Download as xlsx, pdf, or txt

You might also like

- Bergerac SystemsDocument4 pagesBergerac Systemsgogana93100% (1)

- Mathematics SBADocument6 pagesMathematics SBASeifer Rattan67% (3)

- Assigment 5.34Document7 pagesAssigment 5.34Indahna SulfaNo ratings yet

- AML-Excercise Week 4 (Reviandi Ramadhan)Document21 pagesAML-Excercise Week 4 (Reviandi Ramadhan)reviandiramadhanNo ratings yet

- Practice Questions - SolDocument8 pagesPractice Questions - SolNicholas LeeNo ratings yet

- Bergerac Systems: The Challenge of Backward IntegrationDocument8 pagesBergerac Systems: The Challenge of Backward IntegrationSujith KumarNo ratings yet

- Property, Plant and Equipement: Prior To Expense AfterDocument8 pagesProperty, Plant and Equipement: Prior To Expense AfterAvox EverdeenNo ratings yet

- 78Document1 page78laale dijaanNo ratings yet

- Bergerac AUDocument2 pagesBergerac AUPratyashNo ratings yet

- Bergerac D3D3D3Systems: The Challenge of Backward IntegrationDocument4 pagesBergerac D3D3D3Systems: The Challenge of Backward IntegrationZee ShanNo ratings yet

- Chap 4 Job CostingDocument9 pagesChap 4 Job CostingWadiah AkbarNo ratings yet

- Bergessssssrac D3D3D3Systems: The Challenge of Backward IntegrationDocument4 pagesBergessssssrac D3D3D3Systems: The Challenge of Backward IntegrationZee ShanNo ratings yet

- Best Financial Forecast FinalDocument13 pagesBest Financial Forecast Finalitsmethird.26No ratings yet

- Dbergessssssrac D3D3D3Systems: The Challenge of Backward IntegrationDocument4 pagesDbergessssssrac D3D3D3Systems: The Challenge of Backward IntegrationZee ShanNo ratings yet

- 24GK0065Document12 pages24GK0065bernardorasimo26No ratings yet

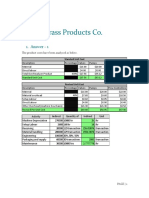

- Destin Brass Products Co.: 1. Answer - 1Document5 pagesDestin Brass Products Co.: 1. Answer - 1Chetan DasguptaNo ratings yet

- MFA - Assignment 2: Management and Financial Accounting - Individual Assignment 2Document9 pagesMFA - Assignment 2: Management and Financial Accounting - Individual Assignment 2Mohan sunderNo ratings yet

- Acct602 Managerial AccountingDocument8 pagesAcct602 Managerial AccountingHaroon KhurshidNo ratings yet

- Chapter 2 and 3 AssignmentDocument12 pagesChapter 2 and 3 AssignmentBien Carlo BuenaventuraNo ratings yet

- Program of Works:: Prop. Kiwalan Public Market BuildingDocument17 pagesProgram of Works:: Prop. Kiwalan Public Market BuildingFred Vincent BaldomeroNo ratings yet

- Cupcake Exports LTD.: Pre Cost Sheet-StarntalerDocument23 pagesCupcake Exports LTD.: Pre Cost Sheet-StarntalerromanNo ratings yet

- Activity Based Costing - APO 9Document13 pagesActivity Based Costing - APO 9manan guptaNo ratings yet

- 24GK0064Document13 pages24GK0064bernardorasimo26No ratings yet

- Imba Case 3: Situation OneDocument6 pagesImba Case 3: Situation OneK IdolsNo ratings yet

- Traditional Vs ABC Costing CaseDocument1 pageTraditional Vs ABC Costing Casesul239No ratings yet

- ClassicPenCompany 2023B2PGPMX012 KshitijDocument3 pagesClassicPenCompany 2023B2PGPMX012 KshitijSuraj KumarNo ratings yet

- CE ExpansionDocument101 pagesCE ExpansionvictoriaNo ratings yet

- Entrep CostingDocument3 pagesEntrep Costingpitik.h4wking.1naNo ratings yet

- ABC Practice Problems Answer KeyDocument10 pagesABC Practice Problems Answer KeyKemberly AribanNo ratings yet

