Download as pdf or txt

You might also like

- Ibc ChartsDocument7 pagesIbc Chartspiyush bansalNo ratings yet

- Ey The Insolvency and Bankruptcy Code 2016 An Overview PDFDocument6 pagesEy The Insolvency and Bankruptcy Code 2016 An Overview PDFRaghav DhootNo ratings yet

- IBC, 2016 (1-20 PG)Document20 pagesIBC, 2016 (1-20 PG)C.A Dhwanik ShahNo ratings yet

- Crypto Project Final Report - 1Document49 pagesCrypto Project Final Report - 1Deepak GowdaNo ratings yet

- BT Raport Anual Pe 2017 Asf December 2017Document41 pagesBT Raport Anual Pe 2017 Asf December 2017Amilia MarinNo ratings yet

- Pre-Post IBC-tableDocument4 pagesPre-Post IBC-tableChristina ShajuNo ratings yet

- IBC and BanksDocument23 pagesIBC and BanksAnonymous VFyoCxNo ratings yet

- Assignment 2 Insolvency and Bankruptcy CodeDocument3 pagesAssignment 2 Insolvency and Bankruptcy CodePratyush BaruaNo ratings yet

- Company Law PresentationDocument25 pagesCompany Law PresentationAnu kushwahaNo ratings yet

- IBC Chap 2Document28 pagesIBC Chap 2Chilapalli SaikiranNo ratings yet

- Pre Pack IBCDocument9 pagesPre Pack IBCNARENRSHARMANo ratings yet

- IBC Notes Part 1 by CA Vivek GabaDocument309 pagesIBC Notes Part 1 by CA Vivek Gabamadaanakansha91No ratings yet

- Can Pre-Packaged Insolvency Resolution Process For MSMEs Prove To Be A Game ChangerDocument2 pagesCan Pre-Packaged Insolvency Resolution Process For MSMEs Prove To Be A Game ChangerRomit ChandrakarNo ratings yet

- Demystifying The Insolvency and Bankruptcy CodeDocument23 pagesDemystifying The Insolvency and Bankruptcy Codedevashish taranekarNo ratings yet

- Analyzing The Viability of Pre-Packaged Insolvency Scheme in India - Saransh AwasthiDocument4 pagesAnalyzing The Viability of Pre-Packaged Insolvency Scheme in India - Saransh AwasthiSaransh AwasthiNo ratings yet

- IBC CodeDocument51 pagesIBC Coderajni agarwalNo ratings yet

- IbcDocument62 pagesIbcpankaj vermaNo ratings yet

- Value Addition Notes - Indian EconomyDocument6 pagesValue Addition Notes - Indian Economynikitash1222No ratings yet

- PPIRP (Pre Packaged Insolvency Resolution Process)Document14 pagesPPIRP (Pre Packaged Insolvency Resolution Process)Bhama AbhayNo ratings yet

- Evolving Landscape of Corporate Stress ResolutionDocument68 pagesEvolving Landscape of Corporate Stress ResolutiongowthampkfNo ratings yet

- Corporate Insolvency Resolution Procedure Under Indian Insolvency and Bankruptcy Code, 2016: A Comparative PerspectiveDocument8 pagesCorporate Insolvency Resolution Procedure Under Indian Insolvency and Bankruptcy Code, 2016: A Comparative PerspectiveDeva SharmaNo ratings yet

- IBC - FinalDocument79 pagesIBC - FinalTUSHAR SHERMALENo ratings yet

- Ias 12-12-19 PDFDocument19 pagesIas 12-12-19 PDFsamNo ratings yet

- EY IBC ReportDocument40 pagesEY IBC ReportShushrut KhannaNo ratings yet

- Women's Rights Are Human RightsDocument7 pagesWomen's Rights Are Human Rightstanmaya_purohitNo ratings yet

- Ibc 2016Document74 pagesIbc 2016Roshini Chinnappa100% (1)

- SSRN Id4706605Document13 pagesSSRN Id4706605Hitesh JethwaNo ratings yet

- Writing SampleDocument10 pagesWriting SampleV NITYANAND 1950137No ratings yet

- IBC - Paradigm Shift From 'Debtor-In-Possession' To 'Creditor-In-Control'Document7 pagesIBC - Paradigm Shift From 'Debtor-In-Possession' To 'Creditor-In-Control'Jai SoniNo ratings yet

- EÝ S Report On IBC's Journey and Next Phase of ReformsDocument64 pagesEÝ S Report On IBC's Journey and Next Phase of ReformsamolrNo ratings yet

