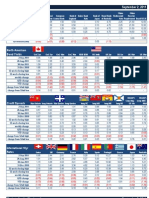

Markets For The Week Ending September 9, 2011: Monetary Policy

Markets For The Week Ending September 9, 2011: Monetary Policy

You might also like

- Steps To Discharging Debt CollectionsDocument3 pagesSteps To Discharging Debt Collectionserickutny93% (42)

- Socio-Economic StudyDocument3 pagesSocio-Economic StudygrenadeboiNo ratings yet

- 2017 Exam With SolutionsDocument4 pages2017 Exam With SolutionsMathew YipNo ratings yet

- Prac 1 - First Preboard - P2 65th NewDocument12 pagesPrac 1 - First Preboard - P2 65th NewArianne Llorente100% (1)

- Financial Planning and ForcastingDocument34 pagesFinancial Planning and ForcastingFarhan JagirdarNo ratings yet

- Markets For The Week Ending September 23, 2011: Monetary PolicyDocument10 pagesMarkets For The Week Ending September 23, 2011: Monetary PolicymwarywodaNo ratings yet

- Markets For The Week Ending September 2, 2011: Monetary PolicyDocument8 pagesMarkets For The Week Ending September 2, 2011: Monetary PolicymwarywodaNo ratings yet

- Markets For The Week Ending September 16, 2011: Monetary PolicyDocument10 pagesMarkets For The Week Ending September 16, 2011: Monetary PolicymwarywodaNo ratings yet

- The End For Berlusconi: Morning ReportDocument3 pagesThe End For Berlusconi: Morning Reportnaudaslietas_lvNo ratings yet

- Disagreement About Ecbs Role: Morning ReportDocument3 pagesDisagreement About Ecbs Role: Morning Reportnaudaslietas_lvNo ratings yet

- Unchanged From Boe and Ecb: Morning ReportDocument3 pagesUnchanged From Boe and Ecb: Morning Reportnaudaslietas_lvNo ratings yet

- Brighter in China: Morning ReportDocument3 pagesBrighter in China: Morning Reportnaudaslietas_lvNo ratings yet

- Growth Weakens in China: Morning ReportDocument3 pagesGrowth Weakens in China: Morning Reportnaudaslietas_lvNo ratings yet

- What Will ECB Deliver Today?: Morning ReportDocument3 pagesWhat Will ECB Deliver Today?: Morning Reportnaudaslietas_lvNo ratings yet

- MRE130114Document3 pagesMRE130114naudaslietas_lvNo ratings yet

- Greek Bail-Out Approved: Morning ReportDocument3 pagesGreek Bail-Out Approved: Morning Reportnaudaslietas_lvNo ratings yet

- OECD Wants Action: Morning ReportDocument3 pagesOECD Wants Action: Morning Reportnaudaslietas_lvNo ratings yet

- More Weak Chinese Data: Morning ReportDocument3 pagesMore Weak Chinese Data: Morning Reportnaudaslietas_lvNo ratings yet

- 50 Bps Rate Cut From Norges Bank: Morning ReportDocument3 pages50 Bps Rate Cut From Norges Bank: Morning Reportnaudaslietas_lvNo ratings yet

- Political Pressure On Boj: Morning ReportDocument3 pagesPolitical Pressure On Boj: Morning Reportnaudaslietas_lvNo ratings yet

- No Change Neither From Ecb Nor Boe: Morning ReportDocument3 pagesNo Change Neither From Ecb Nor Boe: Morning Reportnaudaslietas_lvNo ratings yet

- Boe and Ecb On Hold Today: Morning ReportDocument3 pagesBoe and Ecb On Hold Today: Morning Reportnaudaslietas_lvNo ratings yet

- Greek Debt Sale Wins Time For The Troika: Morning ReportDocument3 pagesGreek Debt Sale Wins Time For The Troika: Morning Reportnaudaslietas_lvNo ratings yet

- Italy Still Faces High Borrowing Costs: Morning ReportDocument3 pagesItaly Still Faces High Borrowing Costs: Morning Reportnaudaslietas_lvNo ratings yet

