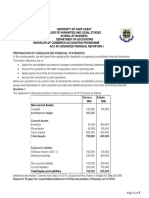

Advanced FR-Review Questions-Complex Groups

Advanced FR-Review Questions-Complex Groups

You might also like

- Financial and Managerial Accounting 15th Edition Warren Solutions ManualDocument35 pagesFinancial and Managerial Accounting 15th Edition Warren Solutions Manualjordancaldwellwjwu100% (28)

- Intermediate Accounting 1 Lecture NotesDocument16 pagesIntermediate Accounting 1 Lecture NotesAnalyn Lafradez100% (2)

- Module Assessment Answers - Group Accounts 2Document11 pagesModule Assessment Answers - Group Accounts 2John Philip L Concepcion100% (1)

- 2023 GR 11 Written Report ABDocument5 pages2023 GR 11 Written Report ABfiercestallionofficial100% (1)

- 10 FS Analysis Sample Exam Discussion KEYDocument10 pages10 FS Analysis Sample Exam Discussion KEYrav danoNo ratings yet

- Exercise Answers - Consolidated FS - Statement of Comprehensive IncomeDocument6 pagesExercise Answers - Consolidated FS - Statement of Comprehensive IncomeJohn Philip L Concepcion50% (2)

- P4-12 AnswerDocument5 pagesP4-12 AnswerPutri Apriliana100% (1)

- Consolidation Review QuestionsDocument9 pagesConsolidation Review QuestionsErnest100% (1)

- Accounting For Special Transactions Partnership AccountingDocument15 pagesAccounting For Special Transactions Partnership AccountingJessaNo ratings yet

- ACC401-Goodwill and Conso SOCIEDocument3 pagesACC401-Goodwill and Conso SOCIEOhene Asare PogastyNo ratings yet

- Advanced Accounting TemplateDocument2 pagesAdvanced Accounting TemplateAhmed MahmoudNo ratings yet

- Seatwork #2: What Is The Capital Balances of All The Partners in The New Partnership?Document4 pagesSeatwork #2: What Is The Capital Balances of All The Partners in The New Partnership?Tifanny MallariNo ratings yet

- MGMT AssignmentDocument79 pagesMGMT AssignmentLuleseged Gebre100% (1)

- AFR - Question BankDocument31 pagesAFR - Question BankDownloder UwambajimanaNo ratings yet

- Tugas Aklan TM7Document7 pagesTugas Aklan TM7AdnanNo ratings yet

- Business Combination Accounted For Under The Equity MethodDocument4 pagesBusiness Combination Accounted For Under The Equity MethodMixx MineNo ratings yet

- Practice Set P2 Transalation in Not and in Hyperinflationary Economy PDFDocument3 pagesPractice Set P2 Transalation in Not and in Hyperinflationary Economy PDFPUNK BEARNo ratings yet

- Papaya Corp. - Hyperninflation Wala Pang Solution PDFDocument3 pagesPapaya Corp. - Hyperninflation Wala Pang Solution PDFLoremar Ellen Dacumos HalogNo ratings yet

- Intercompany InventoryDocument5 pagesIntercompany InventoryMelody Domingo BangayanNo ratings yet

- 1130 - 89 - Tugas Pribadi Akl Pertemuan 9 Dan 11Document9 pages1130 - 89 - Tugas Pribadi Akl Pertemuan 9 Dan 11Maulana AmriNo ratings yet

- MC Problems Chap 2Document4 pagesMC Problems Chap 2AlexandriteNo ratings yet

- Test Bank Advance AccountingDocument16 pagesTest Bank Advance AccountingJahry Kiwalan100% (1)

- PT Ortu PT Bocah Comprehensive Income RP RPDocument8 pagesPT Ortu PT Bocah Comprehensive Income RP RPNcim PoNo ratings yet

- Adv AssignmentDocument3 pagesAdv AssignmentBromanineNo ratings yet

- Chapter Four Problem P4-8 Part B Adjusted Without VoiceDocument13 pagesChapter Four Problem P4-8 Part B Adjusted Without Voicehassan nassereddineNo ratings yet

- BSA 315 Accounting For Business CombinationDocument5 pagesBSA 315 Accounting For Business CombinationJeth MahusayNo ratings yet

- Ac208 2019 11Document6 pagesAc208 2019 11brian mgabi100% (1)

