Download as pdf or txt

You might also like

- Money Send TC28Document9 pagesMoney Send TC28Ahmed AlhunaishieNo ratings yet

- Ace Banking and Static GKDocument210 pagesAce Banking and Static GKOu71% (7)

- Barclays MT199Document2 pagesBarclays MT199Cash monkey100% (1)

- TIA 2/FM Seminar A.1 ProblemsDocument23 pagesTIA 2/FM Seminar A.1 ProblemsPrisco SayNo ratings yet

- Affidavit of Conformity (TPM)Document1 pageAffidavit of Conformity (TPM)ellirehcNo ratings yet

- Termination of Bank-Customer RelationshipDocument5 pagesTermination of Bank-Customer Relationshipmuggzp100% (1)

- Federal Reserve System: Board of GovernorsDocument28 pagesFederal Reserve System: Board of GovernorsAdam DeutschNo ratings yet

- Kashif PresentationDocument18 pagesKashif PresentationM KashifNo ratings yet

- 230 Kashif PresentationDocument18 pages230 Kashif PresentationMuhammad KashifNo ratings yet

- PRACTICE of BANKING LECTURE NOTES 4 - Cessation of Banker Customer RelationshipDocument50 pagesPRACTICE of BANKING LECTURE NOTES 4 - Cessation of Banker Customer RelationshipGaniyu TaslimNo ratings yet

- Termination of Contract by A BankDocument6 pagesTermination of Contract by A Bankkmeshack100% (11)

- CHAPTER 5 Determination of Banker Customer ContractDocument12 pagesCHAPTER 5 Determination of Banker Customer ContractCarl AbruquahNo ratings yet

- BankingDocument4 pagesBankinglukyamuzinicodemus32No ratings yet

- Bank Duties and RightsDocument6 pagesBank Duties and RightsSthita Prajna Mohanty100% (1)

- Banker Customer RelationshipDocument7 pagesBanker Customer RelationshipJitendra VirahyasNo ratings yet

- Assignment Banking Law, Shubham Singh Kirar IX Sem, BBALLBDocument7 pagesAssignment Banking Law, Shubham Singh Kirar IX Sem, BBALLBShubham Singh KirarNo ratings yet

- Bankerandcustomerrelationship 161127170639Document25 pagesBankerandcustomerrelationship 161127170639M KashifNo ratings yet

- Terms and Conditions: Mudaraba AgreementDocument10 pagesTerms and Conditions: Mudaraba AgreementchandraNo ratings yet

- Banker CustomerDocument4 pagesBanker CustomerM KashifNo ratings yet

- The Rights of The Banker IncludeDocument5 pagesThe Rights of The Banker Includem_dattaias67% (3)

- Terms ConditionDocument3 pagesTerms ConditionctgmainulNo ratings yet

- Unit 2 Paying and Collecting Banker NotesDocument11 pagesUnit 2 Paying and Collecting Banker NotesShreekanth GuttedarNo ratings yet

- Rights and Obligations of Banker and CustomerDocument12 pagesRights and Obligations of Banker and Customerbeena antu100% (1)

- Right and Liabilities of Paying and Collecting BankersDocument3 pagesRight and Liabilities of Paying and Collecting BankersAtul KansalNo ratings yet

- Banking LawDocument12 pagesBanking LawArockia AmalanNo ratings yet

- Chapter-3: Relationship Between Banker and CustomerDocument7 pagesChapter-3: Relationship Between Banker and Customerhasan alNo ratings yet

- Banker Customer RelationshipDocument30 pagesBanker Customer RelationshipUtkarsh LodhiNo ratings yet

- Banker's Lien: in The Creditor and Debtor Relationship Between The Banker andDocument30 pagesBanker's Lien: in The Creditor and Debtor Relationship Between The Banker andzviyedzo chimwaraNo ratings yet

- Rights and Obligations of BankerDocument3 pagesRights and Obligations of BankerMoinuddin Khan Kafi100% (1)

- 541 BL 4docxDocument3 pages541 BL 4docxQAISER WASEEQNo ratings yet

- Banker Customer RelationshipDocument11 pagesBanker Customer Relationshipgaurav gharatNo ratings yet

- Banking Chapter FourDocument13 pagesBanking Chapter FourfikremariamNo ratings yet