- Can Mario Monti Save Italy?: Morning ReportDocument3 pagesCan Mario Monti Save Italy?: Morning Reportnaudaslietas_lvNo ratings yet

- New Stimulus From Bank of England: Morning ReportDocument3 pagesNew Stimulus From Bank of England: Morning Reportnaudaslietas_lvNo ratings yet

- Banks Loans Record Amount From ECB: Morning ReportDocument3 pagesBanks Loans Record Amount From ECB: Morning Reportnaudaslietas_lvNo ratings yet

- MPC Meetings Today: Morning ReportDocument3 pagesMPC Meetings Today: Morning Reportnaudaslietas_lvNo ratings yet

- Bini Smaghi Talks For More Action: Morning ReportDocument3 pagesBini Smaghi Talks For More Action: Morning Reportnaudaslietas_lvNo ratings yet

- GDP-drop Weakened The Pound: Morning ReportDocument3 pagesGDP-drop Weakened The Pound: Morning Reportnaudaslietas_lvNo ratings yet

- GDP-growth Disappointed in Q2: Morning ReportDocument3 pagesGDP-growth Disappointed in Q2: Morning Reportnaudaslietas_lvNo ratings yet

- More Cautious Market Sentiment: Morning ReportDocument3 pagesMore Cautious Market Sentiment: Morning Reportnaudaslietas_lvNo ratings yet

- MRE111031Document3 pagesMRE111031naudaslietas_lvNo ratings yet

- Yen Weakening Halts: Morning ReportDocument3 pagesYen Weakening Halts: Morning Reportnaudaslietas_lvNo ratings yet

- Progressing US Manufacturers: Morning ReportDocument3 pagesProgressing US Manufacturers: Morning Reportnaudaslietas_lvNo ratings yet

- Draghi Weakened The Euro: Morning ReportDocument2 pagesDraghi Weakened The Euro: Morning Reportnaudaslietas_lvNo ratings yet

- Markets Cheer Euro Zone Deal: Morning ReportDocument3 pagesMarkets Cheer Euro Zone Deal: Morning Reportnaudaslietas_lvNo ratings yet

- Qvigstad Weakened The NOK: Morning ReportDocument3 pagesQvigstad Weakened The NOK: Morning Reportnaudaslietas_lvNo ratings yet

- Recession Fear Returns: Morning ReportDocument3 pagesRecession Fear Returns: Morning Reportnaudaslietas_lvNo ratings yet

- Weak Start On Second Half of 2012: Morning ReportDocument3 pagesWeak Start On Second Half of 2012: Morning Reportnaudaslietas_lvNo ratings yet

- Expects No Rate Cut From ECB: Morning ReportDocument3 pagesExpects No Rate Cut From ECB: Morning Reportnaudaslietas_lvNo ratings yet

- Spain Cuts 65 Billions: Morning ReportDocument3 pagesSpain Cuts 65 Billions: Morning Reportnaudaslietas_lvNo ratings yet

- The Outlook Remains Negative in China: Morning ReportDocument3 pagesThe Outlook Remains Negative in China: Morning Reportnaudaslietas_lvNo ratings yet

- Draghi Punctured Optimism: Morning ReportDocument3 pagesDraghi Punctured Optimism: Morning Reportnaudaslietas_lvNo ratings yet

- No Change From The Riksbank: Morning ReportDocument3 pagesNo Change From The Riksbank: Morning Reportnaudaslietas_lvNo ratings yet

- Morning Report 30oct2014Document2 pagesMorning Report 30oct2014Joseph DavidsonNo ratings yet

- Weakened Confidence in Europe: Morning ReportDocument3 pagesWeakened Confidence in Europe: Morning Reportnaudaslietas_lvNo ratings yet

- Greece Gets Two More Years: Morning ReportDocument3 pagesGreece Gets Two More Years: Morning Reportnaudaslietas_lvNo ratings yet

- Expect Rate Cut in Norway: Morning ReportDocument3 pagesExpect Rate Cut in Norway: Morning Reportnaudaslietas_lvNo ratings yet

- Weaker Yen and More QE in The US: Morning ReportDocument3 pagesWeaker Yen and More QE in The US: Morning Reportnaudaslietas_lvNo ratings yet

