Download as docx, pdf, or txt

You might also like

- Life Insurance NotesDocument38 pagesLife Insurance Notesshahidjappa67% (3)

- INSURANCEDocument28 pagesINSURANCEcharuNo ratings yet

- Banking and InsuranceDocument20 pagesBanking and Insurancebeena antuNo ratings yet

- RISK Chapter 5Document19 pagesRISK Chapter 5Taresa AdugnaNo ratings yet

- Chapter - 1 Life & Health InsuranceDocument38 pagesChapter - 1 Life & Health InsurancehelloNo ratings yet

- Term Life Insurance PolicyDocument4 pagesTerm Life Insurance PolicyShubham NamdevNo ratings yet

- Knowledge Center GlossaryDocument3 pagesKnowledge Center Glossarychezzter25No ratings yet

- Categories of InsuranceDocument6 pagesCategories of InsurancewilliamyesNo ratings yet

- Importance or Advantages of Insurance To SocietyDocument11 pagesImportance or Advantages of Insurance To SocietyPooja TripathiNo ratings yet

- Origin of The Company: Meaning and Definition Nature and Scope Importance of Insurance Objectives of The StudyDocument32 pagesOrigin of The Company: Meaning and Definition Nature and Scope Importance of Insurance Objectives of The Studypav_deshpande8055No ratings yet

- Whole Life InsuranceDocument16 pagesWhole Life Insuranceemilda_samuel211No ratings yet

- 04 Insurance CompanyDocument38 pages04 Insurance CompanyAnuska JayswalNo ratings yet

- Life Health and Disability 1Document47 pagesLife Health and Disability 1Muhammad ArshadNo ratings yet

- Chapter 2 InsuranceDocument31 pagesChapter 2 InsurancegirishNo ratings yet

- Assignment RiskDocument6 pagesAssignment Riskdejen mengstieNo ratings yet

- Elements of Good Life Insurance PolicyDocument4 pagesElements of Good Life Insurance PolicySaumya JaiswalNo ratings yet

- Insurance & Risk Management JUNE 2022Document11 pagesInsurance & Risk Management JUNE 2022Rajni KumariNo ratings yet

- What Is Life InsuranceDocument5 pagesWhat Is Life InsuranceTeja AndeNo ratings yet

- Basic Information About LIC PoliciesDocument6 pagesBasic Information About LIC PoliciesskumarshopperNo ratings yet

- Company Profile BirlaDocument31 pagesCompany Profile BirlaShivayu VaidNo ratings yet

- Guarantee and OptionsDocument1 pageGuarantee and OptionsRashi JainNo ratings yet

- Chap 5Document18 pagesChap 5yhikmet613No ratings yet

- Life InsuranceDocument13 pagesLife Insurancesmiley12345678910No ratings yet

- RISK Assignment 2Document4 pagesRISK Assignment 2Firaol GeremuNo ratings yet

- 8 (22) (Read-Only)Document54 pages8 (22) (Read-Only)Kookie ShresthaNo ratings yet

- INSURANCE LAW - ImpromptuDocument7 pagesINSURANCE LAW - ImpromptuDiya MirajNo ratings yet

- Introduction To Insurance IndustriesDocument37 pagesIntroduction To Insurance IndustriesNishaTambeNo ratings yet

- Term Paper of BankingDocument22 pagesTerm Paper of BankingnidhijunejaNo ratings yet

- Irda - Hand Book On Life InsuranceDocument12 pagesIrda - Hand Book On Life InsuranceRajesh SinghNo ratings yet

- Life Insurance Is A Contract Between The Policy Owner andDocument23 pagesLife Insurance Is A Contract Between The Policy Owner andshankarinadar100% (1)

- Final ScriptDocument42 pagesFinal ScriptAkhilesh desaiNo ratings yet

- Life Insurance HandbookDocument12 pagesLife Insurance HandbookChi MnuNo ratings yet

- A Project Report On Child Health Plans NEW EDITEDDocument50 pagesA Project Report On Child Health Plans NEW EDITEDShubham MatkarNo ratings yet

