Download as pdf or txt

You might also like

- Ife and Efe Matrix SMDocument4 pagesIfe and Efe Matrix SMAli Laeeq100% (2)

- The McGraw-Hill 36-Hour Course: Finance for Non-Financial Managers 3/EFrom EverandThe McGraw-Hill 36-Hour Course: Finance for Non-Financial Managers 3/ERating: 4.5 out of 5 stars4.5/5 (6)

- Chapter 8Document14 pagesChapter 8Kanton FernandezNo ratings yet

- Quizzes - Chapter 2 - Statement of Comprehensive IncomeDocument6 pagesQuizzes - Chapter 2 - Statement of Comprehensive IncomeAmie Jane Miranda100% (3)

- National College of Business and Arts: Fairview, Quezon CityDocument4 pagesNational College of Business and Arts: Fairview, Quezon CityLouise MchaleNo ratings yet

- Capslet: Capsulized Self - Learning Empowerment ToolkitDocument15 pagesCapslet: Capsulized Self - Learning Empowerment Toolkitun knownNo ratings yet

- Capslet: Capsulized Self - Learning Empowerment ToolkitDocument15 pagesCapslet: Capsulized Self - Learning Empowerment Toolkitun knownNo ratings yet

- Statement of Comprehensive IncomeDocument23 pagesStatement of Comprehensive IncomeMarie FeNo ratings yet

- May-6 - Louise Peralta - 11 - FairnessDocument5 pagesMay-6 - Louise Peralta - 11 - FairnessLouise Joseph PeraltaNo ratings yet

- Activity Group 2Document17 pagesActivity Group 2Shann 2No ratings yet

- Fabm3 M3Document23 pagesFabm3 M3Jolina GabaynoNo ratings yet

- Job Order Costing 16112021 123409pmDocument8 pagesJob Order Costing 16112021 123409pmHassan AliNo ratings yet

- Cost Accounting and Control 3Document3 pagesCost Accounting and Control 3Davis MonNo ratings yet

- Financial Requirements Solutions Financial AccountingDocument7 pagesFinancial Requirements Solutions Financial AccountingRochelle DizonNo ratings yet

- FABM 2 3.ACT SCIdocxDocument10 pagesFABM 2 3.ACT SCIdocxMaryPher CadioganNo ratings yet

- LEARNING KIT Accounting2 Week 3Document4 pagesLEARNING KIT Accounting2 Week 3Asahi HamadaNo ratings yet

- Solved Problems: OlutionDocument9 pagesSolved Problems: OlutionSweta PandeyNo ratings yet

- Solved Prblem of Budget PDFDocument9 pagesSolved Prblem of Budget PDFSweta PandeyNo ratings yet

- Asdos Pert 2Document2 pagesAsdos Pert 2mutiaoooNo ratings yet

- Bit - Financial StatementsDocument10 pagesBit - Financial StatementsAldrin ZolinaNo ratings yet

- 4) Nov 2006 Cost ManagementDocument30 pages4) Nov 2006 Cost Managementshyammy foruNo ratings yet

- Module 4business MathDocument9 pagesModule 4business MathJohniel MartinNo ratings yet

- Statement of Comprehensive Income (SCI)Document7 pagesStatement of Comprehensive Income (SCI)Pedana RañolaNo ratings yet

- Cost-Volume Profit AnalysisDocument3 pagesCost-Volume Profit AnalysisWycliffe Luther RosalesNo ratings yet

- 2 Chapter 1 Statement of Comprehensive Income SCIDocument23 pages2 Chapter 1 Statement of Comprehensive Income SCImorbojennenNo ratings yet

- Statement of Comprehensive Income (SCI)Document10 pagesStatement of Comprehensive Income (SCI)Beverly EroyNo ratings yet

- Capital Budgeting Sample ProblemsDocument10 pagesCapital Budgeting Sample ProblemsMark Gelo WinchesterNo ratings yet

- Financial Planning IllustrationDocument4 pagesFinancial Planning IllustrationJohn Sean CapsaNo ratings yet

- Sample Functional Form of Statement of Comprehensive IncomeDocument2 pagesSample Functional Form of Statement of Comprehensive IncomeHazel Joy DemaganteNo ratings yet

- May-6 - Louise Peralta - 11 - FairnessDocument5 pagesMay-6 - Louise Peralta - 11 - FairnessLouise Joseph Peralta0% (1)

- Projected Financial Statement: Slash CompanyDocument7 pagesProjected Financial Statement: Slash CompanyKevin T. OnaroNo ratings yet

- Chapter 4 Answer Cost AccountingDocument19 pagesChapter 4 Answer Cost AccountingJuline Ashley A CarballoNo ratings yet