- Cost Estimate (Super ST)Document9 pagesCost Estimate (Super ST)Erika BanguilanNo ratings yet

- Solutions-Chapter 6Document4 pagesSolutions-Chapter 6Saurabh SinghNo ratings yet

- CH 5 ExcelDocument37 pagesCH 5 ExcelssdsNo ratings yet

- CH14 AbcDocument8 pagesCH14 AbcamitNo ratings yet

- Contract ID No. 23GF0020Document9 pagesContract ID No. 23GF0020Asia Structural Developer CorpNo ratings yet

- Module 2 Case AssignmentDocument2 pagesModule 2 Case AssignmentMadison HeffronNo ratings yet

- Accy 211 - Week 7 Tut HWDocument1 pageAccy 211 - Week 7 Tut HWIsaac ElhageNo ratings yet

- Case Study WilkersonDocument2 pagesCase Study WilkersonHIMANSHU AGRAWALNo ratings yet

- Exam 2 ReviewDocument18 pagesExam 2 ReviewBrad MellerNo ratings yet

- ALLE0000Document3 pagesALLE0000Ernesto LeonNo ratings yet

- Documents - MX - Destin Brass Products Co 55f065486abf6 PDFDocument9 pagesDocuments - MX - Destin Brass Products Co 55f065486abf6 PDFNikhil WadhwaniNo ratings yet

- Jawaban Soal Kasus 4.2 Bab 17 Akmen LJT Dari Laptop AnasDocument9 pagesJawaban Soal Kasus 4.2 Bab 17 Akmen LJT Dari Laptop AnasMaksi angkatan35No ratings yet

- Suraj T S (Me Cs 4)Document4 pagesSuraj T S (Me Cs 4)Suraj TSNo ratings yet

- 19GK0198 - NoDocument20 pages19GK0198 - NoBernardo RasimoNo ratings yet

- CCCAC Chapter 3Document10 pagesCCCAC Chapter 3rochelle lagmayNo ratings yet

- 23GF0027Document13 pages23GF0027Asia Structural Developer CorpNo ratings yet

- Break Even Analysis in ExcelDocument6 pagesBreak Even Analysis in ExcelsnishapattarNo ratings yet

- Accounting Project Segment 3Document2 pagesAccounting Project Segment 3Zach James LebreiroNo ratings yet

- Actual Bills Total 2,215: BescomDocument1 pageActual Bills Total 2,215: BescomAlokNo ratings yet

- Aaa EditeddddDocument60 pagesAaa EditeddddCristine JacangNo ratings yet

- Class Work AnswersDocument4 pagesClass Work Answersdavid.samhon73No ratings yet

- 19GK0201 - NoDocument20 pages19GK0201 - NoBernardo RasimoNo ratings yet

- Costing: Production Staff 389.00 4Document61 pagesCosting: Production Staff 389.00 4Jelai MatisNo ratings yet

- Local Access Road in KisolonDocument10 pagesLocal Access Road in KisolonKeirl John AsinguaNo ratings yet

- Mabugnao P1 230m ROAD 102 (20 2022)Document1 pageMabugnao P1 230m ROAD 102 (20 2022)Abhyn ANo ratings yet

- Pia Mendez Mendoza SanchezDocument3 pagesPia Mendez Mendoza Sancheznt26k2jc9sNo ratings yet

- Answers To 11 - 16 Assignment in ABC PDFDocument3 pagesAnswers To 11 - 16 Assignment in ABC PDFMubarrach MatabalaoNo ratings yet

- Cost AssignmentDocument6 pagesCost AssignmentDaksh NagpalNo ratings yet

- Contract ID No. 23GF0020 - Detailed EstimateDocument7 pagesContract ID No. 23GF0020 - Detailed EstimateAsia Structural Developer CorpNo ratings yet

- Financial AssumptionsDocument15 pagesFinancial AssumptionsAngelica VinasNo ratings yet