- Revision Exam Questions and Marking GuidesDocument11 pagesRevision Exam Questions and Marking GuidesAamir SaeedNo ratings yet

- Assignment 1Document5 pagesAssignment 1Loveness MphandeNo ratings yet

- BS 420 Exam QuestionsDocument17 pagesBS 420 Exam QuestionsPrince Daniels TutorNo ratings yet

- Chapter 4 AssignmentDocument2 pagesChapter 4 AssignmentJasmin MarreroNo ratings yet

- Final ExamDocument5 pagesFinal ExamSultan LimitNo ratings yet

- 1c213fc3-9b8d-4f8f-b0d2-5c9cd38b9fb3Document3 pages1c213fc3-9b8d-4f8f-b0d2-5c9cd38b9fb3mtarawneh941No ratings yet

- 2.0 ACC Test 2 Test and sug sol (2021)Document3 pages2.0 ACC Test 2 Test and sug sol (2021)molemothekaNo ratings yet

- Financial Accounting Q&aDocument4 pagesFinancial Accounting Q&aGlen JavellanaNo ratings yet

- Problem #23 Page110Document2 pagesProblem #23 Page110jelai anselmoNo ratings yet

- TGL Client DR CR Should Be DR CR Paje DR CRDocument5 pagesTGL Client DR CR Should Be DR CR Paje DR CRALICE NADINE KURNIA SURYANo ratings yet

- Assignment ACC106 8-26-20Document4 pagesAssignment ACC106 8-26-20Kristine VertucioNo ratings yet

- Change in Structure-Notes and QuestionsDocument5 pagesChange in Structure-Notes and QuestionsBilliee ButccherNo ratings yet

- Act130: Accounting For Special Transactions Prelim Exam S.Y 2020-2021Document15 pagesAct130: Accounting For Special Transactions Prelim Exam S.Y 2020-2021Nhel AlvaroNo ratings yet

- ACC401-Basic Conso-Basic QuestionsDocument5 pagesACC401-Basic Conso-Basic Questionsisaacbediako82No ratings yet

- Consolidation After Acquisition Date - Equity Analysis MethodDocument3 pagesConsolidation After Acquisition Date - Equity Analysis MethodPetrinaNo ratings yet

- Practice QUIZ 2Document8 pagesPractice QUIZ 2Cherry Jane CanonioNo ratings yet

- Firda Arfianti - LC53 - Equity Method, Two Consecutive YearsDocument5 pagesFirda Arfianti - LC53 - Equity Method, Two Consecutive YearsFirdaNo ratings yet

- Investment in Associate and Joint VentureDocument5 pagesInvestment in Associate and Joint VenturedumpyforhimNo ratings yet

- Question 7 - Financial-Reporting-Nov-2020 - Kingdom & Paradise-Question 1Document6 pagesQuestion 7 - Financial-Reporting-Nov-2020 - Kingdom & Paradise-Question 1Laud ListowellNo ratings yet

- Acct52 Buisness Combination QuizesDocument24 pagesAcct52 Buisness Combination QuizesCzarmae DumalaonNo ratings yet

- AFAR 3 - Intercompany TransactionsDocument2 pagesAFAR 3 - Intercompany TransactionsPanda ErarNo ratings yet

- Yohannes Wibowo - Akuntansi Keuangan Lanjutan I - Akuntansi (E) - Tugas Minggu 9Document10 pagesYohannes Wibowo - Akuntansi Keuangan Lanjutan I - Akuntansi (E) - Tugas Minggu 9YOHANNES WIBOWONo ratings yet

- Kunci Jawaban Vidcon Pertemuan 4 (4PAK51)Document7 pagesKunci Jawaban Vidcon Pertemuan 4 (4PAK51)Tirza LangkayNo ratings yet

- Multiple Choices - Computational Answer KeyDocument4 pagesMultiple Choices - Computational Answer KeyAleah kay BalontongNo ratings yet

- Latihan-Bahas Chapter5Document8 pagesLatihan-Bahas Chapter5Julia Pratiwi ParhusipNo ratings yet

- Preweek ReviewDocument31 pagesPreweek ReviewLeah Hope CedroNo ratings yet

- Mid Year AcqusitionDocument4 pagesMid Year AcqusitionOmolaja IbukunNo ratings yet