- Banking Law and ProceduresDocument114 pagesBanking Law and ProceduresmonaeNo ratings yet

- Right Under Garnishee OrderDocument16 pagesRight Under Garnishee OrderTeja RaviNo ratings yet

- Banking 2Document13 pagesBanking 2Abhishek SharmaNo ratings yet

- T&C Book June 2021Document24 pagesT&C Book June 20210iamkaran0No ratings yet

- Bulletin 3 Closure of Bank Accounts Final 30.01.2018Document6 pagesBulletin 3 Closure of Bank Accounts Final 30.01.2018Tahir DestaNo ratings yet

- Questions and Answers:: A Banker Customer CanDocument14 pagesQuestions and Answers:: A Banker Customer CanKhaleda AkhterNo ratings yet

- Paying and Collecting BankerDocument12 pagesPaying and Collecting BankerartiNo ratings yet

- Banking Law & PracticeDocument12 pagesBanking Law & PracticeShams TabrezNo ratings yet

- Chapter IV 1Document20 pagesChapter IV 1muluNo ratings yet

- MBF-Banker Customer RelationshipDocument20 pagesMBF-Banker Customer Relationshipsagarg94gmailcomNo ratings yet

- TPB - Module 4 - Reference MaterialDocument8 pagesTPB - Module 4 - Reference MaterialSupreethaNo ratings yet

- RB Chapter 2A-Current Account-MITCDocument9 pagesRB Chapter 2A-Current Account-MITCRohit KumarNo ratings yet

- Termination of The Relationship Between A Banker and A CustomerDocument1 pageTermination of The Relationship Between A Banker and A CustomerEkta YendeNo ratings yet

- Unit - 2: Group Members Srilekha Ujjwal Kunal Kumar Honey Tyagi Roshan Gautam Soumyadeep DasDocument27 pagesUnit - 2: Group Members Srilekha Ujjwal Kunal Kumar Honey Tyagi Roshan Gautam Soumyadeep DasNithyananda PatelNo ratings yet

- Banker CustomerDocument38 pagesBanker CustomerUmer ChaudharyNo ratings yet

- Banker and Customer Relationship PDFDocument25 pagesBanker and Customer Relationship PDFaaditya01No ratings yet

- Assignment On Bankinkg LawDocument14 pagesAssignment On Bankinkg LawrajaramNo ratings yet

- ChequeDocument15 pagesChequesagarg94gmailcomNo ratings yet

- Paying BankerDocument2 pagesPaying BankerwubeNo ratings yet

- Meaning of Banker and Customer Meaning of Banker and CustomerDocument14 pagesMeaning of Banker and Customer Meaning of Banker and CustomerSaiful IslamNo ratings yet

- Meaning of Bank: A Bank Is An Institution, Incorporated With The Authority and The Responsibility ToDocument18 pagesMeaning of Bank: A Bank Is An Institution, Incorporated With The Authority and The Responsibility To657 Suleman Khan100% (1)

- Paying Banker and Collecting Banker (Duties and Responsibility)Document4 pagesPaying Banker and Collecting Banker (Duties and Responsibility)donbaba100% (1)

- Legal Aspects of Opening & Operation of Different Types of ACDocument14 pagesLegal Aspects of Opening & Operation of Different Types of ACNazirul IslamNo ratings yet

- Rights and ObligationsDocument5 pagesRights and ObligationsAmace Placement KanchipuramNo ratings yet

- Module 3 Topic 2 Rights, Duties & Obligations of BankDocument4 pagesModule 3 Topic 2 Rights, Duties & Obligations of Banksarthak chaturvediNo ratings yet

- Banking CH 4 Relationship Between Banker and Customer-1Document9 pagesBanking CH 4 Relationship Between Banker and Customer-1AbiyNo ratings yet

- Terms and Conditions For HBL Conventional AccountsDocument2 pagesTerms and Conditions For HBL Conventional Accountsfaisal_ahsan7919No ratings yet

- Islamic RDA - Terms and ConditionsDocument6 pagesIslamic RDA - Terms and ConditionsMahnoor AnisNo ratings yet

- Account Opening TandCs - Islamic Banking FinalDocument10 pagesAccount Opening TandCs - Islamic Banking FinalWaqar MishwaniNo ratings yet

- Chapter Four The Bank - Customer RelashinshipDocument11 pagesChapter Four The Bank - Customer RelashinshipNigus MollaNo ratings yet

