Handout 5.0 ACP 312 Consolidated FS Subsequent To Date of Acquisition Stock Acquisition v2.0

Handout 5.0 ACP 312 Consolidated FS Subsequent To Date of Acquisition Stock Acquisition v2.0

You might also like

- ACFrOgBKylWIFKqvQUoX2Yag018eml8V2evCY-xyBCergd9v5HXZoTbU3Q8kgtUcNC 5mafD1Hk933Hbe5goLmzsLjTjnum6IB4inPQsm6vrTPgbDppndlBKfMysfn8Document28 pagesACFrOgBKylWIFKqvQUoX2Yag018eml8V2evCY-xyBCergd9v5HXZoTbU3Q8kgtUcNC 5mafD1Hk933Hbe5goLmzsLjTjnum6IB4inPQsm6vrTPgbDppndlBKfMysfn8rodell pabloNo ratings yet

- 2 PDFDocument67 pages2 PDFMarcus MonocayNo ratings yet

- PROBLEM 1: P Company Had 90% Ownership Interest Acquired Several Years Ago in S Company. TheDocument4 pagesPROBLEM 1: P Company Had 90% Ownership Interest Acquired Several Years Ago in S Company. TheMargaveth P. Balbin75% (4)

- AFAR SimulationDocument111 pagesAFAR SimulationLloyd Sonica100% (1)

- AFAR-11 (Consolidated FS - Intercompany Sales of Fixed Assets)Document7 pagesAFAR-11 (Consolidated FS - Intercompany Sales of Fixed Assets)MABI ESPENIDONo ratings yet

- Consolidated FsDocument7 pagesConsolidated FsfreyawonderlandNo ratings yet

- Lecture 2 Business Combination Subsequent DateDocument8 pagesLecture 2 Business Combination Subsequent DateKristine Joy SaavedraNo ratings yet

- CPAR - AFAR - Final PB - Batch89Document18 pagesCPAR - AFAR - Final PB - Batch89MellaniNo ratings yet

- Unit 5. Audit of Investments, Hedging Instruments, and Related Revenues - Handout - T21920 (Final)Document9 pagesUnit 5. Audit of Investments, Hedging Instruments, and Related Revenues - Handout - T21920 (Final)Alyna JNo ratings yet

- Quiz 3 UploadDocument6 pagesQuiz 3 UploadandreamrieNo ratings yet

- ASSET 2019 Mock Boards - AFARDocument8 pagesASSET 2019 Mock Boards - AFARKenneth Christian Wilbur0% (1)

- 105 DepaDocument12 pages105 DepaLA M AENo ratings yet

- SDOADocument2 pagesSDOAassoc.uls2324No ratings yet

- Midterm Quiz in ACCTG2215Document17 pagesMidterm Quiz in ACCTG2215guess who100% (1)

- Advacc Midterm ExamDocument13 pagesAdvacc Midterm ExamJosh TanNo ratings yet

- Solidated Financial Statements Intercompany TransactionsDocument2 pagesSolidated Financial Statements Intercompany TransactionsDarlyn DalidaNo ratings yet

- Assignment No. 5 Hoba Franchising Joint ArrangementsDocument4 pagesAssignment No. 5 Hoba Franchising Joint ArrangementsJean TatsadoNo ratings yet

- Integrated Topic 1 (Far-004a)Document4 pagesIntegrated Topic 1 (Far-004a)lyndon delfinNo ratings yet

- Afar 2019Document9 pagesAfar 2019TakuriNo ratings yet

- S5a FINANCIAL RATIO ANALYSIS ASSIGNMENT QUESTIONSDocument16 pagesS5a FINANCIAL RATIO ANALYSIS ASSIGNMENT QUESTIONSSYED ANEES ALINo ratings yet

- Tugas Pertemuan 4 - Alya Sufi Ikrima - 041911333248Document5 pagesTugas Pertemuan 4 - Alya Sufi Ikrima - 041911333248Alya Sufi IkrimaNo ratings yet

