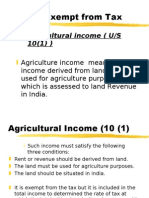

Tax Free Incomes

Tax Free Incomes

You might also like

- Incomes Which Do Not Form Part of Total Income - ItDocument33 pagesIncomes Which Do Not Form Part of Total Income - ItVijayendra RaoNo ratings yet

- 11.tax Free Incomes FinalDocument45 pages11.tax Free Incomes FinalAyushi DixitNo ratings yet

- 11.tax Free Incomes FinalDocument42 pages11.tax Free Incomes FinalAmit PandeyNo ratings yet

- 11.tax Free Incomes FinalDocument48 pages11.tax Free Incomes FinalaeeciviltrNo ratings yet

- 11.tax Free Incomes FinalDocument40 pages11.tax Free Incomes FinalKARTHIK ANo ratings yet

- 11.tax Free Incomes FinalDocument40 pages11.tax Free Incomes FinalGhs ShahpurkandiNo ratings yet

- 11.tax Free Incomes FinalDocument38 pages11.tax Free Incomes FinalshineNo ratings yet

- 11 TaxDocument37 pages11 TaxArpita KapoorNo ratings yet

- 11.tax Free Incomes FinalDocument37 pages11.tax Free Incomes FinalsaandoNo ratings yet

- 11.tax Free Incomes FinalDocument29 pages11.tax Free Incomes FinalRaun JainNo ratings yet

- 11.tax Free Incomes FinalDocument35 pages11.tax Free Incomes Finalpraveenr5883No ratings yet

- IT-03 Incomes Exempt From TaxDocument18 pagesIT-03 Incomes Exempt From TaxAkshat GoyalNo ratings yet

- As Amended by Finance Act, 2017Document3 pagesAs Amended by Finance Act, 2017JonnyNo ratings yet

- Agricultural IncomeDocument2 pagesAgricultural IncomezxcNo ratings yet

- Chapter - 1: Page - 1Document7 pagesChapter - 1: Page - 1Arunangsu ChandaNo ratings yet

- Chinmayanand DTDocument5 pagesChinmayanand DTAnand PandeyNo ratings yet

- Study Note - 13: Incomes Which Do Not Form Part of Total IncomeDocument37 pagesStudy Note - 13: Incomes Which Do Not Form Part of Total Incomes4sahithNo ratings yet

- Incomes Which Do Not Form Part of Total Income: Section 64Document91 pagesIncomes Which Do Not Form Part of Total Income: Section 64d-fbuser-65596417No ratings yet

- Chapter 10 - Incomes Which Do Not Form Part of Total Income - NotesDocument10 pagesChapter 10 - Incomes Which Do Not Form Part of Total Income - NotesRahul TiwariNo ratings yet

- Section 10Document42 pagesSection 10Mrigendra MishraNo ratings yet

- Taxation ProjectDocument12 pagesTaxation ProjectVeronicaNo ratings yet

- Taxation Project 1Document15 pagesTaxation Project 1VeronicaNo ratings yet

- Tax Treatment of Dividend ReceivedDocument10 pagesTax Treatment of Dividend ReceivedmukeshNo ratings yet

- Business Taxation 1Document22 pagesBusiness Taxation 1AnshuNo ratings yet

- Permanent Esta ResearchDocument24 pagesPermanent Esta ResearchNeha PandeyNo ratings yet

- Section 64: Incomes Which Do Not Form Part of Total Income Incomes Not Included in Total Income. 10Document33 pagesSection 64: Incomes Which Do Not Form Part of Total Income Incomes Not Included in Total Income. 10Mandar RaneNo ratings yet

- 62287bos50449 Mod1 cp3Document51 pages62287bos50449 Mod1 cp3monicabhat96No ratings yet

- Direct Taxation ProjectDocument15 pagesDirect Taxation Projectbipin puniaNo ratings yet

- 11 - Exemptions and DeductionsDocument42 pages11 - Exemptions and DeductionsmanikaNo ratings yet

- Income Exempt From TaxDocument20 pagesIncome Exempt From TaxSaad AliNo ratings yet

- Regulatory Provisions Under EcbDocument6 pagesRegulatory Provisions Under EcbAllwyn FlowNo ratings yet

- Benefits Available To Non ResidentsDocument16 pagesBenefits Available To Non ResidentsArchita TiwariNo ratings yet

- Income ExemptDocument21 pagesIncome Exemptapi-3832224100% (1)

