Download as pdf or txt

You might also like

- Littlefield SimulationDocument4 pagesLittlefield Simulationzilikos100% (5)

- BIO102 Practice ExamDocument10 pagesBIO102 Practice ExamKathy YuNo ratings yet

- Petty Cash TestDocument6 pagesPetty Cash TestEhsan Elahi100% (4)

- Oberon 1Document321 pagesOberon 1Grandfather NurgleNo ratings yet

- Latihan Acca v02Document17 pagesLatihan Acca v02Indriyanti KrisdianaNo ratings yet

- Latihan1 Chapter 8-CashDocument2 pagesLatihan1 Chapter 8-CashAgatha MisyelNo ratings yet

- CM 03 Bank ReconciliationDocument7 pagesCM 03 Bank ReconciliationDanicaEsponilla67% (3)

- The Cash BookDocument8 pagesThe Cash BookbritsomaxmillianNo ratings yet

- Cambridge O Level: Accounting 7707/13Document12 pagesCambridge O Level: Accounting 7707/13hafak27227No ratings yet

- Cambridge IGCSE: Accounting 0452/13Document12 pagesCambridge IGCSE: Accounting 0452/13grengtaNo ratings yet

- The Cash Book Grade 11 Business Prepare By: Ms PercivalDocument6 pagesThe Cash Book Grade 11 Business Prepare By: Ms PercivalDenishNo ratings yet

- 10 BANK RECONCILIATIONS (Questions)Document22 pages10 BANK RECONCILIATIONS (Questions)Zeeshan BakaliNo ratings yet

- 0452 w23 QP 11 PDFDocument11 pages0452 w23 QP 11 PDFmixgamer5555No ratings yet

- Chapter 8Document26 pagesChapter 8ENG ZI QINGNo ratings yet

- Activity 4 Bank Reconciliation: Multiple Choice: TheoriesDocument4 pagesActivity 4 Bank Reconciliation: Multiple Choice: TheoriesKrissa Mae Longos100% (1)

- Chapter 5Document5 pagesChapter 5Abrha636No ratings yet

- Activity 4 Bank Reconciliation PDFDocument4 pagesActivity 4 Bank Reconciliation PDFSharmin ReulaNo ratings yet

- Accounting For Cash and ReceivableDocument7 pagesAccounting For Cash and ReceivableAbrha GidayNo ratings yet

- BOOKKEEPING-Petty Cash BookDocument8 pagesBOOKKEEPING-Petty Cash Bookjosephinemusopelo1No ratings yet

- CH 08Document4 pagesCH 08flrnciairnNo ratings yet

- Audit of Cash and Cash Equivalents BA 123 Exercise Set: Kevin Durant (Petty Cash)Document10 pagesAudit of Cash and Cash Equivalents BA 123 Exercise Set: Kevin Durant (Petty Cash)Becky GonzagaNo ratings yet

- Chapter 7 Question Review PDFDocument12 pagesChapter 7 Question Review PDFChit ComisoNo ratings yet

- Stern CorporationsDocument30 pagesStern CorporationsShubham MallikNo ratings yet

- ch08 PDFDocument4 pagesch08 PDFRabie HarounNo ratings yet

- Current JSS 2 BUSINESS STUDIES 3RD TERMDocument34 pagesCurrent JSS 2 BUSINESS STUDIES 3RD TERMpalmer okiemuteNo ratings yet

- Lesson Notes On Cash Book Nov 2023Document6 pagesLesson Notes On Cash Book Nov 2023kxngdawkinz20No ratings yet

- ScriptDocument4 pagesScriptSophia Anne MonillasNo ratings yet

- Cash Book Bank ColumnBank StatementDocument6 pagesCash Book Bank ColumnBank StatementShaikh Ghassan AbidNo ratings yet

- Screenshot 2022-10-29 at 5.34.32 PMDocument56 pagesScreenshot 2022-10-29 at 5.34.32 PMrose williamsNo ratings yet

- Accounting Monthly TestDocument7 pagesAccounting Monthly TestSeyyad Refai Hawana MaryamNo ratings yet

- Control Account NotesDocument2 pagesControl Account NotesNipuni PereraNo ratings yet