- More Stimuli From Central Banks: Morning ReportDocument3 pagesMore Stimuli From Central Banks: Morning Reportnaudaslietas_lvNo ratings yet

- UK Lost AAA-rating: Morning ReportDocument3 pagesUK Lost AAA-rating: Morning Reportnaudaslietas_lvNo ratings yet

- EUR Nears One-Year Low Against USD: Morning ReportDocument3 pagesEUR Nears One-Year Low Against USD: Morning Reportnaudaslietas_lvNo ratings yet

- "Yes, We Have A Deal": Morning ReportDocument3 pages"Yes, We Have A Deal": Morning Reportnaudaslietas_lvNo ratings yet

- IMF Warns About Depression: Morning ReportDocument3 pagesIMF Warns About Depression: Morning Reportnaudaslietas_lvNo ratings yet

- Obama Won The Election: Morning ReportDocument3 pagesObama Won The Election: Morning Reportnaudaslietas_lvNo ratings yet

- Italian Interest Go Sky High: Morning ReportDocument3 pagesItalian Interest Go Sky High: Morning Reportnaudaslietas_lvNo ratings yet

- Large International Banks Downgraded: Morning ReportDocument3 pagesLarge International Banks Downgraded: Morning Reportnaudaslietas_lvNo ratings yet

- Swedish Inflation Drops: Morning ReportDocument3 pagesSwedish Inflation Drops: Morning Reportnaudaslietas_lvNo ratings yet

- Ready To Recapitalize Banks: Morning ReportDocument3 pagesReady To Recapitalize Banks: Morning Reportnaudaslietas_lvNo ratings yet

- Several Important Events This Week: Morning ReportDocument3 pagesSeveral Important Events This Week: Morning Reportnaudaslietas_lvNo ratings yet

- Italy Downgraded by S&P: Morning ReportDocument3 pagesItaly Downgraded by S&P: Morning Reportnaudaslietas_lvNo ratings yet

- MRE120330Document3 pagesMRE120330naudaslietas_lvNo ratings yet

- Asset Rotation: The Demise of Modern Portfolio Theory and the Birth of an Investment RenaissanceFrom EverandAsset Rotation: The Demise of Modern Portfolio Theory and the Birth of an Investment RenaissanceNo ratings yet

- What's Cooking: Digital Transformation of the Agrifood SystemFrom EverandWhat's Cooking: Digital Transformation of the Agrifood SystemNo ratings yet

- Accounting For Companies I: Learning ObjectivesDocument11 pagesAccounting For Companies I: Learning ObjectivesHongWei TeoNo ratings yet

- Introduction To Co-Operative Banking: DefinationDocument9 pagesIntroduction To Co-Operative Banking: DefinationHelloprojectNo ratings yet

- Uppsala Papers in Economic History: 1993 Working Paper No 10Document40 pagesUppsala Papers in Economic History: 1993 Working Paper No 10Michalis RizosNo ratings yet

- Mercial PaperDocument39 pagesMercial PaperArjun Khunt100% (1)

- Neo The United Kingdom of God Sky Earth: Exhibits AbDocument4 pagesNeo The United Kingdom of God Sky Earth: Exhibits AbWORLD MEDIA & COMMUNICATIONSNo ratings yet

- Airports PresentationDocument22 pagesAirports PresentationPulokesh GhoshNo ratings yet

- Urdu SyllabusDocument5 pagesUrdu Syllabusindhu indhuNo ratings yet

- County Wrestles With Tax Hike, Raises: Ledger-NewsDocument28 pagesCounty Wrestles With Tax Hike, Raises: Ledger-Newsspacecat007No ratings yet

- Cred Trans Case Digests Part3Document13 pagesCred Trans Case Digests Part3Ayeesha PagantianNo ratings yet

- Position Review of Port Klang Free Zone Project and Port Klang Free Zone SDN BHDDocument51 pagesPosition Review of Port Klang Free Zone Project and Port Klang Free Zone SDN BHDKenny WongNo ratings yet

