Download as docx, pdf, or txt

You might also like

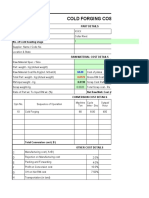

- 94.cold Forging Cost Estimation SheetDocument5 pages94.cold Forging Cost Estimation SheetVenkateswaran venkateswaranNo ratings yet

- Chapter 2-Statement of Financial Position: Problem 2-1 (AICPA Adapted)Document27 pagesChapter 2-Statement of Financial Position: Problem 2-1 (AICPA Adapted)Asi Cas Jav100% (1)

- Transcript - VDO Case - Supply Chain Inventory Management at CrayolaDocument3 pagesTranscript - VDO Case - Supply Chain Inventory Management at CrayolaSakda SiriphattrasophonNo ratings yet

- Chapter 2 #2Document2 pagesChapter 2 #2spp75% (4)

- CH 3 SolutionsDocument37 pagesCH 3 SolutionsRavneet BalNo ratings yet

- Chapter 7 ProblemsDocument25 pagesChapter 7 ProblemsRhoda Claire M. Gansobin100% (1)

- Advacc 1 Millan 2019 Advac 1 Special Transactions 2019Document11 pagesAdvacc 1 Millan 2019 Advac 1 Special Transactions 2019Charlene BolandresNo ratings yet

- Partnership FormationDocument13 pagesPartnership FormationPhilip Dan Jayson LarozaNo ratings yet

- PartnershipDocument7 pagesPartnershipShane Nayah100% (2)

- Special Power of Attorney For Sellers (HQP-HLF-274, V01)Document2 pagesSpecial Power of Attorney For Sellers (HQP-HLF-274, V01)Atoy Liby OjeñarNo ratings yet

- Accounting - Partnership Formation (Answer)Document4 pagesAccounting - Partnership Formation (Answer)mdgomez2021No ratings yet

- 16 UNIT III LiquidationDocument20 pages16 UNIT III LiquidationLeslie Mae Vargas ZafeNo ratings yet

- Instructions: Compute The Amount of Ayesa's Capital Account at September 1, 2014Document10 pagesInstructions: Compute The Amount of Ayesa's Capital Account at September 1, 2014Nicole Fidelson0% (1)

- Problem 8-3Document1 pageProblem 8-3Gilbert MoralesNo ratings yet

- Partnership ActivityDocument12 pagesPartnership ActivityTeresa Pantallano DivinagraciaNo ratings yet

- Chapter 6 FAR Periodic Accounting CycleDocument5 pagesChapter 6 FAR Periodic Accounting CycleShaina Lane B. AmbataliNo ratings yet

- Key Uni 1 Activities Lessons 2 3Document20 pagesKey Uni 1 Activities Lessons 2 3Leslie Mae Vargas ZafeNo ratings yet

- Audit of Cash ActivityDocument13 pagesAudit of Cash ActivityIris FenelleNo ratings yet

- Audit of Cash ActivityDocument13 pagesAudit of Cash ActivityIris FenelleNo ratings yet

- PArtnership FormationDocument6 pagesPArtnership FormationJasmine ActaNo ratings yet

- Answer KeyDocument10 pagesAnswer KeyEvelina Del RosarioNo ratings yet

- Learning Exercises Bsa 3101 Corporate LiquidationDocument2 pagesLearning Exercises Bsa 3101 Corporate LiquidationRachel Mae FajardoNo ratings yet

- Assets: Pedro Castro Statement of Financial Position October 1, 2016Document2 pagesAssets: Pedro Castro Statement of Financial Position October 1, 2016Mandy Bloom0% (1)

- BUSINESS COMBI (Activity On Goodwill Computation) - PALLERDocument5 pagesBUSINESS COMBI (Activity On Goodwill Computation) - PALLERGlayca PallerNo ratings yet

- Nature and Formation of A PartnershipDocument10 pagesNature and Formation of A PartnershipHans ManaliliNo ratings yet

- PacoaDocument12 pagesPacoaSassy GirlNo ratings yet

- Merged-Practice Journal EntriesDocument3 pagesMerged-Practice Journal EntriesAnonymus PershonNo ratings yet

- This Study Resource Was: Current Asset - Cash & Cash Equivalents CompositionsDocument2 pagesThis Study Resource Was: Current Asset - Cash & Cash Equivalents CompositionsKim TanNo ratings yet

