Download as pdf or txt

You might also like

- 2640-1665054891113-Unit - 05 - SecurityDocument52 pages2640-1665054891113-Unit - 05 - SecurityHasantha Indrajith100% (2)

- Unit 6 Managing A Successful Computing Project 2021Document62 pagesUnit 6 Managing A Successful Computing Project 2021ishan maduahanka0% (2)

- AUE3761 2023 OctNov EQP Final 240120 141321Document12 pagesAUE3761 2023 OctNov EQP Final 240120 141321lebiyacNo ratings yet

- Programming Assignment - FINALDocument47 pagesProgramming Assignment - FINALSadiq Nazeer50% (2)

- BSBOPS403 - AE - Pro2of2 ModifiedDocument21 pagesBSBOPS403 - AE - Pro2of2 ModifiedParash RijalNo ratings yet

- Unit 15 Transport Network DesignDocument47 pagesUnit 15 Transport Network Designronica100% (1)

- Internal Verification of Assessment Decisions - BTEC (RQF) : Higher NationalsDocument33 pagesInternal Verification of Assessment Decisions - BTEC (RQF) : Higher NationalsU & Me100% (2)

- Docsity Fundamentals of Accounting 1 3Document5 pagesDocsity Fundamentals of Accounting 1 3Timothy Arbues ReyesNo ratings yet

- Unit 05 - Security - Holistic AssignmentDocument20 pagesUnit 05 - Security - Holistic AssignmentRangana Perera100% (1)

- ABC Assignment PDFDocument65 pagesABC Assignment PDFRaishaNo ratings yet

- MSCP SampleDocument41 pagesMSCP SampleRomali KeerthisingheNo ratings yet

- CPCCBC5003A AE SK 2of3Document42 pagesCPCCBC5003A AE SK 2of3Aiman RashidNo ratings yet

- 77-1557305671121-Unit 6 Managing A Successful Computing Research Project 2019Document14 pages77-1557305671121-Unit 6 Managing A Successful Computing Research Project 2019Kevin JeromNo ratings yet

- Col e 004653 MSCP Com079Document41 pagesCol e 004653 MSCP Com079AliNo ratings yet

- Portfolio Management Case StudyDocument12 pagesPortfolio Management Case StudyayeshajamilafridiNo ratings yet

- Relative Strength IndexDocument53 pagesRelative Strength Indexmmc171167% (3)

- Overnight-Intraday Daily Reversal in Commodities - QuantPediaDocument7 pagesOvernight-Intraday Daily Reversal in Commodities - QuantPediaJames LiuNo ratings yet

- 12 Acc c3 Prelim Exam p2 2023 QP AbDocument23 pages12 Acc c3 Prelim Exam p2 2023 QP AbPax AminiNo ratings yet

- Financial Management Exam Dec 2022Document10 pagesFinancial Management Exam Dec 2022scottNo ratings yet

- Assessment 1 Booklet DISD Semester 2 2302Document9 pagesAssessment 1 Booklet DISD Semester 2 2302laurabrown120No ratings yet

- SFM E1.1 - 6.12.21Document8 pagesSFM E1.1 - 6.12.21Phương HoàiNo ratings yet

- 2018-Proposal For Independent StudyDocument8 pages2018-Proposal For Independent StudySudan SwamyNo ratings yet

- March 2023 Audit and Assurance Paper ICAEWDocument9 pagesMarch 2023 Audit and Assurance Paper ICAEWTaminderNo ratings yet

- Confidential AC/JULY 2021/AUD679: © Hak Cipta Universiti Teknologi MARADocument171 pagesConfidential AC/JULY 2021/AUD679: © Hak Cipta Universiti Teknologi MARAAnisNo ratings yet

- December 2021 Financial Acocunting and Reporting UK GAAPDocument11 pagesDecember 2021 Financial Acocunting and Reporting UK GAAPChoo LeeNo ratings yet

- 2021 December QPDocument11 pages2021 December QPMarchella LukitoNo ratings yet

- Institutional Assessment Tool BookkeepingDocument21 pagesInstitutional Assessment Tool Bookkeepingemmanikan93No ratings yet

- University of The Commonwealth Caribbean School of Business & ManagementDocument13 pagesUniversity of The Commonwealth Caribbean School of Business & ManagementBeyonce SmithNo ratings yet

- Financial Accounting and Reporting Ifrs December 2023 ExamDocument11 pagesFinancial Accounting and Reporting Ifrs December 2023 ExamkarnanNo ratings yet

- Ictict517 Ae Pro 2of3Document19 pagesIctict517 Ae Pro 2of3Ashutosh MaharajNo ratings yet