- SEPARATE and CONSOLIDATED STATEMENTSDocument4 pagesSEPARATE and CONSOLIDATED STATEMENTSCha EsguerraNo ratings yet

- Midterm Examination - ABCDocument5 pagesMidterm Examination - ABCMaria DyNo ratings yet

- AccountingDocument9 pagesAccountingTakuriNo ratings yet

- 16 Consolidation Subsequent To The Date of AcquisitionDocument3 pages16 Consolidation Subsequent To The Date of AcquisitionMila Casandra CastañedaNo ratings yet

- Investment in Associate 2022Document3 pagesInvestment in Associate 2022lirva cantonaNo ratings yet

- Quiz - 3 ABC Problem SolvingDocument6 pagesQuiz - 3 ABC Problem SolvingAngelito Mamersonal0% (1)

- I. Theory. True or False: Consolidated Financial Statements and Separate Financial StatementsDocument4 pagesI. Theory. True or False: Consolidated Financial Statements and Separate Financial StatementsRoxell CaibogNo ratings yet

- Indicate Whether The Statement Is True or FalseDocument11 pagesIndicate Whether The Statement Is True or Falseryan rosalesNo ratings yet

- Module 3 InvestmentDocument12 pagesModule 3 InvestmentKim JisooNo ratings yet

- Ugbs CR 2023 Ia 1 PDDocument8 pagesUgbs CR 2023 Ia 1 PDkelvinflafe974No ratings yet

- Cup-Advanced Financial Accounting and ReportingDocument7 pagesCup-Advanced Financial Accounting and ReportingJerauld Bucol100% (1)

- Key Quiz 2 2022 2023Document4 pagesKey Quiz 2 2022 2023Leslie Mae Vargas ZafeNo ratings yet

- Practice Actp 4 SubsDocument4 pagesPractice Actp 4 SubsWisley GamuzaNo ratings yet

- Financial Reporting: Specimen Exam Applicable From September 2016Document25 pagesFinancial Reporting: Specimen Exam Applicable From September 2016Jodlike bolteNo ratings yet

- 94 - Final Preaboard AFAR - UnlockedDocument17 pages94 - Final Preaboard AFAR - UnlockedJessaNo ratings yet

- Acp - Acc417 Case Study 1Document6 pagesAcp - Acc417 Case Study 1Faker MejiaNo ratings yet

- PART 1-THEORIES (1pt. Each) "A" If TRUE, "B" If FALSEDocument7 pagesPART 1-THEORIES (1pt. Each) "A" If TRUE, "B" If FALSEDrew BanlutaNo ratings yet

- IA2 Finals ReviewerDocument6 pagesIA2 Finals ReviewerJoana MarieNo ratings yet

- Prelim ExamDocument13 pagesPrelim ExamNah HamzaNo ratings yet

- Practice Problems: C. The Consolidated Total Assets After The Combination Is P6,116,250Document5 pagesPractice Problems: C. The Consolidated Total Assets After The Combination Is P6,116,250Will Emmanuel A PinoyNo ratings yet

- FAR AssessmentDocument4 pagesFAR AssessmentLuna VNo ratings yet

- Partnership Formation and Operation.Document4 pagesPartnership Formation and Operation.May RamosNo ratings yet

- Lesson 05B. Inter-Company Transactions - A.TDocument8 pagesLesson 05B. Inter-Company Transactions - A.THayes HareNo ratings yet

- Module 3 InvestmentDocument12 pagesModule 3 Investmenttite ko'y malake100% (1)

- BADVAC1X - MOD 2 Conso FS Date of AcqDocument6 pagesBADVAC1X - MOD 2 Conso FS Date of AcqJopnerth Carl CortezNo ratings yet

- Audit of InvestmentsDocument3 pagesAudit of InvestmentsJasmine Marie Ng Cheong50% (2)

- TOPIC 2 - Topic 2 - Consolidated and Separate Financial StatementsDocument6 pagesTOPIC 2 - Topic 2 - Consolidated and Separate Financial Statementsduguitjinky20.svcNo ratings yet

