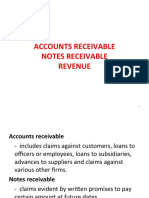

AUD 2 Receivables

AUD 2 Receivables

You might also like

- Substantive Tests of Receivables and SalesDocument4 pagesSubstantive Tests of Receivables and SalesKeith Joshua Gabiason100% (1)

- Performance First Savings: Activity SummaryDocument4 pagesPerformance First Savings: Activity SummaryChris CaytonNo ratings yet

- Chapter 14 AuditingDocument9 pagesChapter 14 Auditingmeiwin manihing100% (1)

- EJTEQJ4JDocument5 pagesEJTEQJ4J132345usdfghj0% (1)

- Auditing Problems: Audit of ReceivablesDocument4 pagesAuditing Problems: Audit of ReceivablesMa. Trixcy De VeraNo ratings yet

- Audit of ReceivablesDocument4 pagesAudit of ReceivablesClarisse AnnNo ratings yet

- Auditing Problems: Audit of ReceivablesDocument4 pagesAuditing Problems: Audit of ReceivablesLaong laanNo ratings yet

- AP Lesson 2Document13 pagesAP Lesson 2Joanne RomaNo ratings yet

- AttachmentDocument14 pagesAttachmentAngelo Jose BalalongNo ratings yet

- Audit of Receivables Lecture NotesDocument10 pagesAudit of Receivables Lecture NotesDebs Fanoga100% (1)

- Audit of ReceivablesDocument15 pagesAudit of ReceivablesLouie De La Torre75% (4)

- Audit of Receivables-1Document16 pagesAudit of Receivables-1jennyMBNo ratings yet

- Audit of ReceivablesDocument3 pagesAudit of ReceivablesJhedz CartasNo ratings yet

- Concepts and PrinciplesDocument13 pagesConcepts and PrinciplesJonafhel RaguinNo ratings yet

- Audit of LiabilitiesDocument5 pagesAudit of LiabilitiesGille Rosa Abajar100% (1)

- 06 ReceivableDocument104 pages06 Receivablefordan Zodorovic100% (4)

- Audit II CH 06 AuditDocument4 pagesAudit II CH 06 AuditmissaassefaNo ratings yet

- Audit G1Document73 pagesAudit G1Jasmine ManuelNo ratings yet

- AUD 2 Audit of Cash and Cash EquivalentDocument14 pagesAUD 2 Audit of Cash and Cash EquivalentJayron NonguiNo ratings yet

- Chapter14 - Answer PDFDocument18 pagesChapter14 - Answer PDFJONAS VINCENT SamsonNo ratings yet

- Lesson 6 - Liabilities - Substantive Tests of Details of BalancesDocument30 pagesLesson 6 - Liabilities - Substantive Tests of Details of BalancesNiña YastoNo ratings yet

- Infonet College: Learning GuideDocument19 pagesInfonet College: Learning Guidemac video teachingNo ratings yet

- Audit of ReceivableDocument14 pagesAudit of ReceivableMr.AccntngNo ratings yet

- Chapter 14 - Accounts Payables and Other LiabilitisDocument28 pagesChapter 14 - Accounts Payables and Other LiabilitisHamda AbdinasirNo ratings yet

- 00 Quick Notes - Revenue and Receipt Cycle PDFDocument5 pages00 Quick Notes - Revenue and Receipt Cycle PDFBecky GonzagaNo ratings yet

- Chapter 6: Audit of Current LiabilityDocument14 pagesChapter 6: Audit of Current LiabilityYidersal DagnawNo ratings yet

- ACC 205 - ReceivablesDocument32 pagesACC 205 - ReceivablesPhilip LarozaNo ratings yet

- Accounts Receivable: Chartered Institute of Internal AuditorsDocument7 pagesAccounts Receivable: Chartered Institute of Internal AuditorsClarice GuintibanoNo ratings yet

- 13 - Audit of Revenue and ReceivablesDocument14 pages13 - Audit of Revenue and ReceivablesChrista LenzNo ratings yet

