Download as pdf or txt

You might also like

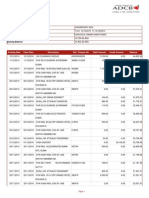

- Account Statement: Account Number Statement Period Account Name(s) Opening Balance Closing BalanceDocument3 pagesAccount Statement: Account Number Statement Period Account Name(s) Opening Balance Closing Balancearns1950% (2)

- DocDocument16 pagesDocNorman Delirio100% (1)

- Partial Fore Closure Receipt 28 03 2018 1522236048Document1 pagePartial Fore Closure Receipt 28 03 2018 1522236048Shridhar JoshiNo ratings yet

- Worksheet BRSDocument2 pagesWorksheet BRSCA Chhavi Gupta100% (1)

- Dkgoel BRS 11Document15 pagesDkgoel BRS 11DhruvNo ratings yet

- BRS PDFDocument14 pagesBRS PDFGautam KhanwaniNo ratings yet

- 06 BRS - Practice QuestionsDocument1 page06 BRS - Practice QuestionsNeelanjana RayNo ratings yet

- WS - Xi BRS - 2Document5 pagesWS - Xi BRS - 2richshivamshahNo ratings yet

- BRS Class 11Document1 pageBRS Class 11tarun aroraNo ratings yet

- Bank Reconciliation StatementDocument12 pagesBank Reconciliation StatementBhuvan PrajapatiNo ratings yet

- BRS RevisionDocument2 pagesBRS RevisionHarsh ModiNo ratings yet

- CA F BRS WithDocument10 pagesCA F BRS WithG. DhanyaNo ratings yet

- Ts Grewal Solutions For Class 11 Accountancy Chapter 9 BankDocument34 pagesTs Grewal Solutions For Class 11 Accountancy Chapter 9 Bankmyankjindal9No ratings yet

- Tsgrewal BRSDocument11 pagesTsgrewal BRSDhruvNo ratings yet

- Bank Reconciliation StatementDocument33 pagesBank Reconciliation StatementMd TahirNo ratings yet

- BRS PDFDocument8 pagesBRS PDFAnshumanNo ratings yet

- 6 BRS 08-2023 RegularDocument7 pages6 BRS 08-2023 RegularjahnaviNo ratings yet

- Bank Reconciliation Statement Practice ProblemsDocument2 pagesBank Reconciliation Statement Practice ProblemsHaya DanishNo ratings yet

- Brs Practical QuestionsDocument5 pagesBrs Practical QuestionsSwarupa VNo ratings yet

- 0c26dbank Reconciliation Statement Practice QuestionsDocument2 pages0c26dbank Reconciliation Statement Practice QuestionsRahul AgarwalNo ratings yet

- FA - Bank Rec. QuestionDocument2 pagesFA - Bank Rec. QuestionAshika JayaweeraNo ratings yet

- B.R.S. Test 3Document5 pagesB.R.S. Test 3Sudhir SinhaNo ratings yet

- Practice With MT - BRSDocument6 pagesPractice With MT - BRSsrushtibhawsar07No ratings yet

- 39759Document3 pages39759MonikaNo ratings yet

- BRS Statement IllustrationsDocument3 pagesBRS Statement Illustrationssurekha khandebharadNo ratings yet

- AC101 Quiz 2Document2 pagesAC101 Quiz 2irene TogaraNo ratings yet

- BRS WSDocument2 pagesBRS WSShrajith A NatarajanNo ratings yet

- Additional Practical Problems-13-1Document5 pagesAdditional Practical Problems-13-1sharmaarmaan103No ratings yet

- BRS PPT StudentDocument26 pagesBRS PPT StudentgganyanNo ratings yet

- Exercises of Bank Reconciliation Statement: Exercise No. IDocument9 pagesExercises of Bank Reconciliation Statement: Exercise No. ITayyab AliNo ratings yet

- CA Foundation - Test 4 Chapters - Answer PaperDocument8 pagesCA Foundation - Test 4 Chapters - Answer PaperKrishna SurekaNo ratings yet

- Bank Reconciliaton Statement Practice Questions: ST ST STDocument2 pagesBank Reconciliaton Statement Practice Questions: ST ST STHuma SamuelNo ratings yet