- Monetary and Credit Information Review: Issue 10Document4 pagesMonetary and Credit Information Review: Issue 10Anonymous AHW3sHNo ratings yet

- Blackbook Project On Credit Rating SystemDocument88 pagesBlackbook Project On Credit Rating SystemAnkit Chheda0% (1)

- 2.1 CommissionDocument28 pages2.1 CommissionAnali Barbon100% (1)

- LSCC Final Bill CC FormDocument3 pagesLSCC Final Bill CC Formకొల్లి రాఘవేణిNo ratings yet

- Ibm 5Document4 pagesIbm 5Shrinidhi HariharasuthanNo ratings yet

- FIN515 W5 Problem SetDocument3 pagesFIN515 W5 Problem Sethy_saingheng_7602609No ratings yet

- LAVASADocument33 pagesLAVASADeepak Narang100% (1)

- Chapter 9Document14 pagesChapter 9Mritunjay KumarNo ratings yet

- CIBC 2012 Performance at A GlanceDocument194 pagesCIBC 2012 Performance at A GlanceshoagNo ratings yet

- Chapter 1: Overview of Commercial Banks' Loans 1. Overview of Commercial BanksDocument10 pagesChapter 1: Overview of Commercial Banks' Loans 1. Overview of Commercial BanksHuỳnh Lữ Thị NhưNo ratings yet

- DOJ OPINION 72 s.2003Document10 pagesDOJ OPINION 72 s.2003Katleya Kate BelderolNo ratings yet

- ICAG Paper 3 - Advance AuditingDocument57 pagesICAG Paper 3 - Advance AuditingScott MensahNo ratings yet

- Alpha Insurance and Surety v. Reyes, 106 SCRA 274 (1981)Document4 pagesAlpha Insurance and Surety v. Reyes, 106 SCRA 274 (1981)Maria Divina Gracia D. MagtotoNo ratings yet

- OMB Control No. 2900-0086 Respondent Burden: 15 MinutesDocument2 pagesOMB Control No. 2900-0086 Respondent Burden: 15 MinutesPatrickCharlesNo ratings yet

- Introduction Seminar FinanceDocument4 pagesIntroduction Seminar FinanceRana TahirNo ratings yet

Download as pdf or txt

You might also like

- Steps To Discharging Debt CollectionsDocument3 pagesSteps To Discharging Debt Collectionserickutny93% (42)

- Socio-Economic StudyDocument3 pagesSocio-Economic StudygrenadeboiNo ratings yet

- 2017 Exam With SolutionsDocument4 pages2017 Exam With SolutionsMathew YipNo ratings yet

- Prac 1 - First Preboard - P2 65th NewDocument12 pagesPrac 1 - First Preboard - P2 65th NewArianne Llorente100% (1)

- Financial Planning and ForcastingDocument34 pagesFinancial Planning and ForcastingFarhan JagirdarNo ratings yet

- Markets For The Week Ending September 23, 2011: Monetary PolicyDocument10 pagesMarkets For The Week Ending September 23, 2011: Monetary PolicymwarywodaNo ratings yet

- Markets For The Week Ending September 2, 2011: Monetary PolicyDocument8 pagesMarkets For The Week Ending September 2, 2011: Monetary PolicymwarywodaNo ratings yet

- Markets For The Week Ending September 16, 2011: Monetary PolicyDocument10 pagesMarkets For The Week Ending September 16, 2011: Monetary PolicymwarywodaNo ratings yet

- The End For Berlusconi: Morning ReportDocument3 pagesThe End For Berlusconi: Morning Reportnaudaslietas_lvNo ratings yet

- Disagreement About Ecbs Role: Morning ReportDocument3 pagesDisagreement About Ecbs Role: Morning Reportnaudaslietas_lvNo ratings yet

- Unchanged From Boe and Ecb: Morning ReportDocument3 pagesUnchanged From Boe and Ecb: Morning Reportnaudaslietas_lvNo ratings yet

- Brighter in China: Morning ReportDocument3 pagesBrighter in China: Morning Reportnaudaslietas_lvNo ratings yet

