Download as pdf or txt

You might also like

- Bm461, Cw1 PestelDocument6 pagesBm461, Cw1 PestelMarui NNo ratings yet

- 11 DOF BLGF Local Revenue Generation and LGU ForecastingDocument20 pages11 DOF BLGF Local Revenue Generation and LGU ForecastingDilg Sadakbayan100% (3)

- JCB Case StudyDocument9 pagesJCB Case StudyPanma PatelNo ratings yet

- Audit Report Real Property TaxDocument6 pagesAudit Report Real Property TaxJomar Villena0% (1)

- PFMIP 2017 New Format-LGUsDocument32 pagesPFMIP 2017 New Format-LGUsGenalyn Española Gantalao DuranoNo ratings yet

- Revenue Memorandum Order No. 4-2002Document8 pagesRevenue Memorandum Order No. 4-2002ricohizon99No ratings yet

- 2020 CBO IRS Enforcement ReportDocument40 pages2020 CBO IRS Enforcement ReportStephen LoiaconiNo ratings yet

- Budget Decentralization - BLGF PresentationDocument15 pagesBudget Decentralization - BLGF PresentationRegie PascuaNo ratings yet

- RMO No. 27-2022Document8 pagesRMO No. 27-2022john carlo UncianoNo ratings yet

- Central Action Plan 2021-22Document73 pagesCentral Action Plan 2021-22raj27385No ratings yet

- 62983rmo 5-2012Document14 pages62983rmo 5-2012Mark Dennis JovenNo ratings yet

- Ctax e PN 2014 15 PDFDocument49 pagesCtax e PN 2014 15 PDFAncy RajNo ratings yet

- Note 6Document55 pagesNote 6sohamdivekar9867No ratings yet

- Corportate Tax Statistics 2023Document87 pagesCorportate Tax Statistics 2023lucienne.cs18No ratings yet

- P05 Tas 2023Document23 pagesP05 Tas 2023lamerqaNo ratings yet

- RMO No. 2-2022Document2 pagesRMO No. 2-2022Premiumly SoloNo ratings yet

- Local Revenue Generation and LGU ForecastingDocument17 pagesLocal Revenue Generation and LGU ForecastingRichard Mendez100% (1)

- BEPS Implementation in Indonesia - Webinar BPPK - v3Document19 pagesBEPS Implementation in Indonesia - Webinar BPPK - v3tonitoni27No ratings yet

- d119378 PDFDocument100 pagesd119378 PDFCecilia CasalNo ratings yet

- 10 POA 8 - Effective Revenue ManagementDocument15 pages10 POA 8 - Effective Revenue Managementapriano30No ratings yet

- Mind The (Tax) Gap-Its Bigger Than You Probably Think! Tax Gap Research: Concepts, Methodologies and FindingsDocument37 pagesMind The (Tax) Gap-Its Bigger Than You Probably Think! Tax Gap Research: Concepts, Methodologies and Findingsxilo10No ratings yet

- Tracking Table DBMDocument3 pagesTracking Table DBMTalaingod MPDONo ratings yet

- Riverside County Response To Grand Jury Report On KPMGDocument11 pagesRiverside County Response To Grand Jury Report On KPMGThe Press-Enterprise / pressenterprise.comNo ratings yet

- APS - Qccs Profile - V1Document5 pagesAPS - Qccs Profile - V1faca9883No ratings yet

- Income Taxes: Basic ConceptsDocument7 pagesIncome Taxes: Basic ConceptsTrisha Mae Mendoza MacalinoNo ratings yet

- TAD Ch.4-7Document109 pagesTAD Ch.4-7Yitera SisayNo ratings yet

- Rmo 1 2012Document4 pagesRmo 1 2012Earl PatrickNo ratings yet

- Session 3, 4 Role of CAG in GST Regim FinalDocument30 pagesSession 3, 4 Role of CAG in GST Regim FinalSuresh Kumar YathirajuNo ratings yet

- M. Govinda Rao Director, National Institute of Public Finance and PolicyDocument12 pagesM. Govinda Rao Director, National Institute of Public Finance and PolicySantosh SinghNo ratings yet

- Pfmat For Lgus-Part 1Document54 pagesPfmat For Lgus-Part 1Josephine Templa-Jamolod100% (2)

- IT Audit CH 3Document5 pagesIT Audit CH 3JC MoralesNo ratings yet

- Operation Profile: Basic DataDocument13 pagesOperation Profile: Basic DataAlan GarcíaNo ratings yet