- Accts Test - BRS & InventoriesDocument2 pagesAccts Test - BRS & Inventoriesprashanttiwari155282No ratings yet

- Q-10 Prepare Bank Reconciliation Statement As On 31Document2 pagesQ-10 Prepare Bank Reconciliation Statement As On 31krish mehtaNo ratings yet

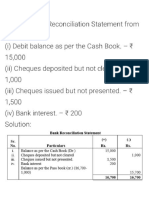

- Prepare Bank Reconciliation Statement From The Following: (I) Debit Balance As Per The Cash BookDocument10 pagesPrepare Bank Reconciliation Statement From The Following: (I) Debit Balance As Per The Cash BookPragya ShuklaNo ratings yet

- BRS Ca FoundationDocument9 pagesBRS Ca FoundationJunaid Iqbal MastoiNo ratings yet

- SET B 11th Acc BRS N RECT.Document2 pagesSET B 11th Acc BRS N RECT.Mohammad Tariq AnsariNo ratings yet

- Chapter 9 - Bank Reconciliation StatementDocument15 pagesChapter 9 - Bank Reconciliation StatementSaurabh GohanNo ratings yet

- Work Book Unit 12 Bank Reconcilaition Statement (Solved)Document9 pagesWork Book Unit 12 Bank Reconcilaition Statement (Solved)Zaheer SwatiNo ratings yet

- 06 SLLC - 2021 - Acc - Review Question - Set 03Document7 pages06 SLLC - 2021 - Acc - Review Question - Set 03Chamela MahiepalaNo ratings yet

- Practice Set BRSDocument15 pagesPractice Set BRSvishwajeetnmoreNo ratings yet

- BRS ProblemsDocument28 pagesBRS ProblemsKutbuddin JawadwalaNo ratings yet

- Bank Reconciliation Statement AssignmentDocument3 pagesBank Reconciliation Statement AssignmentDev KumarNo ratings yet

- Test of BRSDocument3 pagesTest of BRSPervaiz AkhterNo ratings yet

- CHP 2 - BRSDocument5 pagesCHP 2 - BRSPayal Mehta DeshpandeNo ratings yet

- Bank Reconciliation StatementDocument22 pagesBank Reconciliation StatementasimaNo ratings yet

- CA Foundation BRS Practice Questions - DRS - CTC ClassesDocument2 pagesCA Foundation BRS Practice Questions - DRS - CTC ClassesAnas AzeemNo ratings yet

- CA Foundation June 23 BRS Problem - CTC ClassesDocument2 pagesCA Foundation June 23 BRS Problem - CTC ClassesMohit SharmaNo ratings yet

- Class Exercise Bank ReconciliationDocument6 pagesClass Exercise Bank ReconciliationDalia ElarabyNo ratings yet

- Audit of Cash QuizDocument4 pagesAudit of Cash QuizAndy LaluNo ratings yet

- Brs Practise SheetDocument1 pageBrs Practise Sheetapi-252642432No ratings yet

- Bank Reconciliation StatementDocument7 pagesBank Reconciliation Statementkshitijraja18No ratings yet

- 16772BRSDocument47 pages16772BRSSketch KathayatNo ratings yet

- QUIZ 1. Audit of Cash ManuscriptDocument4 pagesQUIZ 1. Audit of Cash ManuscriptJulie Mae Caling MalitNo ratings yet

- Navyug Commerce Institute Lakhanpur Kanpur Topic-B.R.SDocument2 pagesNavyug Commerce Institute Lakhanpur Kanpur Topic-B.R.SparthNo ratings yet

- FA1 Bank ReconciliationDocument4 pagesFA1 Bank Reconciliationamir100% (1)

- BRS Practice QuestionsDocument2 pagesBRS Practice Questionssyed ali raza kazmiNo ratings yet

- Assignment - Cash and CEDocument4 pagesAssignment - Cash and CEAleah Jehan AbuatNo ratings yet

- Practical - Bank Reconciliation StatementDocument5 pagesPractical - Bank Reconciliation StatementUniversal SoldierNo ratings yet