- Investments: Problem 1Document4 pagesInvestments: Problem 1Frederick AbellaNo ratings yet

- ReporttDocument7 pagesReporttaryan nicoleNo ratings yet

- Financial Reporting: Specimen Exam Applicable From September 2016Document25 pagesFinancial Reporting: Specimen Exam Applicable From September 2016Hari RamNo ratings yet

- Q3F - Investment in Associate - 2ndsem 2019-202Document6 pagesQ3F - Investment in Associate - 2ndsem 2019-202Geoff Macarate100% (1)

- ACCExpanded Opportunity Part 1Document4 pagesACCExpanded Opportunity Part 1Hilarie JeanNo ratings yet

- CFR 1 Quiz 1Document7 pagesCFR 1 Quiz 1Ahmed SamadNo ratings yet

- AFAR 3 (Test Questions)Document4 pagesAFAR 3 (Test Questions)Lalaine BeatrizNo ratings yet

- Usc Part 2020 (Far) - RetakeDocument25 pagesUsc Part 2020 (Far) - RetakeVince AbabonNo ratings yet

- ADV ACC TBch04Document21 pagesADV ACC TBch04hassan nassereddine100% (2)

- College of Business, Entrepreneurship and AccountancyDocument8 pagesCollege of Business, Entrepreneurship and AccountancyCherry Ann RoblesNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- 561 600Document13 pages561 600Rhea Jane ParconNo ratings yet

- Audit ReportDocument3 pagesAudit ReportRhea Jane ParconNo ratings yet

- UnitV CabreraDocument14 pagesUnitV CabreraRhea Jane ParconNo ratings yet

- Partnership-2 0Document2 pagesPartnership-2 0Rhea Jane ParconNo ratings yet

- Share Option SARDocument48 pagesShare Option SARRhea Jane ParconNo ratings yet

- Module 3. Direct Finance Lease Lessor AccountingDocument4 pagesModule 3. Direct Finance Lease Lessor AccountingRhea Jane ParconNo ratings yet

- Depreciation-Functions - BlankDocument3 pagesDepreciation-Functions - BlankRhea Jane ParconNo ratings yet

- Working CapitalAnswerkeyDocument52 pagesWorking CapitalAnswerkeyRhea Jane ParconNo ratings yet

- Quiper Quiz Relevant CostingDocument15 pagesQuiper Quiz Relevant CostingRhea Jane ParconNo ratings yet

- PFRS For SMEs and SEs Transition ProvisionsDocument18 pagesPFRS For SMEs and SEs Transition ProvisionsRhea Jane ParconNo ratings yet

- Partnership Notes-6Document3 pagesPartnership Notes-6Rhea Jane ParconNo ratings yet

- Partnership Notes 4Document4 pagesPartnership Notes 4Rhea Jane ParconNo ratings yet

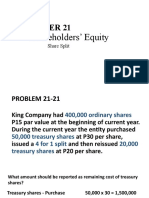

- Prob 21 21Document4 pagesProb 21 21Rhea Jane ParconNo ratings yet

- Partnership Notes 5Document4 pagesPartnership Notes 5Rhea Jane ParconNo ratings yet

- Partnership-1 0Document5 pagesPartnership-1 0Rhea Jane ParconNo ratings yet

- Feasibility Study - 0Document4 pagesFeasibility Study - 0Rhea Jane ParconNo ratings yet

- KLBF Fy2022Document178 pagesKLBF Fy2022Ayu WandiraNo ratings yet

- CHAPTER5Document8 pagesCHAPTER5Anjelika ViescaNo ratings yet

- ACT 1301 L S CommonDocument97 pagesACT 1301 L S CommonSadia AkterNo ratings yet

- Resume Prabesh Chandra AdhikariDocument2 pagesResume Prabesh Chandra AdhikariSrirama SrinivasanNo ratings yet

