Download as pdf or txt

You might also like

- Imperial Administrative Records, Part IDocument323 pagesImperial Administrative Records, Part IHECTOR ORTEGANo ratings yet

- M001 - Level 1 - Accounting Principles and Procedures.Document3 pagesM001 - Level 1 - Accounting Principles and Procedures.nishantdon007No ratings yet

- Understanding Financial Statements (Review and Analysis of Straub's Book)From EverandUnderstanding Financial Statements (Review and Analysis of Straub's Book)Rating: 5 out of 5 stars5/5 (5)

- Differences Between Organization ChangeDocument3 pagesDifferences Between Organization ChangehksNo ratings yet

- Lecture 1. Ratio Analysis Financial AppraisalDocument11 pagesLecture 1. Ratio Analysis Financial AppraisaltiiworksNo ratings yet

- Report in Business Finance: Group 2 - Review of Financial Statement Preparation, Analysis, and InterpretationDocument14 pagesReport in Business Finance: Group 2 - Review of Financial Statement Preparation, Analysis, and InterpretationKOUJI N. MARQUEZNo ratings yet

- FNCE Assignment Week 6Document10 pagesFNCE Assignment Week 6Rajeev ShahdadpuriNo ratings yet

- Financial Statement AnalysisDocument14 pagesFinancial Statement AnalysisJomar TeofiloNo ratings yet

- Alk Bab 4Document5 pagesAlk Bab 4RAFLI RIFALDI -No ratings yet

- Income Statements:: Financial Statement AnalysisDocument11 pagesIncome Statements:: Financial Statement AnalysisSerge Olivier Atchu YudomNo ratings yet

- Ratios and Formulas in Customer Financial AnalysisDocument11 pagesRatios and Formulas in Customer Financial AnalysisPrince Kumar100% (1)

- Q/A: 4 Ways Investment Firms Make Money: Investment Banking Investing and Lending Client Services Investment Management 1. What Is Investment BankingDocument4 pagesQ/A: 4 Ways Investment Firms Make Money: Investment Banking Investing and Lending Client Services Investment Management 1. What Is Investment BankingkrstupNo ratings yet

- Calculations and Interpretations of 14 Key Financial RatiosDocument6 pagesCalculations and Interpretations of 14 Key Financial RatioswarishaaNo ratings yet

- Income Statements:: Financial Statement AnalysisDocument11 pagesIncome Statements:: Financial Statement AnalysisAsim MahatoNo ratings yet

- Income Statement and Accrual AccountingDocument7 pagesIncome Statement and Accrual AccountingJordan Neo Yu Hern100% (1)

- Accounting Fundamentals IIDocument9 pagesAccounting Fundamentals IIShivaprasad HooliNo ratings yet

- Importance of Financial StatementDocument11 pagesImportance of Financial StatementJAY SHUKLANo ratings yet

- AEC 6 - Financial ManagementDocument6 pagesAEC 6 - Financial ManagementRhea May BaluteNo ratings yet

- Financial AnalysisDocument22 pagesFinancial Analysisnomaan khanNo ratings yet

- Management Control Systems: University Question - AnswersDocument19 pagesManagement Control Systems: University Question - AnswersvaishalikatkadeNo ratings yet

- Profitability AnalysisDocument12 pagesProfitability AnalysisJudyeast AstillaNo ratings yet

- Financial RatiosDocument21 pagesFinancial RatiosAamir Hussian100% (1)

- Study MaterialDocument9 pagesStudy MaterialJAYNo ratings yet

- Ulas in Customer Financial Analysis: Liquidity RatiosDocument9 pagesUlas in Customer Financial Analysis: Liquidity RatiosVarun GandhiNo ratings yet

- Chapter 2 Review of Financial Statement Preparation Analysis InterpretationDocument46 pagesChapter 2 Review of Financial Statement Preparation Analysis InterpretationMark DavidNo ratings yet

- Assignment 4 Management 4300Document3 pagesAssignment 4 Management 4300Victor Marcos HyslopNo ratings yet

- Main RatiosDocument2 pagesMain RatiosMansoor Al KabiNo ratings yet

- Masan Group CorporationDocument31 pagesMasan Group Corporationhồ nam longNo ratings yet

- Sample Operational Financial Analysis ReportDocument13 pagesSample Operational Financial Analysis Reportshivkumara27No ratings yet

- Financial Management (1 Day, P.M.)Document12 pagesFinancial Management (1 Day, P.M.)simon berksNo ratings yet

- How To Evaluate FSDocument8 pagesHow To Evaluate FSStephany PolinarNo ratings yet

- BCOM 111 Topic Analysis and Interpretation of Financial StatementsDocument13 pagesBCOM 111 Topic Analysis and Interpretation of Financial Statementskitderoger_391648570No ratings yet

