CASE 80 - PNB v. Bagamaspad, 89 Phil. 365 (1951)

CASE 80 - PNB v. Bagamaspad, 89 Phil. 365 (1951)

You might also like

- Riano - 2019Document385 pagesRiano - 2019Jemuel Ladaban93% (14)

- 02 CVP Analysis For PrintingDocument8 pages02 CVP Analysis For Printingkristine claire50% (2)

- 5th 57. PNB Vs BagamaspadDocument1 page5th 57. PNB Vs BagamaspadXing Keet LuNo ratings yet

- Danao vs. CADocument5 pagesDanao vs. CAvanessa_3No ratings yet

- Viray and Viola Viray For Petitioner. First Assistant Solicitor General Roberto A. Gianzon and Solicitor Manuel Tomacruz For RespondentDocument13 pagesViray and Viola Viray For Petitioner. First Assistant Solicitor General Roberto A. Gianzon and Solicitor Manuel Tomacruz For RespondentCarren Paulet Villar CuyosNo ratings yet

- Nego Fulltext (Rigor - BPI)Document46 pagesNego Fulltext (Rigor - BPI)Roche DaleNo ratings yet

- Ii. Loan (C. Simple Loan or Mutuum)Document195 pagesIi. Loan (C. Simple Loan or Mutuum)ErikaAlidioNo ratings yet

- Obligations and ContractsDocument220 pagesObligations and ContractsDeon marianoNo ratings yet

- 4) BPI Family Bank vs. FrancoDocument10 pages4) BPI Family Bank vs. FrancoNathalie YapNo ratings yet

- G.R. No. L-24837Document2 pagesG.R. No. L-24837Hanifa D. Al-ObinayNo ratings yet

- Plaintiff-Appellee vs. vs. Defendant-Appellant Solicitor General Isabelo P. SamsonDocument6 pagesPlaintiff-Appellee vs. vs. Defendant-Appellant Solicitor General Isabelo P. SamsonJia Chu ChuaNo ratings yet

- Plaintiffs Appellees Defendants Defendant AppellantDocument16 pagesPlaintiffs Appellees Defendants Defendant AppellantEarl YoungNo ratings yet

- G.R. No. 144887 November 17, 2004 ALFREDO RIGOR, Petitioner, People of The Philippines, Respondent. Azcuna, J.Document5 pagesG.R. No. 144887 November 17, 2004 ALFREDO RIGOR, Petitioner, People of The Philippines, Respondent. Azcuna, J.teepeeNo ratings yet

- Reaction Paper On SeminarDocument5 pagesReaction Paper On SeminarJC TuqueroNo ratings yet

- PNB v. BagamaspadDocument2 pagesPNB v. BagamaspadJP Murao IIINo ratings yet

- Serrano vs. Central BankDocument4 pagesSerrano vs. Central BankVilpa VillabasNo ratings yet

- Petitioner vs. vs. Respondent: Second DivisionDocument7 pagesPetitioner vs. vs. Respondent: Second DivisionVener MargalloNo ratings yet

- Republic of The Philippines: Factual AntecedentsDocument7 pagesRepublic of The Philippines: Factual AntecedentsRobert QuiambaoNo ratings yet

- 142558-1968-Singson - v. - Bank - of - The - Philippine - Islands20210424-12-1hrqm8gDocument3 pages142558-1968-Singson - v. - Bank - of - The - Philippine - Islands20210424-12-1hrqm8gNicorobin RobinNo ratings yet

- 137684-1980-Serrano v. Central Bank of The Philippines20190125-5466-19jls49Document5 pages137684-1980-Serrano v. Central Bank of The Philippines20190125-5466-19jls49ShairaCamilleGarciaNo ratings yet

- Soriano V PeopleDocument21 pagesSoriano V PeopleptbattungNo ratings yet

- BDO UNIBANK v. FRANCISCO PUADocument11 pagesBDO UNIBANK v. FRANCISCO PUAsejinmaNo ratings yet

- Mejia vs. Reyes, 4 SCRA 648Document3 pagesMejia vs. Reyes, 4 SCRA 648Doo RaNo ratings yet

- Credit Transactions - Atty. Julian Rodrigo A. Dela CruzDocument7 pagesCredit Transactions - Atty. Julian Rodrigo A. Dela CruzAndrei Da JoseNo ratings yet

- Case 8 - ART. 1953Document4 pagesCase 8 - ART. 1953krizzledelapenaNo ratings yet

- Digests Muttum PDFDocument16 pagesDigests Muttum PDFdennis buclanNo ratings yet

