- Monopoly ProjectDocument13 pagesMonopoly Projectapi-311197959No ratings yet

- Risk Management in Banking Sector MainDocument54 pagesRisk Management in Banking Sector MainJahanvi Bansal55% (11)

- Xerox-Case Study Analysi-JhellDocument10 pagesXerox-Case Study Analysi-Jhelljhell de la cruzNo ratings yet

- MODULE 3 - Part 3 Bank ReconciliationDocument16 pagesMODULE 3 - Part 3 Bank ReconciliationShaena Mae50% (2)

- Bank Reconciliation - For LectureDocument3 pagesBank Reconciliation - For LectureCharlene Jane EspinoNo ratings yet

- Hsslive-Chapter 5 BRS 1 PDFDocument2 pagesHsslive-Chapter 5 BRS 1 PDFRam IyerNo ratings yet

- Fundamentas of Accounting I CH 5Document24 pagesFundamentas of Accounting I CH 5israelbedasa3100% (1)

- Bank ReconciliationDocument12 pagesBank ReconciliationJenny Pearl Dominguez CalizarNo ratings yet

- Chapter 2 Bank Reconciliation (Gatdc)Document20 pagesChapter 2 Bank Reconciliation (Gatdc)Joan LeonorNo ratings yet

- Assignment 1571213669 SmsDocument13 pagesAssignment 1571213669 SmsJayasuriya SNo ratings yet

- Bank Reconciliation StatementDocument27 pagesBank Reconciliation Statementkimuli FreddieNo ratings yet

- Intermidiate FA I ChapterDocument28 pagesIntermidiate FA I Chapteryiberta69No ratings yet

- Group - 11 Bank Reconciliation Statement: CIA (Continuous Internal Assessment) 1Document13 pagesGroup - 11 Bank Reconciliation Statement: CIA (Continuous Internal Assessment) 1shriyanshu padhiNo ratings yet

- Chapter 5 - Bank Reconciliation StatementDocument23 pagesChapter 5 - Bank Reconciliation StatementNchumthung JamiNo ratings yet

- Midterm The Banks Functional DepartmentsDocument49 pagesMidterm The Banks Functional DepartmentsB-jay AledonNo ratings yet

- 6 - Bank Reconciliation StatementDocument3 pages6 - Bank Reconciliation StatementNeeraj RaikwarNo ratings yet

- Learning Activity Sheet No. 16 2 Quarter: Grade Level/ Subject Grade 12 - Fundamentals of ABM 2Document13 pagesLearning Activity Sheet No. 16 2 Quarter: Grade Level/ Subject Grade 12 - Fundamentals of ABM 2Yuri GalloNo ratings yet

- Bank Reconciliation Statement Theory and Practice Question From Sir Jawad and Sir Dawood Shahid and Icap TextDocument64 pagesBank Reconciliation Statement Theory and Practice Question From Sir Jawad and Sir Dawood Shahid and Icap TextJahanzaib ButtNo ratings yet

- Bank Reconciliation PDFDocument17 pagesBank Reconciliation PDFJamaica IndacNo ratings yet

- CFAS - Bank ReconciliationDocument5 pagesCFAS - Bank ReconciliationAltessa Lyn ContigaNo ratings yet

- Accounting For CashDocument9 pagesAccounting For CashNatty STAN100% (1)

- Chapter 6 CashDocument15 pagesChapter 6 CashTesfamlak MulatuNo ratings yet

- Chapter-01 Accounting For Banking CompanyDocument26 pagesChapter-01 Accounting For Banking CompanyRabbi Ul Apon100% (1)

- Lesson 8 - Bank Reconciliation StatementDocument5 pagesLesson 8 - Bank Reconciliation StatementUnknownymousNo ratings yet

- Bank Reconciliation StatementDocument4 pagesBank Reconciliation StatementArshad BashirNo ratings yet

- Bank Reconciliation StatementDocument14 pagesBank Reconciliation StatementMarvie MendozaNo ratings yet

- 206bank Reconcilliation StatementDocument3 pages206bank Reconcilliation StatementRAKESH VARMANo ratings yet

