Download as docx, pdf, or txt

You might also like

- Buckwold 20ce sm04Document68 pagesBuckwold 20ce sm04Kailash Kumar100% (1)

- Case 1-Cat and Joe Pig RigDocument7 pagesCase 1-Cat and Joe Pig RigEj MacadatuNo ratings yet

- The Essential Tax Guide - 2023 EditionDocument116 pagesThe Essential Tax Guide - 2023 Editionธนวัฒน์ ปิยะวิสุทธิกุล100% (3)

- Investment in Associates - IntercompanyDocument13 pagesInvestment in Associates - IntercompanyAmé MoutonNo ratings yet

- Chapter 2 AssignmentDocument8 pagesChapter 2 AssignmentRoss John JimenezNo ratings yet

- Week 3 Course Material For Income TaxationDocument11 pagesWeek 3 Course Material For Income TaxationAshly MateoNo ratings yet

- Individual Illustration and Activity No. 2Document19 pagesIndividual Illustration and Activity No. 2김유나100% (1)

- Liquidity RatiosDocument3 pagesLiquidity RatiosMckenzie PalaganasNo ratings yet

- CHAPTER 3 - Notes To Financial StatementDocument32 pagesCHAPTER 3 - Notes To Financial StatementShane Aberie Villaroza AmidaNo ratings yet

- Chapter 6 - Income Tax For PartnershipDocument40 pagesChapter 6 - Income Tax For PartnershipNineteen Aùgùst100% (1)

- Ia 2Document23 pagesIa 2Gelo OwssNo ratings yet

- Capital BudgetingDocument67 pagesCapital BudgetingRosanna RosalesNo ratings yet

- PRELIM Chapter 9 10 11Document37 pagesPRELIM Chapter 9 10 11Bisag AsaNo ratings yet

- ANSWER: X 2.544: PORTFOLIO BETA: Suppose You Are A Manager of A Mutual Fund and Hold A $10Document1 pageANSWER: X 2.544: PORTFOLIO BETA: Suppose You Are A Manager of A Mutual Fund and Hold A $10MiconNo ratings yet

- Chapter 1 ReviewerDocument16 pagesChapter 1 Revieweranon_879788236No ratings yet

- Evaluating Firm Performance - ReportDocument5 pagesEvaluating Firm Performance - ReportJeane Mae BooNo ratings yet

- Audit Cendant CorpDocument23 pagesAudit Cendant CorpAjeng Feby PalupiNo ratings yet

- Obligations and Contracts - Domingo AnswersDocument2 pagesObligations and Contracts - Domingo AnswersKristan EstebanNo ratings yet

- Pas 28Document6 pagesPas 28AnneNo ratings yet

- ACCO 20063 - Conceptual Framework and Accounting StandardsDocument21 pagesACCO 20063 - Conceptual Framework and Accounting StandardsSarmiento Rona A.No ratings yet

- Shareholders' Equity - Contributed Capital: Part A: The Nature of Shareholders' Equity I. Sources of Shareholders' EquityDocument12 pagesShareholders' Equity - Contributed Capital: Part A: The Nature of Shareholders' Equity I. Sources of Shareholders' Equitycriszel4sobejanaNo ratings yet

- Valix Financial Accounting Vol 3 AnswersDocument1 pageValix Financial Accounting Vol 3 AnswersJobby JaranillaNo ratings yet

- Chapter 1 None CompressDocument9 pagesChapter 1 None CompressiadcNo ratings yet

- Accounting Chapter 9Document7 pagesAccounting Chapter 9Angelica Faye DuroNo ratings yet

- CF Objective of Financial ReportingDocument6 pagesCF Objective of Financial Reportingpanda 1No ratings yet

- Financial Management Principles and Applications Cabrera Solution ManualDocument4 pagesFinancial Management Principles and Applications Cabrera Solution ManualArly Kurt TorresNo ratings yet

- Finalchapter 24Document10 pagesFinalchapter 24Jud Rossette ArcebesNo ratings yet

- CPA Review School of The Philippines Manila First Pre-Board Solutions TaxationDocument8 pagesCPA Review School of The Philippines Manila First Pre-Board Solutions TaxationLive LoveNo ratings yet

- Loss of The Thing DueDocument4 pagesLoss of The Thing DueAnge Buenaventura SalazarNo ratings yet

- Group 7 Inventory ManagementDocument146 pagesGroup 7 Inventory ManagementBhea Irish Joy BuenaflorNo ratings yet

- 93-04 - Partnership TaxDocument8 pages93-04 - Partnership TaxJuan Miguel UngsodNo ratings yet

- Obligations and Contracts Chapter 2Document14 pagesObligations and Contracts Chapter 2Fierryl MenisNo ratings yet

- Exercise 1Document4 pagesExercise 1Nyster Ann RebenitoNo ratings yet

- INCOMETAX M45 ReviewerDocument15 pagesINCOMETAX M45 ReviewerCaryl Isabel Francisco100% (1)

- Byproduct AccountingDocument13 pagesByproduct AccountingAbu NaserNo ratings yet