- Tax PlanningDocument51 pagesTax PlanningSatyajeet MohantyNo ratings yet

- Wa0004.Document64 pagesWa0004.dhruv MehtaNo ratings yet

- Incomes Which Do Not Form Part of Total Income: After Studying This Chapter, You Would Be Able ToDocument49 pagesIncomes Which Do Not Form Part of Total Income: After Studying This Chapter, You Would Be Able ToAnkitaNo ratings yet

- Exempted Income 1Document24 pagesExempted Income 1jerin joshy100% (1)

- Concessional Tax Rates For NrisDocument21 pagesConcessional Tax Rates For Nrislipsa PriyadarshiniNo ratings yet

- Section-10: Income Exempt From TaxDocument21 pagesSection-10: Income Exempt From TaxRakesh SharmaNo ratings yet

- Incomes Which Do Not Form Part of Total Income: After Studying This Chapter, You Would Be Able ToDocument50 pagesIncomes Which Do Not Form Part of Total Income: After Studying This Chapter, You Would Be Able ToLilyNo ratings yet

- Presentation On Income Exempted From Income TaxDocument20 pagesPresentation On Income Exempted From Income Taxyatin rajputNo ratings yet

- What Is Tax Deducted at SourceDocument6 pagesWhat Is Tax Deducted at SourcejdonNo ratings yet

- FEMA Guidelines On Transfer of Securities by An Indian Entity To An NRIDocument3 pagesFEMA Guidelines On Transfer of Securities by An Indian Entity To An NRIPriyanshu GuptaNo ratings yet

- Section-10: Income Exempt From TaxDocument21 pagesSection-10: Income Exempt From TaxJitendra VernekarNo ratings yet

- ODI May2011Document4 pagesODI May2011Parul ShahNo ratings yet

- Unit 4Document14 pagesUnit 4Rupesh PatilNo ratings yet

- Updates SMAIT June 2016Document11 pagesUpdates SMAIT June 2016Harsh SharmaNo ratings yet

- Section 10Document63 pagesSection 10sushil kumarNo ratings yet

- Sources of Foreign Financing or Foreign Currency Finance For Indian CompaniesDocument3 pagesSources of Foreign Financing or Foreign Currency Finance For Indian Companiesarshad391No ratings yet

- It Act Sec 10Document39 pagesIt Act Sec 10Ramod SayedNo ratings yet

- Adobe Scan 09-Nov-2023Document5 pagesAdobe Scan 09-Nov-2023james17stevensNo ratings yet

- Alternative Investment FundDocument3 pagesAlternative Investment FundAnirudh BajpaiNo ratings yet

- Introduction To ResidenceDocument4 pagesIntroduction To ResidenceNiya Maria NixonNo ratings yet

- Faqs View: SearchDocument17 pagesFaqs View: Searchmeenakshi56No ratings yet

- IncomeTax Short QuestionsDocument7 pagesIncomeTax Short QuestionsWatsun ArmstrongNo ratings yet

- General Meaning: Edit Source EditDocument38 pagesGeneral Meaning: Edit Source Editsri_bhairiNo ratings yet

- Income Form Other Sources-9Document10 pagesIncome Form Other Sources-9s4sahith50% (2)

- Section Eligible Assessee Type of Income Limits Conditions For Claiming ExemptionDocument32 pagesSection Eligible Assessee Type of Income Limits Conditions For Claiming ExemptionanilpeddamalliNo ratings yet

- Fema Rbi Org inDocument11 pagesFema Rbi Org inamishtheanalystNo ratings yet

- HRM Unit 2 (1) 2Document46 pagesHRM Unit 2 (1) 2Aayush GiriNo ratings yet

- HRM Unit 3Document17 pagesHRM Unit 3Aayush GiriNo ratings yet

- Unit 1 (Marketing Planning)Document9 pagesUnit 1 (Marketing Planning)Aayush GiriNo ratings yet

- Unit 1 (STP)Document6 pagesUnit 1 (STP)Aayush GiriNo ratings yet

- Unit 1 (Buying Decision Process)Document6 pagesUnit 1 (Buying Decision Process)Aayush GiriNo ratings yet

- Unit 2 (Pricing)Document11 pagesUnit 2 (Pricing)Aayush GiriNo ratings yet

- Unit 3 - Clubbing of IncomeDocument10 pagesUnit 3 - Clubbing of IncomeAayush GiriNo ratings yet