- BS 420 - 16TH MayDocument5 pagesBS 420 - 16TH MayPrince Daniels TutorNo ratings yet

- Acc8fsconso Sdoa2019Document5 pagesAcc8fsconso Sdoa2019Sharmaine Clemencio0No ratings yet

- Ac2091 Za - 2019Document14 pagesAc2091 Za - 2019Isra WaheedNo ratings yet

- FR 2019 Paper FinalDocument58 pagesFR 2019 Paper FinalshashalalaxiangNo ratings yet

- Advanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FDocument7 pagesAdvanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FJames CantorneNo ratings yet

- PART 1-THEORIES (1pt. Each) "A" If TRUE, "B" If FALSEDocument7 pagesPART 1-THEORIES (1pt. Each) "A" If TRUE, "B" If FALSEDrew BanlutaNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- Finding Balance 2016: Benchmarking the Performance of State-Owned Enterprise in Island CountriesFrom EverandFinding Balance 2016: Benchmarking the Performance of State-Owned Enterprise in Island CountriesNo ratings yet

- Hire Purchase Law RevisedDocument46 pagesHire Purchase Law RevisedBilliee ButccherNo ratings yet

- Lect 10Document36 pagesLect 10Billiee ButccherNo ratings yet

- Alternative Dispute ResolutionDocument89 pagesAlternative Dispute ResolutionBilliee ButccherNo ratings yet

- Business Law Assignment (Bcom Acc, B.ed Acc Mbu)Document2 pagesBusiness Law Assignment (Bcom Acc, B.ed Acc Mbu)Billiee ButccherNo ratings yet

- Basic Principles of Insurance Law New 1Document20 pagesBasic Principles of Insurance Law New 1Billiee ButccherNo ratings yet

- Company Law Lecture 3Document37 pagesCompany Law Lecture 3Billiee ButccherNo ratings yet

- Lecture 14Document57 pagesLecture 14Billiee ButccherNo ratings yet

- Lecture TwoDocument49 pagesLecture TwoBilliee ButccherNo ratings yet

- Accountables 2Document6 pagesAccountables 2Billiee ButccherNo ratings yet

- Acc201-Ias 36 SlidesDocument15 pagesAcc201-Ias 36 SlidesBilliee ButccherNo ratings yet

- Alpha Group 74Document20 pagesAlpha Group 74Billiee ButccherNo ratings yet

- AUDIT AND INTERNAL REVIEW SolutionsDocument13 pagesAUDIT AND INTERNAL REVIEW SolutionsBilliee ButccherNo ratings yet

- Copy1-FINAL WORK IIDocument76 pagesCopy1-FINAL WORK IIBilliee ButccherNo ratings yet

- FIN674 - Final - Sample 1 - QuestionsDocument8 pagesFIN674 - Final - Sample 1 - QuestionsFabricio Cifuentes EspinosaNo ratings yet

- Firefighter Matrix1Document16 pagesFirefighter Matrix1Leanne FernandesNo ratings yet

- BG 223071519 Md. Asadujjaman SaheenDocument22 pagesBG 223071519 Md. Asadujjaman SaheenMd. Asadujjaman SaheenNo ratings yet

- Interim Test 2021 10 21Document3 pagesInterim Test 2021 10 21Giulia BarthaNo ratings yet

- Tally - ERP 9 ProjectDocument106 pagesTally - ERP 9 ProjectAbhinandan PahadiNo ratings yet

- Ledger PDFDocument23 pagesLedger PDFStatusNo ratings yet

- Oppstar - Prospectus (Part 2)Document204 pagesOppstar - Prospectus (Part 2)kokueiNo ratings yet

- A Ccount 12 2059 ChaitraDocument2 pagesA Ccount 12 2059 ChaitraNayan KcNo ratings yet

- FS PHE Dec 2020 - AuditedDocument151 pagesFS PHE Dec 2020 - Auditedsultan260606No ratings yet

- Cebu Air, Inc. Parent Company FS - December 31, 2022Document125 pagesCebu Air, Inc. Parent Company FS - December 31, 2022Joelle Patricia ManaliliNo ratings yet

- ACC208 - CH 4 Prefference StockDocument19 pagesACC208 - CH 4 Prefference StockSaja AlbarjesNo ratings yet