- Audit of Receivables - AuditingDocument9 pagesAudit of Receivables - AuditingTara WelshNo ratings yet

- Book SolutionDocument5 pagesBook SolutionJ. EDUNo ratings yet

- ReceivablesDocument12 pagesReceivablesRizalene AgustinNo ratings yet

- Acctg 3 - Learning Material 2, Lesson 1Document13 pagesAcctg 3 - Learning Material 2, Lesson 1Darleen CantiladoNo ratings yet

- FAR Self-Made ReviewerDocument2 pagesFAR Self-Made ReviewerAngelica SumatraNo ratings yet

- Financial Accounting - Study Guide Chapter 7: Internal Control and Cash Internal Control SystemDocument3 pagesFinancial Accounting - Study Guide Chapter 7: Internal Control and Cash Internal Control SystemMurtaza HussainNo ratings yet

- Manage Overdue Customer AccountsDocument15 pagesManage Overdue Customer Accountsmulehabesha.mhNo ratings yet

- Qa Audit of Receivables and SalesDocument7 pagesQa Audit of Receivables and SalesAsniah M. RatabanNo ratings yet

- Center For Review and Special Studies - : Practical Accounting 1/theory of Accounts M. B. GuiaDocument15 pagesCenter For Review and Special Studies - : Practical Accounting 1/theory of Accounts M. B. GuiaSano ManjiroNo ratings yet

- PA1C5 Rec NACFNDocument18 pagesPA1C5 Rec NACFNShaggYNo ratings yet

- Audit of Receivables WubexDocument9 pagesAudit of Receivables WubexZelalem HassenNo ratings yet

- Module 3A - ACCCOB2 Lecture 3 - Receivables T1AY2021Document14 pagesModule 3A - ACCCOB2 Lecture 3 - Receivables T1AY2021Cale Robert RascoNo ratings yet

- Accounts Receivable Notes Receivable RevenueDocument11 pagesAccounts Receivable Notes Receivable RevenueVatchdemonNo ratings yet

- Accounts Theory Q&A - CA Zubair KhanDocument16 pagesAccounts Theory Q&A - CA Zubair KhanAnanya SharmaNo ratings yet

- Topic7 Ch12 ReceivablesDocument29 pagesTopic7 Ch12 ReceivablesCẩm TúNo ratings yet

- FS Audit. Chapter 2Document53 pagesFS Audit. Chapter 2050609212050No ratings yet

- FAR 4.2 ReceivablesDocument15 pagesFAR 4.2 ReceivablesNychi SitchonNo ratings yet

- Chapter 13 Financial Management by CabreraDocument25 pagesChapter 13 Financial Management by CabreraLars FriasNo ratings yet

- Kaplan Audit Procedures GuidanceDocument18 pagesKaplan Audit Procedures Guidancebasit ovaisiNo ratings yet

- AT Lecture 8 - Tests of Transaction CycleDocument13 pagesAT Lecture 8 - Tests of Transaction CycleダニエルNo ratings yet

- Chapter 15 Audit of Other Items of Statement of Financial PositionDocument13 pagesChapter 15 Audit of Other Items of Statement of Financial PositionMiaNo ratings yet

- Module 1 Revenue CycleDocument11 pagesModule 1 Revenue CycleNova PringNo ratings yet

- AuditofLiabilities PDFDocument6 pagesAuditofLiabilities PDFEricka Mher IsletaNo ratings yet

- Financial Control Blueprint: Building a Path to Growth and SuccessFrom EverandFinancial Control Blueprint: Building a Path to Growth and SuccessNo ratings yet

- Engagement Essentials: Preparation, Compilation, and Review of Financial StatementsFrom EverandEngagement Essentials: Preparation, Compilation, and Review of Financial StatementsNo ratings yet

- Annual Update and Practice Issues for Preparation, Compilation, and Review EngagementsFrom EverandAnnual Update and Practice Issues for Preparation, Compilation, and Review EngagementsNo ratings yet

- Textbook of Urgent Care Management: Chapter 13, Financial ManagementFrom EverandTextbook of Urgent Care Management: Chapter 13, Financial ManagementNo ratings yet

