Download as pdf or txt

You might also like

- H1 Visa Interview Sample Questions and AnswersDocument5 pagesH1 Visa Interview Sample Questions and AnswersNoore Alam SarkarNo ratings yet

- Shilpashatra in Ancient India-Digital LibraryDocument41 pagesShilpashatra in Ancient India-Digital LibraryAshok Nene43% (7)

- Cloud Computing in BPODocument15 pagesCloud Computing in BPORahul KunwarNo ratings yet

- Q2 2010-11 OperatingDocument2 pagesQ2 2010-11 Operatingragzktm00No ratings yet

- 3Q17 Earning Eng FinalDocument18 pages3Q17 Earning Eng FinalarakeelNo ratings yet

- Apresentao 4 QENGDocument17 pagesApresentao 4 QENGMultiplan RINo ratings yet

- TNB HandbookDocument43 pagesTNB HandbookpqcmgtNo ratings yet

- Foreign Owned Businesses 2014 15 ChinaDocument1 pageForeign Owned Businesses 2014 15 ChinasawicNo ratings yet

- COOP Impact of Covid-19 Survey ResultsDocument23 pagesCOOP Impact of Covid-19 Survey ResultsSportsHeroes PhNo ratings yet

- CTRA Results Presentation 3M21Document49 pagesCTRA Results Presentation 3M21Fadhel FebryansyahNo ratings yet

- Electricity Market Design Evolution To Efficiently Integrate Wind and Other Emerging Technologies - ERCOT StyleDocument15 pagesElectricity Market Design Evolution To Efficiently Integrate Wind and Other Emerging Technologies - ERCOT StylePAULO KAJIWARANo ratings yet

- Global Outlook For The Composites Industry: Advanced Engineering Show 2018 - Composites ForumDocument31 pagesGlobal Outlook For The Composites Industry: Advanced Engineering Show 2018 - Composites ForumClaudio Enrique Troncoso ParedesNo ratings yet

- 1 PropertyMarketActivity2020Document3 pages1 PropertyMarketActivity2020ClarenceNo ratings yet

- LMI-LMP-2018 PH Labor Market-March 2019 IssueDocument6 pagesLMI-LMP-2018 PH Labor Market-March 2019 IssueAB AgostoNo ratings yet

- 1Q11 Earnings Release: ParkshoppingsãocaetanoDocument12 pages1Q11 Earnings Release: ParkshoppingsãocaetanoMultiplan RINo ratings yet

- Automotive Division BookDocument30 pagesAutomotive Division BookThe Overlord GirlNo ratings yet

- Turkcell Presentation Q123 ENG VfinalDocument18 pagesTurkcell Presentation Q123 ENG Vfinalmahmoud.te.strategyNo ratings yet

- S&P 500 Earnings Dashboard - Dec. 6Document11 pagesS&P 500 Earnings Dashboard - Dec. 6Anonymous V7Ozz1wnNo ratings yet

- Construction Industry ReportDocument12 pagesConstruction Industry Reportyahoooo1234No ratings yet

- TNB Handbook: Prepared By: Investor Relations & Management Reporting DepartmentDocument34 pagesTNB Handbook: Prepared By: Investor Relations & Management Reporting DepartmentRobert GenaroNo ratings yet

- Emerson Capital Quarterly Performance - 3Q 2009Document1 pageEmerson Capital Quarterly Performance - 3Q 2009Joseph HarrisonNo ratings yet

- Austin Local Market Report by Area March 2011Document27 pagesAustin Local Market Report by Area March 2011Bryce CathcartNo ratings yet

- Multiplan Presentation 1Q09 EngDocument9 pagesMultiplan Presentation 1Q09 EngMultiplan RINo ratings yet

- ProjectDocument8 pagesProjectSharan SharanNo ratings yet

- Thinking Breakthroughs: Group Quarterly Statement For The Period Ended September 30, 2021Document21 pagesThinking Breakthroughs: Group Quarterly Statement For The Period Ended September 30, 2021PolloFlautaNo ratings yet

- Howard County May 09Document1 pageHoward County May 09tmcintyreNo ratings yet

- NWPCap PrivateDebt Q2-2023Document2 pagesNWPCap PrivateDebt Q2-2023zackzyp98No ratings yet

- National Accounts Estimates 2023 q2Document1 pageNational Accounts Estimates 2023 q2Sachini ChathurikaNo ratings yet

- Top 225 Design Firms ENRDocument18 pagesTop 225 Design Firms ENRIon PreascaNo ratings yet

- Res RepDocument11 pagesRes Repwayne adjkqheNo ratings yet

- H1 2018 H2 2018 H1 2019 H2 2019 H1 2020: Unit Launched Sales Performance (%)Document2 pagesH1 2018 H2 2018 H1 2019 H2 2019 H1 2020: Unit Launched Sales Performance (%)zulkis73No ratings yet