- Growth Weakens in China: Morning ReportDocument3 pagesGrowth Weakens in China: Morning Reportnaudaslietas_lvNo ratings yet

- What Will ECB Deliver Today?: Morning ReportDocument3 pagesWhat Will ECB Deliver Today?: Morning Reportnaudaslietas_lvNo ratings yet

- MRE130114Document3 pagesMRE130114naudaslietas_lvNo ratings yet

- Greek Bail-Out Approved: Morning ReportDocument3 pagesGreek Bail-Out Approved: Morning Reportnaudaslietas_lvNo ratings yet

- OECD Wants Action: Morning ReportDocument3 pagesOECD Wants Action: Morning Reportnaudaslietas_lvNo ratings yet

- More Weak Chinese Data: Morning ReportDocument3 pagesMore Weak Chinese Data: Morning Reportnaudaslietas_lvNo ratings yet

- 50 Bps Rate Cut From Norges Bank: Morning ReportDocument3 pages50 Bps Rate Cut From Norges Bank: Morning Reportnaudaslietas_lvNo ratings yet

- Political Pressure On Boj: Morning ReportDocument3 pagesPolitical Pressure On Boj: Morning Reportnaudaslietas_lvNo ratings yet

- No Change Neither From Ecb Nor Boe: Morning ReportDocument3 pagesNo Change Neither From Ecb Nor Boe: Morning Reportnaudaslietas_lvNo ratings yet

- Boe and Ecb On Hold Today: Morning ReportDocument3 pagesBoe and Ecb On Hold Today: Morning Reportnaudaslietas_lvNo ratings yet

- Greek Debt Sale Wins Time For The Troika: Morning ReportDocument3 pagesGreek Debt Sale Wins Time For The Troika: Morning Reportnaudaslietas_lvNo ratings yet

- Italy Still Faces High Borrowing Costs: Morning ReportDocument3 pagesItaly Still Faces High Borrowing Costs: Morning Reportnaudaslietas_lvNo ratings yet

- Can Mario Monti Save Italy?: Morning ReportDocument3 pagesCan Mario Monti Save Italy?: Morning Reportnaudaslietas_lvNo ratings yet

- New Stimulus From Bank of England: Morning ReportDocument3 pagesNew Stimulus From Bank of England: Morning Reportnaudaslietas_lvNo ratings yet

- Banks Loans Record Amount From ECB: Morning ReportDocument3 pagesBanks Loans Record Amount From ECB: Morning Reportnaudaslietas_lvNo ratings yet

- MPC Meetings Today: Morning ReportDocument3 pagesMPC Meetings Today: Morning Reportnaudaslietas_lvNo ratings yet

- Bini Smaghi Talks For More Action: Morning ReportDocument3 pagesBini Smaghi Talks For More Action: Morning Reportnaudaslietas_lvNo ratings yet

- GDP-drop Weakened The Pound: Morning ReportDocument3 pagesGDP-drop Weakened The Pound: Morning Reportnaudaslietas_lvNo ratings yet

- GDP-growth Disappointed in Q2: Morning ReportDocument3 pagesGDP-growth Disappointed in Q2: Morning Reportnaudaslietas_lvNo ratings yet

- More Cautious Market Sentiment: Morning ReportDocument3 pagesMore Cautious Market Sentiment: Morning Reportnaudaslietas_lvNo ratings yet

- MRE111031Document3 pagesMRE111031naudaslietas_lvNo ratings yet

- Yen Weakening Halts: Morning ReportDocument3 pagesYen Weakening Halts: Morning Reportnaudaslietas_lvNo ratings yet

- Progressing US Manufacturers: Morning ReportDocument3 pagesProgressing US Manufacturers: Morning Reportnaudaslietas_lvNo ratings yet

- Draghi Weakened The Euro: Morning ReportDocument2 pagesDraghi Weakened The Euro: Morning Reportnaudaslietas_lvNo ratings yet

- Markets Cheer Euro Zone Deal: Morning ReportDocument3 pagesMarkets Cheer Euro Zone Deal: Morning Reportnaudaslietas_lvNo ratings yet

- Qvigstad Weakened The NOK: Morning ReportDocument3 pagesQvigstad Weakened The NOK: Morning Reportnaudaslietas_lvNo ratings yet

