Everything You Need To Know About The Tax Year-End - Vanguard UK Investor

Everything You Need To Know About The Tax Year-End - Vanguard UK Investor

You might also like

- Basic Banking Account As of Feburary 14, 2020: Checking Opening Balance Closing BalanceDocument2 pagesBasic Banking Account As of Feburary 14, 2020: Checking Opening Balance Closing BalanceKellogg Delia100% (1)

- Fake Paystub 2Document1 pageFake Paystub 2Brandon CarpenterNo ratings yet

- FDA Guide To Pension Tax Relief 2021Document15 pagesFDA Guide To Pension Tax Relief 2021FDAunionNo ratings yet

- Cash and Cash Equivalent QuizesDocument4 pagesCash and Cash Equivalent QuizesGIRL100% (1)

- KEY Tax Points From Today'S BudgetDocument6 pagesKEY Tax Points From Today'S Budgetapi-281744226No ratings yet

- KEY Tax Points From Today'S BudgetDocument6 pagesKEY Tax Points From Today'S Budgetapi-281744226No ratings yet

- Seneca Reid Budget Bulletin 2016Document26 pagesSeneca Reid Budget Bulletin 2016SenecaReidNo ratings yet

- Moneysprite Budget Bulletin 2015Document24 pagesMoneysprite Budget Bulletin 2015MoneyspriteNo ratings yet

- Moneysprite Spring Budget 2017 - ReportDocument26 pagesMoneysprite Spring Budget 2017 - ReportMoneyspriteNo ratings yet

- Year-End Tax Guide 2015/16Document10 pagesYear-End Tax Guide 2015/16api-311814387No ratings yet

- SS Tax PlanDocument12 pagesSS Tax PlanChristianNo ratings yet

- Budget Summary PDFDocument18 pagesBudget Summary PDFmark_thurstonNo ratings yet

- KEY Tax Points From George'S Summer Budget: Owner Managed BusinessesDocument8 pagesKEY Tax Points From George'S Summer Budget: Owner Managed Businessesapi-281744226No ratings yet

- Budget 2013Document0 pagesBudget 2013Ern_DabsNo ratings yet

- Tax Planning Guide: 1800 3000 6070 Buyonline@iciciprulifeDocument14 pagesTax Planning Guide: 1800 3000 6070 Buyonline@iciciprulifeRohitNo ratings yet

- Hilton Sharp Clarke Financial Services Money Talk Winter 2014Document4 pagesHilton Sharp Clarke Financial Services Money Talk Winter 2014nathan8848No ratings yet

- Hilton Sharp Clarke Taking Account Spring 2014Document8 pagesHilton Sharp Clarke Taking Account Spring 2014nathan8848No ratings yet

- R04 Trial Study Notes v5.0Document15 pagesR04 Trial Study Notes v5.0michaeleslamiNo ratings yet

- Tax Planning For Year 2010Document24 pagesTax Planning For Year 2010Mehak BhargavaNo ratings yet

- LLB 11Document6 pagesLLB 11shubsNo ratings yet

- Guide To Save Tax in UKDocument8 pagesGuide To Save Tax in UKCyrus KhanNo ratings yet

- Genesys Business Services LTD - Personal and Family Spring Tax Planning Tips - Feb 2010Document1 pageGenesys Business Services LTD - Personal and Family Spring Tax Planning Tips - Feb 2010genesysukNo ratings yet

- Does The Budget Benefit You?Document1 pageDoes The Budget Benefit You?mailwithvaibhav9675No ratings yet

- 5 Tax InstrumentsDocument3 pages5 Tax InstrumentsktsnlNo ratings yet

- Personal Tax - UKDocument8 pagesPersonal Tax - UKAlellie Khay D JordanNo ratings yet

- Ey Budget Connect 2023 Start UpsDocument6 pagesEy Budget Connect 2023 Start Upsgv.vidyadharNo ratings yet

