Download as docx, pdf, or txt

You might also like

- (Ey) Entrance Test & AnswerDocument45 pages(Ey) Entrance Test & AnswerLê Quang Trung100% (5)

- Deloitte Entrance Test: I. ACCOUNTING (20 Questions)Document117 pagesDeloitte Entrance Test: I. ACCOUNTING (20 Questions)Uahnbu Tran100% (4)

- Deloitte Full Test 1 ADocument12 pagesDeloitte Full Test 1 ATrúc Phương100% (3)

- KPMG Entrance Intern Test I. Multiple Choice QuestionDocument5 pagesKPMG Entrance Intern Test I. Multiple Choice QuestionNam Nguyễn Tiến100% (1)

- Projected Operating Costs, Manual Process: Inflatio Mexico 7% Tax Rate 35%Document4 pagesProjected Operating Costs, Manual Process: Inflatio Mexico 7% Tax Rate 35%Cesar Camey100% (1)

- Instant Download Ebook PDF Fundamentals of Corporate Finance Third Canadian 3rd Edition PDF ScribdDocument42 pagesInstant Download Ebook PDF Fundamentals of Corporate Finance Third Canadian 3rd Edition PDF Scribdwalter.herbert733100% (49)

- Principles of Auditing An Introduction To International Standards On Auditing 3rd Edition Hayes Solu 190402061241Document32 pagesPrinciples of Auditing An Introduction To International Standards On Auditing 3rd Edition Hayes Solu 190402061241Nia100% (2)

- Sapp - Ey Entrance Test AnswerDocument21 pagesSapp - Ey Entrance Test AnswerTran Pham Quoc Thuy100% (2)

- Chapter 7 Solution Manual Auditing and Assurance ServicesDocument34 pagesChapter 7 Solution Manual Auditing and Assurance ServicesMāhmõūd Āhmēd100% (2)

- Sapp - PWC Entrance Test AnswerDocument9 pagesSapp - PWC Entrance Test AnswerAnh Thy Nguyễn Hoàng100% (1)

- (Deloitte) Entrance Test & AnswerDocument36 pages(Deloitte) Entrance Test & AnswerLê Quang Trung75% (4)

- Sapp - KPMG Entrance Test Answer PDFDocument11 pagesSapp - KPMG Entrance Test Answer PDFTran Pham Quoc ThuyNo ratings yet

- Oriental Investments (SH) Pte LTD V Catalla Investments Pte LTD PDFDocument35 pagesOriental Investments (SH) Pte LTD V Catalla Investments Pte LTD PDFHenderikTanYiZhouNo ratings yet

- Solution Manual Principles of Auditing 2nd Edition HayesDocument25 pagesSolution Manual Principles of Auditing 2nd Edition Hayeschachaeyescha67% (3)

- Group Assignment Assignment Overview:: 1. Company Background ResearchDocument2 pagesGroup Assignment Assignment Overview:: 1. Company Background ResearchCarla Mae MartinezNo ratings yet

- Sapp - Ey Entrance TestDocument21 pagesSapp - Ey Entrance TestTran Pham Quoc Thuy100% (1)

- Sapp - KPMG Entrance TestDocument12 pagesSapp - KPMG Entrance TestTran Pham Quoc ThuyNo ratings yet

- Sapp - Deloitte Entrance TestDocument19 pagesSapp - Deloitte Entrance TestTran Pham Quoc ThuyNo ratings yet

- (KPMG) Entrance Test & AnswerDocument25 pages(KPMG) Entrance Test & AnswerThanh Tung100% (1)

- Sapp - Deloitte Entrance Test AnswerDocument17 pagesSapp - Deloitte Entrance Test AnswerTran Pham Quoc ThuyNo ratings yet

- Assignment 5 Sistem Informasi Akuntansi: SoalDocument4 pagesAssignment 5 Sistem Informasi Akuntansi: Soalpatrecia 1896No ratings yet

- Case 7-1Document6 pagesCase 7-1congNo ratings yet

- Contoh Soal Audit Pilihan GandaDocument53 pagesContoh Soal Audit Pilihan Gandaerny2412No ratings yet

- Soal Indirect N MutualDocument9 pagesSoal Indirect N MutualarifNo ratings yet

- Instructor Resource Manual: Auditing CasesDocument11 pagesInstructor Resource Manual: Auditing Caseslina_siscanu63560% (2)

- To Take Into Account 2Document8 pagesTo Take Into Account 2Omaira DiazNo ratings yet

- (SAPP) F3 Mock Exam With Answer PDFDocument24 pages(SAPP) F3 Mock Exam With Answer PDFLong NgoNo ratings yet

- Kunci Jawaban ICAEW Part 2Document4 pagesKunci Jawaban ICAEW Part 2Dendi RiskiNo ratings yet

- NY Business Law Journal - Atty. Wallshein Article On Advanced Standing Issues in Securitized MortgagesDocument8 pagesNY Business Law Journal - Atty. Wallshein Article On Advanced Standing Issues in Securitized Mortgages83jjmackNo ratings yet