- 14.17 Al MuqasatDocument5 pages14.17 Al Muqasatamelia stephanie100% (1)

- Demo Company AU - Bank ReconciliationDocument3 pagesDemo Company AU - Bank ReconciliationApril Ann C. GarciaNo ratings yet

- HDFC-Offer-Croma Electronics - Online Electronics Shopping - Buy Electronics OnlineDocument1 pageHDFC-Offer-Croma Electronics - Online Electronics Shopping - Buy Electronics OnlineSahil VishwasNo ratings yet

- ApplicationDocument2 pagesApplicationFabian SandovalNo ratings yet

- Process of Retail LendingDocument26 pagesProcess of Retail Lendingkaren sunil100% (1)

- Financial Management: Topic: Session 6: Philippine Financial Securities and InstitutionsDocument9 pagesFinancial Management: Topic: Session 6: Philippine Financial Securities and InstitutionsAngelo MedinaNo ratings yet

- Natural Care Service Package (NCSP) Agreement: Cuckoo International (B) SDN BHDDocument1 pageNatural Care Service Package (NCSP) Agreement: Cuckoo International (B) SDN BHDWesdi DNo ratings yet

- Provident Fund: How Should Provident Fund Trust Deed and Rules Consist ofDocument3 pagesProvident Fund: How Should Provident Fund Trust Deed and Rules Consist ofAzhar Rana100% (1)

- (EPaC) PDFDocument2 pages(EPaC) PDFTamenji BandaNo ratings yet

- Economies of ScaleDocument6 pagesEconomies of ScaleWordsmith WriterNo ratings yet

- ATM White Label ATM PDFDocument2 pagesATM White Label ATM PDFSURENDRA SAHUNo ratings yet

- SVB Financial Group: United States Securities and Exchange Commission FORM 10-KDocument264 pagesSVB Financial Group: United States Securities and Exchange Commission FORM 10-KBit BitNo ratings yet

- Corporate Net Banking FormDocument6 pagesCorporate Net Banking FormUjjwalNo ratings yet

- 18 (Salvo Automaticamente)Document36 pages18 (Salvo Automaticamente)Tuanny RochaNo ratings yet

- United Delhi DataDocument53 pagesUnited Delhi Data3Sigma Financial Services 3Sigma100% (1)

- International FinanceDocument202 pagesInternational FinanceKannan RNo ratings yet

- Regions Bank StaDocument1 pageRegions Bank StaGIDEONNo ratings yet

- Customer Acknowledgment Form: Applicant InformationDocument2 pagesCustomer Acknowledgment Form: Applicant InformationKamlesh SonareNo ratings yet

- Currency Codes of SEA and MEA CountiresDocument3 pagesCurrency Codes of SEA and MEA Countiresnikhil chhipaNo ratings yet

- PDF Cibil Report PDFDocument8 pagesPDF Cibil Report PDFMargub SubhaniNo ratings yet

- Financial Institutions and Markets: Subject Code: EL15FN505Document63 pagesFinancial Institutions and Markets: Subject Code: EL15FN505Anusha RajNo ratings yet

- Arba Minch Univeristy School of Business and Economics: ID PRBE/075/13Document8 pagesArba Minch Univeristy School of Business and Economics: ID PRBE/075/13Wara GobeNo ratings yet

- Is The Banking Sector An Attractive One To Bring in Foreign Investment in NepalDocument4 pagesIs The Banking Sector An Attractive One To Bring in Foreign Investment in NepalSandesh ShahNo ratings yet

- Dear Kim!Document3 pagesDear Kim!carter michealNo ratings yet

- Financial Services Numerical ExamplesDocument21 pagesFinancial Services Numerical ExamplesgauravNo ratings yet

- Institute of Bankers Pakistan: Branch BankingDocument4 pagesInstitute of Bankers Pakistan: Branch BankingMuhammad KashifNo ratings yet

- Capital Structure and LeverageDocument44 pagesCapital Structure and LeverageThifan AnjarNo ratings yet