- Fim 3Document27 pagesFim 3akshat srivastavaNo ratings yet

- Life InsuranceDocument3 pagesLife Insuranceshailen2uNo ratings yet

- Critical Years in The Programming of Life Insurance MeansDocument8 pagesCritical Years in The Programming of Life Insurance MeansRomz Ninz HernandezNo ratings yet

- Life Insuranc (Sem - LLL)Document20 pagesLife Insuranc (Sem - LLL)Milton Rosario MoraesNo ratings yet

- Handbook On Life InsuranceDocument17 pagesHandbook On Life InsuranceDeeptiNo ratings yet

- 4th Sem TheoryDocument18 pages4th Sem TheoryBISLY MARIAM BINSONNo ratings yet

- Insurance ....Document8 pagesInsurance ....SanyaNo ratings yet

- A Interim Report 1Document28 pagesA Interim Report 1Mayank MahajanNo ratings yet

- Fabozzi FoFMI4 CH06Document15 pagesFabozzi FoFMI4 CH06Jion DiazNo ratings yet

- Ch-5 Edited EndDocument40 pagesCh-5 Edited EndAbatneh mengistNo ratings yet

- Unit - 2 Fundamentals of InsuranceDocument21 pagesUnit - 2 Fundamentals of Insurancepoojaaradhya9677No ratings yet

- Jagendra Kumar RenewedDocument7 pagesJagendra Kumar RenewedbcibaneNo ratings yet

- Executive SummaryDocument25 pagesExecutive SummaryRitika MahenNo ratings yet

- Q1. What Is InsuranceDocument5 pagesQ1. What Is InsuranceDebasis NayakNo ratings yet

- Insurance Glossary: AccidentDocument7 pagesInsurance Glossary: AccidentVipul DesaiNo ratings yet

- Life Insurance ProjectDocument11 pagesLife Insurance ProjectDarshana MathurNo ratings yet

- Life Insurance Kotak Mahindra Group Old MutualDocument16 pagesLife Insurance Kotak Mahindra Group Old MutualKanchan khedaskerNo ratings yet

- Life Insurance FAQsDocument3 pagesLife Insurance FAQsEdappon100% (2)

- Life Insurance Products & Terms PDFDocument16 pagesLife Insurance Products & Terms PDFSuman SinhaNo ratings yet

- InsuranceDocument7 pagesInsuranceVairag JainNo ratings yet

- Insurance & Risk ManagementDocument8 pagesInsurance & Risk ManagementJASONM22No ratings yet

- Stages in Policy IssuanceDocument9 pagesStages in Policy IssuanceNeha AmitNo ratings yet

- Textbook of Urgent Care Management: Chapter 9, Insurance Requirements for the Urgent Care CenterFrom EverandTextbook of Urgent Care Management: Chapter 9, Insurance Requirements for the Urgent Care CenterNo ratings yet

- Health InsuranceDocument29 pagesHealth Insuranceckchetankhatri967No ratings yet

- Insurance Management CompleteDocument63 pagesInsurance Management Completeckchetankhatri967No ratings yet

- Basic Join Example - V2Document2 pagesBasic Join Example - V2ckchetankhatri967No ratings yet

- Age and HeightDocument5 pagesAge and Heightckchetankhatri967No ratings yet

- Project+Management+Fundamentals 2023.07.03Document22 pagesProject+Management+Fundamentals 2023.07.03ckchetankhatri967No ratings yet

- Barangay Minanga: Republic of The Philippines Province of Cagayan Municipality of CamalaniuganDocument2 pagesBarangay Minanga: Republic of The Philippines Province of Cagayan Municipality of CamalaniuganMelody Frac ZapateroNo ratings yet

- Cataquez & Jore Progress Report 01272023Document25 pagesCataquez & Jore Progress Report 01272023Gwyneth Fiona CataquezNo ratings yet

- Corpo OutlineDocument4 pagesCorpo OutlinesuperdaredenNo ratings yet

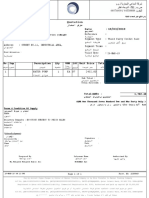

- Quotation Date: Doc No : No. Qty Unit Price Total Price Amount QAR Sup LOC Description UOMDocument1 pageQuotation Date: Doc No : No. Qty Unit Price Total Price Amount QAR Sup LOC Description UOMMechanical EnggNo ratings yet