- 8bank Reconciliation StatementDocument12 pages8bank Reconciliation Statementnikita2802No ratings yet

- Chapter Five CashDocument9 pagesChapter Five CashDawit TesfayeNo ratings yet

- Accounting PPT ReportDocument27 pagesAccounting PPT ReportAbdullah AmjadNo ratings yet

- MC1404 - Unit 5Document11 pagesMC1404 - Unit 5Senthil KumarNo ratings yet

- Cash and Cash EquivalentsDocument9 pagesCash and Cash EquivalentsJna MarieNo ratings yet

- Bank Reconciliation StatementDocument10 pagesBank Reconciliation StatementmuniNo ratings yet

- Financial Accounting Handout 2Document49 pagesFinancial Accounting Handout 2Rhoda Mbabazi ByogaNo ratings yet

- BRS Bank Reconcilation StatementDocument15 pagesBRS Bank Reconcilation Statementbabluon22No ratings yet

- Bank ReconciliationDocument7 pagesBank ReconciliationMikaella Adriana GoNo ratings yet

- Managerial Accounting (Banking) Terms For MBA StudentsDocument3 pagesManagerial Accounting (Banking) Terms For MBA StudentsEbunNo ratings yet

- Accounting Lesson 1 Bank Reconciliation NotesDocument9 pagesAccounting Lesson 1 Bank Reconciliation NotesKabelo SefaliNo ratings yet

- Chp1 Bank Bank Recon STMTDocument16 pagesChp1 Bank Bank Recon STMTMichael AsieduNo ratings yet

- Bank Reconciliation: Ninia C. Pauig-Lumauan, MBA, CPA Lyceum of AparriDocument60 pagesBank Reconciliation: Ninia C. Pauig-Lumauan, MBA, CPA Lyceum of AparriTessang OnongenNo ratings yet

- General BankingDocument32 pagesGeneral BankingTaanzim JhumuNo ratings yet

- Chapter-2 Bank Reconciliation StatementDocument10 pagesChapter-2 Bank Reconciliation Statementyisog79636No ratings yet

- Paying and Collecting BankerDocument12 pagesPaying and Collecting BankerartiNo ratings yet

- Bank Reconciliations: Meaning: A Bank Reconciliation Statement Is A Statement That Compares The Cash Book and TheDocument2 pagesBank Reconciliations: Meaning: A Bank Reconciliation Statement Is A Statement That Compares The Cash Book and TheApurvakc KcNo ratings yet

- Notes On Cash and Cash EquivalentsDocument1 pageNotes On Cash and Cash EquivalentsMariz Julian Pang-aoNo ratings yet

- FABM2 Chapter5Document7 pagesFABM2 Chapter5johnleegiba09No ratings yet

- Material 2Document45 pagesMaterial 2Rocky BassigNo ratings yet

- Banking Law & PracticeDocument12 pagesBanking Law & PracticeShams TabrezNo ratings yet

- Bank ReconciliationDocument18 pagesBank ReconciliationJanaica MacaraegNo ratings yet

- Banking Chapter FourDocument13 pagesBanking Chapter FourfikremariamNo ratings yet

- Bank ReconciliationDocument20 pagesBank ReconciliationLoslyn LumacangNo ratings yet

- Ch.4 - Cash and Receivables - MHDocument75 pagesCh.4 - Cash and Receivables - MHSamZhaoNo ratings yet

- CashDocument9 pagesCashHenok EnkuselassieNo ratings yet

- IA 1 Module Week 3-4Document8 pagesIA 1 Module Week 3-4Yamit, Angel Marie A.No ratings yet

- CH 3 - BrsDocument0 pagesCH 3 - BrsHaseeb Ullah KhanNo ratings yet

- Bank Reconciliation TopicDocument11 pagesBank Reconciliation TopicJoanNo ratings yet

- Paying BankerDocument2 pagesPaying BankerwubeNo ratings yet

- Binayak Academy,: Gandhi Nagar 1 Line, Near NCC Office, BerhampurDocument8 pagesBinayak Academy,: Gandhi Nagar 1 Line, Near NCC Office, BerhampurkunjapNo ratings yet