- Costing DCDocument1 pageCosting DCMharco ColipapaNo ratings yet

- Chapter 5 - A2, B1, & 59Document5 pagesChapter 5 - A2, B1, & 59詹鎮豪No ratings yet

- KELOMPOK 8 - Business Plan Part 1 (Dragged) 2Document3 pagesKELOMPOK 8 - Business Plan Part 1 (Dragged) 2Salsabila AufaNo ratings yet

- Black and Red Geometric Technology Keynote PresentationDocument15 pagesBlack and Red Geometric Technology Keynote PresentationSalsabila AufaNo ratings yet

- 06 - Time Value of Money - 2Document77 pages06 - Time Value of Money - 2Salsabila AufaNo ratings yet

- 10-00-ENG - Stock ValuationDocument38 pages10-00-ENG - Stock ValuationSalsabila AufaNo ratings yet

- 07-01 - An Introduction To Risk and ReturnDocument69 pages07-01 - An Introduction To Risk and ReturnSalsabila AufaNo ratings yet

- 04-01 - Financial Analysis (Dragged) 31Document3 pages04-01 - Financial Analysis (Dragged) 31Salsabila AufaNo ratings yet

- 04-01 - Financial Analysis (Dragged) 20Document3 pages04-01 - Financial Analysis (Dragged) 20Salsabila AufaNo ratings yet

- 04-01 - Financial Analysis (Dragged) 4Document3 pages04-01 - Financial Analysis (Dragged) 4Salsabila AufaNo ratings yet

- 04-01 - Financial Analysis (Dragged) 26Document3 pages04-01 - Financial Analysis (Dragged) 26Salsabila AufaNo ratings yet

- 04-01 - Financial Analysis (Dragged) 15Document3 pages04-01 - Financial Analysis (Dragged) 15Salsabila AufaNo ratings yet

- 04-01 - Financial Analysis (Dragged) 14Document3 pages04-01 - Financial Analysis (Dragged) 14Salsabila AufaNo ratings yet

- 04-01 - Financial Analysis (Dragged) 8Document3 pages04-01 - Financial Analysis (Dragged) 8Salsabila AufaNo ratings yet

- 04-01 - Financial Analysis (Dragged) 19Document3 pages04-01 - Financial Analysis (Dragged) 19Salsabila AufaNo ratings yet

- 04-01 - Financial Analysis (Dragged) 9Document3 pages04-01 - Financial Analysis (Dragged) 9Salsabila AufaNo ratings yet

- 04-01 - Financial Analysis (Dragged) 16Document3 pages04-01 - Financial Analysis (Dragged) 16Salsabila AufaNo ratings yet

- 04-01 - Financial Analysis (Dragged) 18Document3 pages04-01 - Financial Analysis (Dragged) 18Salsabila AufaNo ratings yet

- 04-01 - Financial AnalysisDocument98 pages04-01 - Financial AnalysisSalsabila AufaNo ratings yet

- 04-01 - Financial Analysis (Dragged) 11Document6 pages04-01 - Financial Analysis (Dragged) 11Salsabila AufaNo ratings yet

- B. Intro To Business ValuationDocument4 pagesB. Intro To Business ValuationSalsabila AufaNo ratings yet

- Latihan UAS Soal 01Document3 pagesLatihan UAS Soal 01Salsabila AufaNo ratings yet

- Ass 10 01aDocument1 pageAss 10 01aSalsabila AufaNo ratings yet

- Assignment Week 1 - CHDocument2 pagesAssignment Week 1 - CHSalsabila AufaNo ratings yet

- Ass 10 03BDocument1 pageAss 10 03BSalsabila AufaNo ratings yet

- Ass 10 02DDocument2 pagesAss 10 02DSalsabila AufaNo ratings yet

- Ass 10 02CDocument1 pageAss 10 02CSalsabila AufaNo ratings yet

- Pricing Determination Perfect Competition: Dr. Vijay Kumar GuptaDocument5 pagesPricing Determination Perfect Competition: Dr. Vijay Kumar GuptaNnaemeka UMEH Christian DanielNo ratings yet