- BRS 2Document2 pagesBRS 2Aarnav SharmaNo ratings yet

- Business Acoounting (2020)Document4 pagesBusiness Acoounting (2020)harshdeepgarg5No ratings yet

- Adobe Scan 05 Jan 2024Document2 pagesAdobe Scan 05 Jan 2024Harshit GargNo ratings yet

- A Thesis On Customer Satisfaction OF Nepal Investment Bank LimitedDocument80 pagesA Thesis On Customer Satisfaction OF Nepal Investment Bank LimitedBijay PradhanNo ratings yet

- Questionnaire - Google FormsDocument4 pagesQuestionnaire - Google FormsAkshit AggarwalNo ratings yet

- Module 8 - The Global Financial CrisisDocument5 pagesModule 8 - The Global Financial CrisisAmiteshNo ratings yet

- Procedures For International FundingDocument2 pagesProcedures For International FundingHeart FrozenNo ratings yet

- Questionnaire For Micro-FinanceDocument18 pagesQuestionnaire For Micro-FinanceGovinda GowdaNo ratings yet

- Wells Fargo Everyday CheckingDocument5 pagesWells Fargo Everyday CheckingIsabel LieberNo ratings yet

- Booking Anjum 1436 H 4 SD 9 SephthghjDocument3 pagesBooking Anjum 1436 H 4 SD 9 SephthghjnabilacpNo ratings yet

- SBM September Month Stock Statement 30.09.2015Document11 pagesSBM September Month Stock Statement 30.09.2015SURANA1973No ratings yet

- Statement 28-MAR-23 AC 23122263 02042716 - UnlockedDocument3 pagesStatement 28-MAR-23 AC 23122263 02042716 - Unlockedjonathangoodrick16No ratings yet

- Payments Newsletter: Demystifying The Merchant Acquiring BusinessDocument8 pagesPayments Newsletter: Demystifying The Merchant Acquiring BusinessRazak RadityoNo ratings yet

- Suncoast Bank Statement JulyDocument4 pagesSuncoast Bank Statement JulyamatobertrumNo ratings yet

- Module 16Document10 pagesModule 16sandeepNo ratings yet

- 1458935715587Document8 pages1458935715587Rahimullah QaziNo ratings yet

- Cash and Liquidity Management - Topic 3Document47 pagesCash and Liquidity Management - Topic 3kodeNo ratings yet

- New Balance $5,240.35 Minimum Payment Due $52.00 Payment Due Date 09/06/23Document12 pagesNew Balance $5,240.35 Minimum Payment Due $52.00 Payment Due Date 09/06/23Anthony CastelliNo ratings yet

- Role of Banking in The Modern EconomyDocument18 pagesRole of Banking in The Modern Economybackupsanthosh21 dataNo ratings yet

- UntitledDocument9 pagesUntitledapi-213954485No ratings yet

- Gpay Payment Success But Not Credited - Google SearchDocument1 pageGpay Payment Success But Not Credited - Google SearchAnanthi SadacharamNo ratings yet

- Concept of Legal TenderDocument2 pagesConcept of Legal TenderJesther NuquiNo ratings yet

- What Is The Purpose of PDIC Law? 4. Define A. DepositDocument5 pagesWhat Is The Purpose of PDIC Law? 4. Define A. DepositJoshel MaeNo ratings yet

- UniCredit Auto ABS in EuropeDocument16 pagesUniCredit Auto ABS in EuropeMaxF_2015No ratings yet

- UTI Account STMTDocument1 pageUTI Account STMTfhannyguyNo ratings yet

- An Analysis of Grameen Bank and ASADocument45 pagesAn Analysis of Grameen Bank and ASAAye Nyein ThuNo ratings yet

- PNB vs. PadillaDocument8 pagesPNB vs. PadillajohnmiggyNo ratings yet

- RBI Circular - Release of Property Documents On Rep - 230915 - 085021Document2 pagesRBI Circular - Release of Property Documents On Rep - 230915 - 085021Motorola G6No ratings yet

- Catatan Monetary SystemDocument5 pagesCatatan Monetary SystemKhoirun Nisa'ul AfifahNo ratings yet

- Cashless EconomyDocument5 pagesCashless EconomykumaresanNo ratings yet