Download as docx, pdf, or txt

You might also like

- Test Bank For Foundations and Adult Health Nursing 7th Edition by Kim Cooper Kelly GosnellDocument18 pagesTest Bank For Foundations and Adult Health Nursing 7th Edition by Kim Cooper Kelly Gosnellgomeerrorist.g9vfq698% (51)

- AHM13e Chapter - 02 - Solution To Problems and Key To CasesDocument23 pagesAHM13e Chapter - 02 - Solution To Problems and Key To CasesGaurav ManiyarNo ratings yet

- Chapter 23 Statement of Cash Flows Multiple Choice With SolutionsDocument10 pagesChapter 23 Statement of Cash Flows Multiple Choice With SolutionsHossein Parvardeh50% (2)

- Note For ExamDocument58 pagesNote For ExamMichael Al100% (1)

- Tax Homework Chapter 6Document4 pagesTax Homework Chapter 6RosShanique ColebyNo ratings yet

- F7 SolutionsDocument15 pagesF7 Solutionsnoor ul anum100% (1)

- (IFA 13) - Rendy Filiang - 1402210324Document10 pages(IFA 13) - Rendy Filiang - 1402210324RENDY FILIANGNo ratings yet

- Account Excess FV Over BV $ 200,000 Allocations: TotalDocument6 pagesAccount Excess FV Over BV $ 200,000 Allocations: TotalMcKenzie WNo ratings yet

- Akm. P10Document5 pagesAkm. P10Diandra MurtiNo ratings yet

- Assignment 3 ACC 401Document9 pagesAssignment 3 ACC 401ShannonNo ratings yet

- Accounts Gibson Keller Debit CreditDocument4 pagesAccounts Gibson Keller Debit CreditMcKenzie WNo ratings yet

- Tugas Chapter 6 - Sandra Hanania - 120110180024Document4 pagesTugas Chapter 6 - Sandra Hanania - 120110180024Sandra Hanania PasaribuNo ratings yet

- Tax Homework Chapter 4Document7 pagesTax Homework Chapter 4RosShanique ColebyNo ratings yet

- Accounting 121 Third QuarterDocument23 pagesAccounting 121 Third QuarterNow OnwooNo ratings yet

- Alfiani - QUIZ 1 IASDocument23 pagesAlfiani - QUIZ 1 IASWilda Sania MtNo ratings yet

- Inter-Group TransactionDocument11 pagesInter-Group Transaction庄敏敏No ratings yet

- POA MCQ SolutionsDocument141 pagesPOA MCQ SolutionssyrasgamingttNo ratings yet

- Answers To Week 1 HomeworkDocument6 pagesAnswers To Week 1 Homeworkmzvette234No ratings yet

- Chapter 16 Problem SolutionsDocument6 pagesChapter 16 Problem SolutionsAnila ANo ratings yet

- Dispensers of California (Jeff)Document9 pagesDispensers of California (Jeff)Jeffery KaoNo ratings yet

- Exercises Chapter1Document4 pagesExercises Chapter1Huyen Siu NhưnNo ratings yet

- Tarea Balance GeneralDocument198 pagesTarea Balance GeneralalisongarciaaguilarNo ratings yet

- Chapter 5 Solutions To PostDocument43 pagesChapter 5 Solutions To PostJax TellerNo ratings yet

- ACC1701 Revision Session SlidesDocument38 pagesACC1701 Revision Session SlidesshermaineNo ratings yet

- Chapter 11 In-Class Problems SolutionDocument4 pagesChapter 11 In-Class Problems Solutionliuxuhan3No ratings yet

- UAS PA 2020-2021 Ganjil - JawabanDocument27 pagesUAS PA 2020-2021 Ganjil - JawabanNuruddin AsyifaNo ratings yet

- Feed Back Kuis Akl Praktikum (Uts)Document5 pagesFeed Back Kuis Akl Praktikum (Uts)KiwidNo ratings yet

- Gina Purdiyanti - 20181211031 Asdos AKL2Document6 pagesGina Purdiyanti - 20181211031 Asdos AKL2gina amsyarNo ratings yet

- Answers To Extra QuestionsDocument8 pagesAnswers To Extra QuestionsHashani KumarasingheNo ratings yet

- Dari GoogleDocument6 pagesDari Googleabc defNo ratings yet

- Solution E15-18 1: Revaluation EntryDocument3 pagesSolution E15-18 1: Revaluation EntryTk KimNo ratings yet

