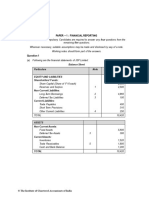

75765bos61307 p1

75765bos61307 p1

You might also like

- RSM230 Cheat SheetDocument2 pagesRSM230 Cheat Sheets_786886338No ratings yet

- Barclays Bank Statement 2Document5 pagesBarclays Bank Statement 2zainabNo ratings yet

- SOALDocument2 pagesSOALjwtrmdhnNo ratings yet

- M4 - Problem Exercises - Statement of Financial Position PDFDocument7 pagesM4 - Problem Exercises - Statement of Financial Position PDFCamille CastroNo ratings yet

- MAS-14 FS Analaysis With EFN (Letran)Document6 pagesMAS-14 FS Analaysis With EFN (Letran)Gio PacayraNo ratings yet

- FR Suggested Answers CompilerDocument150 pagesFR Suggested Answers CompilerSach SahuNo ratings yet

- Paper - 1: Financial Reporting: Assets David Ltd. Parker Ltd. Non-Current AssetsDocument32 pagesPaper - 1: Financial Reporting: Assets David Ltd. Parker Ltd. Non-Current AssetsayushiNo ratings yet

- 71465exam57501 p1Document32 pages71465exam57501 p1ManaliNo ratings yet

- Question ADV GMDocument6 pagesQuestion ADV GMsherlockNo ratings yet

- Aafr Updated Past PapersDocument491 pagesAafr Updated Past PapersSummama Ahmad LodhraNo ratings yet

- Consolidation Q11Document5 pagesConsolidation Q11johny SahaNo ratings yet

- Test Series: March, 2021 Mock Test Paper - 1 Intermediate (New) : Group - Ii Paper - 5: Advanced AccountingDocument7 pagesTest Series: March, 2021 Mock Test Paper - 1 Intermediate (New) : Group - Ii Paper - 5: Advanced AccountingOcto ManNo ratings yet

- Assets: © The Institute of Chartered Accountants of IndiaDocument16 pagesAssets: © The Institute of Chartered Accountants of IndiaMarvel KadaNo ratings yet

- Question No.1 Is Compulsory. Candidates Are Required To Answer Any Four Questions From The Remaining Five QuestionsDocument7 pagesQuestion No.1 Is Compulsory. Candidates Are Required To Answer Any Four Questions From The Remaining Five Questionsritz meshNo ratings yet

- Advanced Accounts MTP M21 S2Document19 pagesAdvanced Accounts MTP M21 S2Harshwardhan PatilNo ratings yet

- Test Series: April, 2021 Mock Test Paper - 2 Intermediate (New) : Group - Ii Paper - 5: Advanced AccountingDocument6 pagesTest Series: April, 2021 Mock Test Paper - 2 Intermediate (New) : Group - Ii Paper - 5: Advanced AccountingOcto ManNo ratings yet

- Test Series: October, 2019 Mock Test Paper Final (Old) Course: Group - I Paper - 1: Financial ReportingDocument8 pagesTest Series: October, 2019 Mock Test Paper Final (Old) Course: Group - I Paper - 1: Financial ReportingDev ReddyNo ratings yet

- CA Inter Law Ans Dec 2021Document21 pagesCA Inter Law Ans Dec 2021Punith KumarNo ratings yet

- CA Final - FR Faster Batch - Consolidation Additional QuestionsDocument8 pagesCA Final - FR Faster Batch - Consolidation Additional QuestionsRonaldo GOmesNo ratings yet

- Question 6 Chic Homes LTD GroupDocument5 pagesQuestion 6 Chic Homes LTD GroupsavagewolfieNo ratings yet

- Cash Flow StatementsDocument21 pagesCash Flow StatementsAnaya KaleNo ratings yet

- The Grape Group (Acquisition) : Cfap 1: A A F RDocument1 pageThe Grape Group (Acquisition) : Cfap 1: A A F R.No ratings yet

- MTP 11 1 Questions 1696062519Document6 pagesMTP 11 1 Questions 1696062519kabeeramitbarot96No ratings yet

- CFAP 2 CLS Winter 2020Document6 pagesCFAP 2 CLS Winter 2020Furqan HanifNo ratings yet

- Chartered Accountancy Professional Ii (Cap-Ii) : Revision Test Paper Group I December 2021Document81 pagesChartered Accountancy Professional Ii (Cap-Ii) : Revision Test Paper Group I December 2021Arpan ParajuliNo ratings yet

- FR Last 4 MTPDocument98 pagesFR Last 4 MTPSHIVSHANKER AGARWALNo ratings yet

- FR Suggested July 2021Document38 pagesFR Suggested July 2021Rahul NandurkarNo ratings yet