- PGL 1b EurosDocument5 pagesPGL 1b EurosAbdul AzizNo ratings yet

Download as pdf or txt

You might also like

- Substantive Tests of Receivables and SalesDocument4 pagesSubstantive Tests of Receivables and SalesKeith Joshua Gabiason100% (1)

- Performance First Savings: Activity SummaryDocument4 pagesPerformance First Savings: Activity SummaryChris CaytonNo ratings yet

- Chapter 14 AuditingDocument9 pagesChapter 14 Auditingmeiwin manihing100% (1)

- EJTEQJ4JDocument5 pagesEJTEQJ4J132345usdfghj0% (1)

- Auditing Problems: Audit of ReceivablesDocument4 pagesAuditing Problems: Audit of ReceivablesMa. Trixcy De VeraNo ratings yet

- Audit of ReceivablesDocument4 pagesAudit of ReceivablesClarisse AnnNo ratings yet

- Auditing Problems: Audit of ReceivablesDocument4 pagesAuditing Problems: Audit of ReceivablesLaong laanNo ratings yet

- AP Lesson 2Document13 pagesAP Lesson 2Joanne RomaNo ratings yet

- AttachmentDocument14 pagesAttachmentAngelo Jose BalalongNo ratings yet

- Audit of Receivables Lecture NotesDocument10 pagesAudit of Receivables Lecture NotesDebs Fanoga100% (1)

- Audit of ReceivablesDocument15 pagesAudit of ReceivablesLouie De La Torre75% (4)

- Audit of Receivables-1Document16 pagesAudit of Receivables-1jennyMBNo ratings yet

- Audit of ReceivablesDocument3 pagesAudit of ReceivablesJhedz CartasNo ratings yet

- Concepts and PrinciplesDocument13 pagesConcepts and PrinciplesJonafhel RaguinNo ratings yet

- Audit of LiabilitiesDocument5 pagesAudit of LiabilitiesGille Rosa Abajar100% (1)

- 06 ReceivableDocument104 pages06 Receivablefordan Zodorovic100% (4)

- Audit II CH 06 AuditDocument4 pagesAudit II CH 06 AuditmissaassefaNo ratings yet

- Audit G1Document73 pagesAudit G1Jasmine ManuelNo ratings yet

- AUD 2 Audit of Cash and Cash EquivalentDocument14 pagesAUD 2 Audit of Cash and Cash EquivalentJayron NonguiNo ratings yet

- Chapter14 - Answer PDFDocument18 pagesChapter14 - Answer PDFJONAS VINCENT SamsonNo ratings yet

- Lesson 6 - Liabilities - Substantive Tests of Details of BalancesDocument30 pagesLesson 6 - Liabilities - Substantive Tests of Details of BalancesNiña YastoNo ratings yet

- Infonet College: Learning GuideDocument19 pagesInfonet College: Learning Guidemac video teachingNo ratings yet

- Audit of ReceivableDocument14 pagesAudit of ReceivableMr.AccntngNo ratings yet

- Chapter 14 - Accounts Payables and Other LiabilitisDocument28 pagesChapter 14 - Accounts Payables and Other LiabilitisHamda AbdinasirNo ratings yet

- 00 Quick Notes - Revenue and Receipt Cycle PDFDocument5 pages00 Quick Notes - Revenue and Receipt Cycle PDFBecky GonzagaNo ratings yet

- Chapter 6: Audit of Current LiabilityDocument14 pagesChapter 6: Audit of Current LiabilityYidersal DagnawNo ratings yet

- ACC 205 - ReceivablesDocument32 pagesACC 205 - ReceivablesPhilip LarozaNo ratings yet

- Accounts Receivable: Chartered Institute of Internal AuditorsDocument7 pagesAccounts Receivable: Chartered Institute of Internal AuditorsClarice GuintibanoNo ratings yet

- 13 - Audit of Revenue and ReceivablesDocument14 pages13 - Audit of Revenue and ReceivablesChrista LenzNo ratings yet

- Audit of Receivables - AuditingDocument9 pagesAudit of Receivables - AuditingTara WelshNo ratings yet