- 2023 Q4 Industrial Houston Report ColliersDocument6 pages2023 Q4 Industrial Houston Report ColliersKevin ParkerNo ratings yet

- ACMA PresentationDocument16 pagesACMA Presentationknlpriya05No ratings yet

- Infographics Systems 2016Document4 pagesInfographics Systems 2016SohailNo ratings yet

- Webinar h1 2023 For ParticipantsDocument66 pagesWebinar h1 2023 For ParticipantsChchristiantoNo ratings yet

- China Suzhou Retail Q4 2019 ENGDocument2 pagesChina Suzhou Retail Q4 2019 ENGAprizal PratamaNo ratings yet

- JobsDB Salary Report 2023Document4 pagesJobsDB Salary Report 2023leotong628No ratings yet

- Sector Perfomance 4th Quarter 2013Document18 pagesSector Perfomance 4th Quarter 2013TANATSWA RON CHINENERENo ratings yet

- 2020 10 19 PH S Tel PDFDocument7 pages2020 10 19 PH S Tel PDFJNo ratings yet

- Short History of MalaysiaDocument1 pageShort History of MalaysiaamranNo ratings yet

- EBLSL Daily Market Update 6th August 2020Document1 pageEBLSL Daily Market Update 6th August 2020Moheuddin SehabNo ratings yet

- BASL Daily Market Commentary - 29.07.2019Document3 pagesBASL Daily Market Commentary - 29.07.2019Tanzir HasanNo ratings yet

- 2020 Deloitte India Workforce and Increment Trends Survey - Participant Report PDFDocument82 pages2020 Deloitte India Workforce and Increment Trends Survey - Participant Report PDFAbhishek GuptaNo ratings yet

- Minneapolis 100Document3 pagesMinneapolis 100Jason SandquistNo ratings yet

- 2020-2029 - Tielco - Tablas Island - PSPPDocument18 pages2020-2029 - Tielco - Tablas Island - PSPPHans CunananNo ratings yet

- 4Q17 Earning Eng Final PDFDocument19 pages4Q17 Earning Eng Final PDFPandi IndraNo ratings yet

- Yo University - StrategyDocument33 pagesYo University - StrategyHan YuNo ratings yet

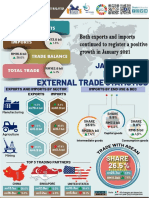

- External Trade Statistics: MalaysiaDocument1 pageExternal Trade Statistics: MalaysiaSiti Khadizah NellyNo ratings yet

- National Accounts Estimates 2023 q1Document1 pageNational Accounts Estimates 2023 q1henryvijayfNo ratings yet

- Economic Forces: Montgomery CountyDocument78 pagesEconomic Forces: Montgomery CountyM-NCPPCNo ratings yet

- Services Sector : Total EstablishmentsDocument5 pagesServices Sector : Total EstablishmentsMohd Yousuf MasoodNo ratings yet

- Successful Fashion With Personality - PDF RoomDocument176 pagesSuccessful Fashion With Personality - PDF Roomverawu05No ratings yet

- Jakarta Greater Jakarta Industrial Market Update - Q4 2020Document16 pagesJakarta Greater Jakarta Industrial Market Update - Q4 2020Esti SusantiNo ratings yet

- 2010 09 30 PH S DMCDocument3 pages2010 09 30 PH S DMCaaronsayNo ratings yet

- Introduction To Teleperformance Greece - May 2016Document31 pagesIntroduction To Teleperformance Greece - May 2016The Tun 91No ratings yet

- Quarterly Report - September 2021Document6 pagesQuarterly Report - September 2021Chaitanya JagarlapudiNo ratings yet

- ETF Newsletter - February - 23Document20 pagesETF Newsletter - February - 23Chuck CookNo ratings yet

- PAK TIKO Mandiri Investment Forum 2024Document17 pagesPAK TIKO Mandiri Investment Forum 2024fransiska lilianiNo ratings yet

- Handbook of Green Building Des6d7b8f7089cb - Anna's Archive 38Document1 pageHandbook of Green Building Des6d7b8f7089cb - Anna's Archive 38gamedesigning87No ratings yet

- Key Performance Indicators of The Roche GroupDocument4 pagesKey Performance Indicators of The Roche GroupSanjay RathiNo ratings yet

- Power Markets and Economics: Energy Costs, Trading, EmissionsFrom EverandPower Markets and Economics: Energy Costs, Trading, EmissionsNo ratings yet

- Transmission PlanningDocument28 pagesTransmission PlanningLauren M. OlivosNo ratings yet

- 2012 Technical Question GeneratorDocument2 pages2012 Technical Question GeneratorLauren M. OlivosNo ratings yet