- Imp RatioDocument6 pagesImp RatiofejalNo ratings yet

- Practical 4 Preparation of Balance Sheet of Broiler in Chitwan District ObjectivesDocument16 pagesPractical 4 Preparation of Balance Sheet of Broiler in Chitwan District ObjectivesPurna DhanukNo ratings yet

- Explain On Financial of A Stock According To R P NWDocument2 pagesExplain On Financial of A Stock According To R P NWSurjit KhomdramNo ratings yet

- Economic Entity AssumptionDocument4 pagesEconomic Entity AssumptionNouman KhanNo ratings yet

- Ratio Analysis TabularDocument4 pagesRatio Analysis TabularKhondaker RiyadhNo ratings yet

- CH 2 - EarningsDocument10 pagesCH 2 - Earnings李承翰No ratings yet

- Income STDocument23 pagesIncome STKholoud LabadyNo ratings yet

- CH 5 - Fin RatiosDocument18 pagesCH 5 - Fin RatiosbavanthinilNo ratings yet

- F2 Chapter 18Document0 pagesF2 Chapter 18Swaita SahaNo ratings yet

- Analyzing Your Financial RatiosDocument38 pagesAnalyzing Your Financial Ratiossakthivels08No ratings yet

- Banking ReviewerDocument4 pagesBanking ReviewerRaymark MejiaNo ratings yet

- Ratios Gross Profit MarginDocument7 pagesRatios Gross Profit MarginBrill brianNo ratings yet

- FM-II-CH-1 Capital Structure and LeverageDocument14 pagesFM-II-CH-1 Capital Structure and LeverageAschalew Ye Giwen LijiNo ratings yet

- Managerial Finance, Financial Accounting and Analysis For Engineering Managers PDFDocument5 pagesManagerial Finance, Financial Accounting and Analysis For Engineering Managers PDFAshuriko KazuNo ratings yet

- CAHPTER 3. Analisis Keuangan (Analysis of Financial Statements) MankeuDocument12 pagesCAHPTER 3. Analisis Keuangan (Analysis of Financial Statements) MankeuKezia NatashaNo ratings yet

- Sample Operational Financial Analysis ReportDocument8 pagesSample Operational Financial Analysis ReportValentinorossiNo ratings yet

- Accounting Ratios Am 71 80Document36 pagesAccounting Ratios Am 71 80Sandy100% (1)

- 20090827120835BBFA2203 Topic 1Document22 pages20090827120835BBFA2203 Topic 1adwin_thomasNo ratings yet

- Ratio Analysis Is A Form of FinancialDocument18 pagesRatio Analysis Is A Form of FinancialAmrutha AyinavoluNo ratings yet

- Lec 14 Fin Perf ManagementDocument21 pagesLec 14 Fin Perf ManagementHaroon RashidNo ratings yet

- Chapter 11 Valuation MethodDocument34 pagesChapter 11 Valuation Methodmansisharma8301No ratings yet

- Ratio AnalysisDocument17 pagesRatio AnalysisFrank Agbeko TorhoNo ratings yet

- Vajrapu Lakshmi Priya - Accountng For ManagersDocument7 pagesVajrapu Lakshmi Priya - Accountng For ManagersGramoday FruitsNo ratings yet

- Unit-Iii Fnancial Analysis Financial AppraisalDocument5 pagesUnit-Iii Fnancial Analysis Financial AppraisalumaushaNo ratings yet

- Financial Accounting MasterDocument80 pagesFinancial Accounting Mastertimbuc202No ratings yet

- Sevilla, Renz Marie A. Bsba FM 2-C: Assignment # 2Document4 pagesSevilla, Renz Marie A. Bsba FM 2-C: Assignment # 2Gerald Noveda RomanNo ratings yet

- Financial Ratio AnalysisDocument12 pagesFinancial Ratio AnalysisKamlesh Kumar KhiyataniNo ratings yet

- Bitumen Some HistoryDocument3 pagesBitumen Some HistoryHECTOR ORTEGANo ratings yet

- Dating The Subterranean Passage at The PDocument12 pagesDating The Subterranean Passage at The PHECTOR ORTEGANo ratings yet

- MALIK The Corrections of Codex Sinaiticus and The Textual Transmission of Revelation Josef Schmid Revisited RevisedDocument27 pagesMALIK The Corrections of Codex Sinaiticus and The Textual Transmission of Revelation Josef Schmid Revisited RevisedHECTOR ORTEGANo ratings yet

- ch01Document20 pagesch01HECTOR ORTEGANo ratings yet

- 4 ELE Chapter 6 y 4. Profitability and Return Ratios (B)Document28 pages4 ELE Chapter 6 y 4. Profitability and Return Ratios (B)HECTOR ORTEGANo ratings yet