- 1.0 CVP AnalysisDocument52 pages1.0 CVP AnalysisAshutosh DayalNo ratings yet

- CA Inter Costing QFP Solutions Ebook - CA Ganesh BharadwajDocument103 pagesCA Inter Costing QFP Solutions Ebook - CA Ganesh Bharadwajsubasha1a1No ratings yet

- Fundamentals of Accountancy, Business and Management 2: Statement of Comprehensive IncomeDocument9 pagesFundamentals of Accountancy, Business and Management 2: Statement of Comprehensive IncomeBea allyssa CanapiNo ratings yet

- 202-0101-001 - ARIF HOSEN - Management Accounting Assignment 1Document11 pages202-0101-001 - ARIF HOSEN - Management Accounting Assignment 1Sayhan Hosen Arif100% (1)

- Installment Sales Consignment Sales Construction ContractsDocument4 pagesInstallment Sales Consignment Sales Construction ContractsShaene GalloraNo ratings yet

- DocumentDocument3 pagesDocumentPhantom LancerNo ratings yet

- Discussion Question 2Document6 pagesDiscussion Question 2Sadhna MaharjanNo ratings yet

- 4 Chapter 7-Cost Volume-Profit Relationship and Break-Even AnalysisDocument2 pages4 Chapter 7-Cost Volume-Profit Relationship and Break-Even AnalysisShenedy Lauresta QuizanaNo ratings yet

- Acctg.7 Chapter 12 CVP R Exercises 910Document5 pagesAcctg.7 Chapter 12 CVP R Exercises 910freaann03No ratings yet

- 1G CVP ANALYSIS EXCEL SCDocument49 pages1G CVP ANALYSIS EXCEL SCAlmirah H. AliNo ratings yet

- Amoroso - Inventory MethodDocument6 pagesAmoroso - Inventory MethodRovey JNo ratings yet

- Oroya Corporation - Oroya SegregationDocument8 pagesOroya Corporation - Oroya SegregationJULLIE CARMELLE H. CHATTONo ratings yet

- ManAc Midterms Chuckie ChukieDocument2 pagesManAc Midterms Chuckie ChukieVAUGHN MARTINEZNo ratings yet

- Name: Jhunard C. Bamuya Abm-12-B Activity 1. Solve For The Elements of Comprehensive Income For The FollowingDocument2 pagesName: Jhunard C. Bamuya Abm-12-B Activity 1. Solve For The Elements of Comprehensive Income For The FollowingIrish C. BamuyaNo ratings yet

- Information For Decision MakingDocument33 pagesInformation For Decision Makingwambualucas74No ratings yet

- Exercise 1: Solution: Dewitt's Budgeted Operating Income StatementDocument6 pagesExercise 1: Solution: Dewitt's Budgeted Operating Income StatementShawn MendezNo ratings yet

- Jose Rizal Memorial State University Main Campus, Dapitan City College of Business and AccountancyDocument6 pagesJose Rizal Memorial State University Main Campus, Dapitan City College of Business and AccountancyBernadette CaduyacNo ratings yet

- Fundamentals in Accountancy and Business Management Ii: Specialized Subject: (GRADE 12 First Semester)Document11 pagesFundamentals in Accountancy and Business Management Ii: Specialized Subject: (GRADE 12 First Semester)MarielLee Ramos VillarealNo ratings yet

- 1chapter 7-Cost Volume-Profit Relationship and Break-Even AnalysisDocument4 pages1chapter 7-Cost Volume-Profit Relationship and Break-Even AnalysisShenedy Lauresta QuizanaNo ratings yet

- P4 Costing Solutions To QFPDocument96 pagesP4 Costing Solutions To QFPparithinilavan07No ratings yet

- Mas 3 CVP TBPDocument6 pagesMas 3 CVP TBPKenneth Christian WilburNo ratings yet

- Problem ADocument5 pagesProblem AKim TaehyungNo ratings yet

- Tempt Tea Income StatementDocument1 pageTempt Tea Income StatementPrincess Adrianne LorenzoNo ratings yet

- Fabm2 Learning-Activity-2Document5 pagesFabm2 Learning-Activity-2Cha Eun WooNo ratings yet

- 7Document8 pages7Indu DahalNo ratings yet

- Exercise in SCIDocument2 pagesExercise in SCIRizty CabibilNo ratings yet

- Financial Planning and Pro Forma Statements Simplistic Approach Part 2Document17 pagesFinancial Planning and Pro Forma Statements Simplistic Approach Part 2ishaNo ratings yet

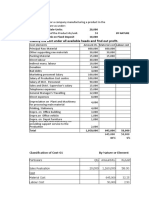

- Classify The Cost Under All Available Heads and Find Out ProfitDocument37 pagesClassify The Cost Under All Available Heads and Find Out ProfitKaustuv RathNo ratings yet