- 00 Nego Combined All Cases Assignment #1 (Full Text)Document244 pages00 Nego Combined All Cases Assignment #1 (Full Text)Ainah BaratamanNo ratings yet

- 14 National Bank Vs Maza PDFDocument4 pages14 National Bank Vs Maza PDFYollaine GaliasNo ratings yet

- BPI V Franco GR123498Document11 pagesBPI V Franco GR123498Jesus Angelo DiosanaNo ratings yet

- Nego 1Document22 pagesNego 1I.F.S. VillanuevaNo ratings yet

- G.R. No. 148163 - Banco Filipino Savings and Mortgage Bank v. YbañezDocument6 pagesG.R. No. 148163 - Banco Filipino Savings and Mortgage Bank v. YbañezlckdsclNo ratings yet

- 013 Florentino v. PNB, 28 April 1956Document4 pages013 Florentino v. PNB, 28 April 1956Alvin Dela LunaNo ratings yet

- Canon 15 CasesDocument8 pagesCanon 15 CasesGe LatoNo ratings yet

- Soriano V PeopleDocument15 pagesSoriano V PeopleanailabucaNo ratings yet

- F10 PNB Vs BagamaspadDocument1 pageF10 PNB Vs Bagamaspadlucky javellanaNo ratings yet

- Florentino v. PNB, G.R. No. L-8782Document4 pagesFlorentino v. PNB, G.R. No. L-8782Eszle Ann L. ChuaNo ratings yet

- PNB V Luzon SuretyDocument7 pagesPNB V Luzon SuretyChristiane Marie BajadaNo ratings yet

- Week 4 Case Digest - MANLUCOB, Lyra Kaye B.Document6 pagesWeek 4 Case Digest - MANLUCOB, Lyra Kaye B.LYRA KAYE MANLUCOBNo ratings yet

- 1 - Philippine Education Company Vs SorianoDocument4 pages1 - Philippine Education Company Vs SorianoKeej DalonosNo ratings yet

- G.R. No. L-26833Document3 pagesG.R. No. L-26833Julian DubaNo ratings yet

- Digest FinalDocument27 pagesDigest FinalLee YouNo ratings yet

- CASES (Til Degree of Dili)Document296 pagesCASES (Til Degree of Dili)redbutterfly_766No ratings yet

- Case Canon 15Document22 pagesCase Canon 15lynne tahilNo ratings yet

- Bpi vs. Iac L-66826, Aug. 19, 1988Document5 pagesBpi vs. Iac L-66826, Aug. 19, 1988rosario orda-caiseNo ratings yet

- Assignment AdminDocument17 pagesAssignment AdminAngel SosaNo ratings yet

- G.R. No. 144887 November 17, 2004 ALFREDO RIGOR, Petitioner, People of The Philippines, RespondentDocument8 pagesG.R. No. 144887 November 17, 2004 ALFREDO RIGOR, Petitioner, People of The Philippines, RespondentBea BaloyoNo ratings yet

- BPI v. CA, Bonnevie v. CA, Republic v. Bagtas, Republic v. Grualdo, Producers Bank v. CADocument11 pagesBPI v. CA, Bonnevie v. CA, Republic v. Bagtas, Republic v. Grualdo, Producers Bank v. CAMarlon SevillaNo ratings yet

- Petitioner vs. vs. Respondents Agapito S. Fajardo Marino E. Eslao Leovillo C. AgustinDocument6 pagesPetitioner vs. vs. Respondents Agapito S. Fajardo Marino E. Eslao Leovillo C. AgustinKarina GarciaNo ratings yet

- People Vs ConcepcionDocument3 pagesPeople Vs ConcepcionTenten Belita PatricioNo ratings yet

- G.R. No. L-22405, June 30, 1971Document4 pagesG.R. No. L-22405, June 30, 1971Jaymie ValisnoNo ratings yet

- PPL vs. ConcepcionDocument1 pagePPL vs. ConcepcionnvmndNo ratings yet

- Arieta Vs Naric - GR L15645Document12 pagesArieta Vs Naric - GR L15645jovelyn davoNo ratings yet

- Oblicon DigestsDocument6 pagesOblicon Digestscharmae casilNo ratings yet

- Banco Filipino Savings and Mortgage Bank v. YbanezDocument14 pagesBanco Filipino Savings and Mortgage Bank v. YbanezArnold BagalanteNo ratings yet

- Arrieta vs. NARIC, G.R. No. 15645, 31 January 1964Document5 pagesArrieta vs. NARIC, G.R. No. 15645, 31 January 1964Sandra DomingoNo ratings yet