- EY ENTRANCE TEST final-ACE THE FUTUREDocument18 pagesEY ENTRANCE TEST final-ACE THE FUTURETrà Hương100% (1)

- Final Test - Deloitte Audit - Q - 3.19.2018Document14 pagesFinal Test - Deloitte Audit - Q - 3.19.2018ĐẶNG THỊ THU HÀNo ratings yet

- Deloitte Full Test 1 QDocument13 pagesDeloitte Full Test 1 QNi LelanNo ratings yet

- Final Test - KPMG - Q - 3.19.2018Document10 pagesFinal Test - KPMG - Q - 3.19.2018ĐẶNG THỊ THU HÀNo ratings yet

- Ey-Entrance-Test 21.22Document22 pagesEy-Entrance-Test 21.22Vũ Tăng ThếNo ratings yet

- Big4. Recruitment Test.Document13 pagesBig4. Recruitment Test.Đoàn DungNo ratings yet

- Sapp - Deloitte Entrance TestDocument19 pagesSapp - Deloitte Entrance TestKim Ngan LeNo ratings yet

- (PWC) Entrance Test & AnswerDocument16 pages(PWC) Entrance Test & AnswerLê Quang TrungNo ratings yet

- EY Written Test SyllabusDocument4 pagesEY Written Test SyllabusAishwarya KarthikeyanNo ratings yet

- Deloitte-Entrance-Test 21.22Document20 pagesDeloitte-Entrance-Test 21.22Vũ Tăng ThếNo ratings yet

- Kpmg-Entrance-Test 21.22Document13 pagesKpmg-Entrance-Test 21.22Vũ Tăng ThếNo ratings yet

- Application Form: Applied Division: Employment StatusDocument3 pagesApplication Form: Applied Division: Employment StatusHealthy HabitsNo ratings yet

- Audit Postulates: Financial Statements and Financial Data Are VerifiableDocument1 pageAudit Postulates: Financial Statements and Financial Data Are VerifiablePhebieon Mukwenha100% (1)

- Kaplan Chapter 2: IAS 16 Property, Plant and EquipmentDocument11 pagesKaplan Chapter 2: IAS 16 Property, Plant and EquipmentRaihan SirNo ratings yet

- PWC AptitudeDocument4 pagesPWC AptitudeSALONI BHATIA 2019017No ratings yet

- Week 2 Assessment: Accounting For Business CombinationsDocument12 pagesWeek 2 Assessment: Accounting For Business Combinationstasya salfiraNo ratings yet

- IA Quiz ImadeDocument4 pagesIA Quiz ImadeKuro ZetsuNo ratings yet

- Tugas Audit Fix Bener Semua PDFDocument19 pagesTugas Audit Fix Bener Semua PDF「絆笑」HodaeNo ratings yet

- Jawaban Quiz 3 AKM Kelas C - Amanda G Erari - F0320007Document2 pagesJawaban Quiz 3 AKM Kelas C - Amanda G Erari - F0320007Amanda Givelline ErariNo ratings yet

- Kieso Ifrs Testbank ch17Document44 pagesKieso Ifrs Testbank ch17Turan, Jel Therese A.No ratings yet

- Test ch7 Audit Test BankDocument45 pagesTest ch7 Audit Test BankFlorenz Nicole Palisoc0% (1)

- AkkeuDocument6 pagesAkkeuMedlin Yustisia RirringNo ratings yet

- 11 24 ArensDocument3 pages11 24 ArenstsziNo ratings yet

- Problem (Objective 20-5) Alyssa Ghose Is Auditing Payroll Accruals For A Manufacturing Company. The ClientDocument2 pagesProblem (Objective 20-5) Alyssa Ghose Is Auditing Payroll Accruals For A Manufacturing Company. The ClientNana BananaNo ratings yet

- Deloitte Mock Aptitude Test - Docx1Document3 pagesDeloitte Mock Aptitude Test - Docx1Anonymous ZVbwfcNo ratings yet

- Chapter 6 and 7 NR and BPDocument2 pagesChapter 6 and 7 NR and BPCa Ada100% (1)

- Financial Accounting - Tugas 2 - 9 Oktober 2019Document3 pagesFinancial Accounting - Tugas 2 - 9 Oktober 2019AlfiyanNo ratings yet

- Audit Case StudiesDocument18 pagesAudit Case StudiesAanand ALNo ratings yet

- 2014 - Lembar Jawaban Soal Latihan Cpa Exam - CoverDocument3 pages2014 - Lembar Jawaban Soal Latihan Cpa Exam - CoverNasrullah Djamil, SE, M.Si, Akt, CA100% (5)

- Prepare TestDocument17 pagesPrepare TestTrà Hương100% (1)

- MOCK TEST F7_AnswersDocument31 pagesMOCK TEST F7_Answerskhoanguyen0973647No ratings yet