- Accounting Project Segment 4Document3 pagesAccounting Project Segment 4Zach James LebreiroNo ratings yet

- Inventory Valuation MethodsDocument10 pagesInventory Valuation Methodssalwa khan100% (5)

- Mzalendo Trust Analysis of The Finance Bill 2023 CQMBHGNDocument16 pagesMzalendo Trust Analysis of The Finance Bill 2023 CQMBHGNRaoNo ratings yet

- Project Report On Operations Management (Case Study Analysis)Document7 pagesProject Report On Operations Management (Case Study Analysis)Hiren PatelNo ratings yet

- Annual Report 2020 - PT MDS TBKDocument306 pagesAnnual Report 2020 - PT MDS TBKyanuar buanaNo ratings yet

- Accounting In Business (Service company) Tổng Quan Về Nguyên Lý Kế Toán Trong Dn Dịch VụDocument45 pagesAccounting In Business (Service company) Tổng Quan Về Nguyên Lý Kế Toán Trong Dn Dịch VụHiep Nguyen TuanNo ratings yet

- Revisiting Kenneth Brown's "10-Point Test"Document6 pagesRevisiting Kenneth Brown's "10-Point Test"DEDY KURNIAWANNo ratings yet

- Financial StatementDocument105 pagesFinancial StatementAnkitha KavyaNo ratings yet

- Revised DASAP Application For MicrograntDocument4 pagesRevised DASAP Application For Micrograntabrshseven8No ratings yet

- Virginia Tech Response On Meals and Lodging TaxesDocument80 pagesVirginia Tech Response On Meals and Lodging Taxeschristian_trejbalNo ratings yet

- CHAP 12 MCQ Theories PDFDocument3 pagesCHAP 12 MCQ Theories PDFKim LeeNo ratings yet

- CSPDCL ReportDocument106 pagesCSPDCL ReporthavejsnjNo ratings yet

- Again AllJEnts PDFDocument6 pagesAgain AllJEnts PDFBethuel KamauNo ratings yet

- Top 52 Financial Analyst Interview Questions and AnswersDocument24 pagesTop 52 Financial Analyst Interview Questions and AnswersJerry TurtleNo ratings yet

- SW Fortune 20 RankingsDocument22 pagesSW Fortune 20 RankingsInyene EkrikpoNo ratings yet

- Performance Analysis of Top 5 Banks in India HDFC Sbi Icici Axis Idbi by SatishpgoyalDocument73 pagesPerformance Analysis of Top 5 Banks in India HDFC Sbi Icici Axis Idbi by SatishpgoyalNaveen Kumar GuptaNo ratings yet

- ACCO 20063 Homework 4 Review of Accounting CycleDocument3 pagesACCO 20063 Homework 4 Review of Accounting CycleVincent Luigil Alcera100% (1)

- Profile On The Production of Disk Brake Pads & LiningsDocument24 pagesProfile On The Production of Disk Brake Pads & LiningsSBT ISBNo ratings yet

- Report On Dell CompanyDocument43 pagesReport On Dell CompanyImtiaz Ali95% (21)

- Merchandising Organized As A Partnership BusinessDocument23 pagesMerchandising Organized As A Partnership BusinessIzza WrapNo ratings yet

- CPD Budget Analysis FY2022Document116 pagesCPD Budget Analysis FY2022Sifat ShahreenNo ratings yet

- Accounting Olevel Theory NotesDocument7 pagesAccounting Olevel Theory NotesMujahid AmanNo ratings yet

- Practice Midterm1 - ADMS 1500Document13 pagesPractice Midterm1 - ADMS 1500Anita SharmaNo ratings yet

- Pas 14 Segment ReportingDocument3 pagesPas 14 Segment ReportingrandyNo ratings yet

- The Case Examines The Marketing Strategy of Samsung in IndiaDocument6 pagesThe Case Examines The Marketing Strategy of Samsung in IndiaSubhankar DasNo ratings yet

- Suggested - Answer - CAP - II - June - 2011 4Document64 pagesSuggested - Answer - CAP - II - June - 2011 4Dipen Adhikari100% (1)

- J&K EconomicSurvey 2013-2014 PDFDocument606 pagesJ&K EconomicSurvey 2013-2014 PDFSuhail MirNo ratings yet

- (L) Chapter 14 Financial AnalysisDocument5 pages(L) Chapter 14 Financial AnalysisCHZE CHZI CHUAH0% (1)

- WEBINAR REPORT Public Financial Management Industry Players Views Converted by AbcdpdfDocument9 pagesWEBINAR REPORT Public Financial Management Industry Players Views Converted by AbcdpdfNajib IsahakNo ratings yet

- PR 11 2016Document28 pagesPR 11 2016Ken ChiaNo ratings yet