- 1st Set Credit TransactionDocument113 pages1st Set Credit TransactionLiz Matarong BayanoNo ratings yet

- Marcelino B Florentino Vs Philippine National Bank098 Phil 959Document3 pagesMarcelino B Florentino Vs Philippine National Bank098 Phil 959Kathleen Ebilane PulangcoNo ratings yet

- 04 A.C. No. 378 March 30, 1962 JOSE G. MEJIA and EMILIA N. ABRERA vs. FRANCISCO S. REYESDocument2 pages04 A.C. No. 378 March 30, 1962 JOSE G. MEJIA and EMILIA N. ABRERA vs. FRANCISCO S. REYESHechelle S. DE LA CRUZNo ratings yet

- Rigor vs. People G.R. No. 144887Document7 pagesRigor vs. People G.R. No. 144887Gendale Am-isNo ratings yet

- BPI vs. IntermeDocument5 pagesBPI vs. IntermenbragasNo ratings yet

- The Fireside Chats of Franklin Delano Roosevelt Radio Addresses to the American People Broadcast Between 1933 and 1944From EverandThe Fireside Chats of Franklin Delano Roosevelt Radio Addresses to the American People Broadcast Between 1933 and 1944No ratings yet

- Santos Vs RasalanDocument5 pagesSantos Vs RasalanJemuel LadabanNo ratings yet

- Pepsi-Cola Bottling Company of The Philippines, Inc. v. City of ButuanDocument6 pagesPepsi-Cola Bottling Company of The Philippines, Inc. v. City of ButuanJemuel LadabanNo ratings yet

- Case 35 - Zobel Inc. vs. Court of Appeals, G.R. No. 113931 (1998)Document7 pagesCase 35 - Zobel Inc. vs. Court of Appeals, G.R. No. 113931 (1998)Jemuel LadabanNo ratings yet

- Case 28 - Banco Filipino vs. CA (2000)Document13 pagesCase 28 - Banco Filipino vs. CA (2000)Jemuel LadabanNo ratings yet

- Case 1 - Berboso v. CabralDocument10 pagesCase 1 - Berboso v. CabralJemuel LadabanNo ratings yet

- GSIS v. DaymielDocument9 pagesGSIS v. DaymielJemuel LadabanNo ratings yet

- ASTEC v. ERCDocument31 pagesASTEC v. ERCJemuel LadabanNo ratings yet

- Case 5 - Philippine Hawk Corporation v. LeeDocument12 pagesCase 5 - Philippine Hawk Corporation v. LeeJemuel LadabanNo ratings yet

- Case 75 - PHILTRANCO v. PWU-AGLO, G.R. No. 180962, February 26, 2014Document11 pagesCase 75 - PHILTRANCO v. PWU-AGLO, G.R. No. 180962, February 26, 2014Jemuel LadabanNo ratings yet

- Board of Trustees v. VelascoDocument11 pagesBoard of Trustees v. VelascoJemuel LadabanNo ratings yet

- Case 83 - Union of Filipro Employees v. Nestle Philippines, March 3, 2008Document14 pagesCase 83 - Union of Filipro Employees v. Nestle Philippines, March 3, 2008Jemuel LadabanNo ratings yet

- Civil Codal PDFDocument125 pagesCivil Codal PDFAbbieBallesterosNo ratings yet

- CASE 151 - Maynard v. HillDocument6 pagesCASE 151 - Maynard v. HillJemuel LadabanNo ratings yet

- Case 68 - Unilever v. Rivera, G.R. No. 201701, June 3, 2013Document10 pagesCase 68 - Unilever v. Rivera, G.R. No. 201701, June 3, 2013Jemuel LadabanNo ratings yet

- Villamaria v. CA (G.R. No. 165881, April 19, 2006)Document18 pagesVillamaria v. CA (G.R. No. 165881, April 19, 2006)Jemuel LadabanNo ratings yet

- Case 76 - Jordan v. Grandeur Security, G.R. No. 206716, June 18, 2014Document13 pagesCase 76 - Jordan v. Grandeur Security, G.R. No. 206716, June 18, 2014Jemuel LadabanNo ratings yet

- Case 86 - Diolosa v. CADocument2 pagesCase 86 - Diolosa v. CAJemuel LadabanNo ratings yet

- CASE 154 - Capin-Cadiz v. Brent HospitalDocument20 pagesCASE 154 - Capin-Cadiz v. Brent HospitalJemuel LadabanNo ratings yet

- 7 - Kala Manter (Imran Series)Document257 pages7 - Kala Manter (Imran Series)Saim YounisNo ratings yet