- Illustration: Formation of Partnership Valuation of Capital A BDocument2 pagesIllustration: Formation of Partnership Valuation of Capital A BArian AmuraoNo ratings yet

- Final Exam Taxation 101Document8 pagesFinal Exam Taxation 101Live LoveNo ratings yet

- P1 - ReviewDocument14 pagesP1 - ReviewEvitaAyneMaliñanaTapit0% (2)

- Extra Credit Renee AronhaltDocument12 pagesExtra Credit Renee Aronhaltapi-240550329No ratings yet

- Sales 140, 800 Less: Cost of Sales (84, 480) Gross ProfitDocument5 pagesSales 140, 800 Less: Cost of Sales (84, 480) Gross ProfitMichaela KowalskiNo ratings yet

- 2E Intermediate (Sat - 16-3-2024) - Final Ch.2 (A)Document20 pages2E Intermediate (Sat - 16-3-2024) - Final Ch.2 (A)ahmedNo ratings yet

- Postemployment BenefitsDocument3 pagesPostemployment BenefitsChristian John PardoNo ratings yet

- Taxation SituationalDocument113 pagesTaxation SituationalMartin GragasinNo ratings yet

- Cash Flow AssignmentDocument39 pagesCash Flow AssignmentMUHAMMAD HASSANNo ratings yet

- Taxation of Partnerships, Estates and Trusts Classification of Partnerships 1. General Professional PartnershipDocument11 pagesTaxation of Partnerships, Estates and Trusts Classification of Partnerships 1. General Professional PartnershipErika DioquinoNo ratings yet

- Situational and Competitor Analysis of StarbucksDocument22 pagesSituational and Competitor Analysis of StarbucksChristine AimhieNo ratings yet

- Illustration 5Document2 pagesIllustration 5Bea Nicole BaltazarNo ratings yet

- Easy Company Financial PositionDocument2 pagesEasy Company Financial PositionSheila May SantosNo ratings yet

- Warranty Liability: Start of DiscussionDocument2 pagesWarranty Liability: Start of DiscussionclarizaNo ratings yet

- Accou NT No. Account Name Trial Balance Adjustment Income Statement Debit Credit Debit Credit DebitDocument40 pagesAccou NT No. Account Name Trial Balance Adjustment Income Statement Debit Credit Debit Credit DebitJam SurdivillaNo ratings yet

- Chap 21 AnswersDocument9 pagesChap 21 AnswersJullie-Ann YbañezNo ratings yet

- 3 ACCT 2AB P. DissolutionDocument6 pages3 ACCT 2AB P. DissolutionMary Angeline LopezNo ratings yet

- Equity InvestmentsDocument43 pagesEquity InvestmentschingNo ratings yet

- 08 ELMS Review 1Document2 pages08 ELMS Review 1Cj MoontonNo ratings yet

- Partnership Dissolution - PART 1Document17 pagesPartnership Dissolution - PART 1Aby ReedNo ratings yet

- Chapter 17 Ia2 No ProblemsDocument23 pagesChapter 17 Ia2 No ProblemsJM Valonda Villena, CPA, MBANo ratings yet

- INTACC2 - Chapter 29Document4 pagesINTACC2 - Chapter 29Shane TabunggaoNo ratings yet

- Repealed PD 692 Known As Revised Accountancy LawDocument8 pagesRepealed PD 692 Known As Revised Accountancy LawLian RamirezNo ratings yet

- Basic Accounting Equation Exercises 2Document2 pagesBasic Accounting Equation Exercises 2Ace Joseph TabaderoNo ratings yet

- MS 3412 Capital BudgetingDocument6 pagesMS 3412 Capital BudgetingMonica GarciaNo ratings yet

- FDNACCT - Quiz #1 - Set B - Answer KeyDocument4 pagesFDNACCT - Quiz #1 - Set B - Answer KeyIchi HasukiNo ratings yet

- Lesson 1 - 2 Tax On The Self Employed Andor Professional 2Document4 pagesLesson 1 - 2 Tax On The Self Employed Andor Professional 2Aaron HernandezNo ratings yet

- Individuals Assign3Document7 pagesIndividuals Assign3jdNo ratings yet

- 5 Important Details - Law2Document15 pages5 Important Details - Law2Marynissa CatibogNo ratings yet

- MODULE 4 Fringe Benefits Tax and de Minimis BenefitsDocument6 pagesMODULE 4 Fringe Benefits Tax and de Minimis BenefitsMarynissa CatibogNo ratings yet

- Catibog-Activity 8-Transaction Processing and Financial ReportingDocument4 pagesCatibog-Activity 8-Transaction Processing and Financial ReportingMarynissa CatibogNo ratings yet

- Reviewer Bank To MiningDocument9 pagesReviewer Bank To MiningMarynissa CatibogNo ratings yet

- Final Exam 301Document9 pagesFinal Exam 301Marynissa CatibogNo ratings yet

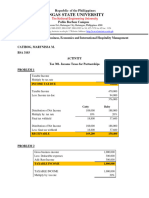

- Catibog, Marynissa M. - Activity On Income Taxes For PartnershipsDocument2 pagesCatibog, Marynissa M. - Activity On Income Taxes For PartnershipsMarynissa CatibogNo ratings yet