- Cash - CRDocument14 pagesCash - CRpingu patwhoNo ratings yet

- Accounting For Petty Cash: ExampleDocument2 pagesAccounting For Petty Cash: Exampleheynuhh gNo ratings yet

- S3 MYE QP 2019-20 (Final)Document13 pagesS3 MYE QP 2019-20 (Final)XinYi ChenNo ratings yet

- Accounting Chapter 22 Test: True/FalseDocument3 pagesAccounting Chapter 22 Test: True/FalseZayli Morales100% (1)

- The Quilt Shop Deposits All Receipts in The Bank Each: Unlock Answers Here Solutiondone - OnlineDocument1 pageThe Quilt Shop Deposits All Receipts in The Bank Each: Unlock Answers Here Solutiondone - Onlinetrilocksp SinghNo ratings yet

- Fa2 PilotDocument16 pagesFa2 PilotBhuiyan Mohammad Iftekhar100% (2)

- Books of Original Entry (Cont)Document16 pagesBooks of Original Entry (Cont)mahmoud abdallahNo ratings yet

- Handout 7.studentDocument6 pagesHandout 7.studentVikrant KapoorNo ratings yet

- Cash and Cash Equivalent HandoutsDocument6 pagesCash and Cash Equivalent HandoutsMichael BongalontaNo ratings yet

- Bank ReconciliationDocument64 pagesBank ReconciliationmarkjohnmagcalengNo ratings yet

- 3 Cash - Assignment PDFDocument6 pages3 Cash - Assignment PDFCatherine RiveraNo ratings yet

- ACC101 Chapter6newxcxDocument18 pagesACC101 Chapter6newxcxAhmed RawyNo ratings yet

- Cash Book and Bank Reconciliation Lecture IDocument10 pagesCash Book and Bank Reconciliation Lecture IDavidNo ratings yet

- 2-Ch8-Internal Control and Cash PDFDocument11 pages2-Ch8-Internal Control and Cash PDFw85rt9wmqnNo ratings yet

- V - Substantive Audit of CashDocument7 pagesV - Substantive Audit of CashVan MateoNo ratings yet

- Chapter 5 - Cash Book & Bank ReconciliationsDocument6 pagesChapter 5 - Cash Book & Bank ReconciliationskundiarshdeepNo ratings yet

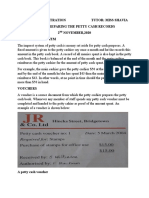

- Office Administration Tutor: Miss Shavia Topic: Preparing The Petty Cash Records 2 NOVEMBER, 2020 The Imprest SystemDocument5 pagesOffice Administration Tutor: Miss Shavia Topic: Preparing The Petty Cash Records 2 NOVEMBER, 2020 The Imprest SystemChristine RamkissoonNo ratings yet

- Chapter 6 Bank Recon Practice QHDocument3 pagesChapter 6 Bank Recon Practice QHSuy Yanghear100% (1)

- Accounting Yr 10 Chapter 3-5 QuizDocument8 pagesAccounting Yr 10 Chapter 3-5 QuizThin Zar Tin WinNo ratings yet

- Cash Book II - Accounting-Workbook - Zaheer-SwatiDocument4 pagesCash Book II - Accounting-Workbook - Zaheer-SwatiZaheer SwatiNo ratings yet

- Revision Questions 2Document14 pagesRevision Questions 2najihah AnualNo ratings yet

- Acc - Section 3B1 Cash BookDocument8 pagesAcc - Section 3B1 Cash BookNathefa LayneNo ratings yet

- Chapter 9.docpart 1 FinalDocument15 pagesChapter 9.docpart 1 FinalRabie HarounNo ratings yet

- BANK RECONCILIATION - WorksheetDocument3 pagesBANK RECONCILIATION - Worksheetna-tri-li-aNo ratings yet

- ACCO TestDocument6 pagesACCO TestvrindadevigtmNo ratings yet

- attachment_1Document10 pagesattachment_1S Nur ApriyaniNo ratings yet

- Intermediate Accounting 1Document14 pagesIntermediate Accounting 1cpacpacpa100% (1)

- It Is October 16 2014 and You Have Just TakenDocument1 pageIt Is October 16 2014 and You Have Just TakenFreelance WorkerNo ratings yet