- ACCA F3-FFA Revision Mock - Answers D15Document12 pagesACCA F3-FFA Revision Mock - Answers D15Kiri chrisNo ratings yet

- Sazkiya Aldina - Lat Soal AKL 1 Chapter 2Document3 pagesSazkiya Aldina - Lat Soal AKL 1 Chapter 2sazkiyaNo ratings yet

- F2 - Mock A - Answers-2-11 143Document10 pagesF2 - Mock A - Answers-2-11 143MD KaifNo ratings yet

- AKL1C - Soal7 Dan E6-11 - Marhaendra Ihza Pahlevi - 18013010085Document4 pagesAKL1C - Soal7 Dan E6-11 - Marhaendra Ihza Pahlevi - 18013010085mahendra ihzaNo ratings yet

- Chapter 1 Answer KeyDocument18 pagesChapter 1 Answer KeyZohaib SiddiqueNo ratings yet

- Assessment Task - Tutorial Questions Assignment Unit Code: HA3011 Question 1 Answer (A It Costed $860,000 To Acquire The Machine. (B)Document7 pagesAssessment Task - Tutorial Questions Assignment Unit Code: HA3011 Question 1 Answer (A It Costed $860,000 To Acquire The Machine. (B)Jaydeep KushwahaNo ratings yet

- Final ExamDocument5 pagesFinal ExamSultan LimitNo ratings yet

- Gonzalez Rincon - Evidencia 3Document17 pagesGonzalez Rincon - Evidencia 3sebgonzalez072006No ratings yet

- Assignment ChemalitDocument8 pagesAssignment ChemalitVinay JajuNo ratings yet

- Jawaban Modul Pertemuan VI - Transaksi Antar Perusahaan - Persediaan (Upstream)Document5 pagesJawaban Modul Pertemuan VI - Transaksi Antar Perusahaan - Persediaan (Upstream)Mega RefiyaniNo ratings yet

- Sheetband & Halyard Inc The Correct AnswerDocument6 pagesSheetband & Halyard Inc The Correct Answermaran_navNo ratings yet

- PA9 TT5.1 Group6Document13 pagesPA9 TT5.1 Group6phamvankhoi281005No ratings yet

- RWJJ Chapter 2: Solutions To Assigned Questions and ProblemsDocument9 pagesRWJJ Chapter 2: Solutions To Assigned Questions and ProblemsvzzrNo ratings yet

- QUIZ 23 Akl 2Document6 pagesQUIZ 23 Akl 2Muhammad Reza AndriantoNo ratings yet

- Latihan AJEDocument13 pagesLatihan AJEkhalzhrni17No ratings yet

- Jawaban Beams Akuntansi p6.6Document11 pagesJawaban Beams Akuntansi p6.6jihan auliaNo ratings yet

- Examination Question and Answers, Set D (Problem Solving), Chapter 15 - Statement of Cash FlowDocument2 pagesExamination Question and Answers, Set D (Problem Solving), Chapter 15 - Statement of Cash Flowjohn carlos doringoNo ratings yet

- P4-3 WPDocument4 pagesP4-3 WPAna LailaNo ratings yet

- Acctg 115 - CH 2 SolutionsDocument9 pagesAcctg 115 - CH 2 SolutionsRand_A100% (1)

- Solutions Chapter 2Document8 pagesSolutions Chapter 2Vân Anh Đỗ LêNo ratings yet

- Akuntansi Keuangan Menengah 1: Kelompok 5 1. Maya Putri Wijaya (142200210) 2. Muhammad Alfarizi (142200278) Kelas EA-IDocument14 pagesAkuntansi Keuangan Menengah 1: Kelompok 5 1. Maya Putri Wijaya (142200210) 2. Muhammad Alfarizi (142200278) Kelas EA-Imuhammad alfariziNo ratings yet

- Amen Cost IIDocument4 pagesAmen Cost IIGetu WeyessaNo ratings yet

- S11171641 - Youvashni Shivali Narayan-20.7Document6 pagesS11171641 - Youvashni Shivali Narayan-20.7shivnilNo ratings yet

- F2 - MOCK A - ANSWERS NowDocument11 pagesF2 - MOCK A - ANSWERS NowRoronoa ZoroNo ratings yet

