Download as docx, pdf, or txt

You might also like

- CMT Curriculum Level 1 2022 Changes PDFDocument12 pagesCMT Curriculum Level 1 2022 Changes PDFson13% (8)

- Summary: Financial Intelligence: Review and Analysis of Berman and Knight's BookFrom EverandSummary: Financial Intelligence: Review and Analysis of Berman and Knight's BookNo ratings yet

- What is Financial Accounting and BookkeepingFrom EverandWhat is Financial Accounting and BookkeepingRating: 4 out of 5 stars4/5 (10)

- Value-based financial management: Towards a Systematic Process for Financial Decision - MakingFrom EverandValue-based financial management: Towards a Systematic Process for Financial Decision - MakingNo ratings yet

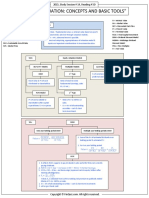

- Smart Summary Equity Valuation Concepts and Basic Tools CFADocument4 pagesSmart Summary Equity Valuation Concepts and Basic Tools CFABhuvnesh KotharNo ratings yet

- Corporate Finance: A Beginner's Guide: Investment series, #1From EverandCorporate Finance: A Beginner's Guide: Investment series, #1No ratings yet

- Options Trading For BeginnersDocument146 pagesOptions Trading For BeginnersMohaideen Subaire100% (6)

- Financial Literacy for Entrepreneurs: Understanding the Numbers Behind Your BusinessFrom EverandFinancial Literacy for Entrepreneurs: Understanding the Numbers Behind Your BusinessNo ratings yet

- Financial Intelligence: Mastering the Numbers for Business SuccessFrom EverandFinancial Intelligence: Mastering the Numbers for Business SuccessNo ratings yet

- The Finace Master: What you Need to Know to Achieve Lasting Financial FreedomFrom EverandThe Finace Master: What you Need to Know to Achieve Lasting Financial FreedomNo ratings yet

- Tactical Objective: Strategic Maneuvers, Decoding the Art of Military PrecisionFrom EverandTactical Objective: Strategic Maneuvers, Decoding the Art of Military PrecisionNo ratings yet

- Finance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersFrom EverandFinance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersNo ratings yet

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- Agencies of Cash Flow: How to Raise and Invest Long-Term Money for Foundations and EndowmentsFrom EverandAgencies of Cash Flow: How to Raise and Invest Long-Term Money for Foundations and EndowmentsNo ratings yet

- Financial Intelligence: Navigating the Numbers in BusinessFrom EverandFinancial Intelligence: Navigating the Numbers in BusinessNo ratings yet

- Dollars and Sense: Demystifying Financial Records for Business OwnersFrom EverandDollars and Sense: Demystifying Financial Records for Business OwnersNo ratings yet

- The Road to Financial Success: Practical Strategies for Building Wealth and Achieving Financial IndependenceFrom EverandThe Road to Financial Success: Practical Strategies for Building Wealth and Achieving Financial IndependenceNo ratings yet

- "From Zero to Millionaire: The Ultimate Guide to Building Wealth and Achieving Financial Freedom"From Everand"From Zero to Millionaire: The Ultimate Guide to Building Wealth and Achieving Financial Freedom"No ratings yet

- Financial Planning: A Guide To Achieve Your Personal Freedom By Building A Strategic Money Plan For Your LifeFrom EverandFinancial Planning: A Guide To Achieve Your Personal Freedom By Building A Strategic Money Plan For Your LifeNo ratings yet

- Financial Control Blueprint: Building a Path to Growth and SuccessFrom EverandFinancial Control Blueprint: Building a Path to Growth and SuccessNo ratings yet

- How to manage your finance for beginners: A guide to promote financial literacyFrom EverandHow to manage your finance for beginners: A guide to promote financial literacyNo ratings yet

- Financial Statements: A Simplified Easy Accounting and Business Owner Guide to Understanding and Creating Financial ReportsFrom EverandFinancial Statements: A Simplified Easy Accounting and Business Owner Guide to Understanding and Creating Financial ReportsNo ratings yet

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingFrom EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingNo ratings yet

- Ethical Valuation: Navigating the Future of Startup InvestmentsFrom EverandEthical Valuation: Navigating the Future of Startup InvestmentsNo ratings yet

- From Data to Decisions: Harnessing FP&A for Financial Leadership: FP&A Mastery Series, #1From EverandFrom Data to Decisions: Harnessing FP&A for Financial Leadership: FP&A Mastery Series, #1No ratings yet

- An Investment Journey II The Essential Tool Kit: Building A Successful Portfolio With Stock FundamentalsFrom EverandAn Investment Journey II The Essential Tool Kit: Building A Successful Portfolio With Stock FundamentalsNo ratings yet

- Dividend Investing: Passive Income and Growth Investing for BeginnersFrom EverandDividend Investing: Passive Income and Growth Investing for BeginnersNo ratings yet