- Cambridge IGCSE: Accounting 0452/13Document12 pagesCambridge IGCSE: Accounting 0452/13khiba04No ratings yet

- Petty Cashbook NotesDocument6 pagesPetty Cashbook NotesBamidele AdegboyeNo ratings yet

- 4 - The Future of Work After COVID-19 - McKinseyDocument15 pages4 - The Future of Work After COVID-19 - McKinseygvillacres1627No ratings yet

- 42 Solar Water Heating and The Plant EngineerDocument8 pages42 Solar Water Heating and The Plant Engineerdumitrescu viorelNo ratings yet

- Foreign Trade Law: The Agreement On Trade-Related Investment Measures (Trims)Document15 pagesForeign Trade Law: The Agreement On Trade-Related Investment Measures (Trims)TanuNo ratings yet

- Discussion Text Introduction and Overview-Fp-8c7af13a-1Document14 pagesDiscussion Text Introduction and Overview-Fp-8c7af13a-1Dina YandiniNo ratings yet

- Bien Prononcer L'anglais: Corrigés Et ScriptsDocument43 pagesBien Prononcer L'anglais: Corrigés Et ScriptsThierry HarmannNo ratings yet

- International Trade TheoriesDocument38 pagesInternational Trade Theoriestrustme77No ratings yet

- Agile Certified Professional: Study Guide Take The Certification OnlineDocument25 pagesAgile Certified Professional: Study Guide Take The Certification OnlineqwertyNo ratings yet

- District Profile ThattaDocument52 pagesDistrict Profile ThattaUrooj Fatima100% (1)

- YarnsDocument38 pagesYarnsAbhinav VermaNo ratings yet

- Himel General CatalogueDocument93 pagesHimel General CatalogueJeffDeCastroNo ratings yet

- Lingüística de Corpus en Español The Routledge Handbook of Spanish Corpus Linguistics 1st Edition Giovanni Parodi Editor Pascual Cantos Gómez Editor Chad Howe Editor Full Chapter Download PDFDocument58 pagesLingüística de Corpus en Español The Routledge Handbook of Spanish Corpus Linguistics 1st Edition Giovanni Parodi Editor Pascual Cantos Gómez Editor Chad Howe Editor Full Chapter Download PDFdressaherns100% (2)

- Website Comprehensibility Research DesignDocument14 pagesWebsite Comprehensibility Research DesignRay Garcia100% (1)

- Army Ants PocketModDocument1 pageArmy Ants PocketModcmr8286No ratings yet

- ELEN 3018 - Macro Test - 2013 - ADocument1 pageELEN 3018 - Macro Test - 2013 - AsirlordbookwormNo ratings yet

- Trillion DollarsDocument95 pagesTrillion DollarsVyacheslav GrzhibovskiyNo ratings yet

- Us Nop Organic Compliant Materials 20171121Document3 pagesUs Nop Organic Compliant Materials 20171121LayfloNo ratings yet

- Honda DAXDocument12 pagesHonda DAXFranco CondeNo ratings yet

- ICOM-CC 2017 Copenhagen 507Document11 pagesICOM-CC 2017 Copenhagen 507Cristi CostinNo ratings yet

- CrsDocument660 pagesCrsaamirmehmoodkhanNo ratings yet

- Subject - Verb AgreementDocument12 pagesSubject - Verb AgreementRistaNo ratings yet

- Breaking Bad TeaserDocument3 pagesBreaking Bad Teaserjorge escobarNo ratings yet

- Chapter Three Edited - Public EnterpriseDocument9 pagesChapter Three Edited - Public EnterpriseMarah Moses BallaNo ratings yet

- RelatórioDocument1 pageRelatórioneveshelenaliceNo ratings yet

- A Case Study of Exploiting Data Mining TechniquesDocument8 pagesA Case Study of Exploiting Data Mining TechniquesAdam GraphiandanaNo ratings yet

- Capital Budgeting Decisions: Solutions To QuestionsDocument61 pagesCapital Budgeting Decisions: Solutions To QuestionsBasanta K SahuNo ratings yet

- Research Paper 1Document14 pagesResearch Paper 1Fatima SinghNo ratings yet

- Acs42 Config GuideDocument214 pagesAcs42 Config GuideOtia ObaNo ratings yet