- PARCOR Exercises PFormationDocument4 pagesPARCOR Exercises PFormationangelovilladoresNo ratings yet

- Name: Section: Date:: Angel SantaDocument5 pagesName: Section: Date:: Angel SantaJoebet DebuyanNo ratings yet

- Jawaban Soal Uas AklDocument13 pagesJawaban Soal Uas AklAnggari SaputraNo ratings yet

- AK Audit of Cash ACP103Document3 pagesAK Audit of Cash ACP103km dummieNo ratings yet

- Banking Final Accounts: Practical ProblemsDocument2 pagesBanking Final Accounts: Practical ProblemsShubakar ReddyNo ratings yet

- Completing The Acctg CycleDocument14 pagesCompleting The Acctg CycleHearty Hitutua100% (1)

- Abyas Amalgamation IPCC G 1 & 2Document34 pagesAbyas Amalgamation IPCC G 1 & 2Caramakr ManthaNo ratings yet

- ACGA 504/ HCGA 507 General Accounting - Part 2Document17 pagesACGA 504/ HCGA 507 General Accounting - Part 2Eliza BethNo ratings yet

- Basic Accounting Midterm ExamDocument11 pagesBasic Accounting Midterm ExamC J A SNo ratings yet

- SOLMAN Chapter-2Document9 pagesSOLMAN Chapter-2Na JaeminNo ratings yet

- Formation 2022 RDocument5 pagesFormation 2022 Rpamriri8No ratings yet

- Cash Flow Statement Numericals QDocument3 pagesCash Flow Statement Numericals QDheeraj BholaNo ratings yet

- AE13 Final ActivityDocument5 pagesAE13 Final ActivityWenjunNo ratings yet

- Module 2 - SumsDocument4 pagesModule 2 - SumsShubakar ReddyNo ratings yet

- Partnership FormationDocument6 pagesPartnership FormationXajimarie StylesNo ratings yet

- MZM Grocery Store Worksheet For The Year Ended December 31, 2021 Trial Balance Account Titles Debit CreditDocument11 pagesMZM Grocery Store Worksheet For The Year Ended December 31, 2021 Trial Balance Account Titles Debit CreditNichole Joy XielSera Tan100% (1)

- Consolidated Workpaper (Intercompany Sales of Inventory, Plant Assets) (100 Points)Document1 pageConsolidated Workpaper (Intercompany Sales of Inventory, Plant Assets) (100 Points)Yumi ShiwaNo ratings yet

- Acc2 CH11Document6 pagesAcc2 CH11Leah CalataNo ratings yet

- Adobe Scan 07-Jul-2022Document2 pagesAdobe Scan 07-Jul-2022Accounting HelpNo ratings yet

- Problem 1Document13 pagesProblem 1Caila Nicole ReyesNo ratings yet

- Module-3-quiz-JE-Posting-TB FarDocument4 pagesModule-3-quiz-JE-Posting-TB FarNicolle AmoyanNo ratings yet

- Activity Review StatementDocument5 pagesActivity Review Statementangel ciiiNo ratings yet

- LEC09A - BSA 2201 - 022021-Single Entry Accounting (P)Document2 pagesLEC09A - BSA 2201 - 022021-Single Entry Accounting (P)Kim FloresNo ratings yet

- CH3 Accounting EquationDocument43 pagesCH3 Accounting EquationAmr HassanNo ratings yet

- And Liabilities To The PartnershipDocument1 pageAnd Liabilities To The PartnershipOSAMANo ratings yet

- Accounting ActivityDocument3 pagesAccounting ActivityKae Abegail GarciaNo ratings yet

- Cash and Cash EquivalentsDocument2 pagesCash and Cash EquivalentsJennifer EcleNo ratings yet

- Group 1Document2 pagesGroup 1Niro MadlusNo ratings yet

- A 1. FormationDocument3 pagesA 1. Formationmartinfaith958No ratings yet

- Assigment 1Document3 pagesAssigment 1Muhd Zulhusni MusaNo ratings yet

- Adjusting Entries From The Desk F JASDocument3 pagesAdjusting Entries From The Desk F JASMalik of ChakwalNo ratings yet

- Acctg Special TransDocument24 pagesAcctg Special TransMina JjangNo ratings yet

- ACA Audit and Assurance Professional: Exam Preparation KitFrom EverandACA Audit and Assurance Professional: Exam Preparation KitNo ratings yet