- Single Entry SystemDocument6 pagesSingle Entry SystemShruti JoseNo ratings yet

- Financial & Managerial Accounting Mbas: Oanhnguyenth231Document64 pagesFinancial & Managerial Accounting Mbas: Oanhnguyenth231Hồng LongNo ratings yet

- Comparative Statement Analysis of Vijaya DairyDocument51 pagesComparative Statement Analysis of Vijaya DairyRajkamalChicha50% (4)

- Public Sector Accounting Developments and Conceptual FrameworkDocument24 pagesPublic Sector Accounting Developments and Conceptual FrameworkREJAY89No ratings yet

- Textbook Managerial Accounting Ray H Garrison Ebook All Chapter PDFDocument53 pagesTextbook Managerial Accounting Ray H Garrison Ebook All Chapter PDFmary.pauling946100% (11)

- Management Discussion and AnalysisDocument11 pagesManagement Discussion and AnalysishihiNo ratings yet

- Toaz - Info Auditing Theory Test Bank PRDocument8 pagesToaz - Info Auditing Theory Test Bank PRChriz VillasNo ratings yet

- Period End Processing - Summary The Following Outlines:: PayablesDocument3 pagesPeriod End Processing - Summary The Following Outlines:: Payablesbritesprite2000No ratings yet

- 03-PSU-ACC 202 - Principles of Accounting 2 - 2022F - Lecture SlidesDocument56 pages03-PSU-ACC 202 - Principles of Accounting 2 - 2022F - Lecture SlidesThanh ThùyNo ratings yet

- Admas University: Course OutlineDocument5 pagesAdmas University: Course Outlinerediet solomonNo ratings yet

- Adani Bs MergedDocument10 pagesAdani Bs MergedRishabhNo ratings yet

- 2.principles of AuditingDocument114 pages2.principles of AuditingGokul.S 20BCP0010No ratings yet

- Structure of The Balance Sheet and Statement of Cash Flows: Revsine/Collins/Johnson/Mittelstaedt/Soffer: Chapter 4Document39 pagesStructure of The Balance Sheet and Statement of Cash Flows: Revsine/Collins/Johnson/Mittelstaedt/Soffer: Chapter 4amyNo ratings yet

- Unit 3 - Bookkeping-1-2Document2 pagesUnit 3 - Bookkeping-1-2JHON ALEJANDRO GALLEGO GALINDONo ratings yet

- Lecture 1 - Accounting in ActionDocument71 pagesLecture 1 - Accounting in Actionarman islamNo ratings yet

- Circular No. 20 (Holiday Homework of Class Xii)Document43 pagesCircular No. 20 (Holiday Homework of Class Xii)rishu ashiNo ratings yet

- Chapter 01 - Intercorporate Acquisitions and Investments in Other EntitiesDocument21 pagesChapter 01 - Intercorporate Acquisitions and Investments in Other Entitiesdella salsabilaNo ratings yet

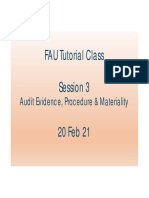

- FAU Session 3 Audit Evidence, Materiality and Procedure 2Document16 pagesFAU Session 3 Audit Evidence, Materiality and Procedure 2BuntheaNo ratings yet

- 12 SSDDDDocument3 pages12 SSDDDAlvira FajriNo ratings yet

- Incf 2017-2Document90 pagesIncf 2017-2RimaNo ratings yet

- B326: Advance Accounting B326 Course Structure: Chapter 5: Intercompany Transaction - InventoryDocument20 pagesB326: Advance Accounting B326 Course Structure: Chapter 5: Intercompany Transaction - InventoryAyeshaNo ratings yet

- IAS-40 Investment PropertyDocument5 pagesIAS-40 Investment Propertymanvi jainNo ratings yet

- Audit Evidence - Unit TwoDocument28 pagesAudit Evidence - Unit TwoKananelo MOSENANo ratings yet