- Unit 2 LPBDocument9 pagesUnit 2 LPBVeena ReddyNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Hitachi Sa Approval LetterDocument1 pageHitachi Sa Approval LetterMohammad T. KhalafNo ratings yet

- FIN7101 Group Assignment (Plantation) - FINAL (Group 3)Document73 pagesFIN7101 Group Assignment (Plantation) - FINAL (Group 3)Azdzharulnizzam AlwiNo ratings yet

- Start Living in Spain - Spanish Residency Free GuideDocument13 pagesStart Living in Spain - Spanish Residency Free GuideMustaffah KabelyyonNo ratings yet

- Foreign InvestmentDocument12 pagesForeign InvestmentMahmudur RahmanNo ratings yet

- Market Studies: Using Information To Guide Your StrategyDocument12 pagesMarket Studies: Using Information To Guide Your StrategyNicolás Galavis VelandiaNo ratings yet

- The State of CPP Purchase Power - Presentation To Utilities Comm 9-29-2020Document35 pagesThe State of CPP Purchase Power - Presentation To Utilities Comm 9-29-2020Sheehan HannanNo ratings yet

- Solution To Ch14 P13 Build A ModelDocument6 pagesSolution To Ch14 P13 Build A ModelALI HAIDERNo ratings yet

- Working Capital: Estimation and Calculation: de Luna, Regina Carla D. AIME330 - AQ1ArDocument5 pagesWorking Capital: Estimation and Calculation: de Luna, Regina Carla D. AIME330 - AQ1ArRegina De LunaNo ratings yet

- Handouts ACCOUNTING-2Document39 pagesHandouts ACCOUNTING-2Marc John IlanoNo ratings yet

- Tax For Rental Income in The PhilippinesDocument3 pagesTax For Rental Income in The PhilippinesRESIE GALANGNo ratings yet

- Financial Technologies and DeFi A Revisit To The Digital Finance RevolutionDocument3 pagesFinancial Technologies and DeFi A Revisit To The Digital Finance RevolutionAista Putra WisenewNo ratings yet

- Business English-FinalDocument37 pagesBusiness English-FinalLee's WorldNo ratings yet

- Ganning Your Own IndependenceDocument3 pagesGanning Your Own Independenceferreira MBNo ratings yet

- Financial Management-Lecture 7Document26 pagesFinancial Management-Lecture 7TinoManhangaNo ratings yet

- NFIR LecturesDocument9 pagesNFIR LecturesEliNo ratings yet

- Dokumen - Tips Industry Analysis Splash CorpDocument32 pagesDokumen - Tips Industry Analysis Splash CorpJayNo ratings yet

- Block 4Document84 pagesBlock 4Abhinav Ashok ChandelNo ratings yet

- 2 4ms of ProductionDocument31 pages2 4ms of ProductionYancey LucasNo ratings yet

- Comprehensive ExerciseDocument4 pagesComprehensive Exerciseوائل مصطفىNo ratings yet

- Solution Far670 Dec 2019Document5 pagesSolution Far670 Dec 2019Farissa ElyaNo ratings yet

- Case Ocean CarriersDocument2 pagesCase Ocean CarriersMorsal SarwarzadehNo ratings yet

- DSE McSleepersDocument1 pageDSE McSleepersJo FarrellNo ratings yet

- Cons of Global Free TradeDocument4 pagesCons of Global Free TradeGlydel Mae LaidanNo ratings yet

- (Done) Q2 - GenMath WEEK 11 (M1)Document3 pages(Done) Q2 - GenMath WEEK 11 (M1)aespa karinaNo ratings yet

- MSFIN 223 - Case 1 - Du Pont (Cauton, Cortez, Dy, Lui, Mamaril, Papa, Rasco)Document3 pagesMSFIN 223 - Case 1 - Du Pont (Cauton, Cortez, Dy, Lui, Mamaril, Papa, Rasco)Leophil RascoNo ratings yet

- BS 4662Document41 pagesBS 4662hessian123100% (1)