Download as docx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5825)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- CCA Conduct Rule 1965 MCQDocument56 pagesCCA Conduct Rule 1965 MCQANURAG SINGH100% (10)

- Pe3042 ManualDocument21 pagesPe3042 ManualEDGARNo ratings yet

- 161 - Updated - Combined Offer LettersDocument9 pages161 - Updated - Combined Offer LettersAnkit ChoudharyNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 2004 Rules On Notarial Practice As AmendedDocument102 pages2004 Rules On Notarial Practice As AmendedNovo FarmsNo ratings yet

- Tan Tiong Tick Vs American ApothecariesDocument10 pagesTan Tiong Tick Vs American ApothecariesNovo FarmsNo ratings yet

- 11 Judicial RegionDocument9 pages11 Judicial RegionNovo FarmsNo ratings yet

- Phil. Banking Corp. v. CADocument15 pagesPhil. Banking Corp. v. CANovo FarmsNo ratings yet

- Citibank Vs Sps CabamonganDocument10 pagesCitibank Vs Sps CabamonganNovo FarmsNo ratings yet

- Fair Land Vs Loo PooDocument9 pagesFair Land Vs Loo PooNovo FarmsNo ratings yet

- By-Laws (Stock Corporation)Document3 pagesBy-Laws (Stock Corporation)Novo FarmsNo ratings yet

- Acknowledgment-Deed of SaleDocument2 pagesAcknowledgment-Deed of SaleNovo FarmsNo ratings yet

- Minutes of Organizational Meeting OF Abcs CorporationDocument1 pageMinutes of Organizational Meeting OF Abcs CorporationNovo FarmsNo ratings yet

- Notice of Stockholder's MeetingDocument1 pageNotice of Stockholder's MeetingNovo FarmsNo ratings yet

- Escalation Clause - Sampaguita Vs PNBDocument34 pagesEscalation Clause - Sampaguita Vs PNBNovo FarmsNo ratings yet

- Secretary's CertificateDocument1 pageSecretary's CertificateNovo FarmsNo ratings yet

- 6.articles of IncorporationDocument5 pages6.articles of IncorporationNovo FarmsNo ratings yet

- Moran Vs CADocument10 pagesMoran Vs CANovo FarmsNo ratings yet

- Lapreciosisima Vs Planters Development BankDocument11 pagesLapreciosisima Vs Planters Development BankNovo FarmsNo ratings yet

- PNB Vs Sps CheahDocument10 pagesPNB Vs Sps CheahNovo FarmsNo ratings yet

- Tormis Vs Judge ParedesDocument2 pagesTormis Vs Judge ParedesacAc acNo ratings yet

- Fernandez V DimagibaDocument1 pageFernandez V DimagibaLuz Celine CabadingNo ratings yet

- Ebook Calculus and Its Applications 14Th Edition Goldstein Solutions Manual Full Chapter PDFDocument56 pagesEbook Calculus and Its Applications 14Th Edition Goldstein Solutions Manual Full Chapter PDFMarcusKingbicy100% (14)

- Letter of Tender Addendum No. 2ADocument2 pagesLetter of Tender Addendum No. 2AKevin JulianNo ratings yet

- Government of India: Notes: 1. Attempt Any 8 Questions. 2. All Questions Carry Equal MarksDocument35 pagesGovernment of India: Notes: 1. Attempt Any 8 Questions. 2. All Questions Carry Equal MarksMadhabi NaskarNo ratings yet

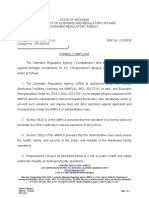

- Michigan Investments Formal Complaint 22-00330Document5 pagesMichigan Investments Formal Complaint 22-00330Fergus BurnsNo ratings yet

- MahaRERA General Amendment Regulations 2017 - Form and AgreementDocument12 pagesMahaRERA General Amendment Regulations 2017 - Form and AgreementQurban Hussain KudleNo ratings yet

- Adr Notes ExtrasDocument10 pagesAdr Notes ExtrasJimmy KiharaNo ratings yet

- Company Law Solomon V SolomonDocument4 pagesCompany Law Solomon V SolomonDolan SahaNo ratings yet

- N KK 58 BUYg FJL 1626951361612Document1 pageN KK 58 BUYg FJL 1626951361612Ashish Singh Negi100% (1)

- 09.21.18 Metro Stonerich Offer No. 1077.18Document2 pages09.21.18 Metro Stonerich Offer No. 1077.18SBR CENTER BUILDERS INC.No ratings yet

- Irba Audit Compliance FaqDocument7 pagesIrba Audit Compliance FaqrendaninNo ratings yet

- Angel Meza Motion For Partial Summary Judgment W. ExhibitsDocument235 pagesAngel Meza Motion For Partial Summary Judgment W. ExhibitsRichNo ratings yet

- Ups Saver: Dubai United Arab EmiratesDocument1 pageUps Saver: Dubai United Arab Emirateswaleed.engr361No ratings yet

- Bodige Ramdas Revenue 30012023Document9 pagesBodige Ramdas Revenue 30012023srr legalNo ratings yet

- A Collection of Appendices From Mott Et. ElDocument41 pagesA Collection of Appendices From Mott Et. ElSaif KNo ratings yet

- Digest Magdalo-vs.-COMELEC-6-19-12Document2 pagesDigest Magdalo-vs.-COMELEC-6-19-12Rochelle GablinesNo ratings yet

- PoliticsDocument6 pagesPoliticsCristopher IanNo ratings yet

- People v. Coca JR., G.R. No. 133739, May 29, 2002, 382 SCRA 508Document14 pagesPeople v. Coca JR., G.R. No. 133739, May 29, 2002, 382 SCRA 508PRINCES ALLEN MATULACNo ratings yet

- The Hand That Signed The PaperDocument4 pagesThe Hand That Signed The PaperMarta FernandesNo ratings yet

- Design of TunnelsDocument6 pagesDesign of Tunnels位团结No ratings yet

- Federal Republic of Nigeria Official Gazette: ExtraordinaryDocument14 pagesFederal Republic of Nigeria Official Gazette: Extraordinarymerife franklinNo ratings yet

- Chapter 12. Grothendieck's Family IDocument4 pagesChapter 12. Grothendieck's Family IInamulhaq kNo ratings yet

- Copyright Bar ExamDocument18 pagesCopyright Bar ExamVance Ceballos100% (1)

- Mark Anthony Zabal, Thiting Estoso Jacosalem, and Odon S. Bandiola v. President Rodrigo Duterte, Salvador Medildea, and Eduardo Año, G.R No. 238467, February 12, 2019.Document1 pageMark Anthony Zabal, Thiting Estoso Jacosalem, and Odon S. Bandiola v. President Rodrigo Duterte, Salvador Medildea, and Eduardo Año, G.R No. 238467, February 12, 2019.christopher1julian1aNo ratings yet

- 1tanzaniasaruji Corporation V.african 155 of 2004Document5 pages1tanzaniasaruji Corporation V.african 155 of 2004ALFRED WEREMANo ratings yet

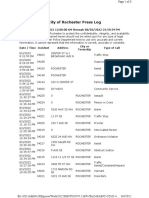

- RPD Daily Incident Report 8/3/22Document8 pagesRPD Daily Incident Report 8/3/22inforumdocsNo ratings yet