Download as pdf or txt

You might also like

- ch03 PDFDocument42 pagesch03 PDFerylpaez100% (1)

- Lecture 4 Pharmaceutical Marketing PlanDocument35 pagesLecture 4 Pharmaceutical Marketing PlanOla Gamal50% (2)

- PACRA REPORT ON KK RICE MILLS (19-Feb-21)Document5 pagesPACRA REPORT ON KK RICE MILLS (19-Feb-21)Adeel AhmedNo ratings yet

- Ahmed Fine Weaving LTDDocument5 pagesAhmed Fine Weaving LTDHamza AsifNo ratings yet

- Reliance Weaving LTDDocument5 pagesReliance Weaving LTDhhaiderNo ratings yet

- RR 1751 11498 02-May-23Document5 pagesRR 1751 11498 02-May-23rida84377No ratings yet

- Research Report of Masood Roomi FabricDocument5 pagesResearch Report of Masood Roomi FabricWaqas AkramNo ratings yet

- RR 2394 12042 05-Sep-23Document5 pagesRR 2394 12042 05-Sep-23Muhammad Abubakar SheikhNo ratings yet

- Nishat Power - RR - 78 - 10732 - 24-Sep-22Document5 pagesNishat Power - RR - 78 - 10732 - 24-Sep-22Kristian MacariolaNo ratings yet

- RR 2269 11061 18-Jan-23Document5 pagesRR 2269 11061 18-Jan-23khurramsadiq888No ratings yet

- PACRA Rating Report SampleDocument5 pagesPACRA Rating Report Samplenithyaveda96No ratings yet

- RR 1538 11562 23-Jun-23Document6 pagesRR 1538 11562 23-Jun-23muhammadtahir425No ratings yet

- RR 28 11636 23-Jun-23Document5 pagesRR 28 11636 23-Jun-23salmababu7675No ratings yet

- Bulleh Shah Packaging (PVT.) Limited: Rating ReportDocument5 pagesBulleh Shah Packaging (PVT.) Limited: Rating Report057-Kaynat khanNo ratings yet

- RR 1645 9836 11-Feb-22Document5 pagesRR 1645 9836 11-Feb-22Ghulam MurtazaNo ratings yet

- Rating 2Document5 pagesRating 2sardar amanat aliHadian00rNo ratings yet

- Khaadi - 14 Dec 21Document5 pagesKhaadi - 14 Dec 21Anum ShamimNo ratings yet

- RR 1664 9107 1Document5 pagesRR 1664 9107 1Saifullah SaifiNo ratings yet

- AnalysisDocument5 pagesAnalysissardar amanat aliHadian00rNo ratings yet

- PACRA-K Electric-Jun-23Document5 pagesPACRA-K Electric-Jun-23saad JavaidNo ratings yet

- PACRA-United Insurance RatingDocument5 pagesPACRA-United Insurance RatingRaja HaroonNo ratings yet

- RR 1356 9614 10-Dec-21Document5 pagesRR 1356 9614 10-Dec-21aanis HaiderNo ratings yet

- LIberty Power Tech - RR - 74 - 10861 - 10-Nov-22Document5 pagesLIberty Power Tech - RR - 74 - 10861 - 10-Nov-22Kristian MacariolaNo ratings yet

- RR 2493 10921 30-Dec-22Document5 pagesRR 2493 10921 30-Dec-22Talha NafeesNo ratings yet

- LOTTE Kolson (PVT.) Limited: Rating ReportDocument5 pagesLOTTE Kolson (PVT.) Limited: Rating ReportAreeba AmirNo ratings yet

- Narowal Energy - RR - 1579 - 10334 - 22-Jun-22Document5 pagesNarowal Energy - RR - 1579 - 10334 - 22-Jun-22Kristian MacariolaNo ratings yet

- Quarterly Commodity Price Update: Global Equity ResearchDocument24 pagesQuarterly Commodity Price Update: Global Equity ResearchForexliveNo ratings yet

- InvestoreyeDocument21 pagesInvestoreyeAnkitNo ratings yet

- Pacra Report On JL Rice (2019)Document5 pagesPacra Report On JL Rice (2019)Adeel AhmedNo ratings yet

- Big Bags International PVT LTDDocument7 pagesBig Bags International PVT LTDnayabrasul208No ratings yet