- HI5020 Corporate Accounting: Session 7c Accounting For Group StructuresDocument30 pagesHI5020 Corporate Accounting: Session 7c Accounting For Group StructuresFeku RamNo ratings yet

- Assignment 2 Far110Document4 pagesAssignment 2 Far110AisyahNo ratings yet

- Question Paper - CFS & IND As 19Document6 pagesQuestion Paper - CFS & IND As 19pratikdubey9586No ratings yet

- Learning Unit 7 - Elimination of Intragroup TransactionsDocument61 pagesLearning Unit 7 - Elimination of Intragroup TransactionsThulani NdlovuNo ratings yet

- Vidya Sagar Career Institute Limited Mobile: 93514 - 68666 Phone: 7821821250 / 51 / 52 / 53 / 54Document9 pagesVidya Sagar Career Institute Limited Mobile: 93514 - 68666 Phone: 7821821250 / 51 / 52 / 53 / 54shrenik bhuratNo ratings yet

- Suggested CAP II Group I June 2023Document43 pagesSuggested CAP II Group I June 2023pratyushmudbhari340No ratings yet

- FR MTP 2Document8 pagesFR MTP 2gaurav gargNo ratings yet

- 78018bos62659 c13 TykDocument38 pages78018bos62659 c13 TykHirak PatelNo ratings yet

- TPP PP 2024Document225 pagesTPP PP 2024AminaNo ratings yet

- Lecture No. 2 - Financial Statements & Illustrative ProblemDocument6 pagesLecture No. 2 - Financial Statements & Illustrative ProblemJA LAYUG100% (1)

- Nov22 Final gp1Document108 pagesNov22 Final gp1navin kumarNo ratings yet

- 64746bos51938 Fnew p4Document21 pages64746bos51938 Fnew p4AagamNo ratings yet

- 69587bos55533-P1.pdf 2Document46 pages69587bos55533-P1.pdf 2pittujb2002No ratings yet

- Banking QaDocument10 pagesBanking QaBijay AgrawalNo ratings yet

- CA FINAL (May 2019 - New Course) Paper - 1 (Financial Reporting)Document32 pagesCA FINAL (May 2019 - New Course) Paper - 1 (Financial Reporting)Upasana NimjeNo ratings yet

- Numericals Schedule 3Document4 pagesNumericals Schedule 3Achyut AwasthiNo ratings yet

- FE QUESTION FIN 2224 Sept2021Document6 pagesFE QUESTION FIN 2224 Sept2021Tabish HyderNo ratings yet

- Financial Accounting WorkbookDocument4 pagesFinancial Accounting WorkbookZiyaad SolomonNo ratings yet

- Inp 2205 - Advance Accounting - Question PaperDocument10 pagesInp 2205 - Advance Accounting - Question PaperAnshit BahediaNo ratings yet

- RTP June 19 QnsDocument15 pagesRTP June 19 QnsbinuNo ratings yet

- June 2019Document182 pagesJune 2019shankar k.c.No ratings yet

- Calculation of Rebate: Particular Dr. CRDocument12 pagesCalculation of Rebate: Particular Dr. CRDennis BijuNo ratings yet

- Paper - 1: Financial Reporting: AssetsDocument43 pagesPaper - 1: Financial Reporting: AssetsTisha AggarwalNo ratings yet

- Unit IV Corporate Liquidation PDFDocument20 pagesUnit IV Corporate Liquidation PDFLeslie Mae Vargas ZafeNo ratings yet

- PDF 04Document7 pagesPDF 04Hiruni LakshaniNo ratings yet

- CA Inter Law Suggested Answer Nov 2022Document20 pagesCA Inter Law Suggested Answer Nov 2022V DHARSHININo ratings yet

- Advanced AccountingDocument39 pagesAdvanced AccountingHemanth Singh RajpurohitNo ratings yet

- Statement Of: Financial PositionDocument22 pagesStatement Of: Financial PositionZyriece Camille CentenoNo ratings yet

- Ga PP Module 3 Dec2022Document125 pagesGa PP Module 3 Dec2022preethi alNo ratings yet

- CAP-III SA Group-I Dec2021 FinalDocument79 pagesCAP-III SA Group-I Dec2021 FinalSanjay AryalNo ratings yet

- © The Institute of Chartered Accountants of India: TH STDocument46 pages© The Institute of Chartered Accountants of India: TH STheikNo ratings yet

- Test 4Document8 pagesTest 4govarthan1976No ratings yet

- Super 50 Cma Final Dt June 2024Document52 pagesSuper 50 Cma Final Dt June 2024Raja MunagalaNo ratings yet

