Download as pdf or txt

You might also like

- Test Bank For Berne and Levy Physiology 6th Edition KoeppenDocument24 pagesTest Bank For Berne and Levy Physiology 6th Edition KoeppenChristopherWrightgipe100% (46)

- Roller DooyaDocument147 pagesRoller DooyaNachoNo ratings yet

- Iso 21905-HRSGDocument106 pagesIso 21905-HRSGadepp8642100% (1)

- Aspect® Unified IP® 7.4 SP1 Aspect® Unified IP® - Advanced List Management 7.4 ™ SP1 Product Release NotesDocument29 pagesAspect® Unified IP® 7.4 SP1 Aspect® Unified IP® - Advanced List Management 7.4 ™ SP1 Product Release NotesAbNo ratings yet

- WTO - International Arrivals To Venezuela (2012-2016)Document2 pagesWTO - International Arrivals To Venezuela (2012-2016)Anonymous mF1cc3NNo ratings yet

- Country Profile: ColombiaDocument10 pagesCountry Profile: ColombiaPaula Andrea RodríguezNo ratings yet

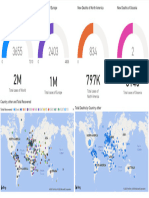

- PowerBI Dashboard ExampleDocument1 pagePowerBI Dashboard ExampleCharielle Esthelin BacuganNo ratings yet

- PowerBI Dashboard ExampleDocument1 pagePowerBI Dashboard ExampleKolade OrimoladeNo ratings yet

- Shell Immersion Cooling Fluid Marketing Brochure Updated Oct 23Document12 pagesShell Immersion Cooling Fluid Marketing Brochure Updated Oct 23Optus 583No ratings yet

- TopGlove - Integrated - Annual - Report - 2022 - Part 1Document25 pagesTopGlove - Integrated - Annual - Report - 2022 - Part 1Dharesini ChandranNo ratings yet

- Vietnam and The Global Value Chain: FIGURE 2.1. Export-Led Growth and Poverty Reduction, 1992-2017Document1 pageVietnam and The Global Value Chain: FIGURE 2.1. Export-Led Growth and Poverty Reduction, 1992-2017hnmjzhviNo ratings yet

- Study - Id67394 - Foreign Direct Investments in IndiaDocument26 pagesStudy - Id67394 - Foreign Direct Investments in IndiavishnuNo ratings yet

- 21-4-6 IDFC MF Equity Market Outlook FY 22Document42 pages21-4-6 IDFC MF Equity Market Outlook FY 22reddyramireddy2022No ratings yet

- Valuation Report of BPCLDocument35 pagesValuation Report of BPCLJobin JohnNo ratings yet

- Urban: Pay Date Cac No. Amount Paid Punch DateDocument1 pageUrban: Pay Date Cac No. Amount Paid Punch DateDivyansh JohriNo ratings yet

- Madhya Pradesh Road Development Corporation: Last 11 Yrs. Completed Road Length (In KM)Document15 pagesMadhya Pradesh Road Development Corporation: Last 11 Yrs. Completed Road Length (In KM)Rajveer Singh YadavNo ratings yet

- Standards - Report - e by WTODocument6 pagesStandards - Report - e by WTOVivek BadkurNo ratings yet

- Menap PPT 042020Document25 pagesMenap PPT 042020AbhinavSinghNo ratings yet

- Q3 2022 ID ColliersQuarterly JakartaDocument27 pagesQ3 2022 ID ColliersQuarterly JakartaGeraldy Dearma PradhanaNo ratings yet

- FRB 8 Acctg For FWL Waiver Rebate (Final)Document19 pagesFRB 8 Acctg For FWL Waiver Rebate (Final)cheezhen5047No ratings yet

- Malaysian House Price Index (MHPI)Document2 pagesMalaysian House Price Index (MHPI)Afiq KhidhirNo ratings yet

- ReviewDocument7 pagesReviewAbdullah CheemaNo ratings yet

- Group 2Document1 pageGroup 2HamzaMehmoodBhattiNo ratings yet

- Oil Companies TransitoinDocument1 pageOil Companies TransitoinandresNo ratings yet

- Madhya Pradesh Road Development Corporation: Last 11 Yrs. Completed Road Length (In KM)Document16 pagesMadhya Pradesh Road Development Corporation: Last 11 Yrs. Completed Road Length (In KM)Vivek VermaNo ratings yet

- Nazara IM - Spark CapitalDocument27 pagesNazara IM - Spark CapitalBBNo ratings yet