- Finance Act 2020Document9 pagesFinance Act 2020Raza AliNo ratings yet

- EV EIS Guide v3Document13 pagesEV EIS Guide v3dotidis390No ratings yet

- Autumn Statement 2014Document5 pagesAutumn Statement 2014Martin ForsytheNo ratings yet

- Direct Taxes Semester 3 Roll No: 19P0310307: Filing Your Income Tax ReturnDocument5 pagesDirect Taxes Semester 3 Roll No: 19P0310307: Filing Your Income Tax ReturnPriya KudnekarNo ratings yet

- Chapter Seven Tax Planning BackgroundDocument9 pagesChapter Seven Tax Planning BackgroundTriila manillaNo ratings yet

- The Financial Kaleidoscope - July 19 PDFDocument8 pagesThe Financial Kaleidoscope - July 19 PDFhemanth1128No ratings yet

- Tax Planning IndiaDocument20 pagesTax Planning IndiaRohanTheGreatNo ratings yet

- TDS Calculation Sheet in Excel and Slabs For FY 2017-18 and AY 2018-19Document5 pagesTDS Calculation Sheet in Excel and Slabs For FY 2017-18 and AY 2018-19Nishit MarvaniaNo ratings yet

- Budget 2020 What It Means For YouDocument3 pagesBudget 2020 What It Means For YouAngela AlqueroNo ratings yet

- FAQ S On Income Tax 2022-23Document4 pagesFAQ S On Income Tax 2022-23Ranjan SatapathyNo ratings yet

- The Income Tax 2024: A Complete Guide to Permanently Reducing Your Taxes: Step-by-Step StrategiesFrom EverandThe Income Tax 2024: A Complete Guide to Permanently Reducing Your Taxes: Step-by-Step StrategiesNo ratings yet

- Build Tax-Free Wealth: How to Permanently Lower Your Taxes and Build More WealthFrom EverandBuild Tax-Free Wealth: How to Permanently Lower Your Taxes and Build More WealthNo ratings yet

- Federal Budget 2020-21Document7 pagesFederal Budget 2020-21yiang.tranNo ratings yet

- Parametric U.S. Tax Primer 2013.web .CADocument24 pagesParametric U.S. Tax Primer 2013.web .CAGabriella RicardoNo ratings yet

- New Analysis Shows Economic Impact of Obama's 2016 Budget by The Tax FoundationDocument8 pagesNew Analysis Shows Economic Impact of Obama's 2016 Budget by The Tax FoundationBarbara EspinosaNo ratings yet

- MjsmithPWP Autumn Statement 2012 WebDocument10 pagesMjsmithPWP Autumn Statement 2012 Webmiles6026No ratings yet

- SIPP GUIDE A5 03 DownloadDocument20 pagesSIPP GUIDE A5 03 DownloadStephenAshtonNo ratings yet

- Pdfs AFTR2016 PDFDocument111 pagesPdfs AFTR2016 PDFpaulgiron275No ratings yet

- Highlights of Federal Budget of Australia and Its Winners and LosersDocument4 pagesHighlights of Federal Budget of Australia and Its Winners and LosersM.K.PereraNo ratings yet

- CPP Legislation IntroducedDocument3 pagesCPP Legislation IntroducedMeegan ScottNo ratings yet

- 5 Tax-Planning Tips For Salaried People: Share ThisDocument3 pages5 Tax-Planning Tips For Salaried People: Share ThisPriya DubeyNo ratings yet

- How To Make Yourself A MillionaireDocument5 pagesHow To Make Yourself A MillionaireSiddharth MenonNo ratings yet

- Personal Exemptions: UK: Income Tax ExemptionsDocument4 pagesPersonal Exemptions: UK: Income Tax ExemptionsLuiza ŢîmbaliucNo ratings yet

- How To Calculate Income TaxDocument4 pagesHow To Calculate Income TaxreemaNo ratings yet