- Level 4 Thoery-1Document25 pagesLevel 4 Thoery-1EdomNo ratings yet

- CA Final PARAM Question Bank Vol-2 Colour (10 MB)Document262 pagesCA Final PARAM Question Bank Vol-2 Colour (10 MB)Pooja DewanNo ratings yet

Download as pdf or txt

You might also like

- ACFrOgBKylWIFKqvQUoX2Yag018eml8V2evCY-xyBCergd9v5HXZoTbU3Q8kgtUcNC 5mafD1Hk933Hbe5goLmzsLjTjnum6IB4inPQsm6vrTPgbDppndlBKfMysfn8Document28 pagesACFrOgBKylWIFKqvQUoX2Yag018eml8V2evCY-xyBCergd9v5HXZoTbU3Q8kgtUcNC 5mafD1Hk933Hbe5goLmzsLjTjnum6IB4inPQsm6vrTPgbDppndlBKfMysfn8rodell pabloNo ratings yet

- 2 PDFDocument67 pages2 PDFMarcus MonocayNo ratings yet

- PROBLEM 1: P Company Had 90% Ownership Interest Acquired Several Years Ago in S Company. TheDocument4 pagesPROBLEM 1: P Company Had 90% Ownership Interest Acquired Several Years Ago in S Company. TheMargaveth P. Balbin75% (4)

- AFAR SimulationDocument111 pagesAFAR SimulationLloyd Sonica100% (1)

- AFAR-11 (Consolidated FS - Intercompany Sales of Fixed Assets)Document7 pagesAFAR-11 (Consolidated FS - Intercompany Sales of Fixed Assets)MABI ESPENIDONo ratings yet

- Consolidated FsDocument7 pagesConsolidated FsfreyawonderlandNo ratings yet

- Lecture 2 Business Combination Subsequent DateDocument8 pagesLecture 2 Business Combination Subsequent DateKristine Joy SaavedraNo ratings yet

- CPAR - AFAR - Final PB - Batch89Document18 pagesCPAR - AFAR - Final PB - Batch89MellaniNo ratings yet

- Unit 5. Audit of Investments, Hedging Instruments, and Related Revenues - Handout - T21920 (Final)Document9 pagesUnit 5. Audit of Investments, Hedging Instruments, and Related Revenues - Handout - T21920 (Final)Alyna JNo ratings yet

- Quiz 3 UploadDocument6 pagesQuiz 3 UploadandreamrieNo ratings yet

- ASSET 2019 Mock Boards - AFARDocument8 pagesASSET 2019 Mock Boards - AFARKenneth Christian Wilbur0% (1)

- 105 DepaDocument12 pages105 DepaLA M AENo ratings yet

- SDOADocument2 pagesSDOAassoc.uls2324No ratings yet

- Midterm Quiz in ACCTG2215Document17 pagesMidterm Quiz in ACCTG2215guess who100% (1)

- Advacc Midterm ExamDocument13 pagesAdvacc Midterm ExamJosh TanNo ratings yet

- Solidated Financial Statements Intercompany TransactionsDocument2 pagesSolidated Financial Statements Intercompany TransactionsDarlyn DalidaNo ratings yet

- Assignment No. 5 Hoba Franchising Joint ArrangementsDocument4 pagesAssignment No. 5 Hoba Franchising Joint ArrangementsJean TatsadoNo ratings yet

- Integrated Topic 1 (Far-004a)Document4 pagesIntegrated Topic 1 (Far-004a)lyndon delfinNo ratings yet

- Afar 2019Document9 pagesAfar 2019TakuriNo ratings yet

- S5a FINANCIAL RATIO ANALYSIS ASSIGNMENT QUESTIONSDocument16 pagesS5a FINANCIAL RATIO ANALYSIS ASSIGNMENT QUESTIONSSYED ANEES ALINo ratings yet

- Tugas Pertemuan 4 - Alya Sufi Ikrima - 041911333248Document5 pagesTugas Pertemuan 4 - Alya Sufi Ikrima - 041911333248Alya Sufi IkrimaNo ratings yet