- Ictict517 Ae Pro 1of3Document18 pagesIctict517 Ae Pro 1of3Ashutosh MaharajNo ratings yet

- S2021 Financial Management PDFDocument10 pagesS2021 Financial Management PDFscottNo ratings yet

- June 2023 Audit and Assurance Paper ICAEWDocument10 pagesJune 2023 Audit and Assurance Paper ICAEWTaminderNo ratings yet

- 1150-1619622396900-Unit-01 Programming Assignment Reworded 2021Document46 pages1150-1619622396900-Unit-01 Programming Assignment Reworded 2021Rodrick FernandoNo ratings yet

- RIIMPO320F Participant Assessment VC2017255 v1.3Document27 pagesRIIMPO320F Participant Assessment VC2017255 v1.3doylegarrett92No ratings yet

- AssignmentDocument136 pagesAssignmentMohamed SabrinNo ratings yet

- 21-4-TM1 Pts-Institutional AssessmentDocument18 pages21-4-TM1 Pts-Institutional Assessmentbob guintoNo ratings yet

- Unit 01 - Programming - 2020 - RewordedDocument16 pagesUnit 01 - Programming - 2020 - Rewordedmohammed shalmanNo ratings yet

- 788-1601897459456-Unit 05 - Security - 2020Document14 pages788-1601897459456-Unit 05 - Security - 2020Career and EducationNo ratings yet

- Assessment Brief - BY2 - OL - Unit6 - BDM - January2023 - SB - FVDocument3 pagesAssessment Brief - BY2 - OL - Unit6 - BDM - January2023 - SB - FVSamaNo ratings yet

- Assignment PDFDocument101 pagesAssignment PDFMaduranga WijesooriyaNo ratings yet

- Internship Report Format - 1Document7 pagesInternship Report Format - 1Obito UchichaNo ratings yet

- 4546-1688752552456-Unit 28 - Cloud-Computing - Assignment 2023Document13 pages4546-1688752552456-Unit 28 - Cloud-Computing - Assignment 2023sanjeevan2376No ratings yet

- 1150-1619622396900-Unit-01 Programming Assignment Reworded 2021Document33 pages1150-1619622396900-Unit-01 Programming Assignment Reworded 2021K A V I NNo ratings yet

- Assessment: Queensland International Business AcademyDocument42 pagesAssessment: Queensland International Business AcademysammyNo ratings yet

- Practical Report Primavera (Report) RQS4103 Lok Zhen Teng (Assessed)Document222 pagesPractical Report Primavera (Report) RQS4103 Lok Zhen Teng (Assessed)Tan HsientungNo ratings yet

- ProgrammingDocument44 pagesProgrammingblackrl girlNo ratings yet

- Audit and Assurance September 2023 ExamDocument11 pagesAudit and Assurance September 2023 ExamkarnanNo ratings yet

- Programming AssignmentDocument42 pagesProgramming AssignmentkaushalyasasithNo ratings yet

- 1150-1619622396900-Unit-01 Programming Assignment Reworded 2021Document36 pages1150-1619622396900-Unit-01 Programming Assignment Reworded 2021Cool MarttNo ratings yet

- Higher Nationals: Internal Verification of Assessment Decisions - BTEC (RQF)Document52 pagesHigher Nationals: Internal Verification of Assessment Decisions - BTEC (RQF)diniya.ranaNo ratings yet

- AUI3703 Exam May 2023 230525 075327Document14 pagesAUI3703 Exam May 2023 230525 075327Terrence MokoenaNo ratings yet

- Programming AssestmentDocument23 pagesProgramming AssestmentAnto VivekNo ratings yet

- Grifindo Toys DocumentDocument45 pagesGrifindo Toys DocumentC. GrinathNo ratings yet

- ICTWEB501 - Build A Dynamic WebsiteDocument9 pagesICTWEB501 - Build A Dynamic WebsiteKushal BajracharyaNo ratings yet

- BSBMGT517 Student Assessment Tasks - Hospitality 10-08-20Document68 pagesBSBMGT517 Student Assessment Tasks - Hospitality 10-08-20RameshNo ratings yet

- Material DerivativeDFSFSDFDocument5 pagesMaterial DerivativeDFSFSDFUmair AnsariNo ratings yet

- FAC 3702 - 4th November 2022 - Examination PaperDocument14 pagesFAC 3702 - 4th November 2022 - Examination Paperashleyapril1995No ratings yet

- HRMN5111Tb THTDocument5 pagesHRMN5111Tb THTOmphile MahloaneNo ratings yet

- Financial Management Exam Sept 2022Document10 pagesFinancial Management Exam Sept 2022scottNo ratings yet