- Resolution of NPA and Insolvency and Bankruptcy Code, 2016Document7 pagesResolution of NPA and Insolvency and Bankruptcy Code, 2016AkashNo ratings yet

- Insolvency Law FinalDocument19 pagesInsolvency Law FinalISHAN SINGHNo ratings yet

- A Resolve For ResolutionDocument18 pagesA Resolve For ResolutionSuraj KumarNo ratings yet

- Ibc FinalsDocument51 pagesIbc FinalsMALKANI DISHA DEEPAKNo ratings yet

- Concept of Insolvency and Bankruptcy: The IBC, 2016Document82 pagesConcept of Insolvency and Bankruptcy: The IBC, 2016Gautham ReddyNo ratings yet

- Insolvency and Bankruptcy Code of India: The Past, The Present and The FutureDocument11 pagesInsolvency and Bankruptcy Code of India: The Past, The Present and The FutureAdv Gaurav KhondNo ratings yet

- Essar Steel IBC Article - IBA Journal ADocument7 pagesEssar Steel IBC Article - IBA Journal ASakthi NathanNo ratings yet

- Insolvency and Bankruptcy CODE 2016 Regulatory Framework For Distressed M&As Under IBC 2016Document60 pagesInsolvency and Bankruptcy CODE 2016 Regulatory Framework For Distressed M&As Under IBC 2016IIM RohtakNo ratings yet

- The Insolvency and Bankruptcy Code, 2016: Erstwhile Legislative Framework New FrameworkDocument4 pagesThe Insolvency and Bankruptcy Code, 2016: Erstwhile Legislative Framework New FrameworkGyan PrakashNo ratings yet

- CCRA Session 19Document19 pagesCCRA Session 19VISHAL PATILNo ratings yet

- IBC Amendment Bill 2021 UPSC NotesDocument5 pagesIBC Amendment Bill 2021 UPSC NotesAvik PodderNo ratings yet

- Ey The Insolvency and Bankruptcy CodeDocument28 pagesEy The Insolvency and Bankruptcy CodeAnkita AggarwalNo ratings yet

- Report of The Working Group On Tracking Outcomes Under The Insolvency and Bankruptcy Code, 2016Document26 pagesReport of The Working Group On Tracking Outcomes Under The Insolvency and Bankruptcy Code, 2016SagarNo ratings yet

- TLP IBC Briefing Document - Compressed PDFDocument27 pagesTLP IBC Briefing Document - Compressed PDFPratik BakshiNo ratings yet

- COmpany LAw-1Document11 pagesCOmpany LAw-1Suruchi SinghNo ratings yet

- Insolvency and Bankruptcy CodeDocument27 pagesInsolvency and Bankruptcy Codeshivam_2607No ratings yet

- IBCDocument47 pagesIBCAmbuj JainNo ratings yet

- Insolvency and Bankruptcy Code (Amendment Bill), 2021: Why in NewsDocument4 pagesInsolvency and Bankruptcy Code (Amendment Bill), 2021: Why in NewsMehak KaushikkNo ratings yet

- Ibc, 2016Document24 pagesIbc, 2016Ekta ChaudharyNo ratings yet

- Future of Indian Banking The Road Ahead 17 23Document7 pagesFuture of Indian Banking The Road Ahead 17 23kamaiiiNo ratings yet

- Pre-Pack Insolvency Resolution Process: A Critical AnalysisDocument20 pagesPre-Pack Insolvency Resolution Process: A Critical AnalysisShivani SrivastavaNo ratings yet

- Article On Debt Recovery Tribunal - FinalDocument6 pagesArticle On Debt Recovery Tribunal - Finalvasantharao venkataraoNo ratings yet

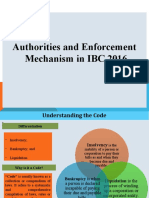

- Authorities and Enforcement Mechanism in IBC 2016Document16 pagesAuthorities and Enforcement Mechanism in IBC 2016SNEHA SOLANKI0% (1)

- 72236cajournal Dec2022 3Document1 page72236cajournal Dec2022 3SUBHASISH AGRAWALNo ratings yet

- ICMA 30 MarchDocument50 pagesICMA 30 MarchNusrat ShatyNo ratings yet

- CFD - Financial - Distress Bankruptcy Process FinalDocument14 pagesCFD - Financial - Distress Bankruptcy Process Finalsuparshva99iimNo ratings yet

- RBI Governor On IBCDocument15 pagesRBI Governor On IBCyashs-pgdm-2022-24No ratings yet