- General Conditions For The Supply and Installation of Mechanical, Electrical and Electronic ProductsDocument8 pagesGeneral Conditions For The Supply and Installation of Mechanical, Electrical and Electronic ProductsЯрослав ДронинNo ratings yet

- Bill of Sale (Motorcycle)Document2 pagesBill of Sale (Motorcycle)bradley omariNo ratings yet

- Real Estate NotesDocument8 pagesReal Estate NotesSteven ElsingaNo ratings yet

- Term Paper Business FinanceDocument31 pagesTerm Paper Business FinanceJodi LegpitanNo ratings yet

- Basic FinanceDocument23 pagesBasic FinanceGessille SalavariaNo ratings yet

- Nabus Vs PacsonDocument8 pagesNabus Vs PacsonGladys BantilanNo ratings yet

- CH 15 Inventory ManagementDocument21 pagesCH 15 Inventory ManagementAshwin MishraNo ratings yet

- Sandeep Garg Solutions Class 12 - Chapter 4Document4 pagesSandeep Garg Solutions Class 12 - Chapter 4Manshika LakhmaniNo ratings yet

- (비밀노트 (edu-lab.kr) ) 24대비 - 수특영어 05강 - 차별화된 최종찍기 - 통합 - OK - FDocument29 pages(비밀노트 (edu-lab.kr) ) 24대비 - 수특영어 05강 - 차별화된 최종찍기 - 통합 - OK - FᄋᄋNo ratings yet

- Lecture 2 A - Contracts Project Delivery Methods-Canadian FormsDocument38 pagesLecture 2 A - Contracts Project Delivery Methods-Canadian FormsKeyvan HajjarizadehNo ratings yet

- Quiz 1 - IPF 2022Document5 pagesQuiz 1 - IPF 2022Kunal MondalNo ratings yet

- Regional Science High School For Region 02: Camp Samal, Arcon, Tumauini, Isabela 3325Document28 pagesRegional Science High School For Region 02: Camp Samal, Arcon, Tumauini, Isabela 3325Niña MogarteNo ratings yet

- SDM Cases HighlightedDocument33 pagesSDM Cases HighlightedRoshan HmNo ratings yet

- Price Ceilings and Price FloorsDocument28 pagesPrice Ceilings and Price FloorsKRISP ABEARNo ratings yet

- CH.09.Job&Contract CostDocument38 pagesCH.09.Job&Contract CostRohit AgarwalNo ratings yet

- Quantitative Strategic AnalysisDocument16 pagesQuantitative Strategic AnalysisBlaine Bateman, EAF LLCNo ratings yet

- Customs IntroductionDocument62 pagesCustoms IntroductionJitendra VernekarNo ratings yet

- EbayDocument81 pagesEbayJohnny ChanNo ratings yet

- Surabaya Property Market Report: Colliers Half Year Report H1 2018 20 September 2018Document22 pagesSurabaya Property Market Report: Colliers Half Year Report H1 2018 20 September 2018anthony csNo ratings yet

- MBF and I2b NotesDocument100 pagesMBF and I2b NotesMKALl100% (1)

- Elton John Demetita - Unit II Activity 2 Business Ethical CasesDocument6 pagesElton John Demetita - Unit II Activity 2 Business Ethical CasesLaiven Ryle100% (1)

- As Short Revision Notes BusinessDocument31 pagesAs Short Revision Notes BusinessAbu BakarNo ratings yet

- Man TparDocument10 pagesMan TparFrederick GbliNo ratings yet

- Jose S Authentic Mexican Restaurant Case StudyDocument30 pagesJose S Authentic Mexican Restaurant Case StudyPrakash PrakashNo ratings yet

- Strama PaperDocument35 pagesStrama PaperHavanaNo ratings yet

- What Is Toyota Financial ServicesDocument3 pagesWhat Is Toyota Financial ServicesSaurabh TyagiNo ratings yet

- Chapter Eight: Using Financial Futures, Options, Swaps, and Other Hedging Tools in Asset-Liability ManagementDocument45 pagesChapter Eight: Using Financial Futures, Options, Swaps, and Other Hedging Tools in Asset-Liability Managementশাহরিয়ার মৃধাNo ratings yet