- Kanchan India BL 20mar2019Document7 pagesKanchan India BL 20mar2019aaravNo ratings yet

- Apex Spinning & Knitting Mills Rating Report Surveillance 2015 PDFDocument5 pagesApex Spinning & Knitting Mills Rating Report Surveillance 2015 PDFben crabbNo ratings yet

- Khaadi Annual Report 22Document5 pagesKhaadi Annual Report 22hussainahmadkhan89No ratings yet

- Cottony FashionsDocument6 pagesCottony FashionsHarishKumar JNo ratings yet

- Bhuwalka and Sons Private LimitedDocument4 pagesBhuwalka and Sons Private LimiteddoctorsabeehNo ratings yet

- Gujarat Themis Biosyn LimitedDocument5 pagesGujarat Themis Biosyn LimitedAshwani KesharwaniNo ratings yet

- Press Release 3B Fibreglass SPRL: Facilities Amount (Rs. Crore) Rating Rating ActionDocument4 pagesPress Release 3B Fibreglass SPRL: Facilities Amount (Rs. Crore) Rating Rating ActionData CentrumNo ratings yet

- Maruti Suzuki Kizashi Marketing PlanDocument8 pagesMaruti Suzuki Kizashi Marketing Planniranjan bhagatNo ratings yet

- Welcon Chemicals (PVT.) Limited: Rating ReportDocument5 pagesWelcon Chemicals (PVT.) Limited: Rating ReportM TayyabNo ratings yet

- Prime Urban ICRA April 17Document7 pagesPrime Urban ICRA April 17BALMERNo ratings yet

- Bata India Limited: Summary of Rating ActionDocument6 pagesBata India Limited: Summary of Rating ActionDhrubajyoti DattaNo ratings yet

- Pakistan Banking Perspective2022Document65 pagesPakistan Banking Perspective2022Muhammad NadeemNo ratings yet

- Press Release RACL Geartech LTDDocument4 pagesPress Release RACL Geartech LTDSourav DuttaNo ratings yet

- Save Microfinance Private Limited: RatingsDocument4 pagesSave Microfinance Private Limited: RatingsSubhamNo ratings yet

- Super Screws Private Limited: Summary of Rated InstrumentsDocument7 pagesSuper Screws Private Limited: Summary of Rated InstrumentsAnonymous bdUhUNm7JNo ratings yet

- Rating MBHDocument5 pagesRating MBHHamzaMehmoodBhattiNo ratings yet

- RR 2392 11196 02-Feb-23Document6 pagesRR 2392 11196 02-Feb-23محمد ارسلان امتیازNo ratings yet

- Pharmagen Limited: Rating ReportDocument5 pagesPharmagen Limited: Rating ReportMuhammad Ahmed MirzaNo ratings yet

- Customer Private LimitedDocument4 pagesCustomer Private LimitedData CentrumNo ratings yet

- Rating ReportDocument5 pagesRating Reportl202095No ratings yet

- A One Steel Alloys 10may2021Document7 pagesA One Steel Alloys 10may2021L KNo ratings yet

- Ganga Rasayanie Private Limited-R-10102019Document7 pagesGanga Rasayanie Private Limited-R-10102019DarshanNo ratings yet

- Pakistan BankingPerspective 2021Document82 pagesPakistan BankingPerspective 2021jamilkhannNo ratings yet

- Shri Balaji Rollings Private LimDocument4 pagesShri Balaji Rollings Private LimData CentrumNo ratings yet

- Credit Rating Report G.P. 2 PDFDocument16 pagesCredit Rating Report G.P. 2 PDFMohammad AdnanNo ratings yet

- Maybank Sustainability Report 2023Document135 pagesMaybank Sustainability Report 2023Rahoul123No ratings yet

- PR Baidyanath 19dec22Document6 pagesPR Baidyanath 19dec22tusharj0934No ratings yet

- Luxor Writing Instruments Pvt. LTDDocument7 pagesLuxor Writing Instruments Pvt. LTDbookdekho.ytNo ratings yet

- Aavas Q4FY21 ResultsDocument16 pagesAavas Q4FY21 ResultsdarshanmaldeNo ratings yet

- Bpops Plan 2020-22Document4 pagesBpops Plan 2020-22Ronnie ManaoNo ratings yet

- Tripurashwari Agro Product Pvt. Ltd.-07-21-2020Document4 pagesTripurashwari Agro Product Pvt. Ltd.-07-21-2020Manish DadlaniNo ratings yet