- Essay 2019Document10 pagesEssay 2019Tushar KumarNo ratings yet

- Project ReportDocument31 pagesProject ReportDiksha ChhabraNo ratings yet

- THE IBC, 2016 SymbiosisDocument35 pagesTHE IBC, 2016 SymbiosisNavya TomerNo ratings yet

- Insolveny and Bankruptcy CodeDocument4 pagesInsolveny and Bankruptcy CodeSING ALONGNo ratings yet

- Bank Account StatementDocument1 pageBank Account Statement739589asdalkom.liveNo ratings yet

- Solved William Rubin President of Tri State Mining Co Sought A LoanDocument1 pageSolved William Rubin President of Tri State Mining Co Sought A LoanAnbu jaromiaNo ratings yet

- Module 4 - 7 - Different Ways of Calculating WACCDocument10 pagesModule 4 - 7 - Different Ways of Calculating WACCBaher WilliamNo ratings yet

- Regional Stock ExchangeDocument26 pagesRegional Stock ExchangeChandrika DasNo ratings yet

- New-Bank DAO TemplateDocument4 pagesNew-Bank DAO TemplateHarish MylatNo ratings yet

- Final ProposalDocument6 pagesFinal ProposalSanam_Sam_273780% (10)

- Redemption OF Debentures: After Studying This Unit, You Will Be Able ToDocument36 pagesRedemption OF Debentures: After Studying This Unit, You Will Be Able ToAkansha GuptaNo ratings yet

- Chapter 1 - International Financial Markets & MNCsDocument97 pagesChapter 1 - International Financial Markets & MNCsDung VươngNo ratings yet

- 7 Secrets of Eternal WealthDocument52 pages7 Secrets of Eternal WealthdhruvNo ratings yet

- Medical Repricing 95925429Document10 pagesMedical Repricing 95925429Jason MaldonadoNo ratings yet

- FbsDocument10 pagesFbsPrince Matthew NatanawanNo ratings yet

- Sma CertificateDocument2 pagesSma CertificateAnil MishraNo ratings yet

- TylerBD 2017 TVMCaseStudy MainDocDocument21 pagesTylerBD 2017 TVMCaseStudy MainDocAndro HutabaratNo ratings yet

- Class XII Acc PB HC Mock 2021-22Document15 pagesClass XII Acc PB HC Mock 2021-22Satinder SandhuNo ratings yet

- 2 - International Parity ConditionsDocument116 pages2 - International Parity ConditionsMUKESH KUMARNo ratings yet

- Foreign Exchange 111Document10 pagesForeign Exchange 111CHRISTIAN PAUL ALPECHENo ratings yet

- Reference: Financial Accounting - 2 by Conrado T. Valix and Christian ValixDocument2 pagesReference: Financial Accounting - 2 by Conrado T. Valix and Christian ValixMie CuarteroNo ratings yet

- BD5 SM12Document10 pagesBD5 SM12didiajaNo ratings yet

- Acc 291 Acc 291 Acc 291 Acc 291 Acc 291 Acc 291Document201 pagesAcc 291 Acc 291 Acc 291 Acc 291 Acc 291 Acc 291290acc100% (2)

- Iceland Foods RecommendationDocument2 pagesIceland Foods Recommendationccohen6410No ratings yet

- Financial Management Research Paper Financial Ratios of BritanniaDocument15 pagesFinancial Management Research Paper Financial Ratios of BritanniaShaik Noor Mohammed Ali Jinnah 19DBLAW036No ratings yet

- Project Allotment SheetDocument20 pagesProject Allotment SheetRoushan RajNo ratings yet

- ACCTG 221 Final Exam Part 1Document6 pagesACCTG 221 Final Exam Part 1Get BurnNo ratings yet

- Monetary Policy and Central Banking - Finance 7 SyllabusDocument9 pagesMonetary Policy and Central Banking - Finance 7 SyllabusMarjon DimafilisNo ratings yet

- AmericanExpressCompany 10K 20120224Document306 pagesAmericanExpressCompany 10K 20120224technoxplorer100% (1)

- Tybms Sem5 RM Nov19Document2 pagesTybms Sem5 RM Nov19Kritika SinghNo ratings yet

- FF Full Eng PDFDocument146 pagesFF Full Eng PDFAnonymous YgBIdKxvNo ratings yet

- Gisela Huyssen vs. Atty. Fred L. GutierrezDocument5 pagesGisela Huyssen vs. Atty. Fred L. GutierrezAdhara CelerianNo ratings yet