- Ch2b Accounting TransactionDocument58 pagesCh2b Accounting TransactionLizette Janiya SumantingNo ratings yet

- Income Tax Planning: A Study of Tax Saving Instruments: PreprintDocument11 pagesIncome Tax Planning: A Study of Tax Saving Instruments: PreprintPallavi PalluNo ratings yet

- A Comparison of The Finance Companies in BangladeshDocument27 pagesA Comparison of The Finance Companies in BangladeshAnik MuidNo ratings yet

- ERP Software - Financial Accounting Module ProposalDocument19 pagesERP Software - Financial Accounting Module Proposalrohit@turtlerepublic.com0% (1)

- Junior Philippine Institute of AccountantsDocument6 pagesJunior Philippine Institute of AccountantsA BNo ratings yet

- Tutorial FIN221 Chapter 3 - Part 1 (Q&A)Document17 pagesTutorial FIN221 Chapter 3 - Part 1 (Q&A)jojojoNo ratings yet

- JFK Vs The Fed - Fractional BankingDocument8 pagesJFK Vs The Fed - Fractional BankingAprajita SinghNo ratings yet

- Answer Far270 Feb2021Document8 pagesAnswer Far270 Feb2021Nur Fatin AmirahNo ratings yet

- Joy and Jolly Day Care CentreDocument20 pagesJoy and Jolly Day Care CentreSsemakula FrankNo ratings yet

- Invoice: Excelcargo LogisticsDocument1 pageInvoice: Excelcargo LogisticsJohn MaxwellNo ratings yet

- Assessing The Risk of Material Misstatement: Audit I Class Unsoed 22 May 2021Document37 pagesAssessing The Risk of Material Misstatement: Audit I Class Unsoed 22 May 2021julietNo ratings yet

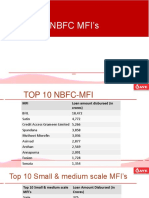

- NBFC Mfi AnalysisDocument10 pagesNBFC Mfi AnalysisNeeraj KumarNo ratings yet

- Chapter 22 Contract CostingDocument18 pagesChapter 22 Contract CostingPavan Kalyan JennyNo ratings yet

- APC 403 PFRS For SMEsDocument10 pagesAPC 403 PFRS For SMEsHazel Seguerra BicadaNo ratings yet

- Multiple Choice - DerivativesDocument3 pagesMultiple Choice - DerivativesLouiseNo ratings yet

- ACC 308 Final Management AnalysisDocument6 pagesACC 308 Final Management AnalysisBREANNA JOHNSONNo ratings yet

- Cashless Society: Presented By: Arsalan ArifDocument24 pagesCashless Society: Presented By: Arsalan ArifArsalan ArifNo ratings yet

- Assumptions: Dec-YE Unit 2018A 2019A 2020A 2021E 2022E 2023E 2024E 2025EDocument3 pagesAssumptions: Dec-YE Unit 2018A 2019A 2020A 2021E 2022E 2023E 2024E 2025ENouf ANo ratings yet

- The FBI Estimates That 80 Percent of All Mortgage Fraud Involves Collaboration or Collusion by Industry InsidersDocument31 pagesThe FBI Estimates That 80 Percent of All Mortgage Fraud Involves Collaboration or Collusion by Industry Insiders83jjmack50% (2)

- Trigonometry and Investments QuizDocument6 pagesTrigonometry and Investments QuizTimNo ratings yet

- 2019 - 1 POP Final Timetable - 0Document30 pages2019 - 1 POP Final Timetable - 0Anonymous IjhB0kuFNo ratings yet

- Ud Wirastri Siklus AkuntansiDocument39 pagesUd Wirastri Siklus AkuntansiPutri EkawatiNo ratings yet

- Chapter 09: Long-Lived Assets Land 5,000 Additional 15K CASH 100,000 MACHINE 30 or 52 Debt X 100,000Document14 pagesChapter 09: Long-Lived Assets Land 5,000 Additional 15K CASH 100,000 MACHINE 30 or 52 Debt X 100,000mostakNo ratings yet

- Day 1 ECCA TrainingDocument78 pagesDay 1 ECCA Trainingadinsmaradhana100% (1)

- Saregamappd 20211102210939-1Document415 pagesSaregamappd 20211102210939-1dilip kumarNo ratings yet

- Using The MACD EffectivelyDocument21 pagesUsing The MACD Effectivelypderby1No ratings yet

- ACCA Audit & Assurance Complete Notes PwC's AcademyDocument187 pagesACCA Audit & Assurance Complete Notes PwC's AcademyZainab SyedaNo ratings yet