- Income Tax Saving: Using Only 80C For Tax Saving? New Tax Regime May Be Beneficial For You at This Income - The Economic Times PDFDocument5 pagesIncome Tax Saving: Using Only 80C For Tax Saving? New Tax Regime May Be Beneficial For You at This Income - The Economic Times PDFDDSingh SinghNo ratings yet

- Seize The Day 2016Document24 pagesSeize The Day 2016DrewCampbell-GriffithsNo ratings yet

- Horner Downey 2011 Budget BookletDocument17 pagesHorner Downey 2011 Budget BookletgsdltdNo ratings yet

- Tax Saving and Investment AvenuesDocument39 pagesTax Saving and Investment AvenuesHimanshu SharmaNo ratings yet

- Taxation Flow PresentationDocument73 pagesTaxation Flow PresentationMohan ChoudharyNo ratings yet

- Financial Support For Irish BusinessDocument6 pagesFinancial Support For Irish BusinessInforoomNo ratings yet

- Tax Law Snapshot 2014Document4 pagesTax Law Snapshot 2014HosameldeenSalehNo ratings yet

- PIT09 Tax ReducersDocument8 pagesPIT09 Tax ReducersAlellie Khay D JordanNo ratings yet

- Tax PlanningDocument7 pagesTax PlanningJyoti SinghNo ratings yet

- ITR GuideDocument8 pagesITR Guiderajesh kumar muhal jaatNo ratings yet

- Standardisation of Tax Statement FormatDocument31 pagesStandardisation of Tax Statement FormatContrarian Investors' JournalNo ratings yet

- GST Audit - Trans Hindon - 19!05!2018 by CA. Chitresh GuptaDocument38 pagesGST Audit - Trans Hindon - 19!05!2018 by CA. Chitresh GuptaRavigmailNo ratings yet

- Latihan Soal 1Document1 pageLatihan Soal 1Anggraeni AyuningtyasNo ratings yet

- ACH Written Statement OF Unauthorized Debit 03 13 14 PDFDocument1 pageACH Written Statement OF Unauthorized Debit 03 13 14 PDFwilliam mcinnisNo ratings yet

- Ap Ele 230255Document1 pageAp Ele 230255Mohammad Azhar AliNo ratings yet

- Bsa 2105 Atty. F. R. Soriano Value-Added TaxDocument2 pagesBsa 2105 Atty. F. R. Soriano Value-Added Taxela kikayNo ratings yet

- 12 - Iepf Div 2015 16 2 IntDocument136 pages12 - Iepf Div 2015 16 2 IntRimoNo ratings yet

- Intermediate Accounting 1a Cash and Cash EquivalentsDocument8 pagesIntermediate Accounting 1a Cash and Cash EquivalentsGinalyn FormentosNo ratings yet

- Dabur Presentation 1Document16 pagesDabur Presentation 1srinathr99No ratings yet

- Capital Gains Summary: Residential Property (And Carried Interest)Document4 pagesCapital Gains Summary: Residential Property (And Carried Interest)Hassan jalilNo ratings yet

- Functional Requirements ManagersDocument32 pagesFunctional Requirements ManagersmaibackupimaliNo ratings yet

- WWW - Aieee.nic - In: BE/B.Tech OR B.Arch/B.Planning General/Obc India Rs. 500Document4 pagesWWW - Aieee.nic - In: BE/B.Tech OR B.Arch/B.Planning General/Obc India Rs. 500Narendra MehtaNo ratings yet

- Payment VoucherDocument1 pagePayment Voucherشاہ زر علیNo ratings yet

- Tax Invoice: Service Details: Customer DetailsDocument5 pagesTax Invoice: Service Details: Customer DetailsIT MalurNo ratings yet

- Business and Other Local TaxesDocument73 pagesBusiness and Other Local Taxesflordeliza de jesusNo ratings yet