- 1 Prospectus FinalDocument283 pages1 Prospectus FinalLaxmikant RathiNo ratings yet

- Quality of Online Banking Services: in Comparitive Study of Sbi & Icici Bank"Document105 pagesQuality of Online Banking Services: in Comparitive Study of Sbi & Icici Bank"Simran ChauhanNo ratings yet

- Working Capital Management: Project ReportDocument41 pagesWorking Capital Management: Project Reportmahnoor afzalNo ratings yet

- ANLG BANK Case StudyDocument9 pagesANLG BANK Case StudyRadhika ThapaNo ratings yet

- Yitay ElemaDocument127 pagesYitay Elemacourse heroNo ratings yet

- India Dream RunDocument13 pagesIndia Dream RunNAMYA ARORANo ratings yet

- Help WalaDocument36 pagesHelp WalaPratikshya KarkiNo ratings yet

- Bharat Petroleum Corporation LTDDocument15 pagesBharat Petroleum Corporation LTDsagunkumarNo ratings yet

- International Equity FinancingDocument14 pagesInternational Equity FinancingMuazzam Mughal100% (1)

- Resume - Anthony J. SilvaDocument6 pagesResume - Anthony J. Silvatonysilva06No ratings yet

- Assignment - 2: Fundamentals of Management Science For Built EnvironmentDocument23 pagesAssignment - 2: Fundamentals of Management Science For Built EnvironmentVarma LakkamrajuNo ratings yet

- Application Form Account Opening UBIDocument4 pagesApplication Form Account Opening UBIDba ApsuNo ratings yet

- JURNAL 3 BISNIS SyariahDocument9 pagesJURNAL 3 BISNIS SyariahGevin SilitongaNo ratings yet

- HR Kazakhstan Country Report FinalDocument20 pagesHR Kazakhstan Country Report Finalanushikha banerjeeNo ratings yet

- Audit-Of-Specialized-Industries-2021-Module To Use-1Document107 pagesAudit-Of-Specialized-Industries-2021-Module To Use-1Virgie MartinezNo ratings yet

- Barclays Money Skills Activity Pack 16 25 YearsDocument50 pagesBarclays Money Skills Activity Pack 16 25 Yearslol123d100% (1)

- A2 Cum LRS FormDocument4 pagesA2 Cum LRS Formdeepakbannu2012No ratings yet

- LW-204 Professional Ethics and Bar Bench Relation and Accountancy For Lawyers PDFDocument2 pagesLW-204 Professional Ethics and Bar Bench Relation and Accountancy For Lawyers PDFRubab ShaikhNo ratings yet

- A Period of Consequence - How Abraaj Sees The World & Outlook, Dec 2008Document66 pagesA Period of Consequence - How Abraaj Sees The World & Outlook, Dec 2008Shirjeel NaseemNo ratings yet

- Pilgrim BankDocument2 pagesPilgrim Bankschatterjee780% (1)

- N-23-14 Jai Alai V BPIDocument2 pagesN-23-14 Jai Alai V BPIKobe Lawrence VeneracionNo ratings yet

- Small and Medium EnterprisesDocument19 pagesSmall and Medium EnterpriseskalaivaniNo ratings yet

- BIBM Program Summary - 05082018Document4 pagesBIBM Program Summary - 05082018mitemkt9683No ratings yet

- Chapter 11 Financial Accounting With Adjustment: Question 1 FuguangDocument15 pagesChapter 11 Financial Accounting With Adjustment: Question 1 FuguangClaudia WongNo ratings yet

- Reconciling The Bank StatementDocument6 pagesReconciling The Bank StatementOSAMANo ratings yet

- Ahsan Mehanti PDFDocument1 pageAhsan Mehanti PDFAftab Kanwal12No ratings yet

- Eurobank Presentation October2015Document76 pagesEurobank Presentation October2015vasilaros.kefNo ratings yet

- Tier 1 capital/TA (Tier 1+tier 2) /TA Tier 1 capital/RWA Including OBS Items (Tier 1+tier 2) /RAW Including OBS ItemsDocument10 pagesTier 1 capital/TA (Tier 1+tier 2) /TA Tier 1 capital/RWA Including OBS Items (Tier 1+tier 2) /RAW Including OBS ItemsThảo ĐỗNo ratings yet

- Performance Evaluation of Urban Co OperDocument131 pagesPerformance Evaluation of Urban Co Operudayaganavi sbNo ratings yet