- Etude Avolta-VC-MA-Tech-Trends-France-2022Document26 pagesEtude Avolta-VC-MA-Tech-Trends-France-2022Thibaud CombeNo ratings yet

- Madan Bohara Marketing PRESENTATION R I1Document22 pagesMadan Bohara Marketing PRESENTATION R I1Navin AcharyaNo ratings yet

- 溫室氣體盤查3日種子班-第一天-講義 1121130Document82 pages溫室氣體盤查3日種子班-第一天-講義 1121130MillerNo ratings yet

- Covid 19Document1 pageCovid 19oyuka oyukaNo ratings yet

- 2 - Avendano - Digital Regulation Framework For ASEANDocument15 pages2 - Avendano - Digital Regulation Framework For ASEANAom SakornNo ratings yet

- Chart PackDocument35 pagesChart Packxyan.zohar7No ratings yet

- Energy September 2023Document41 pagesEnergy September 2023Dalina Maria AndreiNo ratings yet

- 3.4 Financial Analysis Kena Buat Huraikan SikitDocument7 pages3.4 Financial Analysis Kena Buat Huraikan SikitSolehah OmarNo ratings yet

- ERTMSETCS in Numbers 1Document2 pagesERTMSETCS in Numbers 1Donato ToccoNo ratings yet

- Surabaya Property Market Report: Colliers Half Year Report H1 2018 20 September 2018Document22 pagesSurabaya Property Market Report: Colliers Half Year Report H1 2018 20 September 2018anthony csNo ratings yet

- 09.EK September 2022Document6 pages09.EK September 2022kleber VergaraNo ratings yet

- Guide To: ExcellenceDocument12 pagesGuide To: ExcellenceSuri SANo ratings yet

- SHS WFP PPMP App Sob MDP Fy2020Document114 pagesSHS WFP PPMP App Sob MDP Fy2020Haydee YuriNo ratings yet

- Digitalization in Mining IndustryDocument49 pagesDigitalization in Mining IndustryOskr FdzNo ratings yet

- Chart PackDocument34 pagesChart Packmodeste29001No ratings yet

- GEM - Structure - Vietnam - AB 2021 10 19Document34 pagesGEM - Structure - Vietnam - AB 2021 10 19Trần Thái Đình KhươngNo ratings yet

- Indonesia IEP June 2021 SlidesDocument17 pagesIndonesia IEP June 2021 Slidesfrisdian97No ratings yet

- MOSL New Year Top Picks 2023Document19 pagesMOSL New Year Top Picks 2023dcpjimmy100% (1)

- The New Global Competence in Hot Rolling 2019Document15 pagesThe New Global Competence in Hot Rolling 2019belkacemNo ratings yet

- 乐鑫科技2021年企业社会责任报告Document48 pages乐鑫科技2021年企业社会责任报告王烁然No ratings yet

- Telematics Product Catalog 2021 FebruaryDocument38 pagesTelematics Product Catalog 2021 FebruaryAli AnbaaNo ratings yet

- The President's Eskom Sustainability Task Team - Anton EberhardDocument20 pagesThe President's Eskom Sustainability Task Team - Anton EberhardChristo88No ratings yet

- Service Sector in IndiaDocument15 pagesService Sector in IndiaNick NickyNo ratings yet

- Telematics Product Catalog 2021 AugustDocument39 pagesTelematics Product Catalog 2021 AugustFiros KNo ratings yet

- KPO IndustryDocument33 pagesKPO IndustryManish Saran100% (6)

- PROJ02 - Bao-idangC & JimenezJDocument6 pagesPROJ02 - Bao-idangC & JimenezJChaermalyn Bao-idangNo ratings yet

- Najeeb Gas BillDocument1 pageNajeeb Gas BillAbdul ghaffarNo ratings yet

- Global Economic Prospects Jun2020 PressHighlights Chp4Document3 pagesGlobal Economic Prospects Jun2020 PressHighlights Chp4CristianMilciadesNo ratings yet

- Valuation Report of BPCLDocument24 pagesValuation Report of BPCLJobin JohnNo ratings yet

- World Trade Statical Review in 2021Document136 pagesWorld Trade Statical Review in 2021Lê Thị TìnhNo ratings yet

- Full Glossary of Statistics TermsDocument150 pagesFull Glossary of Statistics Termsshahid 1shahNo ratings yet

- The Australian EconomyDocument35 pagesThe Australian Economybiangbiang bangNo ratings yet

- PT Bekasi Fajar Industrial Estate TBK: Investors Highlight - 3M 2021Document6 pagesPT Bekasi Fajar Industrial Estate TBK: Investors Highlight - 3M 2021ninja vibelNo ratings yet