- C 20: C C F: Hapter Onsolidation ASH LowsDocument1 pageC 20: C C F: Hapter Onsolidation ASH Lows.No ratings yet

- Far320 Capital Reduction ExercisesDocument7 pagesFar320 Capital Reduction ExercisesALIA MAISARA MD AKHIRNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- AP.3501 Audit of InventoriesDocument7 pagesAP.3501 Audit of InventoriesMarinoNo ratings yet

- CFIA Sample Exam Questions and Instructions - 2024Document12 pagesCFIA Sample Exam Questions and Instructions - 2024martin.rosNo ratings yet

- 2 Just For FEET Case Analysis REWRITEDocument7 pages2 Just For FEET Case Analysis REWRITEJuris Renier MendozaNo ratings yet

- Finals - II. Deductions & ExemptionsDocument13 pagesFinals - II. Deductions & ExemptionsJovince Daño DoceNo ratings yet

- Kasneb Examinations Information BookletDocument58 pagesKasneb Examinations Information BookletCollins OgiloNo ratings yet

- Assignment in Financial ManagementDocument6 pagesAssignment in Financial ManagementEricaNo ratings yet

- 119 Jasmine Tirkey PDFDocument30 pages119 Jasmine Tirkey PDFDinki ChouhanNo ratings yet

- Chapter 3 (Accounting - What The Numbers Mean 10e)Document17 pagesChapter 3 (Accounting - What The Numbers Mean 10e)Nguyen Dac ThichNo ratings yet

- TATA CONSULTANCY SERVICES ValautionDocument3 pagesTATA CONSULTANCY SERVICES ValautionRohit Kumar 4170No ratings yet

- Management Accounting Notes 20.02.2024Document11 pagesManagement Accounting Notes 20.02.2024damienmugabo3No ratings yet

- 01 Mar 2023 To 31 Mar 2023 FCMB StatementDocument2 pages01 Mar 2023 To 31 Mar 2023 FCMB StatementMoses Iyekekpolor OtaborNo ratings yet

- Fundamentals 2024 PDF SPCCDocument82 pagesFundamentals 2024 PDF SPCCJeetalal GadaNo ratings yet

- Endnotes 1 AA Atkinson and GA FelthamDocument4 pagesEndnotes 1 AA Atkinson and GA FelthamLina JapNo ratings yet

- SM 06Document73 pagesSM 06Mai Anh ĐàoNo ratings yet

- GMD FICC Sales (New)Document1 pageGMD FICC Sales (New)Ritik BaliNo ratings yet

- Incoterms 2020 Chart 2023Document1 pageIncoterms 2020 Chart 2023dc-183159No ratings yet

- NOTES G RCCP Stocks, StockholdersDocument3 pagesNOTES G RCCP Stocks, StockholdersMelissa Kayla ManiulitNo ratings yet

- WCM of Cipla LTDDocument53 pagesWCM of Cipla LTDChanderNo ratings yet

- ACC 610 Final Project SubmissionDocument26 pagesACC 610 Final Project SubmissionvincentNo ratings yet

- Audit of LedgersDocument28 pagesAudit of LedgersShahbaz NoorNo ratings yet

- Analysis On Combating Hostile TakeoverDocument14 pagesAnalysis On Combating Hostile TakeoverLAW MANTRA100% (1)

- Corporate Finance - Teaching Plan - 2019-21Document18 pagesCorporate Finance - Teaching Plan - 2019-21Dimpy KatharNo ratings yet

- Factsheet Nifty100 Alpha30Document2 pagesFactsheet Nifty100 Alpha30sumonNo ratings yet

- FM & Eco Grand Test 3Document9 pagesFM & Eco Grand Test 3moniNo ratings yet

- Chapter 16 Advanced Accounting Solution ManualDocument119 pagesChapter 16 Advanced Accounting Solution ManualAsuncion BarquerosNo ratings yet

- Resume Chapter 11Document2 pagesResume Chapter 11dwiNo ratings yet

- Topic: Introduction To Financial Statements K W LDocument3 pagesTopic: Introduction To Financial Statements K W Lfatima waqar100% (1)

Download as pdf or txt

You might also like

- RSM230 Cheat SheetDocument2 pagesRSM230 Cheat Sheets_786886338No ratings yet

- Barclays Bank Statement 2Document5 pagesBarclays Bank Statement 2zainabNo ratings yet

- SOALDocument2 pagesSOALjwtrmdhnNo ratings yet

- M4 - Problem Exercises - Statement of Financial Position PDFDocument7 pagesM4 - Problem Exercises - Statement of Financial Position PDFCamille CastroNo ratings yet