- The Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiFrom EverandThe Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiNo ratings yet

- Lease 12 AprilDocument32 pagesLease 12 Aprilr4vemaster100% (1)

- 538ASM 2 FrontsheetDocument40 pages538ASM 2 FrontsheetNguyen Ngoc Long (FGW HN)No ratings yet

- Chapter 2 - Cost Concepts and Design EconomicsDocument21 pagesChapter 2 - Cost Concepts and Design EconomicsChristine ParkNo ratings yet

- 317 - Mba English MediumDocument3 pages317 - Mba English MediumBoon India TrichyNo ratings yet

- A. QB Lesson 6Document28 pagesA. QB Lesson 6Shena Mari Trixia Gepana100% (1)

- Group 2 ADocument29 pagesGroup 2 Ax9pv446dhjNo ratings yet

- Channel Trading StrategyDocument51 pagesChannel Trading StrategyVijay86% (7)

- The Influence of Digital MarkeDocument9 pagesThe Influence of Digital MarkeOurpanNo ratings yet

- Internal Routine Reporting and Decisions Internal Non-Routine Reporting and Decisions External ReportingDocument22 pagesInternal Routine Reporting and Decisions Internal Non-Routine Reporting and Decisions External ReportingBarbie GarzaNo ratings yet

- PR-2331-Vinamilk- Nguyễn Trần Thiên PhúcDocument6 pagesPR-2331-Vinamilk- Nguyễn Trần Thiên Phúcphuc.ntt06260No ratings yet

- Michael Mcmillin ResumeDocument1 pageMichael Mcmillin Resumeapi-379802175No ratings yet

- Ch-1 PPT Principles of MKTDocument22 pagesCh-1 PPT Principles of MKTBamlak WenduNo ratings yet

- CPA 4 Affiliate - PremiumDocument78 pagesCPA 4 Affiliate - Premiumjonattan rodriguesNo ratings yet

- IFRS-Deferred Tax Balance Sheet ApproachDocument8 pagesIFRS-Deferred Tax Balance Sheet ApproachJitendra JawalekarNo ratings yet

- Chapter 6 Supply Network DesignDocument22 pagesChapter 6 Supply Network DesignErick Quan LunaNo ratings yet

- Harshit HR1Document1 pageHarshit HR1Harshit AgarwalNo ratings yet

- 2018 FSF Scholarship Case Study - MerchandisingAndMarketing - SubmissionDocument16 pages2018 FSF Scholarship Case Study - MerchandisingAndMarketing - SubmissionZoia KozakovNo ratings yet

- Eco BCK Q MTP CAF Mar 2021Document16 pagesEco BCK Q MTP CAF Mar 2021JainulNo ratings yet

- Managerial AccountingDocument38 pagesManagerial AccountingLEA100% (1)

- Adjustments and The Ten-Column Work Sheet: What You'll LearnDocument34 pagesAdjustments and The Ten-Column Work Sheet: What You'll LearnJhazz Landagan100% (1)

- ECON2103 Midterm 2 Fall2021+ (For+practice) +cindyDocument14 pagesECON2103 Midterm 2 Fall2021+ (For+practice) +cindyjocelyn.hy.chenNo ratings yet

- Answer 11Document10 pagesAnswer 11kamallNo ratings yet

- Our Lady of Fatima University For Accounting For Sole Proprietorship For BS Accountancy DiscussionDocument8 pagesOur Lady of Fatima University For Accounting For Sole Proprietorship For BS Accountancy DiscussionJANNA RAZONNo ratings yet

- An20231002 1430Document4 pagesAn20231002 1430Jozel DogelioNo ratings yet

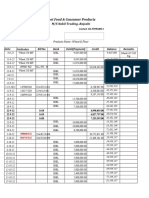

- Nabil TradingDocument5 pagesNabil TradingRoot Food and Consumer ProductsNo ratings yet

- (Secured Transactions) Act, 2016.Document2 pages(Secured Transactions) Act, 2016.mohammad faraz aliNo ratings yet

- Raj Singh Fazilka 24.06.2023Document7 pagesRaj Singh Fazilka 24.06.2023rohit. remooNo ratings yet

- 2021 Answer Chapter 5Document15 pages2021 Answer Chapter 5prettyjessyNo ratings yet