- Module 4 CONSTRUCTION CONTRACTSDocument5 pagesModule 4 CONSTRUCTION CONTRACTSMarynissa CatibogNo ratings yet

- Asean ReviewerDocument7 pagesAsean ReviewerMarynissa CatibogNo ratings yet

- Catibog, Marynissa M. - Assignment 1 - Taxes On IndividualsDocument7 pagesCatibog, Marynissa M. - Assignment 1 - Taxes On IndividualsMarynissa CatibogNo ratings yet

- Catibog, Marynissa M. (Intermediate Acctg Activity)Document9 pagesCatibog, Marynissa M. (Intermediate Acctg Activity)Marynissa CatibogNo ratings yet

- Catibog, Marynissa M. - Assignment 2 - Income Taxes For CorporationDocument5 pagesCatibog, Marynissa M. - Assignment 2 - Income Taxes For CorporationMarynissa CatibogNo ratings yet

- Marynissa Catibog - Case On Law On Sales (Batch 3)Document2 pagesMarynissa Catibog - Case On Law On Sales (Batch 3)Marynissa CatibogNo ratings yet

- CATIBOG - 1.-Assignment - VAT-and-Exemptions-from-VATDocument2 pagesCATIBOG - 1.-Assignment - VAT-and-Exemptions-from-VATMarynissa CatibogNo ratings yet

- Advanced Taxation - United Kingdom (Atx - Uk) : Strategic Professional - OptionsDocument15 pagesAdvanced Taxation - United Kingdom (Atx - Uk) : Strategic Professional - OptionsONASHI DEVNANI BBANo ratings yet

- INCTAXA - Module 1Document26 pagesINCTAXA - Module 1JOVIE KATE MARIE MOLINANo ratings yet

- Overview of Vietnam Tax SystemDocument13 pagesOverview of Vietnam Tax SystemNhung HồngNo ratings yet

- Income Tax Course Manual (2021 T1) PDFDocument138 pagesIncome Tax Course Manual (2021 T1) PDFMrDorakonNo ratings yet

- Consolidated Financial Statements - Ownership Patterns and Income TaxesDocument33 pagesConsolidated Financial Statements - Ownership Patterns and Income Taxeslukring20100% (1)

- Irs RNH enDocument14 pagesIrs RNH enRui Sequeira IINo ratings yet

- Chapter 3 PDFDocument15 pagesChapter 3 PDFJay BrockNo ratings yet

- Philippine Public FinanceDocument77 pagesPhilippine Public Financeflesteban100% (1)

- Income TaxDocument38 pagesIncome TaxNaiza Mae R. BinayaoNo ratings yet

- Test BankDocument34 pagesTest Bankarslan0989No ratings yet

- A Comprehensive Study Among The Working Women Towards The Awareness of Tax Saving Schemes in AllahabadDocument9 pagesA Comprehensive Study Among The Working Women Towards The Awareness of Tax Saving Schemes in AllahabadAbhishek Janvier Frederick abhishek.frederickNo ratings yet

- SMChap 015Document41 pagesSMChap 015testbank100% (2)

- Chapter 15 PDFDocument12 pagesChapter 15 PDFDarijun SaldañaNo ratings yet

- Finance Zutter CH 1 4 REVIEWDocument112 pagesFinance Zutter CH 1 4 REVIEWMarjorie PalmaNo ratings yet

- Local TaxesDocument25 pagesLocal TaxesJims Leñar CezarNo ratings yet

- TaxDocument4 pagesTaxCielito AlvarezNo ratings yet

- Sison V AnchetaDocument7 pagesSison V Anchetacha chaNo ratings yet

- Chapter 16 Homework SolutionsDocument6 pagesChapter 16 Homework SolutionsJackNo ratings yet

- The Replacement Ratio Making It PersonalDocument11 pagesThe Replacement Ratio Making It PersonalDorothy LamNo ratings yet

- Cfa Level Iii 2019 Formula SheetDocument3 pagesCfa Level Iii 2019 Formula SheetFaizan UllahNo ratings yet

- Chapter 1 Basic Tax ConceptsDocument13 pagesChapter 1 Basic Tax ConceptsJoey Aw YongNo ratings yet

- Lecture 4 TAXES AND THE MARGINAL INVESTORDocument14 pagesLecture 4 TAXES AND THE MARGINAL INVESTORAshiv MungurNo ratings yet

- Business Tax Reviewer UpdatedDocument36 pagesBusiness Tax Reviewer UpdatedCaptain ObviousNo ratings yet

- Mathematics: Standardised Competence-Oriented Written School-Leaving ExaminationDocument12 pagesMathematics: Standardised Competence-Oriented Written School-Leaving ExaminationbestgamerNo ratings yet

- Slice and DiceDocument153 pagesSlice and Dicejunohcu310No ratings yet

- Categories of Income and Tax RatesDocument5 pagesCategories of Income and Tax RatesRonel CacheroNo ratings yet

- Chapter 19 BKM Investments 9e SolutionsDocument11 pagesChapter 19 BKM Investments 9e Solutionsnpiper29100% (1)