- Accounting Principles and Practice: The Commonwealth and International Library: Commerce, Economics and Administration DivisionFrom EverandAccounting Principles and Practice: The Commonwealth and International Library: Commerce, Economics and Administration DivisionRating: 2.5 out of 5 stars2.5/5 (2)

- Financial Accounting-I Sem-1 (GU-DEC-2014)Document12 pagesFinancial Accounting-I Sem-1 (GU-DEC-2014)Ekta RanaNo ratings yet

- Swift Apertura MT700 K315563 20201223Document3 pagesSwift Apertura MT700 K315563 20201223Hasibul Ehsan KhanNo ratings yet

- SAP User Manual - MB21Document16 pagesSAP User Manual - MB21Lajos KovácsNo ratings yet

- Sensex Rolling ReturnsDocument1 pageSensex Rolling Returnsmaheshtech76No ratings yet

- Impact of Covid-19 On Banking SectorDocument2 pagesImpact of Covid-19 On Banking SectorAtia KhalidNo ratings yet

- Market Segments: (Structure of FX Market)Document4 pagesMarket Segments: (Structure of FX Market)Leo the BulldogNo ratings yet

- Gs 51 General 6 PageDocument6 pagesGs 51 General 6 PageOneNationNo ratings yet

- Crane and Matten: Business Ethics (3rd Edition)Document35 pagesCrane and Matten: Business Ethics (3rd Edition)Usama RahmanNo ratings yet

- Travel Elite BRDocument2 pagesTravel Elite BRdevil insideNo ratings yet

- 6195bea26b80c - BAFIA 2073 Summary Questions AnswersDocument10 pages6195bea26b80c - BAFIA 2073 Summary Questions AnswersAnuska Thapa100% (1)

- Indian EconomyDocument4 pagesIndian EconomyLoveleen GargNo ratings yet

- Quick Notes On Growth: Professor: Alan G. Isaac February 3, 2017Document60 pagesQuick Notes On Growth: Professor: Alan G. Isaac February 3, 2017Thk RayyNo ratings yet

- Make My Trip: Dil Toh Roaming HaiDocument23 pagesMake My Trip: Dil Toh Roaming Hairadhikaasharmaa2211No ratings yet

- TYBFM A 36 Vignesh Khandelwal Black BookDocument74 pagesTYBFM A 36 Vignesh Khandelwal Black Bookpreet doshiNo ratings yet

- Principles of Costs and CostingDocument50 pagesPrinciples of Costs and CostingSOOMA OSMANNo ratings yet

- PST ECON 2015 2023Document47 pagesPST ECON 2015 2023PhilipNo ratings yet

- ASSIGNMENT 2 Business CombinationDocument3 pagesASSIGNMENT 2 Business CombinationApril ManjaresNo ratings yet

- ACC 101 - NR Assignment SolutionDocument6 pagesACC 101 - NR Assignment SolutionAdyangNo ratings yet

- University of Gondar Institute of Technology Dep't of Civil EngineeringDocument35 pagesUniversity of Gondar Institute of Technology Dep't of Civil Engineeringbereket gNo ratings yet

- Introduction To Economics Group Assignment KenenisaDocument1 pageIntroduction To Economics Group Assignment KenenisaGelan DuferaNo ratings yet

- Definition of EconomicsDocument5 pagesDefinition of EconomicsKINGS GroupNo ratings yet

- Correct Amount of Inventory 677,500Document8 pagesCorrect Amount of Inventory 677,500Maria Kathreena Andrea AdevaNo ratings yet

- Weekly Credit Update: Week Ending 12 June, 2020Document3 pagesWeekly Credit Update: Week Ending 12 June, 2020muhjaerNo ratings yet

- My Risk BNM Statistical ReportingDocument20 pagesMy Risk BNM Statistical ReportingSoraya AimanNo ratings yet

- Business Com Part 1Document39 pagesBusiness Com Part 1Peter GonzagaNo ratings yet

- Revised Format For Filing Affidavit Regarding Criminal Background, Assets, Liabilities and Educational Qualifications.Document7 pagesRevised Format For Filing Affidavit Regarding Criminal Background, Assets, Liabilities and Educational Qualifications.Nikhil SinghNo ratings yet

- Hosteller 4 TH 5 THDocument4 pagesHosteller 4 TH 5 THDhriti AgarwalNo ratings yet