- Kepada Yth. /: Ahmad Afdul GufronDocument7 pagesKepada Yth. /: Ahmad Afdul GufronSujinta AnnasNo ratings yet

- Chapter 2 Problem SolutionsDocument11 pagesChapter 2 Problem SolutionsLealith CañeteNo ratings yet

- Intermediate Accounting Stice 19th Edition Solutions ManualDocument8 pagesIntermediate Accounting Stice 19th Edition Solutions ManualLisa Beighley100% (34)

- CAIIB Paper 1 Module C ABM Credit Management PDF by Ambitious BabaDocument56 pagesCAIIB Paper 1 Module C ABM Credit Management PDF by Ambitious BabaAmit KanojiaNo ratings yet

- Form TP 2007120Document9 pagesForm TP 2007120Jael BernardNo ratings yet

- Assignment 8 AnswersDocument6 pagesAssignment 8 AnswersMyaNo ratings yet

- Marasigan WorksheetDocument15 pagesMarasigan WorksheetLyca MaeNo ratings yet

- Business Finance12 Q3 M2Document52 pagesBusiness Finance12 Q3 M2Chriztal TejadaNo ratings yet

- CH 1Document85 pagesCH 1EmadNo ratings yet

- Acc 201 CH 9Document7 pagesAcc 201 CH 9Trickster TwelveNo ratings yet

- Lecture 1 SlidesDocument63 pagesLecture 1 Slidesnatasha carmichaelNo ratings yet

- MACR (2nd) May2022Document3 pagesMACR (2nd) May2022Jagjit GillNo ratings yet

- Main Exam 2014-Sol-1Document7 pagesMain Exam 2014-Sol-1Diego AguirreNo ratings yet

- Mid Term QPDocument8 pagesMid Term QPawaisawais95138No ratings yet

- e-StatementBRImo 709601019320532 Nov2023 20231115 181629Document1 pagee-StatementBRImo 709601019320532 Nov2023 20231115 181629Dhika LNo ratings yet

- CASH Module Q N ADocument20 pagesCASH Module Q N AAndrea Gwen ArapocNo ratings yet

- Assignment Comparative Ratio Analysis ofDocument16 pagesAssignment Comparative Ratio Analysis ofAbhishekDey162b BBANo ratings yet

Download as pdf or txt

You might also like

- Financial and Managerial Accounting 15th Edition Warren Solutions ManualDocument35 pagesFinancial and Managerial Accounting 15th Edition Warren Solutions Manualjordancaldwellwjwu100% (28)

- Intermediate Accounting 1 Lecture NotesDocument16 pagesIntermediate Accounting 1 Lecture NotesAnalyn Lafradez100% (2)

- Module Assessment Answers - Group Accounts 2Document11 pagesModule Assessment Answers - Group Accounts 2John Philip L Concepcion100% (1)

- 2023 GR 11 Written Report ABDocument5 pages2023 GR 11 Written Report ABfiercestallionofficial100% (1)

- 10 FS Analysis Sample Exam Discussion KEYDocument10 pages10 FS Analysis Sample Exam Discussion KEYrav danoNo ratings yet

- Exercise Answers - Consolidated FS - Statement of Comprehensive IncomeDocument6 pagesExercise Answers - Consolidated FS - Statement of Comprehensive IncomeJohn Philip L Concepcion50% (2)

- P4-12 AnswerDocument5 pagesP4-12 AnswerPutri Apriliana100% (1)

- Consolidation Review QuestionsDocument9 pagesConsolidation Review QuestionsErnest100% (1)

- Accounting For Special Transactions Partnership AccountingDocument15 pagesAccounting For Special Transactions Partnership AccountingJessaNo ratings yet

- ACC401-Goodwill and Conso SOCIEDocument3 pagesACC401-Goodwill and Conso SOCIEOhene Asare PogastyNo ratings yet

- Advanced Accounting TemplateDocument2 pagesAdvanced Accounting TemplateAhmed MahmoudNo ratings yet

- Seatwork #2: What Is The Capital Balances of All The Partners in The New Partnership?Document4 pagesSeatwork #2: What Is The Capital Balances of All The Partners in The New Partnership?Tifanny MallariNo ratings yet

- MGMT AssignmentDocument79 pagesMGMT AssignmentLuleseged Gebre100% (1)