- M16 Gitm4380 13e Im C16 PDFDocument17 pagesM16 Gitm4380 13e Im C16 PDFGolamSarwar100% (2)

Download as pdf or txt

You might also like

- Incomes Which Do Not Form Part of Total Income - ItDocument33 pagesIncomes Which Do Not Form Part of Total Income - ItVijayendra RaoNo ratings yet

- 11.tax Free Incomes FinalDocument45 pages11.tax Free Incomes FinalAyushi DixitNo ratings yet

- 11.tax Free Incomes FinalDocument42 pages11.tax Free Incomes FinalAmit PandeyNo ratings yet

- 11.tax Free Incomes FinalDocument48 pages11.tax Free Incomes FinalaeeciviltrNo ratings yet

- 11.tax Free Incomes FinalDocument40 pages11.tax Free Incomes FinalKARTHIK ANo ratings yet

- 11.tax Free Incomes FinalDocument40 pages11.tax Free Incomes FinalGhs ShahpurkandiNo ratings yet

- 11.tax Free Incomes FinalDocument38 pages11.tax Free Incomes FinalshineNo ratings yet

- 11 TaxDocument37 pages11 TaxArpita KapoorNo ratings yet

- 11.tax Free Incomes FinalDocument37 pages11.tax Free Incomes FinalsaandoNo ratings yet

- 11.tax Free Incomes FinalDocument29 pages11.tax Free Incomes FinalRaun JainNo ratings yet

- 11.tax Free Incomes FinalDocument35 pages11.tax Free Incomes Finalpraveenr5883No ratings yet

- IT-03 Incomes Exempt From TaxDocument18 pagesIT-03 Incomes Exempt From TaxAkshat GoyalNo ratings yet

- As Amended by Finance Act, 2017Document3 pagesAs Amended by Finance Act, 2017JonnyNo ratings yet

- Agricultural IncomeDocument2 pagesAgricultural IncomezxcNo ratings yet

- Chapter - 1: Page - 1Document7 pagesChapter - 1: Page - 1Arunangsu ChandaNo ratings yet

- Chinmayanand DTDocument5 pagesChinmayanand DTAnand PandeyNo ratings yet

- Study Note - 13: Incomes Which Do Not Form Part of Total IncomeDocument37 pagesStudy Note - 13: Incomes Which Do Not Form Part of Total Incomes4sahithNo ratings yet

- Incomes Which Do Not Form Part of Total Income: Section 64Document91 pagesIncomes Which Do Not Form Part of Total Income: Section 64d-fbuser-65596417No ratings yet

- Chapter 10 - Incomes Which Do Not Form Part of Total Income - NotesDocument10 pagesChapter 10 - Incomes Which Do Not Form Part of Total Income - NotesRahul TiwariNo ratings yet

- Section 10Document42 pagesSection 10Mrigendra MishraNo ratings yet

- Taxation ProjectDocument12 pagesTaxation ProjectVeronicaNo ratings yet

- Taxation Project 1Document15 pagesTaxation Project 1VeronicaNo ratings yet

- Tax Treatment of Dividend ReceivedDocument10 pagesTax Treatment of Dividend ReceivedmukeshNo ratings yet

- Business Taxation 1Document22 pagesBusiness Taxation 1AnshuNo ratings yet

- Permanent Esta ResearchDocument24 pagesPermanent Esta ResearchNeha PandeyNo ratings yet

- Section 64: Incomes Which Do Not Form Part of Total Income Incomes Not Included in Total Income. 10Document33 pagesSection 64: Incomes Which Do Not Form Part of Total Income Incomes Not Included in Total Income. 10Mandar RaneNo ratings yet

- 62287bos50449 Mod1 cp3Document51 pages62287bos50449 Mod1 cp3monicabhat96No ratings yet

- Direct Taxation ProjectDocument15 pagesDirect Taxation Projectbipin puniaNo ratings yet

- 11 - Exemptions and DeductionsDocument42 pages11 - Exemptions and DeductionsmanikaNo ratings yet

- Income Exempt From TaxDocument20 pagesIncome Exempt From TaxSaad AliNo ratings yet

- Regulatory Provisions Under EcbDocument6 pagesRegulatory Provisions Under EcbAllwyn FlowNo ratings yet

- Benefits Available To Non ResidentsDocument16 pagesBenefits Available To Non ResidentsArchita TiwariNo ratings yet

- Income ExemptDocument21 pagesIncome Exemptapi-3832224100% (1)