- Agent Banking Uganda Handbook: A simple guide to starting and running a profitable agent banking business in UgandaFrom EverandAgent Banking Uganda Handbook: A simple guide to starting and running a profitable agent banking business in UgandaNo ratings yet

- Statement - 2014 06 05Document4 pagesStatement - 2014 06 05Sebastian WatersNo ratings yet

- L-5&6 642 ReserveDocument44 pagesL-5&6 642 ReserveNiloy AhmedNo ratings yet

- EximDocument3 pagesEximHabibullah ForkanNo ratings yet

- Big Bazar BillDocument2 pagesBig Bazar Billvilge rogesonNo ratings yet

- Business Research Methods ReportDocument5 pagesBusiness Research Methods Reportvijay choudhariNo ratings yet

- Cashless Economy: Merits and DemeritsDocument23 pagesCashless Economy: Merits and DemeritsHarshit VermaNo ratings yet

- Case Study: Commitment To A Fixed Exchange Rate Regime: Key QuestionsDocument3 pagesCase Study: Commitment To A Fixed Exchange Rate Regime: Key QuestionskarmenNo ratings yet

- Accounting Test Bank 4Document5 pagesAccounting Test Bank 4likesNo ratings yet

- El Llano en Llamas - de Juan RulfoDocument26 pagesEl Llano en Llamas - de Juan RulfoRAUL LASES ZAYASNo ratings yet

- Mapping of ICRA's Long-Term and Short-Term RatingsDocument3 pagesMapping of ICRA's Long-Term and Short-Term RatingsmaheshNo ratings yet

- A History of BankingDocument3 pagesA History of BankinglengocthangNo ratings yet

- BOG Notice No. BG GOV SEC 2021 13 Requirement To Paticipate in The Credit Reporting SystemDocument2 pagesBOG Notice No. BG GOV SEC 2021 13 Requirement To Paticipate in The Credit Reporting SystemFuaad DodooNo ratings yet

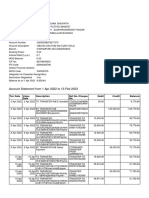

- Account Statement: Date Value Date Description Cheque Deposit Withdrawal BalanceDocument42 pagesAccount Statement: Date Value Date Description Cheque Deposit Withdrawal Balanceyashyuvjitconsultancies331No ratings yet

- Account StatementDocument1 pageAccount Statementsarahjawad125No ratings yet

- Unclaimed BalancesDocument4 pagesUnclaimed BalancesCatherine Joy MoralesNo ratings yet

- CBDC For Commercial Banks - Part 2Document5 pagesCBDC For Commercial Banks - Part 2amul_muthaNo ratings yet

- Jamia Millia Islamia: Mortgage of Immovable PropertyDocument18 pagesJamia Millia Islamia: Mortgage of Immovable PropertyHritikka KakNo ratings yet

- MP Manulife ADA Retry FormDocument1 pageMP Manulife ADA Retry FormRhuejane Gay Maquiling0% (1)

- CZG GC EGl Qa 6 XW Co XDocument6 pagesCZG GC EGl Qa 6 XW Co XvenkatNo ratings yet

- ABA Bank: Garcia, Renz Xavier Vinluan, Jan Danniel Bañares, Zcyrelle Yvonne Salazar, Diana Mae Torres, Mhariecar AubreyDocument9 pagesABA Bank: Garcia, Renz Xavier Vinluan, Jan Danniel Bañares, Zcyrelle Yvonne Salazar, Diana Mae Torres, Mhariecar AubreyRichard Rhamil Carganillo Garcia Jr.No ratings yet

- Q4 NUP - Promo Mechanics - 1004 (Final)Document4 pagesQ4 NUP - Promo Mechanics - 1004 (Final)Lyht TVNo ratings yet

- What Is An RFC Savings Account? Why Choose An RFC Savings Account?Document6 pagesWhat Is An RFC Savings Account? Why Choose An RFC Savings Account?Prachikarambelkar100% (1)

- Netwrokers Home Education Loan FacilitiesDocument2 pagesNetwrokers Home Education Loan Facilitiessk64232No ratings yet

- Estmt - 2023 10 19Document6 pagesEstmt - 2023 10 19lucasortegabrandonarturo24No ratings yet