- AFR - Question BankDocument31 pagesAFR - Question BankDownloder UwambajimanaNo ratings yet

- Tugas Aklan TM7Document7 pagesTugas Aklan TM7AdnanNo ratings yet

- Business Combination Accounted For Under The Equity MethodDocument4 pagesBusiness Combination Accounted For Under The Equity MethodMixx MineNo ratings yet

- Practice Set P2 Transalation in Not and in Hyperinflationary Economy PDFDocument3 pagesPractice Set P2 Transalation in Not and in Hyperinflationary Economy PDFPUNK BEARNo ratings yet

- Papaya Corp. - Hyperninflation Wala Pang Solution PDFDocument3 pagesPapaya Corp. - Hyperninflation Wala Pang Solution PDFLoremar Ellen Dacumos HalogNo ratings yet

- Intercompany InventoryDocument5 pagesIntercompany InventoryMelody Domingo BangayanNo ratings yet

- 1130 - 89 - Tugas Pribadi Akl Pertemuan 9 Dan 11Document9 pages1130 - 89 - Tugas Pribadi Akl Pertemuan 9 Dan 11Maulana AmriNo ratings yet

- MC Problems Chap 2Document4 pagesMC Problems Chap 2AlexandriteNo ratings yet

- Test Bank Advance AccountingDocument16 pagesTest Bank Advance AccountingJahry Kiwalan100% (1)

- PT Ortu PT Bocah Comprehensive Income RP RPDocument8 pagesPT Ortu PT Bocah Comprehensive Income RP RPNcim PoNo ratings yet

- Adv AssignmentDocument3 pagesAdv AssignmentBromanineNo ratings yet

- Chapter Four Problem P4-8 Part B Adjusted Without VoiceDocument13 pagesChapter Four Problem P4-8 Part B Adjusted Without Voicehassan nassereddineNo ratings yet

- BSA 315 Accounting For Business CombinationDocument5 pagesBSA 315 Accounting For Business CombinationJeth MahusayNo ratings yet

- Ac208 2019 11Document6 pagesAc208 2019 11brian mgabi100% (1)

- Revision Exam Questions and Marking GuidesDocument11 pagesRevision Exam Questions and Marking GuidesAamir SaeedNo ratings yet

- Assignment 1Document5 pagesAssignment 1Loveness MphandeNo ratings yet

- BS 420 Exam QuestionsDocument17 pagesBS 420 Exam QuestionsPrince Daniels TutorNo ratings yet

- Chapter 4 AssignmentDocument2 pagesChapter 4 AssignmentJasmin MarreroNo ratings yet

- Final ExamDocument5 pagesFinal ExamSultan LimitNo ratings yet

- 1c213fc3-9b8d-4f8f-b0d2-5c9cd38b9fb3Document3 pages1c213fc3-9b8d-4f8f-b0d2-5c9cd38b9fb3mtarawneh941No ratings yet

- 2.0 ACC Test 2 Test and sug sol (2021)Document3 pages2.0 ACC Test 2 Test and sug sol (2021)molemothekaNo ratings yet

- Financial Accounting Q&aDocument4 pagesFinancial Accounting Q&aGlen JavellanaNo ratings yet

- Problem #23 Page110Document2 pagesProblem #23 Page110jelai anselmoNo ratings yet

- TGL Client DR CR Should Be DR CR Paje DR CRDocument5 pagesTGL Client DR CR Should Be DR CR Paje DR CRALICE NADINE KURNIA SURYANo ratings yet

- Assignment ACC106 8-26-20Document4 pagesAssignment ACC106 8-26-20Kristine VertucioNo ratings yet

- Change in Structure-Notes and QuestionsDocument5 pagesChange in Structure-Notes and QuestionsBilliee ButccherNo ratings yet

- Act130: Accounting For Special Transactions Prelim Exam S.Y 2020-2021Document15 pagesAct130: Accounting For Special Transactions Prelim Exam S.Y 2020-2021Nhel AlvaroNo ratings yet

- ACC401-Basic Conso-Basic QuestionsDocument5 pagesACC401-Basic Conso-Basic Questionsisaacbediako82No ratings yet

- Consolidation After Acquisition Date - Equity Analysis MethodDocument3 pagesConsolidation After Acquisition Date - Equity Analysis MethodPetrinaNo ratings yet