- Do Not Turn Over This Question Paper Until You Are Told To Do SoDocument17 pagesDo Not Turn Over This Question Paper Until You Are Told To Do SoMin HeoNo ratings yet

- Diagnostic Exam 1 23 AKDocument11 pagesDiagnostic Exam 1 23 AKAbegail Kaye BiadoNo ratings yet

- Deloitte TestDocument19 pagesDeloitte TestTrà HươngNo ratings yet

- AF208 F2F Exam 15Document17 pagesAF208 F2F Exam 15savoupNo ratings yet

- Chapter 4 The Time Value of MoneyDocument39 pagesChapter 4 The Time Value of MoneyQuỳnh NguyễnNo ratings yet

- From: To:: Annexure-ADocument3 pagesFrom: To:: Annexure-AAnilNo ratings yet

- Abdul Sattar 2018Document48 pagesAbdul Sattar 2018ABDUL sattarNo ratings yet

- A Brief Introduction To The KMI-30 Index and Stock Screening Process For Shariah ComplianceDocument12 pagesA Brief Introduction To The KMI-30 Index and Stock Screening Process For Shariah ComplianceAbdul RafayNo ratings yet

- Ch.1 Business CombinationsDocument29 pagesCh.1 Business CombinationsdhfbbbbbbbbbbbbbbbbbhNo ratings yet

- Question of Cost of CapitalDocument3 pagesQuestion of Cost of CapitalAngel Atia IbnatNo ratings yet

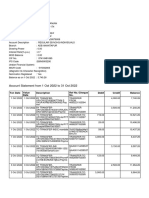

- Account Statement From 1 Jan 2018 To 31 Jan 2018: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 1 Jan 2018 To 31 Jan 2018: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceATULNo ratings yet

- Bañas vs. Asia Pacific Corp., 343 SCRA 527 October 18, 2000 TEODORO BAÑASDocument39 pagesBañas vs. Asia Pacific Corp., 343 SCRA 527 October 18, 2000 TEODORO BAÑASRizza Mae EudNo ratings yet

- Stock Market For Beginners 2022 - Step by Step CDocument49 pagesStock Market For Beginners 2022 - Step by Step Cdaniel nicolaeNo ratings yet

- Accounting Formats For Cambridge Igcse CompressDocument11 pagesAccounting Formats For Cambridge Igcse Compresslegendza010No ratings yet

- Problem Solving 1Document3 pagesProblem Solving 1Heap Ke XinNo ratings yet

- Ifrs 1 First Time AdoptionDocument27 pagesIfrs 1 First Time Adoptionesulawyer2001No ratings yet

- All Your Answers Should Be On An Excel Sheet. Show Your Calculation Process.Document6 pagesAll Your Answers Should Be On An Excel Sheet. Show Your Calculation Process.Adi SadiNo ratings yet

- Branch Banking Vs Unit BankingDocument7 pagesBranch Banking Vs Unit BankingBoruah SwapnaNo ratings yet

- Niruword 3Document11 pagesNiruword 3Raju BhaiNo ratings yet

- PT. MULTIMEDIA TECHNOLOGY COMP (BB) - Dikonversi PDFDocument2 pagesPT. MULTIMEDIA TECHNOLOGY COMP (BB) - Dikonversi PDFBulan julpi suwelly100% (1)

- Financial and Monetary Policies in Ghana: A Review of Recent TrendsDocument11 pagesFinancial and Monetary Policies in Ghana: A Review of Recent TrendsrytchluvNo ratings yet

- Accounting Entries For Issuance & Payment of DDDocument2 pagesAccounting Entries For Issuance & Payment of DDSamra QasimNo ratings yet

- Commission StructureDocument3 pagesCommission StructureRandom ManiacNo ratings yet

- The Bottom Line July 2023Document25 pagesThe Bottom Line July 2023Vinayak ChaturvediNo ratings yet

- 2014 AFP Treasury in Practice Guide Bank Account Reconciliation 3Document7 pages2014 AFP Treasury in Practice Guide Bank Account Reconciliation 3Ar TiNo ratings yet

- FIN202 - SU23 - Individual AssignmentDocument8 pagesFIN202 - SU23 - Individual AssignmentÁnh Dương NguyễnNo ratings yet

- What Is An Automated Teller MachineDocument7 pagesWhat Is An Automated Teller MachineNeha SoningraNo ratings yet

- FM II 2022 Assignment IDocument7 pagesFM II 2022 Assignment IAmanuel AbebawNo ratings yet

- Management of Non Performing Assests in Tiruchirapalli District Central Co-Operative Bank LTDDocument6 pagesManagement of Non Performing Assests in Tiruchirapalli District Central Co-Operative Bank LTDYadunandan NandaNo ratings yet

- Way2wealth Org Study Report 8 Nov 2022Document65 pagesWay2wealth Org Study Report 8 Nov 2022Manu DvNo ratings yet