- Book SolutionDocument5 pagesBook SolutionJ. EDUNo ratings yet

- ReceivablesDocument12 pagesReceivablesRizalene AgustinNo ratings yet

- Acctg 3 - Learning Material 2, Lesson 1Document13 pagesAcctg 3 - Learning Material 2, Lesson 1Darleen CantiladoNo ratings yet

- FAR Self-Made ReviewerDocument2 pagesFAR Self-Made ReviewerAngelica SumatraNo ratings yet

- Financial Accounting - Study Guide Chapter 7: Internal Control and Cash Internal Control SystemDocument3 pagesFinancial Accounting - Study Guide Chapter 7: Internal Control and Cash Internal Control SystemMurtaza HussainNo ratings yet

- Manage Overdue Customer AccountsDocument15 pagesManage Overdue Customer Accountsmulehabesha.mhNo ratings yet

- Qa Audit of Receivables and SalesDocument7 pagesQa Audit of Receivables and SalesAsniah M. RatabanNo ratings yet

- Center For Review and Special Studies - : Practical Accounting 1/theory of Accounts M. B. GuiaDocument15 pagesCenter For Review and Special Studies - : Practical Accounting 1/theory of Accounts M. B. GuiaSano ManjiroNo ratings yet

- PA1C5 Rec NACFNDocument18 pagesPA1C5 Rec NACFNShaggYNo ratings yet

- Audit of Receivables WubexDocument9 pagesAudit of Receivables WubexZelalem HassenNo ratings yet

- Module 3A - ACCCOB2 Lecture 3 - Receivables T1AY2021Document14 pagesModule 3A - ACCCOB2 Lecture 3 - Receivables T1AY2021Cale Robert RascoNo ratings yet

- Accounts Receivable Notes Receivable RevenueDocument11 pagesAccounts Receivable Notes Receivable RevenueVatchdemonNo ratings yet

- Accounts Theory Q&A - CA Zubair KhanDocument16 pagesAccounts Theory Q&A - CA Zubair KhanAnanya SharmaNo ratings yet

- Topic7 Ch12 ReceivablesDocument29 pagesTopic7 Ch12 ReceivablesCẩm TúNo ratings yet

- FS Audit. Chapter 2Document53 pagesFS Audit. Chapter 2050609212050No ratings yet

- FAR 4.2 ReceivablesDocument15 pagesFAR 4.2 ReceivablesNychi SitchonNo ratings yet

- Chapter 13 Financial Management by CabreraDocument25 pagesChapter 13 Financial Management by CabreraLars FriasNo ratings yet

- Kaplan Audit Procedures GuidanceDocument18 pagesKaplan Audit Procedures Guidancebasit ovaisiNo ratings yet

- AT Lecture 8 - Tests of Transaction CycleDocument13 pagesAT Lecture 8 - Tests of Transaction CycleダニエルNo ratings yet

- Chapter 15 Audit of Other Items of Statement of Financial PositionDocument13 pagesChapter 15 Audit of Other Items of Statement of Financial PositionMiaNo ratings yet

- Module 1 Revenue CycleDocument11 pagesModule 1 Revenue CycleNova PringNo ratings yet

- AuditofLiabilities PDFDocument6 pagesAuditofLiabilities PDFEricka Mher IsletaNo ratings yet

- Financial Control Blueprint: Building a Path to Growth and SuccessFrom EverandFinancial Control Blueprint: Building a Path to Growth and SuccessNo ratings yet

- Engagement Essentials: Preparation, Compilation, and Review of Financial StatementsFrom EverandEngagement Essentials: Preparation, Compilation, and Review of Financial StatementsNo ratings yet

- Annual Update and Practice Issues for Preparation, Compilation, and Review EngagementsFrom EverandAnnual Update and Practice Issues for Preparation, Compilation, and Review EngagementsNo ratings yet

- Textbook of Urgent Care Management: Chapter 13, Financial ManagementFrom EverandTextbook of Urgent Care Management: Chapter 13, Financial ManagementNo ratings yet