- Employment Insurance Sytem (Eis) : VOLUME 4/2020 The Impact of Covid-19 On LoeDocument26 pagesEmployment Insurance Sytem (Eis) : VOLUME 4/2020 The Impact of Covid-19 On LoeunicornmfkNo ratings yet

- BV Cia 3Document27 pagesBV Cia 3Jobin JohnNo ratings yet

- ObliconDocument111 pagesObliconBroy D BriumNo ratings yet

- FINAL - Commercial Law (From Divina Rev)Document22 pagesFINAL - Commercial Law (From Divina Rev)Lynnette ChungNo ratings yet

- The Scope of Corporate FinanceDocument11 pagesThe Scope of Corporate Financelinda zyongweNo ratings yet

- COMPANY LAW LECTURE NOTES - Tracked - Nov15.2020Document59 pagesCOMPANY LAW LECTURE NOTES - Tracked - Nov15.2020John Quachie100% (1)

- Definition, Concept and Purpose of Taxation: Taxation 1 Case Digest Atty. Marvin CaneroDocument13 pagesDefinition, Concept and Purpose of Taxation: Taxation 1 Case Digest Atty. Marvin CaneroStela PantaleonNo ratings yet

- Obligations and Contracts (Dean Ulan)Document26 pagesObligations and Contracts (Dean Ulan)Priscilla DawnNo ratings yet

- Business Basics Handout Types of Business OwnershipDocument5 pagesBusiness Basics Handout Types of Business OwnershipToniann LawrenceNo ratings yet

- Labor BarQsDocument10 pagesLabor BarQsAtheena Marie PalomariaNo ratings yet

- CM-f3e Module: Technical DescriptionDocument34 pagesCM-f3e Module: Technical DescriptionLejlaNo ratings yet

- G.R. No. 185522Document6 pagesG.R. No. 185522Kyla AbadNo ratings yet

- Case Labor Law Alilin VS PetronDocument9 pagesCase Labor Law Alilin VS Petronedawrd aroncianoNo ratings yet

- Transcultural Health Care A Culturally Competent Approach 4th Edition Purnell Test BankDocument18 pagesTranscultural Health Care A Culturally Competent Approach 4th Edition Purnell Test Bankjadialuwaehs100% (20)

- MC14027B Dual J-K Flip-Flop: FeaturesDocument6 pagesMC14027B Dual J-K Flip-Flop: Featuresmarcos cordovaNo ratings yet

- Ez-Light SP Series Signal Light: DatasheetDocument8 pagesEz-Light SP Series Signal Light: DatasheetJosé Antonio Solorzano cruzNo ratings yet

- Abandoned Property (Disposal) Act, 1974Document5 pagesAbandoned Property (Disposal) Act, 1974Maame Ekua Yaakwae AsaamNo ratings yet

- Occupiers Liability Act 1957Document4 pagesOccupiers Liability Act 1957Abdullah SaeedNo ratings yet

- Iphone Software License4Document11 pagesIphone Software License4raghuNo ratings yet

- A Comparitive Study On Inevitable Accident and Act of GodDocument9 pagesA Comparitive Study On Inevitable Accident and Act of GodAkash JNo ratings yet

- Corporation Code (De Leon, 2010) PDFDocument1,114 pagesCorporation Code (De Leon, 2010) PDFJayson De LemonNo ratings yet

- 3 TNV 88 FDocument266 pages3 TNV 88 FKhaled Naseem Abu-Sabha100% (1)

- Mercantile Law Q and A Set 1Document5 pagesMercantile Law Q and A Set 1Enzo OfilanNo ratings yet

- Corporation Law Digested CasesDocument11 pagesCorporation Law Digested CasesKarl Jason JosolNo ratings yet

- License SASDocument3 pagesLicense SASjharmifer stiven heredia duranNo ratings yet

- ReadmeDocument3 pagesReadmeTemelkoski DarkoNo ratings yet

- Loans and Credit Corporation." The Assailed Rulings Reversed and Set Aside The DecisionDocument12 pagesLoans and Credit Corporation." The Assailed Rulings Reversed and Set Aside The DecisionJulian DubaNo ratings yet

- The Workmen Compensation Act 1923Document12 pagesThe Workmen Compensation Act 1923Vishnu BalajiNo ratings yet

- Yes HospitalDocument4 pagesYes Hospitalhare_07No ratings yet

- Torts and Damages Notes FinalllyDocument192 pagesTorts and Damages Notes FinalllyVanessa VelascoNo ratings yet