- SEPARATE and CONSOLIDATED STATEMENTSDocument4 pagesSEPARATE and CONSOLIDATED STATEMENTSCha EsguerraNo ratings yet

- Midterm Examination - ABCDocument5 pagesMidterm Examination - ABCMaria DyNo ratings yet

- AccountingDocument9 pagesAccountingTakuriNo ratings yet

- 16 Consolidation Subsequent To The Date of AcquisitionDocument3 pages16 Consolidation Subsequent To The Date of AcquisitionMila Casandra CastañedaNo ratings yet

- Investment in Associate 2022Document3 pagesInvestment in Associate 2022lirva cantonaNo ratings yet

- Quiz - 3 ABC Problem SolvingDocument6 pagesQuiz - 3 ABC Problem SolvingAngelito Mamersonal0% (1)

- I. Theory. True or False: Consolidated Financial Statements and Separate Financial StatementsDocument4 pagesI. Theory. True or False: Consolidated Financial Statements and Separate Financial StatementsRoxell CaibogNo ratings yet

- Indicate Whether The Statement Is True or FalseDocument11 pagesIndicate Whether The Statement Is True or Falseryan rosalesNo ratings yet

- Module 3 InvestmentDocument12 pagesModule 3 InvestmentKim JisooNo ratings yet

- Ugbs CR 2023 Ia 1 PDDocument8 pagesUgbs CR 2023 Ia 1 PDkelvinflafe974No ratings yet

- Cup-Advanced Financial Accounting and ReportingDocument7 pagesCup-Advanced Financial Accounting and ReportingJerauld Bucol100% (1)

- Key Quiz 2 2022 2023Document4 pagesKey Quiz 2 2022 2023Leslie Mae Vargas ZafeNo ratings yet

- Practice Actp 4 SubsDocument4 pagesPractice Actp 4 SubsWisley GamuzaNo ratings yet

- Financial Reporting: Specimen Exam Applicable From September 2016Document25 pagesFinancial Reporting: Specimen Exam Applicable From September 2016Jodlike bolteNo ratings yet

- 94 - Final Preaboard AFAR - UnlockedDocument17 pages94 - Final Preaboard AFAR - UnlockedJessaNo ratings yet

- Acp - Acc417 Case Study 1Document6 pagesAcp - Acc417 Case Study 1Faker MejiaNo ratings yet

- PART 1-THEORIES (1pt. Each) "A" If TRUE, "B" If FALSEDocument7 pagesPART 1-THEORIES (1pt. Each) "A" If TRUE, "B" If FALSEDrew BanlutaNo ratings yet

- IA2 Finals ReviewerDocument6 pagesIA2 Finals ReviewerJoana MarieNo ratings yet

- Prelim ExamDocument13 pagesPrelim ExamNah HamzaNo ratings yet

- Practice Problems: C. The Consolidated Total Assets After The Combination Is P6,116,250Document5 pagesPractice Problems: C. The Consolidated Total Assets After The Combination Is P6,116,250Will Emmanuel A PinoyNo ratings yet

- FAR AssessmentDocument4 pagesFAR AssessmentLuna VNo ratings yet

- Partnership Formation and Operation.Document4 pagesPartnership Formation and Operation.May RamosNo ratings yet

- Lesson 05B. Inter-Company Transactions - A.TDocument8 pagesLesson 05B. Inter-Company Transactions - A.THayes HareNo ratings yet

- Module 3 InvestmentDocument12 pagesModule 3 Investmenttite ko'y malake100% (1)

- BADVAC1X - MOD 2 Conso FS Date of AcqDocument6 pagesBADVAC1X - MOD 2 Conso FS Date of AcqJopnerth Carl CortezNo ratings yet

- Audit of InvestmentsDocument3 pagesAudit of InvestmentsJasmine Marie Ng Cheong50% (2)