- Recession Fear Returns: Morning ReportDocument3 pagesRecession Fear Returns: Morning Reportnaudaslietas_lvNo ratings yet

- Weak Start On Second Half of 2012: Morning ReportDocument3 pagesWeak Start On Second Half of 2012: Morning Reportnaudaslietas_lvNo ratings yet

- Expects No Rate Cut From ECB: Morning ReportDocument3 pagesExpects No Rate Cut From ECB: Morning Reportnaudaslietas_lvNo ratings yet

- Spain Cuts 65 Billions: Morning ReportDocument3 pagesSpain Cuts 65 Billions: Morning Reportnaudaslietas_lvNo ratings yet

- The Outlook Remains Negative in China: Morning ReportDocument3 pagesThe Outlook Remains Negative in China: Morning Reportnaudaslietas_lvNo ratings yet

- Draghi Punctured Optimism: Morning ReportDocument3 pagesDraghi Punctured Optimism: Morning Reportnaudaslietas_lvNo ratings yet

- No Change From The Riksbank: Morning ReportDocument3 pagesNo Change From The Riksbank: Morning Reportnaudaslietas_lvNo ratings yet

- Morning Report 30oct2014Document2 pagesMorning Report 30oct2014Joseph DavidsonNo ratings yet

- Weakened Confidence in Europe: Morning ReportDocument3 pagesWeakened Confidence in Europe: Morning Reportnaudaslietas_lvNo ratings yet

- Greece Gets Two More Years: Morning ReportDocument3 pagesGreece Gets Two More Years: Morning Reportnaudaslietas_lvNo ratings yet

- Expect Rate Cut in Norway: Morning ReportDocument3 pagesExpect Rate Cut in Norway: Morning Reportnaudaslietas_lvNo ratings yet

- Weaker Yen and More QE in The US: Morning ReportDocument3 pagesWeaker Yen and More QE in The US: Morning Reportnaudaslietas_lvNo ratings yet

- More Stimuli From Central Banks: Morning ReportDocument3 pagesMore Stimuli From Central Banks: Morning Reportnaudaslietas_lvNo ratings yet

- UK Lost AAA-rating: Morning ReportDocument3 pagesUK Lost AAA-rating: Morning Reportnaudaslietas_lvNo ratings yet

- EUR Nears One-Year Low Against USD: Morning ReportDocument3 pagesEUR Nears One-Year Low Against USD: Morning Reportnaudaslietas_lvNo ratings yet

- "Yes, We Have A Deal": Morning ReportDocument3 pages"Yes, We Have A Deal": Morning Reportnaudaslietas_lvNo ratings yet

- IMF Warns About Depression: Morning ReportDocument3 pagesIMF Warns About Depression: Morning Reportnaudaslietas_lvNo ratings yet

- Obama Won The Election: Morning ReportDocument3 pagesObama Won The Election: Morning Reportnaudaslietas_lvNo ratings yet

- Italian Interest Go Sky High: Morning ReportDocument3 pagesItalian Interest Go Sky High: Morning Reportnaudaslietas_lvNo ratings yet

- Large International Banks Downgraded: Morning ReportDocument3 pagesLarge International Banks Downgraded: Morning Reportnaudaslietas_lvNo ratings yet

- Swedish Inflation Drops: Morning ReportDocument3 pagesSwedish Inflation Drops: Morning Reportnaudaslietas_lvNo ratings yet

- Ready To Recapitalize Banks: Morning ReportDocument3 pagesReady To Recapitalize Banks: Morning Reportnaudaslietas_lvNo ratings yet

- Several Important Events This Week: Morning ReportDocument3 pagesSeveral Important Events This Week: Morning Reportnaudaslietas_lvNo ratings yet

- Italy Downgraded by S&P: Morning ReportDocument3 pagesItaly Downgraded by S&P: Morning Reportnaudaslietas_lvNo ratings yet