- Practice QUIZ 2Document8 pagesPractice QUIZ 2Cherry Jane CanonioNo ratings yet

- Firda Arfianti - LC53 - Equity Method, Two Consecutive YearsDocument5 pagesFirda Arfianti - LC53 - Equity Method, Two Consecutive YearsFirdaNo ratings yet

- Investment in Associate and Joint VentureDocument5 pagesInvestment in Associate and Joint VenturedumpyforhimNo ratings yet

- Question 7 - Financial-Reporting-Nov-2020 - Kingdom & Paradise-Question 1Document6 pagesQuestion 7 - Financial-Reporting-Nov-2020 - Kingdom & Paradise-Question 1Laud ListowellNo ratings yet

- Acct52 Buisness Combination QuizesDocument24 pagesAcct52 Buisness Combination QuizesCzarmae DumalaonNo ratings yet

- AFAR 3 - Intercompany TransactionsDocument2 pagesAFAR 3 - Intercompany TransactionsPanda ErarNo ratings yet

- Yohannes Wibowo - Akuntansi Keuangan Lanjutan I - Akuntansi (E) - Tugas Minggu 9Document10 pagesYohannes Wibowo - Akuntansi Keuangan Lanjutan I - Akuntansi (E) - Tugas Minggu 9YOHANNES WIBOWONo ratings yet

- Kunci Jawaban Vidcon Pertemuan 4 (4PAK51)Document7 pagesKunci Jawaban Vidcon Pertemuan 4 (4PAK51)Tirza LangkayNo ratings yet

- Multiple Choices - Computational Answer KeyDocument4 pagesMultiple Choices - Computational Answer KeyAleah kay BalontongNo ratings yet

- Latihan-Bahas Chapter5Document8 pagesLatihan-Bahas Chapter5Julia Pratiwi ParhusipNo ratings yet

- Preweek ReviewDocument31 pagesPreweek ReviewLeah Hope CedroNo ratings yet

- Mid Year AcqusitionDocument4 pagesMid Year AcqusitionOmolaja IbukunNo ratings yet

- BS 420 - 16TH MayDocument5 pagesBS 420 - 16TH MayPrince Daniels TutorNo ratings yet

- Acc8fsconso Sdoa2019Document5 pagesAcc8fsconso Sdoa2019Sharmaine Clemencio0No ratings yet

- Ac2091 Za - 2019Document14 pagesAc2091 Za - 2019Isra WaheedNo ratings yet

- FR 2019 Paper FinalDocument58 pagesFR 2019 Paper FinalshashalalaxiangNo ratings yet

- Advanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FDocument7 pagesAdvanced Accounting 2 - Chapter 4 James B. Cantorne Problem 1. T/FJames CantorneNo ratings yet

- PART 1-THEORIES (1pt. Each) "A" If TRUE, "B" If FALSEDocument7 pagesPART 1-THEORIES (1pt. Each) "A" If TRUE, "B" If FALSEDrew BanlutaNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- Finding Balance 2016: Benchmarking the Performance of State-Owned Enterprise in Island CountriesFrom EverandFinding Balance 2016: Benchmarking the Performance of State-Owned Enterprise in Island CountriesNo ratings yet

- Hire Purchase Law RevisedDocument46 pagesHire Purchase Law RevisedBilliee ButccherNo ratings yet

- Lect 10Document36 pagesLect 10Billiee ButccherNo ratings yet

- Alternative Dispute ResolutionDocument89 pagesAlternative Dispute ResolutionBilliee ButccherNo ratings yet

- Business Law Assignment (Bcom Acc, B.ed Acc Mbu)Document2 pagesBusiness Law Assignment (Bcom Acc, B.ed Acc Mbu)Billiee ButccherNo ratings yet

- Basic Principles of Insurance Law New 1Document20 pagesBasic Principles of Insurance Law New 1Billiee ButccherNo ratings yet

- Company Law Lecture 3Document37 pagesCompany Law Lecture 3Billiee ButccherNo ratings yet

- Lecture 14Document57 pagesLecture 14Billiee ButccherNo ratings yet

- Lecture TwoDocument49 pagesLecture TwoBilliee ButccherNo ratings yet

- Accountables 2Document6 pagesAccountables 2Billiee ButccherNo ratings yet

- Acc201-Ias 36 SlidesDocument15 pagesAcc201-Ias 36 SlidesBilliee ButccherNo ratings yet