- Competency-Based Accounting Education, Training, and Certification: An Implementation GuideFrom EverandCompetency-Based Accounting Education, Training, and Certification: An Implementation GuideNo ratings yet

- Buy Sell Back Annex GMRA 2011Document4 pagesBuy Sell Back Annex GMRA 2011Soala Henry AmabeokuNo ratings yet

- Windham Capital Diversified StrategiesDocument2 pagesWindham Capital Diversified StrategiesdimtharsNo ratings yet

- CH 10Document62 pagesCH 10hidaNo ratings yet

- Mutual: FundsDocument20 pagesMutual: FundsNitin GuptaNo ratings yet

- Aqualisa Quartz Simply A Better Shower Case Study Central Problem: Aqualisa Showers Launched Quartz Shower in May 2001 To Satisfy TheDocument7 pagesAqualisa Quartz Simply A Better Shower Case Study Central Problem: Aqualisa Showers Launched Quartz Shower in May 2001 To Satisfy TheCode GeekNo ratings yet

- T8 Financial Strategy III (Suggested Answers)Document3 pagesT8 Financial Strategy III (Suggested Answers)xinghe666No ratings yet

- FinMod 2022-2023 Tutorial Exercise + Answers Week 5Document36 pagesFinMod 2022-2023 Tutorial Exercise + Answers Week 5jjpasemperNo ratings yet

- Using Quickbooks Accountant 2012 For Accounting 11th Edition Glenn Owen Solutions ManualDocument26 pagesUsing Quickbooks Accountant 2012 For Accounting 11th Edition Glenn Owen Solutions ManualMaryJohnsonsmni100% (38)

- Customer Life Time Value-HeraDocument10 pagesCustomer Life Time Value-HerayokanituNo ratings yet

- DT 0101 Company Income Tax Self Assessment Return Form v1Document10 pagesDT 0101 Company Income Tax Self Assessment Return Form v1hudu iddrisuNo ratings yet

- Chapter 10Document30 pagesChapter 10Mahmoud Abu ShamlehNo ratings yet

- Computerized Accounting Notes - Unit III For StudentsDocument17 pagesComputerized Accounting Notes - Unit III For StudentsTanyaNo ratings yet

- Warren Buffet 2005Document15 pagesWarren Buffet 2005Henny ZahranyNo ratings yet

- A New Bridge in Shipping FinanceDocument15 pagesA New Bridge in Shipping FinanceBilly LeeNo ratings yet

- A Building That Was Purchased December 31Document2 pagesA Building That Was Purchased December 31muhaNo ratings yet

- Form MGT-7-31122019 - SignedDocument14 pagesForm MGT-7-31122019 - SignedNi007ckNo ratings yet

- PRE CLASS QUIZ WEEK 10 - Principles of Accounting T321PWB 1Document6 pagesPRE CLASS QUIZ WEEK 10 - Principles of Accounting T321PWB 1Khải Hưng NguyễnNo ratings yet

- 2018 Equity Valuation and Financial AnalysisDocument66 pages2018 Equity Valuation and Financial AnalysisAdi PratamaNo ratings yet

- A Study On Goldstar ShowroomsDocument26 pagesA Study On Goldstar ShowroomsNilish ShakyaNo ratings yet

- Partnership DissolutionDocument19 pagesPartnership DissolutionRujean Salar Altejar100% (1)

- GARCH Models in Python 4Document30 pagesGARCH Models in Python 4visNo ratings yet

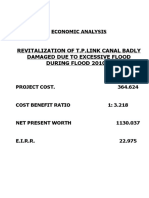

- Revitalization of T.P.Link Canal Badly Damaged Due To Excessive Flood During Flood 2010"Document4 pagesRevitalization of T.P.Link Canal Badly Damaged Due To Excessive Flood During Flood 2010"Xshf AkNo ratings yet

- International Business Finance FINS3616: By: Mishal Manzoor M.manzoor@unsw - Edu.auDocument43 pagesInternational Business Finance FINS3616: By: Mishal Manzoor M.manzoor@unsw - Edu.auKelvin ChenNo ratings yet

- Victor Fasciani (Last) Interview With Manual of IdeasDocument6 pagesVictor Fasciani (Last) Interview With Manual of IdeasVitaliyKatsenelsonNo ratings yet

- Test Bank For Corporate Finance 13th Stephen Ross Randolph Westerfield Jeffrey JaffeDocument54 pagesTest Bank For Corporate Finance 13th Stephen Ross Randolph Westerfield Jeffrey Jaffemarcuskenyatta275No ratings yet

- Making Money Trading Volatility Indices by L Mapfuti Shared by UltimateDocument134 pagesMaking Money Trading Volatility Indices by L Mapfuti Shared by Ultimateletsoalo411No ratings yet