- MRE120330Document3 pagesMRE120330naudaslietas_lvNo ratings yet

- Asset Rotation: The Demise of Modern Portfolio Theory and the Birth of an Investment RenaissanceFrom EverandAsset Rotation: The Demise of Modern Portfolio Theory and the Birth of an Investment RenaissanceNo ratings yet

- What's Cooking: Digital Transformation of the Agrifood SystemFrom EverandWhat's Cooking: Digital Transformation of the Agrifood SystemNo ratings yet

- Accounting For Companies I: Learning ObjectivesDocument11 pagesAccounting For Companies I: Learning ObjectivesHongWei TeoNo ratings yet

- Introduction To Co-Operative Banking: DefinationDocument9 pagesIntroduction To Co-Operative Banking: DefinationHelloprojectNo ratings yet

- Uppsala Papers in Economic History: 1993 Working Paper No 10Document40 pagesUppsala Papers in Economic History: 1993 Working Paper No 10Michalis RizosNo ratings yet

- Mercial PaperDocument39 pagesMercial PaperArjun Khunt100% (1)

- Neo The United Kingdom of God Sky Earth: Exhibits AbDocument4 pagesNeo The United Kingdom of God Sky Earth: Exhibits AbWORLD MEDIA & COMMUNICATIONSNo ratings yet

- Airports PresentationDocument22 pagesAirports PresentationPulokesh GhoshNo ratings yet

- Urdu SyllabusDocument5 pagesUrdu Syllabusindhu indhuNo ratings yet

- County Wrestles With Tax Hike, Raises: Ledger-NewsDocument28 pagesCounty Wrestles With Tax Hike, Raises: Ledger-Newsspacecat007No ratings yet

- Cred Trans Case Digests Part3Document13 pagesCred Trans Case Digests Part3Ayeesha PagantianNo ratings yet

- Position Review of Port Klang Free Zone Project and Port Klang Free Zone SDN BHDDocument51 pagesPosition Review of Port Klang Free Zone Project and Port Klang Free Zone SDN BHDKenny WongNo ratings yet

- Monetary and Credit Information Review: Issue 10Document4 pagesMonetary and Credit Information Review: Issue 10Anonymous AHW3sHNo ratings yet

- Blackbook Project On Credit Rating SystemDocument88 pagesBlackbook Project On Credit Rating SystemAnkit Chheda0% (1)

- 2.1 CommissionDocument28 pages2.1 CommissionAnali Barbon100% (1)

- LSCC Final Bill CC FormDocument3 pagesLSCC Final Bill CC Formకొల్లి రాఘవేణిNo ratings yet

- Ibm 5Document4 pagesIbm 5Shrinidhi HariharasuthanNo ratings yet

- FIN515 W5 Problem SetDocument3 pagesFIN515 W5 Problem Sethy_saingheng_7602609No ratings yet

- LAVASADocument33 pagesLAVASADeepak Narang100% (1)

- Chapter 9Document14 pagesChapter 9Mritunjay KumarNo ratings yet

- CIBC 2012 Performance at A GlanceDocument194 pagesCIBC 2012 Performance at A GlanceshoagNo ratings yet

- Chapter 1: Overview of Commercial Banks' Loans 1. Overview of Commercial BanksDocument10 pagesChapter 1: Overview of Commercial Banks' Loans 1. Overview of Commercial BanksHuỳnh Lữ Thị NhưNo ratings yet

- DOJ OPINION 72 s.2003Document10 pagesDOJ OPINION 72 s.2003Katleya Kate BelderolNo ratings yet

- ICAG Paper 3 - Advance AuditingDocument57 pagesICAG Paper 3 - Advance AuditingScott MensahNo ratings yet

- Alpha Insurance and Surety v. Reyes, 106 SCRA 274 (1981)Document4 pagesAlpha Insurance and Surety v. Reyes, 106 SCRA 274 (1981)Maria Divina Gracia D. MagtotoNo ratings yet

- OMB Control No. 2900-0086 Respondent Burden: 15 MinutesDocument2 pagesOMB Control No. 2900-0086 Respondent Burden: 15 MinutesPatrickCharlesNo ratings yet

- Introduction Seminar FinanceDocument4 pagesIntroduction Seminar FinanceRana TahirNo ratings yet