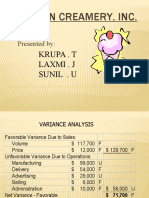

- Boston Creamery CaseDocument9 pagesBoston Creamery Caselion_heart3001100% (1)

- Answers To Concepts Review and Critical Thinking QuestionsDocument6 pagesAnswers To Concepts Review and Critical Thinking QuestionsHimanshu KatheriaNo ratings yet

- Prelim Quiz 1-Problem SolvingDocument3 pagesPrelim Quiz 1-Problem SolvingPaupauNo ratings yet

- Problem Statement: Done By: Nabeel, Cristol, Lekkar, Irfan, Adlin, JoeyDocument19 pagesProblem Statement: Done By: Nabeel, Cristol, Lekkar, Irfan, Adlin, Joeyfariduddin4520No ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Practice Exam BHO2285 T2 2018Document4 pagesPractice Exam BHO2285 T2 2018庄敏敏No ratings yet

- Session 3 Qualitative ResearchDocument44 pagesSession 3 Qualitative Research庄敏敏No ratings yet

- Session 1 Marketing ResearchDocument37 pagesSession 1 Marketing Research庄敏敏No ratings yet

- Assessment 4 Presentation Final PDFDocument20 pagesAssessment 4 Presentation Final PDF庄敏敏No ratings yet

- Session 2 Defining The ProblemDocument46 pagesSession 2 Defining The Problem庄敏敏No ratings yet

- Session 5a Survey ResearchDocument37 pagesSession 5a Survey Research庄敏敏No ratings yet

- Assessment 4 DetailsDocument14 pagesAssessment 4 Details庄敏敏No ratings yet

- Session 10 Bivariate Statistical AnalysisDocument72 pagesSession 10 Bivariate Statistical Analysis庄敏敏No ratings yet

- Session 8 SPSS PracticalDocument12 pagesSession 8 SPSS Practical庄敏敏No ratings yet

- Revision 2 Sem 2 2019Document4 pagesRevision 2 Sem 2 2019庄敏敏No ratings yet

- MARKETINGRESEARCHREVIEWQSDocument10 pagesMARKETINGRESEARCHREVIEWQS庄敏敏No ratings yet

- Session 10 Bivariate Statistical AnalysisDocument72 pagesSession 10 Bivariate Statistical Analysis庄敏敏No ratings yet

- MKTG 470 Marketing Research Exam 1 PDFDocument15 pagesMKTG 470 Marketing Research Exam 1 PDF庄敏敏No ratings yet

- Society Quizzes & Trivia Page 20Document15 pagesSociety Quizzes & Trivia Page 20庄敏敏No ratings yet

- Society Quizzes & Trivia Page 14Document15 pagesSociety Quizzes & Trivia Page 14庄敏敏No ratings yet

- Society Quizzes & Trivia Page 16Document19 pagesSociety Quizzes & Trivia Page 16庄敏敏No ratings yet

- Society Quizzes & Trivia Page 4Document16 pagesSociety Quizzes & Trivia Page 4庄敏敏No ratings yet

- Society Quizzes & Trivia Page 19Document15 pagesSociety Quizzes & Trivia Page 19庄敏敏No ratings yet

- Society Quizzes & Trivia Page 13Document15 pagesSociety Quizzes & Trivia Page 13庄敏敏No ratings yet

- Critical ThinkingDocument8 pagesCritical Thinking庄敏敏No ratings yet

- Society Quizzes & Trivia Page 11Document17 pagesSociety Quizzes & Trivia Page 11庄敏敏No ratings yet

- Society Quizzes & Trivia Page 15Document16 pagesSociety Quizzes & Trivia Page 15庄敏敏No ratings yet

- Society Quizzes & Trivia Page 12Document17 pagesSociety Quizzes & Trivia Page 12庄敏敏No ratings yet

- Society Quizzes & Trivia Page 10Document14 pagesSociety Quizzes & Trivia Page 10庄敏敏No ratings yet

- Society Quizzes & Trivia Page 18Document18 pagesSociety Quizzes & Trivia Page 18庄敏敏No ratings yet

- Society Quizzes & Trivia Page 17Document15 pagesSociety Quizzes & Trivia Page 17庄敏敏No ratings yet

- Society Quizzes & Trivia Page 5Document14 pagesSociety Quizzes & Trivia Page 5庄敏敏No ratings yet