- TOPIC 2 - Topic 2 - Consolidated and Separate Financial StatementsDocument6 pagesTOPIC 2 - Topic 2 - Consolidated and Separate Financial Statementsduguitjinky20.svcNo ratings yet

- Investments: Problem 1Document4 pagesInvestments: Problem 1Frederick AbellaNo ratings yet

- ReporttDocument7 pagesReporttaryan nicoleNo ratings yet

- Financial Reporting: Specimen Exam Applicable From September 2016Document25 pagesFinancial Reporting: Specimen Exam Applicable From September 2016Hari RamNo ratings yet

- Q3F - Investment in Associate - 2ndsem 2019-202Document6 pagesQ3F - Investment in Associate - 2ndsem 2019-202Geoff Macarate100% (1)

- ACCExpanded Opportunity Part 1Document4 pagesACCExpanded Opportunity Part 1Hilarie JeanNo ratings yet

- CFR 1 Quiz 1Document7 pagesCFR 1 Quiz 1Ahmed SamadNo ratings yet

- AFAR 3 (Test Questions)Document4 pagesAFAR 3 (Test Questions)Lalaine BeatrizNo ratings yet

- Usc Part 2020 (Far) - RetakeDocument25 pagesUsc Part 2020 (Far) - RetakeVince AbabonNo ratings yet

- ADV ACC TBch04Document21 pagesADV ACC TBch04hassan nassereddine100% (2)

- College of Business, Entrepreneurship and AccountancyDocument8 pagesCollege of Business, Entrepreneurship and AccountancyCherry Ann RoblesNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- 561 600Document13 pages561 600Rhea Jane ParconNo ratings yet

- Audit ReportDocument3 pagesAudit ReportRhea Jane ParconNo ratings yet

- UnitV CabreraDocument14 pagesUnitV CabreraRhea Jane ParconNo ratings yet

- Partnership-2 0Document2 pagesPartnership-2 0Rhea Jane ParconNo ratings yet

- Share Option SARDocument48 pagesShare Option SARRhea Jane ParconNo ratings yet

- Module 3. Direct Finance Lease Lessor AccountingDocument4 pagesModule 3. Direct Finance Lease Lessor AccountingRhea Jane ParconNo ratings yet

- Depreciation-Functions - BlankDocument3 pagesDepreciation-Functions - BlankRhea Jane ParconNo ratings yet

- Working CapitalAnswerkeyDocument52 pagesWorking CapitalAnswerkeyRhea Jane ParconNo ratings yet

- Quiper Quiz Relevant CostingDocument15 pagesQuiper Quiz Relevant CostingRhea Jane ParconNo ratings yet

- PFRS For SMEs and SEs Transition ProvisionsDocument18 pagesPFRS For SMEs and SEs Transition ProvisionsRhea Jane ParconNo ratings yet

- Partnership Notes-6Document3 pagesPartnership Notes-6Rhea Jane ParconNo ratings yet

- Partnership Notes 4Document4 pagesPartnership Notes 4Rhea Jane ParconNo ratings yet

- Prob 21 21Document4 pagesProb 21 21Rhea Jane ParconNo ratings yet

- Partnership Notes 5Document4 pagesPartnership Notes 5Rhea Jane ParconNo ratings yet

- Partnership-1 0Document5 pagesPartnership-1 0Rhea Jane ParconNo ratings yet

- Feasibility Study - 0Document4 pagesFeasibility Study - 0Rhea Jane ParconNo ratings yet

- KLBF Fy2022Document178 pagesKLBF Fy2022Ayu WandiraNo ratings yet

- CHAPTER5Document8 pagesCHAPTER5Anjelika ViescaNo ratings yet

- ACT 1301 L S CommonDocument97 pagesACT 1301 L S CommonSadia AkterNo ratings yet

- Resume Prabesh Chandra AdhikariDocument2 pagesResume Prabesh Chandra AdhikariSrirama SrinivasanNo ratings yet