- Tax PlanningDocument51 pagesTax PlanningSatyajeet MohantyNo ratings yet

- Wa0004.Document64 pagesWa0004.dhruv MehtaNo ratings yet

- Incomes Which Do Not Form Part of Total Income: After Studying This Chapter, You Would Be Able ToDocument49 pagesIncomes Which Do Not Form Part of Total Income: After Studying This Chapter, You Would Be Able ToAnkitaNo ratings yet

- Exempted Income 1Document24 pagesExempted Income 1jerin joshy100% (1)

- Concessional Tax Rates For NrisDocument21 pagesConcessional Tax Rates For Nrislipsa PriyadarshiniNo ratings yet

- Section-10: Income Exempt From TaxDocument21 pagesSection-10: Income Exempt From TaxRakesh SharmaNo ratings yet

- Incomes Which Do Not Form Part of Total Income: After Studying This Chapter, You Would Be Able ToDocument50 pagesIncomes Which Do Not Form Part of Total Income: After Studying This Chapter, You Would Be Able ToLilyNo ratings yet

- Presentation On Income Exempted From Income TaxDocument20 pagesPresentation On Income Exempted From Income Taxyatin rajputNo ratings yet

- What Is Tax Deducted at SourceDocument6 pagesWhat Is Tax Deducted at SourcejdonNo ratings yet

- FEMA Guidelines On Transfer of Securities by An Indian Entity To An NRIDocument3 pagesFEMA Guidelines On Transfer of Securities by An Indian Entity To An NRIPriyanshu GuptaNo ratings yet

- Section-10: Income Exempt From TaxDocument21 pagesSection-10: Income Exempt From TaxJitendra VernekarNo ratings yet

- ODI May2011Document4 pagesODI May2011Parul ShahNo ratings yet

- Unit 4Document14 pagesUnit 4Rupesh PatilNo ratings yet

- Updates SMAIT June 2016Document11 pagesUpdates SMAIT June 2016Harsh SharmaNo ratings yet

- Section 10Document63 pagesSection 10sushil kumarNo ratings yet

- Sources of Foreign Financing or Foreign Currency Finance For Indian CompaniesDocument3 pagesSources of Foreign Financing or Foreign Currency Finance For Indian Companiesarshad391No ratings yet

- It Act Sec 10Document39 pagesIt Act Sec 10Ramod SayedNo ratings yet

- Adobe Scan 09-Nov-2023Document5 pagesAdobe Scan 09-Nov-2023james17stevensNo ratings yet

- Alternative Investment FundDocument3 pagesAlternative Investment FundAnirudh BajpaiNo ratings yet

- Introduction To ResidenceDocument4 pagesIntroduction To ResidenceNiya Maria NixonNo ratings yet

- Faqs View: SearchDocument17 pagesFaqs View: Searchmeenakshi56No ratings yet

- IncomeTax Short QuestionsDocument7 pagesIncomeTax Short QuestionsWatsun ArmstrongNo ratings yet

- General Meaning: Edit Source EditDocument38 pagesGeneral Meaning: Edit Source Editsri_bhairiNo ratings yet

- Income Form Other Sources-9Document10 pagesIncome Form Other Sources-9s4sahith50% (2)

- Section Eligible Assessee Type of Income Limits Conditions For Claiming ExemptionDocument32 pagesSection Eligible Assessee Type of Income Limits Conditions For Claiming ExemptionanilpeddamalliNo ratings yet

- Fema Rbi Org inDocument11 pagesFema Rbi Org inamishtheanalystNo ratings yet

- HRM Unit 2 (1) 2Document46 pagesHRM Unit 2 (1) 2Aayush GiriNo ratings yet

- HRM Unit 3Document17 pagesHRM Unit 3Aayush GiriNo ratings yet

- Unit 1 (Marketing Planning)Document9 pagesUnit 1 (Marketing Planning)Aayush GiriNo ratings yet

- Unit 1 (STP)Document6 pagesUnit 1 (STP)Aayush GiriNo ratings yet

- Unit 1 (Buying Decision Process)Document6 pagesUnit 1 (Buying Decision Process)Aayush GiriNo ratings yet

- Unit 2 (Pricing)Document11 pagesUnit 2 (Pricing)Aayush GiriNo ratings yet

- Unit 3 - Clubbing of IncomeDocument10 pagesUnit 3 - Clubbing of IncomeAayush GiriNo ratings yet

- 1 Prospectus FinalDocument283 pages1 Prospectus FinalLaxmikant RathiNo ratings yet