- Introduction To Price Action TradingDocument19 pagesIntroduction To Price Action TradingGio GameloNo ratings yet

Download as pdf or txt

You might also like

- Riano - 2019Document385 pagesRiano - 2019Jemuel Ladaban93% (14)

- 02 CVP Analysis For PrintingDocument8 pages02 CVP Analysis For Printingkristine claire50% (2)

- 5th 57. PNB Vs BagamaspadDocument1 page5th 57. PNB Vs BagamaspadXing Keet LuNo ratings yet

- Danao vs. CADocument5 pagesDanao vs. CAvanessa_3No ratings yet

- Viray and Viola Viray For Petitioner. First Assistant Solicitor General Roberto A. Gianzon and Solicitor Manuel Tomacruz For RespondentDocument13 pagesViray and Viola Viray For Petitioner. First Assistant Solicitor General Roberto A. Gianzon and Solicitor Manuel Tomacruz For RespondentCarren Paulet Villar CuyosNo ratings yet

- Nego Fulltext (Rigor - BPI)Document46 pagesNego Fulltext (Rigor - BPI)Roche DaleNo ratings yet

- Ii. Loan (C. Simple Loan or Mutuum)Document195 pagesIi. Loan (C. Simple Loan or Mutuum)ErikaAlidioNo ratings yet

- Obligations and ContractsDocument220 pagesObligations and ContractsDeon marianoNo ratings yet

- 4) BPI Family Bank vs. FrancoDocument10 pages4) BPI Family Bank vs. FrancoNathalie YapNo ratings yet

- G.R. No. L-24837Document2 pagesG.R. No. L-24837Hanifa D. Al-ObinayNo ratings yet

- Plaintiff-Appellee vs. vs. Defendant-Appellant Solicitor General Isabelo P. SamsonDocument6 pagesPlaintiff-Appellee vs. vs. Defendant-Appellant Solicitor General Isabelo P. SamsonJia Chu ChuaNo ratings yet

- Plaintiffs Appellees Defendants Defendant AppellantDocument16 pagesPlaintiffs Appellees Defendants Defendant AppellantEarl YoungNo ratings yet

- G.R. No. 144887 November 17, 2004 ALFREDO RIGOR, Petitioner, People of The Philippines, Respondent. Azcuna, J.Document5 pagesG.R. No. 144887 November 17, 2004 ALFREDO RIGOR, Petitioner, People of The Philippines, Respondent. Azcuna, J.teepeeNo ratings yet

- Reaction Paper On SeminarDocument5 pagesReaction Paper On SeminarJC TuqueroNo ratings yet

- PNB v. BagamaspadDocument2 pagesPNB v. BagamaspadJP Murao IIINo ratings yet

- Serrano vs. Central BankDocument4 pagesSerrano vs. Central BankVilpa VillabasNo ratings yet

- Petitioner vs. vs. Respondent: Second DivisionDocument7 pagesPetitioner vs. vs. Respondent: Second DivisionVener MargalloNo ratings yet

- Republic of The Philippines: Factual AntecedentsDocument7 pagesRepublic of The Philippines: Factual AntecedentsRobert QuiambaoNo ratings yet

- 142558-1968-Singson - v. - Bank - of - The - Philippine - Islands20210424-12-1hrqm8gDocument3 pages142558-1968-Singson - v. - Bank - of - The - Philippine - Islands20210424-12-1hrqm8gNicorobin RobinNo ratings yet

- 137684-1980-Serrano v. Central Bank of The Philippines20190125-5466-19jls49Document5 pages137684-1980-Serrano v. Central Bank of The Philippines20190125-5466-19jls49ShairaCamilleGarciaNo ratings yet

- Soriano V PeopleDocument21 pagesSoriano V PeopleptbattungNo ratings yet

- BDO UNIBANK v. FRANCISCO PUADocument11 pagesBDO UNIBANK v. FRANCISCO PUAsejinmaNo ratings yet

- Mejia vs. Reyes, 4 SCRA 648Document3 pagesMejia vs. Reyes, 4 SCRA 648Doo RaNo ratings yet

- Credit Transactions - Atty. Julian Rodrigo A. Dela CruzDocument7 pagesCredit Transactions - Atty. Julian Rodrigo A. Dela CruzAndrei Da JoseNo ratings yet

- Case 8 - ART. 1953Document4 pagesCase 8 - ART. 1953krizzledelapenaNo ratings yet

- Digests Muttum PDFDocument16 pagesDigests Muttum PDFdennis buclanNo ratings yet