- Calibehr Business Support Services Pvt. LTD.: ITC Park 6th Floor Tower No.8 CBD Belapur Navi MumbaiDocument1 pageCalibehr Business Support Services Pvt. LTD.: ITC Park 6th Floor Tower No.8 CBD Belapur Navi MumbaiRram NagarNo ratings yet

- Break-Even Analysis (Single Product)Document1 pageBreak-Even Analysis (Single Product)Rikki Mae TeofistoNo ratings yet

- PayablesUnaccountedTransactions - Payables Unaccounted Transactions and Sweep ReportDocument3 pagesPayablesUnaccountedTransactions - Payables Unaccounted Transactions and Sweep ReportLeonardo MenesesNo ratings yet

- English For Academic Purposes (EAP) : Humber - Ca/myhumberDocument4 pagesEnglish For Academic Purposes (EAP) : Humber - Ca/myhumberRodrigo MartinezNo ratings yet

- Vit Men'S Hostel: CircularDocument6 pagesVit Men'S Hostel: CircularSoumyajyoti MukherjeeNo ratings yet

- CAT Rules Against Grossing Up Method On PAYE - 3Document3 pagesCAT Rules Against Grossing Up Method On PAYE - 3vicenza-marie FukoNo ratings yet

- 73 153 1 PBDocument18 pages73 153 1 PBTataNo ratings yet

- Principles of TaxationDocument25 pagesPrinciples of TaxationceejayeNo ratings yet

- Corporation Tax GuideDocument122 pagesCorporation Tax Guideishu1707No ratings yet

- SBF Iocl 19.11.12Document18 pagesSBF Iocl 19.11.12ParameshNo ratings yet

- CPA Review - VAT Quizzer - 2019Document11 pagesCPA Review - VAT Quizzer - 2019Kenneth Bryan Tegerero Tegio50% (2)

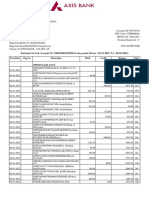

- Acct Statement - XX4920 - 02022023Document4 pagesAcct Statement - XX4920 - 02022023Popi BhowmikNo ratings yet

- BUK View Invoice - ReceiptDocument1 pageBUK View Invoice - ReceiptIbrahim AdewumiNo ratings yet

Download as pdf or txt

You might also like

- Basic Banking Account As of Feburary 14, 2020: Checking Opening Balance Closing BalanceDocument2 pagesBasic Banking Account As of Feburary 14, 2020: Checking Opening Balance Closing BalanceKellogg Delia100% (1)

- Fake Paystub 2Document1 pageFake Paystub 2Brandon CarpenterNo ratings yet

- FDA Guide To Pension Tax Relief 2021Document15 pagesFDA Guide To Pension Tax Relief 2021FDAunionNo ratings yet

- Cash and Cash Equivalent QuizesDocument4 pagesCash and Cash Equivalent QuizesGIRL100% (1)

- KEY Tax Points From Today'S BudgetDocument6 pagesKEY Tax Points From Today'S Budgetapi-281744226No ratings yet

- KEY Tax Points From Today'S BudgetDocument6 pagesKEY Tax Points From Today'S Budgetapi-281744226No ratings yet

- Seneca Reid Budget Bulletin 2016Document26 pagesSeneca Reid Budget Bulletin 2016SenecaReidNo ratings yet

- Moneysprite Budget Bulletin 2015Document24 pagesMoneysprite Budget Bulletin 2015MoneyspriteNo ratings yet

- Moneysprite Spring Budget 2017 - ReportDocument26 pagesMoneysprite Spring Budget 2017 - ReportMoneyspriteNo ratings yet

- Year-End Tax Guide 2015/16Document10 pagesYear-End Tax Guide 2015/16api-311814387No ratings yet

- SS Tax PlanDocument12 pagesSS Tax PlanChristianNo ratings yet

- Budget Summary PDFDocument18 pagesBudget Summary PDFmark_thurstonNo ratings yet

- KEY Tax Points From George'S Summer Budget: Owner Managed BusinessesDocument8 pagesKEY Tax Points From George'S Summer Budget: Owner Managed Businessesapi-281744226No ratings yet