- Engineering Economy Lecture Notes 1Document4 pagesEngineering Economy Lecture Notes 1warlockeNo ratings yet

- Higher Education Strategy CenterDocument88 pagesHigher Education Strategy CentergetachewNo ratings yet

- Accounting ExercisesDocument6 pagesAccounting ExercisesLiu PNo ratings yet

- General Announcements: December 2015Document11 pagesGeneral Announcements: December 2015ArgyriosNo ratings yet

- Planning Final ReportDocument30 pagesPlanning Final ReportAndyMaviaNo ratings yet

- The Role of Corporate Boards IN THE 1990s: February 29, 1992 Beaver Creek, ColoradoDocument21 pagesThe Role of Corporate Boards IN THE 1990s: February 29, 1992 Beaver Creek, ColoradoMuhammad RandyNo ratings yet

- Considerations For Entrepreneurs Entering The Recreational Marijuana IndustryDocument15 pagesConsiderations For Entrepreneurs Entering The Recreational Marijuana IndustryRay RodriguezNo ratings yet

- Differential Analysis and Product Pricing: Principles of Managerial AccountingDocument90 pagesDifferential Analysis and Product Pricing: Principles of Managerial AccountingLucy UnNo ratings yet

- Market Structure in BangladeshDocument15 pagesMarket Structure in BangladeshTalukder Riman80% (5)

- HuskyDocument10 pagesHuskypreetimurali100% (1)

- Chapter 6 Theory and Estimation of Production Function MCQs1Document8 pagesChapter 6 Theory and Estimation of Production Function MCQs1Muhammad Ahmed100% (1)

- 2 Effective and Nominal RateDocument19 pages2 Effective and Nominal RateKelvin BarceLonNo ratings yet

- Morningstar Economic Moats II - ExcellentDocument42 pagesMorningstar Economic Moats II - Excellentee1993100% (1)

- GHR M: A Case Study ON Hutchinson Essar India Acquisition BY VodafoneDocument10 pagesGHR M: A Case Study ON Hutchinson Essar India Acquisition BY VodafoneGaurav_Saha_9826No ratings yet

- Fundamental of Taxation and Auditing (Mgt.218) - BBS Third Year - 4 Years Program - Model Question - With SOLUTIONDocument21 pagesFundamental of Taxation and Auditing (Mgt.218) - BBS Third Year - 4 Years Program - Model Question - With SOLUTIONRiyaz RangrezNo ratings yet

- Sources of Finance - CreditDocument12 pagesSources of Finance - CreditSanta PinkaNo ratings yet

- Case Study On Tushar EnterprisesDocument15 pagesCase Study On Tushar EnterprisesVivek RajNo ratings yet

- Security of Energy Supply in Europe PDFDocument328 pagesSecurity of Energy Supply in Europe PDFCybercratNo ratings yet

- Islamic vs. Conventional BankingDocument32 pagesIslamic vs. Conventional BankingNuwan Tharanga LiyanageNo ratings yet

- Misrad Haklita Bituach Leumi BookletDocument58 pagesMisrad Haklita Bituach Leumi BookletEnglishAccessibilityNo ratings yet

- Dwnload Full Macroeconomics Canadian 5th Edition Williamson Test Bank PDFDocument30 pagesDwnload Full Macroeconomics Canadian 5th Edition Williamson Test Bank PDFmichelettigeorgianna100% (9)

- Marketing AuditDocument7 pagesMarketing AudithrsrinivasNo ratings yet

- This Study Resource Was: Amanda Hardesty, 801069183, HCA 342 Chapter 11 Discussion QuestionsDocument3 pagesThis Study Resource Was: Amanda Hardesty, 801069183, HCA 342 Chapter 11 Discussion QuestionsHugsNo ratings yet

- D2 Case Study V CDL Creating Value Through Sustainability PDFDocument9 pagesD2 Case Study V CDL Creating Value Through Sustainability PDFfredz.acctNo ratings yet

- Mba Elective Strategic Sourcing Syllabus 2019Document8 pagesMba Elective Strategic Sourcing Syllabus 2019Dhanabal WiskillNo ratings yet

- Tda ProfileDocument8 pagesTda ProfileZubair MohammedNo ratings yet