- 00 Nego Combined All Cases Assignment #1 (Full Text)Document244 pages00 Nego Combined All Cases Assignment #1 (Full Text)Ainah BaratamanNo ratings yet

- 14 National Bank Vs Maza PDFDocument4 pages14 National Bank Vs Maza PDFYollaine GaliasNo ratings yet

- BPI V Franco GR123498Document11 pagesBPI V Franco GR123498Jesus Angelo DiosanaNo ratings yet

- Nego 1Document22 pagesNego 1I.F.S. VillanuevaNo ratings yet

- G.R. No. 148163 - Banco Filipino Savings and Mortgage Bank v. YbañezDocument6 pagesG.R. No. 148163 - Banco Filipino Savings and Mortgage Bank v. YbañezlckdsclNo ratings yet

- 013 Florentino v. PNB, 28 April 1956Document4 pages013 Florentino v. PNB, 28 April 1956Alvin Dela LunaNo ratings yet

- Canon 15 CasesDocument8 pagesCanon 15 CasesGe LatoNo ratings yet

- Soriano V PeopleDocument15 pagesSoriano V PeopleanailabucaNo ratings yet

- F10 PNB Vs BagamaspadDocument1 pageF10 PNB Vs Bagamaspadlucky javellanaNo ratings yet

- Florentino v. PNB, G.R. No. L-8782Document4 pagesFlorentino v. PNB, G.R. No. L-8782Eszle Ann L. ChuaNo ratings yet

- PNB V Luzon SuretyDocument7 pagesPNB V Luzon SuretyChristiane Marie BajadaNo ratings yet

- Week 4 Case Digest - MANLUCOB, Lyra Kaye B.Document6 pagesWeek 4 Case Digest - MANLUCOB, Lyra Kaye B.LYRA KAYE MANLUCOBNo ratings yet

- 1 - Philippine Education Company Vs SorianoDocument4 pages1 - Philippine Education Company Vs SorianoKeej DalonosNo ratings yet

- G.R. No. L-26833Document3 pagesG.R. No. L-26833Julian DubaNo ratings yet

- Digest FinalDocument27 pagesDigest FinalLee YouNo ratings yet

- CASES (Til Degree of Dili)Document296 pagesCASES (Til Degree of Dili)redbutterfly_766No ratings yet

- Case Canon 15Document22 pagesCase Canon 15lynne tahilNo ratings yet

- Bpi vs. Iac L-66826, Aug. 19, 1988Document5 pagesBpi vs. Iac L-66826, Aug. 19, 1988rosario orda-caiseNo ratings yet

- Assignment AdminDocument17 pagesAssignment AdminAngel SosaNo ratings yet

- G.R. No. 144887 November 17, 2004 ALFREDO RIGOR, Petitioner, People of The Philippines, RespondentDocument8 pagesG.R. No. 144887 November 17, 2004 ALFREDO RIGOR, Petitioner, People of The Philippines, RespondentBea BaloyoNo ratings yet

- BPI v. CA, Bonnevie v. CA, Republic v. Bagtas, Republic v. Grualdo, Producers Bank v. CADocument11 pagesBPI v. CA, Bonnevie v. CA, Republic v. Bagtas, Republic v. Grualdo, Producers Bank v. CAMarlon SevillaNo ratings yet

- Petitioner vs. vs. Respondents Agapito S. Fajardo Marino E. Eslao Leovillo C. AgustinDocument6 pagesPetitioner vs. vs. Respondents Agapito S. Fajardo Marino E. Eslao Leovillo C. AgustinKarina GarciaNo ratings yet

- People Vs ConcepcionDocument3 pagesPeople Vs ConcepcionTenten Belita PatricioNo ratings yet

- G.R. No. L-22405, June 30, 1971Document4 pagesG.R. No. L-22405, June 30, 1971Jaymie ValisnoNo ratings yet

- PPL vs. ConcepcionDocument1 pagePPL vs. ConcepcionnvmndNo ratings yet

- Arieta Vs Naric - GR L15645Document12 pagesArieta Vs Naric - GR L15645jovelyn davoNo ratings yet

- Oblicon DigestsDocument6 pagesOblicon Digestscharmae casilNo ratings yet

- Banco Filipino Savings and Mortgage Bank v. YbanezDocument14 pagesBanco Filipino Savings and Mortgage Bank v. YbanezArnold BagalanteNo ratings yet

- Arrieta vs. NARIC, G.R. No. 15645, 31 January 1964Document5 pagesArrieta vs. NARIC, G.R. No. 15645, 31 January 1964Sandra DomingoNo ratings yet