- 14.17 Al MuqasatDocument5 pages14.17 Al Muqasatamelia stephanie100% (1)

- Demo Company AU - Bank ReconciliationDocument3 pagesDemo Company AU - Bank ReconciliationApril Ann C. GarciaNo ratings yet

- HDFC-Offer-Croma Electronics - Online Electronics Shopping - Buy Electronics OnlineDocument1 pageHDFC-Offer-Croma Electronics - Online Electronics Shopping - Buy Electronics OnlineSahil VishwasNo ratings yet

- ApplicationDocument2 pagesApplicationFabian SandovalNo ratings yet

- Process of Retail LendingDocument26 pagesProcess of Retail Lendingkaren sunil100% (1)

- Financial Management: Topic: Session 6: Philippine Financial Securities and InstitutionsDocument9 pagesFinancial Management: Topic: Session 6: Philippine Financial Securities and InstitutionsAngelo MedinaNo ratings yet

- Natural Care Service Package (NCSP) Agreement: Cuckoo International (B) SDN BHDDocument1 pageNatural Care Service Package (NCSP) Agreement: Cuckoo International (B) SDN BHDWesdi DNo ratings yet

- Provident Fund: How Should Provident Fund Trust Deed and Rules Consist ofDocument3 pagesProvident Fund: How Should Provident Fund Trust Deed and Rules Consist ofAzhar Rana100% (1)

- (EPaC) PDFDocument2 pages(EPaC) PDFTamenji BandaNo ratings yet

- Economies of ScaleDocument6 pagesEconomies of ScaleWordsmith WriterNo ratings yet

- ATM White Label ATM PDFDocument2 pagesATM White Label ATM PDFSURENDRA SAHUNo ratings yet

- SVB Financial Group: United States Securities and Exchange Commission FORM 10-KDocument264 pagesSVB Financial Group: United States Securities and Exchange Commission FORM 10-KBit BitNo ratings yet

- Corporate Net Banking FormDocument6 pagesCorporate Net Banking FormUjjwalNo ratings yet

- 18 (Salvo Automaticamente)Document36 pages18 (Salvo Automaticamente)Tuanny RochaNo ratings yet

- United Delhi DataDocument53 pagesUnited Delhi Data3Sigma Financial Services 3Sigma100% (1)

- International FinanceDocument202 pagesInternational FinanceKannan RNo ratings yet

- Regions Bank StaDocument1 pageRegions Bank StaGIDEONNo ratings yet

- Customer Acknowledgment Form: Applicant InformationDocument2 pagesCustomer Acknowledgment Form: Applicant InformationKamlesh SonareNo ratings yet

- Currency Codes of SEA and MEA CountiresDocument3 pagesCurrency Codes of SEA and MEA Countiresnikhil chhipaNo ratings yet

- PDF Cibil Report PDFDocument8 pagesPDF Cibil Report PDFMargub SubhaniNo ratings yet

- Financial Institutions and Markets: Subject Code: EL15FN505Document63 pagesFinancial Institutions and Markets: Subject Code: EL15FN505Anusha RajNo ratings yet

- Arba Minch Univeristy School of Business and Economics: ID PRBE/075/13Document8 pagesArba Minch Univeristy School of Business and Economics: ID PRBE/075/13Wara GobeNo ratings yet

- Is The Banking Sector An Attractive One To Bring in Foreign Investment in NepalDocument4 pagesIs The Banking Sector An Attractive One To Bring in Foreign Investment in NepalSandesh ShahNo ratings yet

- Dear Kim!Document3 pagesDear Kim!carter michealNo ratings yet

- Financial Services Numerical ExamplesDocument21 pagesFinancial Services Numerical ExamplesgauravNo ratings yet

- Institute of Bankers Pakistan: Branch BankingDocument4 pagesInstitute of Bankers Pakistan: Branch BankingMuhammad KashifNo ratings yet

- Capital Structure and LeverageDocument44 pagesCapital Structure and LeverageThifan AnjarNo ratings yet

- PGL 1b EurosDocument5 pagesPGL 1b EurosAbdul AzizNo ratings yet