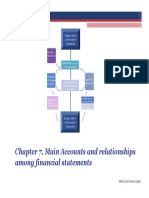

- 6 ELE Chapter 7. Relationships Among Financial StatementsDocument39 pages6 ELE Chapter 7. Relationships Among Financial StatementsHECTOR ORTEGANo ratings yet

- N.H. Snaith. 1962. "The Ben Asher Text." Textus, 2, Pp. 8-13Document6 pagesN.H. Snaith. 1962. "The Ben Asher Text." Textus, 2, Pp. 8-13HECTOR ORTEGANo ratings yet

- Chapter 1 - Exercises Part BDocument7 pagesChapter 1 - Exercises Part BHECTOR ORTEGANo ratings yet

- A Diggers Life EbookDocument59 pagesA Diggers Life EbookHECTOR ORTEGANo ratings yet

- By Rev. Theo. G. Soares, PH.D.,: Galesburg, IllDocument11 pagesBy Rev. Theo. G. Soares, PH.D.,: Galesburg, IllHECTOR ORTEGANo ratings yet

- C. Rabin. 1962. "The Ancient Versions and The Indefinite Subject." Textus, 2, Pp. 60-76.Document17 pagesC. Rabin. 1962. "The Ancient Versions and The Indefinite Subject." Textus, 2, Pp. 60-76.HECTOR ORTEGANo ratings yet

- S. Talmon. 1962. "The Three Scrolls of The Law That Were Found in The Temple Court." Textus, 2, Pp. 14-27.Document14 pagesS. Talmon. 1962. "The Three Scrolls of The Law That Were Found in The Temple Court." Textus, 2, Pp. 14-27.HECTOR ORTEGANo ratings yet

- G.R. Driver. 1960. "Abbreviations in The MassoreticText." Textus, 1, Pp. 112-131Document20 pagesG.R. Driver. 1960. "Abbreviations in The MassoreticText." Textus, 1, Pp. 112-131HECTOR ORTEGANo ratings yet

- J. Shunary. 1962. "An Arabic Tafsīr of The Song of Deborah." Textus, 2, Pp. 77-86Document10 pagesJ. Shunary. 1962. "An Arabic Tafsīr of The Song of Deborah." Textus, 2, Pp. 77-86HECTOR ORTEGANo ratings yet

- S. Talmon. 1960. "Double Readings in The Massoretic Text." Textus, 1, Pp. 144-184Document41 pagesS. Talmon. 1960. "Double Readings in The Massoretic Text." Textus, 1, Pp. 144-184HECTOR ORTEGANo ratings yet

- M.H. Goshen-Gottstein. 1960. "The Authenticity of The Aleppo Codex." Textus, 1, Pp. 17-58Document42 pagesM.H. Goshen-Gottstein. 1960. "The Authenticity of The Aleppo Codex." Textus, 1, Pp. 17-58HECTOR ORTEGANo ratings yet

- Kahle. 1962. "Pre-Massoretic Hebrew." Textus, 2, Pp. 1-7.Document7 pagesKahle. 1962. "Pre-Massoretic Hebrew." Textus, 2, Pp. 1-7.HECTOR ORTEGANo ratings yet

- B. Kedar-Kopfstein. 1962. "A Note On Isaiah XIV, 31." Textus, 2, Pp. 143-145Document3 pagesB. Kedar-Kopfstein. 1962. "A Note On Isaiah XIV, 31." Textus, 2, Pp. 143-145HECTOR ORTEGANo ratings yet

- 1 Timothy 4, Photo Companion BiblePlacesDocument67 pages1 Timothy 4, Photo Companion BiblePlacesHECTOR ORTEGANo ratings yet

- D.S .Loewinger. 1960. "The Aleppo Codex and The Ben Asher Tradition." Textus, 1, Pp. 59-111.Document53 pagesD.S .Loewinger. 1960. "The Aleppo Codex and The Ben Asher Tradition." Textus, 1, Pp. 59-111.HECTOR ORTEGANo ratings yet

- Powers of Darkness Principalities Po...Document201 pagesPowers of Darkness Principalities Po...HECTOR ORTEGA100% (3)

- 369441-Text de L'article-532360-1-10-20200602Document40 pages369441-Text de L'article-532360-1-10-20200602HECTOR ORTEGANo ratings yet

- 174 The Greek Biblical Texts From The JuDocument28 pages174 The Greek Biblical Texts From The JuHECTOR ORTEGANo ratings yet

- 279 The Use of The Earliest Greek ScriptDocument20 pages279 The Use of The Earliest Greek ScriptHECTOR ORTEGANo ratings yet

- 2018 The Nude at The Entrance ContextualDocument23 pages2018 The Nude at The Entrance ContextualHECTOR ORTEGANo ratings yet