- Laporan Tahunan DJP 2020 - EnglishDocument256 pagesLaporan Tahunan DJP 2020 - EnglishHaryo BagaskaraNo ratings yet

- Tax PDFDocument32 pagesTax PDFAd ElouNo ratings yet

- LGUScoreCard BLGFDocument32 pagesLGUScoreCard BLGFKristel ClaudineNo ratings yet

- BLGF PPT On Coaches Training On The Enhanced BPLS (Revised)Document62 pagesBLGF PPT On Coaches Training On The Enhanced BPLS (Revised)DILG Manolo FortichNo ratings yet

- 11 BEPS Final Report - Action 11Document32 pages11 BEPS Final Report - Action 11ktrihnnguyen299No ratings yet

- Commercial Taxes and Registration DepartmentDocument24 pagesCommercial Taxes and Registration DepartmentAncy RajNo ratings yet

- A Study in Pratama Tax Office of Serang Regency Banten ProvinceDocument9 pagesA Study in Pratama Tax Office of Serang Regency Banten Provinceyuliana jaengNo ratings yet

- Rmo 41-2011Document51 pagesRmo 41-2011Christian Albert HerreraNo ratings yet

- trr266 Global MNC Tax Complexity Survey 2020Document30 pagestrr266 Global MNC Tax Complexity Survey 2020venipin416No ratings yet

- Beps Webcast 8 Launch 2015 Final Reports 151005150005 Lva1 App6891Document78 pagesBeps Webcast 8 Launch 2015 Final Reports 151005150005 Lva1 App6891Tural AbbasovNo ratings yet

- VR12 PRM SKDocument116 pagesVR12 PRM SKJimNo ratings yet

- CPBRD Policy Brief: A E A F A R P T C P CDocument28 pagesCPBRD Policy Brief: A E A F A R P T C P CPbjlr ElevenNo ratings yet

- Presentation Of: Revenue and Expenditure DataDocument21 pagesPresentation Of: Revenue and Expenditure DataEya Guerrero CalvaridoNo ratings yet

- BLGF Change Request 1 - Correction of Reports For Ave LRGDocument1 pageBLGF Change Request 1 - Correction of Reports For Ave LRGRosalie T. Orbon-TamondongNo ratings yet

- Local Public Financial Management Tools For ESREDocument54 pagesLocal Public Financial Management Tools For ESRERandy Sioson100% (1)

- SCP Dharamshala 1Document50 pagesSCP Dharamshala 1rhythm subediNo ratings yet

- Office of The City Assessor/1101 Mandate, Vision/Mission, Major Final Output, Performance Indicators and Targets Cy 2020Document2 pagesOffice of The City Assessor/1101 Mandate, Vision/Mission, Major Final Output, Performance Indicators and Targets Cy 2020Charles D. FloresNo ratings yet

- Machine Learning Analytics ForpredictingtaxrevenuepotentialDocument13 pagesMachine Learning Analytics ForpredictingtaxrevenuepotentialAlifah MuwafiqohNo ratings yet

- Guidelines PBBDocument9 pagesGuidelines PBBNova TeresaNo ratings yet

- Results ChainDocument5 pagesResults ChainFloyd L PetallanoNo ratings yet

- Intermediate Paper 11 PDFDocument456 pagesIntermediate Paper 11 PDFjesurajajNo ratings yet

- Pfmat Concepts 2016 DBMDocument44 pagesPfmat Concepts 2016 DBMBern100% (1)

- Tax Compliance FinalDocument23 pagesTax Compliance FinalMahamood FaisalNo ratings yet

- Volume 4 - Revenue Administration & Resouce Mobilization Tools and ApproachesDocument79 pagesVolume 4 - Revenue Administration & Resouce Mobilization Tools and ApproachesBong RicoNo ratings yet

- Factors Affecting Turnover Tax Collection Performance A Case of West Shoa Selected WoredasDocument22 pagesFactors Affecting Turnover Tax Collection Performance A Case of West Shoa Selected Woredasedwin shikukuNo ratings yet

- EA 2000 Desk Review & ReconciliationDocument43 pagesEA 2000 Desk Review & ReconciliationSushant SaxenaNo ratings yet

- System Audit CELD Financial Audit ProcedureDocument2 pagesSystem Audit CELD Financial Audit ProcedureSerza ConsultNo ratings yet

- Tax Administration/ Reforms in Pakistan: Fazal Amin ShahDocument12 pagesTax Administration/ Reforms in Pakistan: Fazal Amin ShahMubashir SheheryarNo ratings yet