- Single Entry SystemDocument6 pagesSingle Entry SystemShruti JoseNo ratings yet

- Financial & Managerial Accounting Mbas: Oanhnguyenth231Document64 pagesFinancial & Managerial Accounting Mbas: Oanhnguyenth231Hồng LongNo ratings yet

- Comparative Statement Analysis of Vijaya DairyDocument51 pagesComparative Statement Analysis of Vijaya DairyRajkamalChicha50% (4)

- Public Sector Accounting Developments and Conceptual FrameworkDocument24 pagesPublic Sector Accounting Developments and Conceptual FrameworkREJAY89No ratings yet

- Textbook Managerial Accounting Ray H Garrison Ebook All Chapter PDFDocument53 pagesTextbook Managerial Accounting Ray H Garrison Ebook All Chapter PDFmary.pauling946100% (11)

- Management Discussion and AnalysisDocument11 pagesManagement Discussion and AnalysishihiNo ratings yet

- Toaz - Info Auditing Theory Test Bank PRDocument8 pagesToaz - Info Auditing Theory Test Bank PRChriz VillasNo ratings yet

- Period End Processing - Summary The Following Outlines:: PayablesDocument3 pagesPeriod End Processing - Summary The Following Outlines:: Payablesbritesprite2000No ratings yet

- 03-PSU-ACC 202 - Principles of Accounting 2 - 2022F - Lecture SlidesDocument56 pages03-PSU-ACC 202 - Principles of Accounting 2 - 2022F - Lecture SlidesThanh ThùyNo ratings yet

- Admas University: Course OutlineDocument5 pagesAdmas University: Course Outlinerediet solomonNo ratings yet

- Adani Bs MergedDocument10 pagesAdani Bs MergedRishabhNo ratings yet

- 2.principles of AuditingDocument114 pages2.principles of AuditingGokul.S 20BCP0010No ratings yet

- Structure of The Balance Sheet and Statement of Cash Flows: Revsine/Collins/Johnson/Mittelstaedt/Soffer: Chapter 4Document39 pagesStructure of The Balance Sheet and Statement of Cash Flows: Revsine/Collins/Johnson/Mittelstaedt/Soffer: Chapter 4amyNo ratings yet

- Unit 3 - Bookkeping-1-2Document2 pagesUnit 3 - Bookkeping-1-2JHON ALEJANDRO GALLEGO GALINDONo ratings yet

- Lecture 1 - Accounting in ActionDocument71 pagesLecture 1 - Accounting in Actionarman islamNo ratings yet

- Circular No. 20 (Holiday Homework of Class Xii)Document43 pagesCircular No. 20 (Holiday Homework of Class Xii)rishu ashiNo ratings yet

- Chapter 01 - Intercorporate Acquisitions and Investments in Other EntitiesDocument21 pagesChapter 01 - Intercorporate Acquisitions and Investments in Other Entitiesdella salsabilaNo ratings yet

- FAU Session 3 Audit Evidence, Materiality and Procedure 2Document16 pagesFAU Session 3 Audit Evidence, Materiality and Procedure 2BuntheaNo ratings yet

- 12 SSDDDDocument3 pages12 SSDDDAlvira FajriNo ratings yet

- Incf 2017-2Document90 pagesIncf 2017-2RimaNo ratings yet

- B326: Advance Accounting B326 Course Structure: Chapter 5: Intercompany Transaction - InventoryDocument20 pagesB326: Advance Accounting B326 Course Structure: Chapter 5: Intercompany Transaction - InventoryAyeshaNo ratings yet

- IAS-40 Investment PropertyDocument5 pagesIAS-40 Investment Propertymanvi jainNo ratings yet

- Audit Evidence - Unit TwoDocument28 pagesAudit Evidence - Unit TwoKananelo MOSENANo ratings yet

- Level 4 Thoery-1Document25 pagesLevel 4 Thoery-1EdomNo ratings yet

- CA Final PARAM Question Bank Vol-2 Colour (10 MB)Document262 pagesCA Final PARAM Question Bank Vol-2 Colour (10 MB)Pooja DewanNo ratings yet