- Alpha Group 74Document20 pagesAlpha Group 74Billiee ButccherNo ratings yet

- AUDIT AND INTERNAL REVIEW SolutionsDocument13 pagesAUDIT AND INTERNAL REVIEW SolutionsBilliee ButccherNo ratings yet

- Copy1-FINAL WORK IIDocument76 pagesCopy1-FINAL WORK IIBilliee ButccherNo ratings yet

- FIN674 - Final - Sample 1 - QuestionsDocument8 pagesFIN674 - Final - Sample 1 - QuestionsFabricio Cifuentes EspinosaNo ratings yet

- Firefighter Matrix1Document16 pagesFirefighter Matrix1Leanne FernandesNo ratings yet

- BG 223071519 Md. Asadujjaman SaheenDocument22 pagesBG 223071519 Md. Asadujjaman SaheenMd. Asadujjaman SaheenNo ratings yet

- Interim Test 2021 10 21Document3 pagesInterim Test 2021 10 21Giulia BarthaNo ratings yet

- Tally - ERP 9 ProjectDocument106 pagesTally - ERP 9 ProjectAbhinandan PahadiNo ratings yet

- Ledger PDFDocument23 pagesLedger PDFStatusNo ratings yet

- Oppstar - Prospectus (Part 2)Document204 pagesOppstar - Prospectus (Part 2)kokueiNo ratings yet

- A Ccount 12 2059 ChaitraDocument2 pagesA Ccount 12 2059 ChaitraNayan KcNo ratings yet

- FS PHE Dec 2020 - AuditedDocument151 pagesFS PHE Dec 2020 - Auditedsultan260606No ratings yet

- Cebu Air, Inc. Parent Company FS - December 31, 2022Document125 pagesCebu Air, Inc. Parent Company FS - December 31, 2022Joelle Patricia ManaliliNo ratings yet

- ACC208 - CH 4 Prefference StockDocument19 pagesACC208 - CH 4 Prefference StockSaja AlbarjesNo ratings yet

- Kepada Yth. /: Ahmad Afdul GufronDocument7 pagesKepada Yth. /: Ahmad Afdul GufronSujinta AnnasNo ratings yet

- Chapter 2 Problem SolutionsDocument11 pagesChapter 2 Problem SolutionsLealith CañeteNo ratings yet

- Intermediate Accounting Stice 19th Edition Solutions ManualDocument8 pagesIntermediate Accounting Stice 19th Edition Solutions ManualLisa Beighley100% (34)

- CAIIB Paper 1 Module C ABM Credit Management PDF by Ambitious BabaDocument56 pagesCAIIB Paper 1 Module C ABM Credit Management PDF by Ambitious BabaAmit KanojiaNo ratings yet

- Form TP 2007120Document9 pagesForm TP 2007120Jael BernardNo ratings yet

- Assignment 8 AnswersDocument6 pagesAssignment 8 AnswersMyaNo ratings yet

- Marasigan WorksheetDocument15 pagesMarasigan WorksheetLyca MaeNo ratings yet

- Business Finance12 Q3 M2Document52 pagesBusiness Finance12 Q3 M2Chriztal TejadaNo ratings yet

- CH 1Document85 pagesCH 1EmadNo ratings yet

- Acc 201 CH 9Document7 pagesAcc 201 CH 9Trickster TwelveNo ratings yet

- Lecture 1 SlidesDocument63 pagesLecture 1 Slidesnatasha carmichaelNo ratings yet

- MACR (2nd) May2022Document3 pagesMACR (2nd) May2022Jagjit GillNo ratings yet

- Main Exam 2014-Sol-1Document7 pagesMain Exam 2014-Sol-1Diego AguirreNo ratings yet

- Mid Term QPDocument8 pagesMid Term QPawaisawais95138No ratings yet

- e-StatementBRImo 709601019320532 Nov2023 20231115 181629Document1 pagee-StatementBRImo 709601019320532 Nov2023 20231115 181629Dhika LNo ratings yet

- CASH Module Q N ADocument20 pagesCASH Module Q N AAndrea Gwen ArapocNo ratings yet

- Assignment Comparative Ratio Analysis ofDocument16 pagesAssignment Comparative Ratio Analysis ofAbhishekDey162b BBANo ratings yet