- Budget 2013Document0 pagesBudget 2013Ern_DabsNo ratings yet

- Tax Planning Guide: 1800 3000 6070 Buyonline@iciciprulifeDocument14 pagesTax Planning Guide: 1800 3000 6070 Buyonline@iciciprulifeRohitNo ratings yet

- Hilton Sharp Clarke Financial Services Money Talk Winter 2014Document4 pagesHilton Sharp Clarke Financial Services Money Talk Winter 2014nathan8848No ratings yet

- Hilton Sharp Clarke Taking Account Spring 2014Document8 pagesHilton Sharp Clarke Taking Account Spring 2014nathan8848No ratings yet

- R04 Trial Study Notes v5.0Document15 pagesR04 Trial Study Notes v5.0michaeleslamiNo ratings yet

- Tax Planning For Year 2010Document24 pagesTax Planning For Year 2010Mehak BhargavaNo ratings yet

- LLB 11Document6 pagesLLB 11shubsNo ratings yet

- Guide To Save Tax in UKDocument8 pagesGuide To Save Tax in UKCyrus KhanNo ratings yet

- Genesys Business Services LTD - Personal and Family Spring Tax Planning Tips - Feb 2010Document1 pageGenesys Business Services LTD - Personal and Family Spring Tax Planning Tips - Feb 2010genesysukNo ratings yet

- Does The Budget Benefit You?Document1 pageDoes The Budget Benefit You?mailwithvaibhav9675No ratings yet

- 5 Tax InstrumentsDocument3 pages5 Tax InstrumentsktsnlNo ratings yet

- Personal Tax - UKDocument8 pagesPersonal Tax - UKAlellie Khay D JordanNo ratings yet

- Ey Budget Connect 2023 Start UpsDocument6 pagesEy Budget Connect 2023 Start Upsgv.vidyadharNo ratings yet

- Finance Act 2020Document9 pagesFinance Act 2020Raza AliNo ratings yet

- EV EIS Guide v3Document13 pagesEV EIS Guide v3dotidis390No ratings yet

- Autumn Statement 2014Document5 pagesAutumn Statement 2014Martin ForsytheNo ratings yet

- Direct Taxes Semester 3 Roll No: 19P0310307: Filing Your Income Tax ReturnDocument5 pagesDirect Taxes Semester 3 Roll No: 19P0310307: Filing Your Income Tax ReturnPriya KudnekarNo ratings yet

- Chapter Seven Tax Planning BackgroundDocument9 pagesChapter Seven Tax Planning BackgroundTriila manillaNo ratings yet

- The Financial Kaleidoscope - July 19 PDFDocument8 pagesThe Financial Kaleidoscope - July 19 PDFhemanth1128No ratings yet

- Tax Planning IndiaDocument20 pagesTax Planning IndiaRohanTheGreatNo ratings yet

- TDS Calculation Sheet in Excel and Slabs For FY 2017-18 and AY 2018-19Document5 pagesTDS Calculation Sheet in Excel and Slabs For FY 2017-18 and AY 2018-19Nishit MarvaniaNo ratings yet

- Budget 2020 What It Means For YouDocument3 pagesBudget 2020 What It Means For YouAngela AlqueroNo ratings yet

- FAQ S On Income Tax 2022-23Document4 pagesFAQ S On Income Tax 2022-23Ranjan SatapathyNo ratings yet

- The Income Tax 2024: A Complete Guide to Permanently Reducing Your Taxes: Step-by-Step StrategiesFrom EverandThe Income Tax 2024: A Complete Guide to Permanently Reducing Your Taxes: Step-by-Step StrategiesNo ratings yet

- Build Tax-Free Wealth: How to Permanently Lower Your Taxes and Build More WealthFrom EverandBuild Tax-Free Wealth: How to Permanently Lower Your Taxes and Build More WealthNo ratings yet