- The Correspondence of Sargon II, Part IIDocument319 pagesThe Correspondence of Sargon II, Part IIHECTOR ORTEGANo ratings yet

- A History of The Babylonians and Assyrians (George Stephen Goodspeed)Document242 pagesA History of The Babylonians and Assyrians (George Stephen Goodspeed)HECTOR ORTEGANo ratings yet

- Kosher Fat: Mony Almalech (NBU)Document47 pagesKosher Fat: Mony Almalech (NBU)HECTOR ORTEGANo ratings yet

- Nippon SteelDocument7 pagesNippon SteelAnonymous 9PIxHy13No ratings yet

- Software Quality Assurance: Lecture # 6Document37 pagesSoftware Quality Assurance: Lecture # 6rabiaNo ratings yet

- Ziehl Neelsen Staining - Principle, Procedure and Interpretations - HowMedDocument4 pagesZiehl Neelsen Staining - Principle, Procedure and Interpretations - HowMedMeenachi ChidambaramNo ratings yet

- Endocrine SystemDocument11 pagesEndocrine SystemDayledaniel SorvetoNo ratings yet

- CTPaper IIDocument118 pagesCTPaper IIMahmoud MansourNo ratings yet

- Feedback XI G PRA MID-TERM EP 2Document8 pagesFeedback XI G PRA MID-TERM EP 2Syifa KamilaNo ratings yet

- Zeus - AntipasDocument2 pagesZeus - AntipasPaw LabadiaNo ratings yet

- The Ayurveda Encyclopedia - Natural Secrets To Healing, PreventionDocument10 pagesThe Ayurveda Encyclopedia - Natural Secrets To Healing, PreventionBhushan100% (2)

- Tariqah Muammadiyyah As Tariqah Jami ADocument36 pagesTariqah Muammadiyyah As Tariqah Jami AUzairNo ratings yet

- Gopi EnglishDocument31 pagesGopi EnglishGopi ShankarNo ratings yet

- Group 112-111 My Daily RoutineDocument9 pagesGroup 112-111 My Daily Routineapi-306090241No ratings yet

- Cbet Curriculum RegulationsDocument15 pagesCbet Curriculum RegulationsCharles OndiekiNo ratings yet

- Sant Rajinder Singh Ji Maharaj - Visions of The New MilleniumDocument8 pagesSant Rajinder Singh Ji Maharaj - Visions of The New MilleniumjjcalderNo ratings yet

- Introductions To Valuation Methods and Requirements 1672683839Document51 pagesIntroductions To Valuation Methods and Requirements 1672683839v7qksq5bzg100% (1)

- Nokia Siemens Networks Flexitrunk Brochure Low-Res 15032013Document4 pagesNokia Siemens Networks Flexitrunk Brochure Low-Res 15032013chadi_lbNo ratings yet

- 102 192 1 SMDocument8 pages102 192 1 SMLinaNo ratings yet

- ProfileDocument21 pagesProfileasersamuel21No ratings yet

- Darft Pas Xii GasalDocument11 pagesDarft Pas Xii GasalMutia ChimoetNo ratings yet

- HexWeb HRH10 DataSheet EuDocument6 pagesHexWeb HRH10 DataSheet EuMatijaNo ratings yet

- DLL - Mathematics 6 - Q4 - W2Document8 pagesDLL - Mathematics 6 - Q4 - W2RirinNo ratings yet

- Needle Metal Contamination Control SOP 2Document16 pagesNeedle Metal Contamination Control SOP 2vikkas vermaNo ratings yet

- The SNG Blueprint Part 1 PDFDocument26 pagesThe SNG Blueprint Part 1 PDFAdrian PatrikNo ratings yet

- DJ Lemon (Official Profile 2013)Document6 pagesDJ Lemon (Official Profile 2013)Monica Kshirsagar100% (1)

- Research Proposal SMEs and SMPs AppDocument7 pagesResearch Proposal SMEs and SMPs AppKebede MergaNo ratings yet

- Facts On Why Homework Is Bad For YouDocument7 pagesFacts On Why Homework Is Bad For Youafmsxohtq100% (1)

- Quiz Bank Recon and Proof of CashDocument3 pagesQuiz Bank Recon and Proof of CashAlexander ONo ratings yet

- Sociology 13th Edition Macionis Test BankDocument20 pagesSociology 13th Edition Macionis Test Bankdoctorsantalumu9coab100% (34)

- IIAS 1.0.21 - Columnar Incremental Schema Backup and Restore Feature - 1Document12 pagesIIAS 1.0.21 - Columnar Incremental Schema Backup and Restore Feature - 1HS UFNo ratings yet

- 2410014738242451Document2 pages2410014738242451abdul wahabNo ratings yet