- 1st Set Credit TransactionDocument113 pages1st Set Credit TransactionLiz Matarong BayanoNo ratings yet

- Marcelino B Florentino Vs Philippine National Bank098 Phil 959Document3 pagesMarcelino B Florentino Vs Philippine National Bank098 Phil 959Kathleen Ebilane PulangcoNo ratings yet

- 04 A.C. No. 378 March 30, 1962 JOSE G. MEJIA and EMILIA N. ABRERA vs. FRANCISCO S. REYESDocument2 pages04 A.C. No. 378 March 30, 1962 JOSE G. MEJIA and EMILIA N. ABRERA vs. FRANCISCO S. REYESHechelle S. DE LA CRUZNo ratings yet

- Rigor vs. People G.R. No. 144887Document7 pagesRigor vs. People G.R. No. 144887Gendale Am-isNo ratings yet

- BPI vs. IntermeDocument5 pagesBPI vs. IntermenbragasNo ratings yet

- The Fireside Chats of Franklin Delano Roosevelt Radio Addresses to the American People Broadcast Between 1933 and 1944From EverandThe Fireside Chats of Franklin Delano Roosevelt Radio Addresses to the American People Broadcast Between 1933 and 1944No ratings yet

- Santos Vs RasalanDocument5 pagesSantos Vs RasalanJemuel LadabanNo ratings yet

- Pepsi-Cola Bottling Company of The Philippines, Inc. v. City of ButuanDocument6 pagesPepsi-Cola Bottling Company of The Philippines, Inc. v. City of ButuanJemuel LadabanNo ratings yet

- Case 35 - Zobel Inc. vs. Court of Appeals, G.R. No. 113931 (1998)Document7 pagesCase 35 - Zobel Inc. vs. Court of Appeals, G.R. No. 113931 (1998)Jemuel LadabanNo ratings yet

- Case 28 - Banco Filipino vs. CA (2000)Document13 pagesCase 28 - Banco Filipino vs. CA (2000)Jemuel LadabanNo ratings yet

- Case 1 - Berboso v. CabralDocument10 pagesCase 1 - Berboso v. CabralJemuel LadabanNo ratings yet

- GSIS v. DaymielDocument9 pagesGSIS v. DaymielJemuel LadabanNo ratings yet

- ASTEC v. ERCDocument31 pagesASTEC v. ERCJemuel LadabanNo ratings yet

- Case 5 - Philippine Hawk Corporation v. LeeDocument12 pagesCase 5 - Philippine Hawk Corporation v. LeeJemuel LadabanNo ratings yet

- Case 75 - PHILTRANCO v. PWU-AGLO, G.R. No. 180962, February 26, 2014Document11 pagesCase 75 - PHILTRANCO v. PWU-AGLO, G.R. No. 180962, February 26, 2014Jemuel LadabanNo ratings yet

- Board of Trustees v. VelascoDocument11 pagesBoard of Trustees v. VelascoJemuel LadabanNo ratings yet

- Case 83 - Union of Filipro Employees v. Nestle Philippines, March 3, 2008Document14 pagesCase 83 - Union of Filipro Employees v. Nestle Philippines, March 3, 2008Jemuel LadabanNo ratings yet

- Civil Codal PDFDocument125 pagesCivil Codal PDFAbbieBallesterosNo ratings yet

- CASE 151 - Maynard v. HillDocument6 pagesCASE 151 - Maynard v. HillJemuel LadabanNo ratings yet

- Case 68 - Unilever v. Rivera, G.R. No. 201701, June 3, 2013Document10 pagesCase 68 - Unilever v. Rivera, G.R. No. 201701, June 3, 2013Jemuel LadabanNo ratings yet

- Villamaria v. CA (G.R. No. 165881, April 19, 2006)Document18 pagesVillamaria v. CA (G.R. No. 165881, April 19, 2006)Jemuel LadabanNo ratings yet

- Case 76 - Jordan v. Grandeur Security, G.R. No. 206716, June 18, 2014Document13 pagesCase 76 - Jordan v. Grandeur Security, G.R. No. 206716, June 18, 2014Jemuel LadabanNo ratings yet

- Case 86 - Diolosa v. CADocument2 pagesCase 86 - Diolosa v. CAJemuel LadabanNo ratings yet

- CASE 154 - Capin-Cadiz v. Brent HospitalDocument20 pagesCASE 154 - Capin-Cadiz v. Brent HospitalJemuel LadabanNo ratings yet

- 7 - Kala Manter (Imran Series)Document257 pages7 - Kala Manter (Imran Series)Saim YounisNo ratings yet