- Federal Budget 2020-21Document7 pagesFederal Budget 2020-21yiang.tranNo ratings yet

- Parametric U.S. Tax Primer 2013.web .CADocument24 pagesParametric U.S. Tax Primer 2013.web .CAGabriella RicardoNo ratings yet

- New Analysis Shows Economic Impact of Obama's 2016 Budget by The Tax FoundationDocument8 pagesNew Analysis Shows Economic Impact of Obama's 2016 Budget by The Tax FoundationBarbara EspinosaNo ratings yet

- MjsmithPWP Autumn Statement 2012 WebDocument10 pagesMjsmithPWP Autumn Statement 2012 Webmiles6026No ratings yet

- SIPP GUIDE A5 03 DownloadDocument20 pagesSIPP GUIDE A5 03 DownloadStephenAshtonNo ratings yet

- Pdfs AFTR2016 PDFDocument111 pagesPdfs AFTR2016 PDFpaulgiron275No ratings yet

- Highlights of Federal Budget of Australia and Its Winners and LosersDocument4 pagesHighlights of Federal Budget of Australia and Its Winners and LosersM.K.PereraNo ratings yet

- CPP Legislation IntroducedDocument3 pagesCPP Legislation IntroducedMeegan ScottNo ratings yet

- 5 Tax-Planning Tips For Salaried People: Share ThisDocument3 pages5 Tax-Planning Tips For Salaried People: Share ThisPriya DubeyNo ratings yet

- How To Make Yourself A MillionaireDocument5 pagesHow To Make Yourself A MillionaireSiddharth MenonNo ratings yet

- Personal Exemptions: UK: Income Tax ExemptionsDocument4 pagesPersonal Exemptions: UK: Income Tax ExemptionsLuiza ŢîmbaliucNo ratings yet

- How To Calculate Income TaxDocument4 pagesHow To Calculate Income TaxreemaNo ratings yet

- Income Tax Saving: Using Only 80C For Tax Saving? New Tax Regime May Be Beneficial For You at This Income - The Economic Times PDFDocument5 pagesIncome Tax Saving: Using Only 80C For Tax Saving? New Tax Regime May Be Beneficial For You at This Income - The Economic Times PDFDDSingh SinghNo ratings yet

- Seize The Day 2016Document24 pagesSeize The Day 2016DrewCampbell-GriffithsNo ratings yet

- Horner Downey 2011 Budget BookletDocument17 pagesHorner Downey 2011 Budget BookletgsdltdNo ratings yet

- Tax Saving and Investment AvenuesDocument39 pagesTax Saving and Investment AvenuesHimanshu SharmaNo ratings yet

- Taxation Flow PresentationDocument73 pagesTaxation Flow PresentationMohan ChoudharyNo ratings yet

- Financial Support For Irish BusinessDocument6 pagesFinancial Support For Irish BusinessInforoomNo ratings yet

- Tax Law Snapshot 2014Document4 pagesTax Law Snapshot 2014HosameldeenSalehNo ratings yet

- PIT09 Tax ReducersDocument8 pagesPIT09 Tax ReducersAlellie Khay D JordanNo ratings yet

- Tax PlanningDocument7 pagesTax PlanningJyoti SinghNo ratings yet

- ITR GuideDocument8 pagesITR Guiderajesh kumar muhal jaatNo ratings yet

- Standardisation of Tax Statement FormatDocument31 pagesStandardisation of Tax Statement FormatContrarian Investors' JournalNo ratings yet

- GST Audit - Trans Hindon - 19!05!2018 by CA. Chitresh GuptaDocument38 pagesGST Audit - Trans Hindon - 19!05!2018 by CA. Chitresh GuptaRavigmailNo ratings yet

- Latihan Soal 1Document1 pageLatihan Soal 1Anggraeni AyuningtyasNo ratings yet

- ACH Written Statement OF Unauthorized Debit 03 13 14 PDFDocument1 pageACH Written Statement OF Unauthorized Debit 03 13 14 PDFwilliam mcinnisNo ratings yet