- Current Asset ManagementDocument15 pagesCurrent Asset Managementliesly buticNo ratings yet

- Inventory Cost Flow LCNRVDocument8 pagesInventory Cost Flow LCNRVliesly buticNo ratings yet

- Data Management SystemDocument52 pagesData Management Systemliesly buticNo ratings yet

- LP Model Formulation 2021Document25 pagesLP Model Formulation 2021liesly buticNo ratings yet

- The Accounting CycleDocument3 pagesThe Accounting Cycleliesly buticNo ratings yet

- LP Maximization Graphical Method 2021Document28 pagesLP Maximization Graphical Method 2021liesly buticNo ratings yet

- LInear Equations One Variable Examples & SolutionsDocument11 pagesLInear Equations One Variable Examples & Solutionsliesly buticNo ratings yet

- Systems of Linear Equations: Using A Graph To SolveDocument8 pagesSystems of Linear Equations: Using A Graph To Solveliesly buticNo ratings yet

- Solving Linear Systems of Inequalities by GraphingDocument31 pagesSolving Linear Systems of Inequalities by Graphingliesly buticNo ratings yet

- FMI Unit 1Document30 pagesFMI Unit 1Debajit DasNo ratings yet

- CFA CaseletsDocument27 pagesCFA CaseletsArk SrivastavaNo ratings yet

- Behavioural Biases Theories 2nd ChapterDocument26 pagesBehavioural Biases Theories 2nd Chaptersadhana gawade/AwateNo ratings yet

- KIM - Kotak Multicap FundDocument34 pagesKIM - Kotak Multicap FunddrstudyteamNo ratings yet

- Question Reviews - Financial Services (Till April 2021)Document6 pagesQuestion Reviews - Financial Services (Till April 2021)jeganrajrajNo ratings yet

- SME IPOs & Startups in 2024Document11 pagesSME IPOs & Startups in 2024singhkabir989898No ratings yet

- Financial Marketing RegulationDocument7 pagesFinancial Marketing RegulationRVNo ratings yet

- Blackbook Project 1920728Document91 pagesBlackbook Project 1920728Vignesh Sirimalla100% (1)

- 2020 Mock Exam C - Morning SessionDocument21 pages2020 Mock Exam C - Morning SessionJay100% (1)

- Capital MarketDocument25 pagesCapital MarketAnna Mae NebresNo ratings yet

- Manajemen Keuangan LanjutanDocument4 pagesManajemen Keuangan Lanjutancerella ayanaNo ratings yet

- The Sociology of Finance Carruthers and Kim ARS PaperDocument24 pagesThe Sociology of Finance Carruthers and Kim ARS PaperThais MoreiraNo ratings yet

- Checkpoint Exam 2 (Study Sessions 10-15)Document11 pagesCheckpoint Exam 2 (Study Sessions 10-15)Krishna GoelNo ratings yet

- Investment Analysis and Portfolio ManagementDocument237 pagesInvestment Analysis and Portfolio ManagementKannan RNo ratings yet

- Fin3105 SC 780: Chapter 5 - Security Market Indexes (Questions)Document2 pagesFin3105 SC 780: Chapter 5 - Security Market Indexes (Questions)Christy Mae EderNo ratings yet

- Linda Raschke SlidesDocument28 pagesLinda Raschke SlidessuneetaNo ratings yet

- Stock Market Course ContentDocument12 pagesStock Market Course ContentSrikanth SanipiniNo ratings yet

- Mid-Term Managerial Finance - Uts - 15 May 2024Document1 pageMid-Term Managerial Finance - Uts - 15 May 2024Ani MarianiNo ratings yet

- Shibanda Proposal 31-8-2021 (400) FinalDocument42 pagesShibanda Proposal 31-8-2021 (400) FinalDigichange AgronomistsNo ratings yet

- Stock ExchangeDocument43 pagesStock ExchangeGaurav JindalNo ratings yet

- Capital Financing - Corporate Finance InstituteDocument30 pagesCapital Financing - Corporate Finance InstituteOyewande ToyinNo ratings yet

- Notes of 12. Stock ExchangeDocument14 pagesNotes of 12. Stock Exchangeatul AgalaweNo ratings yet

- IAP Presentation - Motilal OswalDocument40 pagesIAP Presentation - Motilal OswalDr. Deepa Bhindora100% (1)

- JahanzaibDocument2 pagesJahanzaibjahanzaib malikNo ratings yet

- Performance Overview: As of Sep 14, 2023Document2 pagesPerformance Overview: As of Sep 14, 2023Tirthkumar PatelNo ratings yet

- Nicki InvestmentDocument13 pagesNicki InvestmentMellisaNo ratings yet

- Data Analysis Mutual FundDocument9 pagesData Analysis Mutual Fundjayswalhiralal899No ratings yet