- Tool Kit for Tax Administration Management Information SystemFrom EverandTool Kit for Tax Administration Management Information SystemRating: 1 out of 5 stars1/5 (1)

- Extending The Use of RiskDocument7 pagesExtending The Use of RiskRADU LAURENTIUNo ratings yet

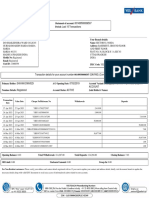

- Account Statement Last 10 TransactionsDocument2 pagesAccount Statement Last 10 TransactionsAshish kumarNo ratings yet

- ACCA - Advanced Audit and Assurance (AAA) - Course Exam 1 Solutions - 2019Document12 pagesACCA - Advanced Audit and Assurance (AAA) - Course Exam 1 Solutions - 2019Ruddhi JainNo ratings yet

- Chapter 1editedDocument13 pagesChapter 1editedMuktar jiboNo ratings yet

- Craigslist PDFDocument2 pagesCraigslist PDFSerNo ratings yet

- History of Vivo 123Document14 pagesHistory of Vivo 123VenkateshKonda100% (2)

- Tds On Provison of Expenses (Tax Gls Open For Direct Manual Posting On 17.04.23 & 18.04.23 Only by Corporate Office) Urgent & Statuary ComplianceDocument1 pageTds On Provison of Expenses (Tax Gls Open For Direct Manual Posting On 17.04.23 & 18.04.23 Only by Corporate Office) Urgent & Statuary ComplianceArvind Kumar GuptaNo ratings yet

- Suspensing and Termination undIC REDBOOK & MDM ED-NEAL BUNNI 13Document1 pageSuspensing and Termination undIC REDBOOK & MDM ED-NEAL BUNNI 13Ahmet KöşNo ratings yet

- Project Report FormatDocument8 pagesProject Report FormatBhartiNo ratings yet

- BSBMGT517 - Management Operational Plan - Nicolas Larrarte - V1.1Document79 pagesBSBMGT517 - Management Operational Plan - Nicolas Larrarte - V1.1Nicolas EscobarNo ratings yet

- Gay7e Irm Ch04Document18 pagesGay7e Irm Ch04Thùy Linh Lê ThịNo ratings yet

- Dell's Working Capital: Case BriefDocument6 pagesDell's Working Capital: Case BriefTanya Ahuja100% (1)

- 7739 14817 1 SMDocument16 pages7739 14817 1 SMAry Surya PurnamaNo ratings yet

- JP 4-0 Joint Logistic 18jun2008Document124 pagesJP 4-0 Joint Logistic 18jun2008Bryan FenclNo ratings yet

- Case Study ReportDocument15 pagesCase Study ReportMira SyahirahNo ratings yet

- DPR Selwa 02.07.2020Document22 pagesDPR Selwa 02.07.2020ravibelavadiNo ratings yet

- A Project Report ON: Youth Attraction in Bikano at BikanervalaDocument31 pagesA Project Report ON: Youth Attraction in Bikano at Bikanervalamanoj kumar Das67% (3)

- Role of Rbi in The Indian Banking SystemDocument20 pagesRole of Rbi in The Indian Banking SystemSakshi JainNo ratings yet

- Tess Zero Accident Program For ZAP Conf 09Document29 pagesTess Zero Accident Program For ZAP Conf 09Armin GomezNo ratings yet

- Listado Afilliados Dic 2019Document117 pagesListado Afilliados Dic 2019JEIDER ROJASNo ratings yet

- Fit & TolleranceDocument73 pagesFit & TolleranceyudhveerNo ratings yet

- Industrial VisitDocument8 pagesIndustrial VisitmarySibiliaNo ratings yet

- Marketing Management Introduction Group GDocument3 pagesMarketing Management Introduction Group Gritheesha mahadev0216No ratings yet

- My IdolDocument1 pageMy IdolSyed FarisNo ratings yet

- Op No 13 - Understanding The Filipino Green ConsumerDocument40 pagesOp No 13 - Understanding The Filipino Green Consumermilrosebatilo2012No ratings yet

- The Advanteges and Disadvanteges of Being Your Own Boss: Essay by Madalina IonDocument2 pagesThe Advanteges and Disadvanteges of Being Your Own Boss: Essay by Madalina IonAna Maria GavrilaNo ratings yet

- 写作申请信Document5 pages写作申请信ewa9wwn1100% (1)

- Purdue University Contract With Ibram KendiDocument8 pagesPurdue University Contract With Ibram KendiThe College FixNo ratings yet