- Quality of Online Banking Services: in Comparitive Study of Sbi & Icici Bank"Document105 pagesQuality of Online Banking Services: in Comparitive Study of Sbi & Icici Bank"Simran ChauhanNo ratings yet

- Working Capital Management: Project ReportDocument41 pagesWorking Capital Management: Project Reportmahnoor afzalNo ratings yet

- ANLG BANK Case StudyDocument9 pagesANLG BANK Case StudyRadhika ThapaNo ratings yet

- Yitay ElemaDocument127 pagesYitay Elemacourse heroNo ratings yet

- India Dream RunDocument13 pagesIndia Dream RunNAMYA ARORANo ratings yet

- Help WalaDocument36 pagesHelp WalaPratikshya KarkiNo ratings yet

- Bharat Petroleum Corporation LTDDocument15 pagesBharat Petroleum Corporation LTDsagunkumarNo ratings yet

- International Equity FinancingDocument14 pagesInternational Equity FinancingMuazzam Mughal100% (1)

- Resume - Anthony J. SilvaDocument6 pagesResume - Anthony J. Silvatonysilva06No ratings yet

- Assignment - 2: Fundamentals of Management Science For Built EnvironmentDocument23 pagesAssignment - 2: Fundamentals of Management Science For Built EnvironmentVarma LakkamrajuNo ratings yet

- Application Form Account Opening UBIDocument4 pagesApplication Form Account Opening UBIDba ApsuNo ratings yet

- JURNAL 3 BISNIS SyariahDocument9 pagesJURNAL 3 BISNIS SyariahGevin SilitongaNo ratings yet

- HR Kazakhstan Country Report FinalDocument20 pagesHR Kazakhstan Country Report Finalanushikha banerjeeNo ratings yet

- Audit-Of-Specialized-Industries-2021-Module To Use-1Document107 pagesAudit-Of-Specialized-Industries-2021-Module To Use-1Virgie MartinezNo ratings yet

- Barclays Money Skills Activity Pack 16 25 YearsDocument50 pagesBarclays Money Skills Activity Pack 16 25 Yearslol123d100% (1)

- A2 Cum LRS FormDocument4 pagesA2 Cum LRS Formdeepakbannu2012No ratings yet

- LW-204 Professional Ethics and Bar Bench Relation and Accountancy For Lawyers PDFDocument2 pagesLW-204 Professional Ethics and Bar Bench Relation and Accountancy For Lawyers PDFRubab ShaikhNo ratings yet

- A Period of Consequence - How Abraaj Sees The World & Outlook, Dec 2008Document66 pagesA Period of Consequence - How Abraaj Sees The World & Outlook, Dec 2008Shirjeel NaseemNo ratings yet

- Pilgrim BankDocument2 pagesPilgrim Bankschatterjee780% (1)

- N-23-14 Jai Alai V BPIDocument2 pagesN-23-14 Jai Alai V BPIKobe Lawrence VeneracionNo ratings yet

- Small and Medium EnterprisesDocument19 pagesSmall and Medium EnterpriseskalaivaniNo ratings yet

- BIBM Program Summary - 05082018Document4 pagesBIBM Program Summary - 05082018mitemkt9683No ratings yet

- Chapter 11 Financial Accounting With Adjustment: Question 1 FuguangDocument15 pagesChapter 11 Financial Accounting With Adjustment: Question 1 FuguangClaudia WongNo ratings yet

- Reconciling The Bank StatementDocument6 pagesReconciling The Bank StatementOSAMANo ratings yet

- Ahsan Mehanti PDFDocument1 pageAhsan Mehanti PDFAftab Kanwal12No ratings yet

- Eurobank Presentation October2015Document76 pagesEurobank Presentation October2015vasilaros.kefNo ratings yet

- Tier 1 capital/TA (Tier 1+tier 2) /TA Tier 1 capital/RWA Including OBS Items (Tier 1+tier 2) /RAW Including OBS ItemsDocument10 pagesTier 1 capital/TA (Tier 1+tier 2) /TA Tier 1 capital/RWA Including OBS Items (Tier 1+tier 2) /RAW Including OBS ItemsThảo ĐỗNo ratings yet

- Performance Evaluation of Urban Co OperDocument131 pagesPerformance Evaluation of Urban Co Operudayaganavi sbNo ratings yet

- M16 Gitm4380 13e Im C16 PDFDocument17 pagesM16 Gitm4380 13e Im C16 PDFGolamSarwar100% (2)