- Ch2b Accounting TransactionDocument58 pagesCh2b Accounting TransactionLizette Janiya SumantingNo ratings yet

- Income Tax Planning: A Study of Tax Saving Instruments: PreprintDocument11 pagesIncome Tax Planning: A Study of Tax Saving Instruments: PreprintPallavi PalluNo ratings yet

- A Comparison of The Finance Companies in BangladeshDocument27 pagesA Comparison of The Finance Companies in BangladeshAnik MuidNo ratings yet

- ERP Software - Financial Accounting Module ProposalDocument19 pagesERP Software - Financial Accounting Module Proposalrohit@turtlerepublic.com0% (1)

- Junior Philippine Institute of AccountantsDocument6 pagesJunior Philippine Institute of AccountantsA BNo ratings yet

- Tutorial FIN221 Chapter 3 - Part 1 (Q&A)Document17 pagesTutorial FIN221 Chapter 3 - Part 1 (Q&A)jojojoNo ratings yet

- JFK Vs The Fed - Fractional BankingDocument8 pagesJFK Vs The Fed - Fractional BankingAprajita SinghNo ratings yet

- Answer Far270 Feb2021Document8 pagesAnswer Far270 Feb2021Nur Fatin AmirahNo ratings yet

- Joy and Jolly Day Care CentreDocument20 pagesJoy and Jolly Day Care CentreSsemakula FrankNo ratings yet

- Invoice: Excelcargo LogisticsDocument1 pageInvoice: Excelcargo LogisticsJohn MaxwellNo ratings yet

- Assessing The Risk of Material Misstatement: Audit I Class Unsoed 22 May 2021Document37 pagesAssessing The Risk of Material Misstatement: Audit I Class Unsoed 22 May 2021julietNo ratings yet

- NBFC Mfi AnalysisDocument10 pagesNBFC Mfi AnalysisNeeraj KumarNo ratings yet

- Chapter 22 Contract CostingDocument18 pagesChapter 22 Contract CostingPavan Kalyan JennyNo ratings yet

- APC 403 PFRS For SMEsDocument10 pagesAPC 403 PFRS For SMEsHazel Seguerra BicadaNo ratings yet

- Multiple Choice - DerivativesDocument3 pagesMultiple Choice - DerivativesLouiseNo ratings yet

- ACC 308 Final Management AnalysisDocument6 pagesACC 308 Final Management AnalysisBREANNA JOHNSONNo ratings yet

- Cashless Society: Presented By: Arsalan ArifDocument24 pagesCashless Society: Presented By: Arsalan ArifArsalan ArifNo ratings yet

- Assumptions: Dec-YE Unit 2018A 2019A 2020A 2021E 2022E 2023E 2024E 2025EDocument3 pagesAssumptions: Dec-YE Unit 2018A 2019A 2020A 2021E 2022E 2023E 2024E 2025ENouf ANo ratings yet

- The FBI Estimates That 80 Percent of All Mortgage Fraud Involves Collaboration or Collusion by Industry InsidersDocument31 pagesThe FBI Estimates That 80 Percent of All Mortgage Fraud Involves Collaboration or Collusion by Industry Insiders83jjmack50% (2)

- Trigonometry and Investments QuizDocument6 pagesTrigonometry and Investments QuizTimNo ratings yet

- 2019 - 1 POP Final Timetable - 0Document30 pages2019 - 1 POP Final Timetable - 0Anonymous IjhB0kuFNo ratings yet

- Ud Wirastri Siklus AkuntansiDocument39 pagesUd Wirastri Siklus AkuntansiPutri EkawatiNo ratings yet

- Chapter 09: Long-Lived Assets Land 5,000 Additional 15K CASH 100,000 MACHINE 30 or 52 Debt X 100,000Document14 pagesChapter 09: Long-Lived Assets Land 5,000 Additional 15K CASH 100,000 MACHINE 30 or 52 Debt X 100,000mostakNo ratings yet

- Day 1 ECCA TrainingDocument78 pagesDay 1 ECCA Trainingadinsmaradhana100% (1)

- Saregamappd 20211102210939-1Document415 pagesSaregamappd 20211102210939-1dilip kumarNo ratings yet

- Using The MACD EffectivelyDocument21 pagesUsing The MACD Effectivelypderby1No ratings yet

- ACCA Audit & Assurance Complete Notes PwC's AcademyDocument187 pagesACCA Audit & Assurance Complete Notes PwC's AcademyZainab SyedaNo ratings yet

- Introduction To Price Action TradingDocument19 pagesIntroduction To Price Action TradingGio GameloNo ratings yet