- Ap Ele 230255Document1 pageAp Ele 230255Mohammad Azhar AliNo ratings yet

- Bsa 2105 Atty. F. R. Soriano Value-Added TaxDocument2 pagesBsa 2105 Atty. F. R. Soriano Value-Added Taxela kikayNo ratings yet

- 12 - Iepf Div 2015 16 2 IntDocument136 pages12 - Iepf Div 2015 16 2 IntRimoNo ratings yet

- Intermediate Accounting 1a Cash and Cash EquivalentsDocument8 pagesIntermediate Accounting 1a Cash and Cash EquivalentsGinalyn FormentosNo ratings yet

- Dabur Presentation 1Document16 pagesDabur Presentation 1srinathr99No ratings yet

- Capital Gains Summary: Residential Property (And Carried Interest)Document4 pagesCapital Gains Summary: Residential Property (And Carried Interest)Hassan jalilNo ratings yet

- Functional Requirements ManagersDocument32 pagesFunctional Requirements ManagersmaibackupimaliNo ratings yet

- WWW - Aieee.nic - In: BE/B.Tech OR B.Arch/B.Planning General/Obc India Rs. 500Document4 pagesWWW - Aieee.nic - In: BE/B.Tech OR B.Arch/B.Planning General/Obc India Rs. 500Narendra MehtaNo ratings yet

- Payment VoucherDocument1 pagePayment Voucherشاہ زر علیNo ratings yet

- Tax Invoice: Service Details: Customer DetailsDocument5 pagesTax Invoice: Service Details: Customer DetailsIT MalurNo ratings yet

- Business and Other Local TaxesDocument73 pagesBusiness and Other Local Taxesflordeliza de jesusNo ratings yet

- Calibehr Business Support Services Pvt. LTD.: ITC Park 6th Floor Tower No.8 CBD Belapur Navi MumbaiDocument1 pageCalibehr Business Support Services Pvt. LTD.: ITC Park 6th Floor Tower No.8 CBD Belapur Navi MumbaiRram NagarNo ratings yet

- Break-Even Analysis (Single Product)Document1 pageBreak-Even Analysis (Single Product)Rikki Mae TeofistoNo ratings yet

- PayablesUnaccountedTransactions - Payables Unaccounted Transactions and Sweep ReportDocument3 pagesPayablesUnaccountedTransactions - Payables Unaccounted Transactions and Sweep ReportLeonardo MenesesNo ratings yet

- English For Academic Purposes (EAP) : Humber - Ca/myhumberDocument4 pagesEnglish For Academic Purposes (EAP) : Humber - Ca/myhumberRodrigo MartinezNo ratings yet

- Vit Men'S Hostel: CircularDocument6 pagesVit Men'S Hostel: CircularSoumyajyoti MukherjeeNo ratings yet

- CAT Rules Against Grossing Up Method On PAYE - 3Document3 pagesCAT Rules Against Grossing Up Method On PAYE - 3vicenza-marie FukoNo ratings yet

- 73 153 1 PBDocument18 pages73 153 1 PBTataNo ratings yet

- Principles of TaxationDocument25 pagesPrinciples of TaxationceejayeNo ratings yet

- Corporation Tax GuideDocument122 pagesCorporation Tax Guideishu1707No ratings yet

- SBF Iocl 19.11.12Document18 pagesSBF Iocl 19.11.12ParameshNo ratings yet

- CPA Review - VAT Quizzer - 2019Document11 pagesCPA Review - VAT Quizzer - 2019Kenneth Bryan Tegerero Tegio50% (2)

- Acct Statement - XX4920 - 02022023Document4 pagesAcct Statement - XX4920 - 02022023Popi BhowmikNo ratings yet

- BUK View Invoice - ReceiptDocument1 pageBUK View Invoice - ReceiptIbrahim AdewumiNo ratings yet