- Society Quizzes & Trivia Page 6Document16 pagesSociety Quizzes & Trivia Page 6庄敏敏No ratings yet

- Society Quizzes & Trivia Page 2Document15 pagesSociety Quizzes & Trivia Page 2庄敏敏No ratings yet

- Society Quizzes & Trivia Page 3Document14 pagesSociety Quizzes & Trivia Page 3庄敏敏No ratings yet

- Oracle ERP Cloud Service Integrations OverviewDocument12 pagesOracle ERP Cloud Service Integrations OverviewSergeyNo ratings yet

- The Walt Disney CompanyDocument2 pagesThe Walt Disney Companyfriend_foru2121No ratings yet

- m1 PT - Specification Writing v1.0-1.GmdDocument28 pagesm1 PT - Specification Writing v1.0-1.GmdMIKA ELLA BALQUINNo ratings yet

- Plaquette FIAC 2023 AngDocument5 pagesPlaquette FIAC 2023 Angsama clintonNo ratings yet

- Ivana Telečki: Unit 1 Careeres / Exercise 1Document4 pagesIvana Telečki: Unit 1 Careeres / Exercise 1benjaminsaraNo ratings yet

- Ethical Issues and Problems in The Business and Corporate WorldDocument4 pagesEthical Issues and Problems in The Business and Corporate WorldMarie Mhel DacapioNo ratings yet

- Global SourcingDocument50 pagesGlobal SourcingJason Chen100% (1)

- Importance of Productivity MeasurementDocument4 pagesImportance of Productivity MeasurementrajatNo ratings yet

- Dissertation Topics in HR For MbaDocument5 pagesDissertation Topics in HR For MbaBuyWritingPaperCanada100% (1)

- Proposal For Edumate: (SEO: Search Engine OptimizerDocument14 pagesProposal For Edumate: (SEO: Search Engine Optimizerseoservices singaporeNo ratings yet

- Project Report On Recuriting and Selection in ParleDocument78 pagesProject Report On Recuriting and Selection in ParleRoyal Projects67% (12)

- Entrepreneurship DevelopmentDocument74 pagesEntrepreneurship DevelopmentrutujachoudeNo ratings yet

- Spec - Shop Inspection RequirementDocument28 pagesSpec - Shop Inspection RequirementarissaNo ratings yet

- Niit ReportDocument122 pagesNiit ReportMohammad ShoebNo ratings yet

- Aquabest FranchisingDocument30 pagesAquabest FranchisingJohn Kenneth Bohol100% (1)

- Mitsubishi Case StudyDocument19 pagesMitsubishi Case StudyAmar KunamNo ratings yet

- Process Overview Business Relationship Management ItilDocument1 pageProcess Overview Business Relationship Management ItilrkamundimuNo ratings yet

- 1.2 Ma Elec 1Document76 pages1.2 Ma Elec 1Feonicel JimenezNo ratings yet

- The Challenges of Nigerian Agricultural Firms in Implementing The Marketing ConceptDocument10 pagesThe Challenges of Nigerian Agricultural Firms in Implementing The Marketing Conceptrohan singhNo ratings yet

- Company Highlights - Manz Slovakia ContactDocument2 pagesCompany Highlights - Manz Slovakia ContactAlexander AvramovNo ratings yet

- QUIz MasDocument1 pageQUIz Maslady chaseNo ratings yet

- SBI ResultsDocument51 pagesSBI ResultssidharthNo ratings yet

- Standstill AgreementDocument3 pagesStandstill AgreementLegal Forms100% (1)

- Ch15 Management Costs and UncertaintyDocument21 pagesCh15 Management Costs and UncertaintyZaira PangesfanNo ratings yet

- Aerospace & Defense - Airline Management Solution Map: Edition 2004Document13 pagesAerospace & Defense - Airline Management Solution Map: Edition 2004Luis Hernandez100% (1)

- Prepare For Final ExamDocument12 pagesPrepare For Final ExamLê Thị Hiền VyNo ratings yet

- ( (Dœmr' Boimßh$Z Ho$ (G'M V Edß Ï'Dhma)Document19 pages( (Dœmr' Boimßh$Z Ho$ (G'M V Edß Ï'Dhma)Satyam MishraNo ratings yet

- Pretest L1 FloristDocument5 pagesPretest L1 FloristnisasuriantoNo ratings yet

- JSMR PDFDocument3 pagesJSMR PDFRaehanunNo ratings yet