- 2012+Transformer+Loss Evaluations Rev4 FinalDocument4 pages2012+Transformer+Loss Evaluations Rev4 FinalLauren M. OlivosNo ratings yet

- Gulf Engineering & Industrial ConsultancyDocument5 pagesGulf Engineering & Industrial ConsultancyLauren M. OlivosNo ratings yet

- Construction MethodologyDocument3 pagesConstruction MethodologyLauren M. Olivos100% (1)

- Will Future Simple Making Predictions Fortune Teller Exercises WorksheetDocument2 pagesWill Future Simple Making Predictions Fortune Teller Exercises WorksheetMaria EduardaNo ratings yet

- CH 7 Timers, Counters, T/C Applications 1Document67 pagesCH 7 Timers, Counters, T/C Applications 1tino pawNo ratings yet

- Effect On The PerformanceDocument11 pagesEffect On The Performancehanna abadiNo ratings yet

- Aircraft Materials, Construction and RepairDocument34 pagesAircraft Materials, Construction and RepairJoshua BarteNo ratings yet

- Lesson 4 - History of Development Economics (First Part)Document12 pagesLesson 4 - History of Development Economics (First Part)Rose RaboNo ratings yet

- ID Strategi Pengembangan Usahatani Ubi Kayu Manihot Utilissima Di Kecamatan MenggalDocument9 pagesID Strategi Pengembangan Usahatani Ubi Kayu Manihot Utilissima Di Kecamatan MenggalBukhori Thomas EdvanNo ratings yet

- The Pathophysiology of Peptic UlcerDocument15 pagesThe Pathophysiology of Peptic UlcerKike Meneses100% (1)

- Code BatmanDocument43 pagesCode BatmanLi Jie TeoNo ratings yet

- CASIODocument9 pagesCASIOThomas GeorgeNo ratings yet

- Acceleration WorksheetDocument3 pagesAcceleration WorksheetJulia RibeiroNo ratings yet

- Intelectual Properties Management For Pharmaceuticals Drugs and Food Products Nurul Ainina (201626099)Document3 pagesIntelectual Properties Management For Pharmaceuticals Drugs and Food Products Nurul Ainina (201626099)Nurul AininaNo ratings yet

- Communicationskillunit1 - LSRWDocument187 pagesCommunicationskillunit1 - LSRWjasjisha4No ratings yet

- 10 Question Related To InheritanceDocument4 pages10 Question Related To InheritancePrashant kumarNo ratings yet

- Acctg 17nd-Final Exam BDocument14 pagesAcctg 17nd-Final Exam BKristinelle AragoNo ratings yet

- Psychiatric Considerations in The Management of Dizzy PatientsDocument10 pagesPsychiatric Considerations in The Management of Dizzy PatientsmykedindealNo ratings yet

- Critical Self-Assessment LetterDocument2 pagesCritical Self-Assessment Letterapi-570528793No ratings yet

- Physics 12 - 4Document30 pagesPhysics 12 - 4zeamayf.biasNo ratings yet

- Republic v. PLDT, 26 SCRA 620Document1 pageRepublic v. PLDT, 26 SCRA 620YANG FLNo ratings yet

- Timeline: 2 To 3 Weeks Timeline 4-5 WeeksDocument1 pageTimeline: 2 To 3 Weeks Timeline 4-5 WeeksKester Ray de VeraNo ratings yet

- Intuitive Surgical JP Morgan PresentationDocument25 pagesIntuitive Surgical JP Morgan PresentationmedtechyNo ratings yet

- Russian Future 2030Document108 pagesRussian Future 2030AnamariaMaximNo ratings yet

- Concept BoardDocument5 pagesConcept BoardMelvin AlarillaNo ratings yet

- SLK Ol5 Q1 W3 Zamora Patrick John BsesDocument4 pagesSLK Ol5 Q1 W3 Zamora Patrick John BsesPatrick John ZamoraNo ratings yet

- Principles of Marketing Eighth Edition Philip Kotler and Gary ArmstrongDocument15 pagesPrinciples of Marketing Eighth Edition Philip Kotler and Gary ArmstrongFahim KhanNo ratings yet

- Glorious Innings of Prof.a R RaoDocument24 pagesGlorious Innings of Prof.a R RaoMeghmeghparva100% (1)

- Polar Loop ManualDocument21 pagesPolar Loop ManualpetarNo ratings yet

- He Had A Vague Sense That Trees Gave Birth To DinosaursDocument2 pagesHe Had A Vague Sense That Trees Gave Birth To DinosaursHusain Adaman TamimyNo ratings yet

- Night of Tournaments 2010 MW2 RulesDocument2 pagesNight of Tournaments 2010 MW2 RulesrohinvijNo ratings yet