- MAS-14 FS Analaysis With EFN (Letran)Document6 pagesMAS-14 FS Analaysis With EFN (Letran)Gio PacayraNo ratings yet

- FR Suggested Answers CompilerDocument150 pagesFR Suggested Answers CompilerSach SahuNo ratings yet

- Paper - 1: Financial Reporting: Assets David Ltd. Parker Ltd. Non-Current AssetsDocument32 pagesPaper - 1: Financial Reporting: Assets David Ltd. Parker Ltd. Non-Current AssetsayushiNo ratings yet

- 71465exam57501 p1Document32 pages71465exam57501 p1ManaliNo ratings yet

- Question ADV GMDocument6 pagesQuestion ADV GMsherlockNo ratings yet

- Aafr Updated Past PapersDocument491 pagesAafr Updated Past PapersSummama Ahmad LodhraNo ratings yet

- Consolidation Q11Document5 pagesConsolidation Q11johny SahaNo ratings yet

- Test Series: March, 2021 Mock Test Paper - 1 Intermediate (New) : Group - Ii Paper - 5: Advanced AccountingDocument7 pagesTest Series: March, 2021 Mock Test Paper - 1 Intermediate (New) : Group - Ii Paper - 5: Advanced AccountingOcto ManNo ratings yet

- Assets: © The Institute of Chartered Accountants of IndiaDocument16 pagesAssets: © The Institute of Chartered Accountants of IndiaMarvel KadaNo ratings yet

- Question No.1 Is Compulsory. Candidates Are Required To Answer Any Four Questions From The Remaining Five QuestionsDocument7 pagesQuestion No.1 Is Compulsory. Candidates Are Required To Answer Any Four Questions From The Remaining Five Questionsritz meshNo ratings yet

- Advanced Accounts MTP M21 S2Document19 pagesAdvanced Accounts MTP M21 S2Harshwardhan PatilNo ratings yet

- Test Series: April, 2021 Mock Test Paper - 2 Intermediate (New) : Group - Ii Paper - 5: Advanced AccountingDocument6 pagesTest Series: April, 2021 Mock Test Paper - 2 Intermediate (New) : Group - Ii Paper - 5: Advanced AccountingOcto ManNo ratings yet

- Test Series: October, 2019 Mock Test Paper Final (Old) Course: Group - I Paper - 1: Financial ReportingDocument8 pagesTest Series: October, 2019 Mock Test Paper Final (Old) Course: Group - I Paper - 1: Financial ReportingDev ReddyNo ratings yet

- CA Inter Law Ans Dec 2021Document21 pagesCA Inter Law Ans Dec 2021Punith KumarNo ratings yet

- CA Final - FR Faster Batch - Consolidation Additional QuestionsDocument8 pagesCA Final - FR Faster Batch - Consolidation Additional QuestionsRonaldo GOmesNo ratings yet

- Question 6 Chic Homes LTD GroupDocument5 pagesQuestion 6 Chic Homes LTD GroupsavagewolfieNo ratings yet

- Cash Flow StatementsDocument21 pagesCash Flow StatementsAnaya KaleNo ratings yet

- The Grape Group (Acquisition) : Cfap 1: A A F RDocument1 pageThe Grape Group (Acquisition) : Cfap 1: A A F R.No ratings yet

- MTP 11 1 Questions 1696062519Document6 pagesMTP 11 1 Questions 1696062519kabeeramitbarot96No ratings yet

- CFAP 2 CLS Winter 2020Document6 pagesCFAP 2 CLS Winter 2020Furqan HanifNo ratings yet

- Chartered Accountancy Professional Ii (Cap-Ii) : Revision Test Paper Group I December 2021Document81 pagesChartered Accountancy Professional Ii (Cap-Ii) : Revision Test Paper Group I December 2021Arpan ParajuliNo ratings yet

- FR Last 4 MTPDocument98 pagesFR Last 4 MTPSHIVSHANKER AGARWALNo ratings yet

- FR Suggested July 2021Document38 pagesFR Suggested July 2021Rahul NandurkarNo ratings yet

- HI5020 Corporate Accounting: Session 7c Accounting For Group StructuresDocument30 pagesHI5020 Corporate Accounting: Session 7c Accounting For Group StructuresFeku RamNo ratings yet

- Assignment 2 Far110Document4 pagesAssignment 2 Far110AisyahNo ratings yet

- Question Paper - CFS & IND As 19Document6 pagesQuestion Paper - CFS & IND As 19pratikdubey9586No ratings yet

- Learning Unit 7 - Elimination of Intragroup TransactionsDocument61 pagesLearning Unit 7 - Elimination of Intragroup TransactionsThulani NdlovuNo ratings yet

- Vidya Sagar Career Institute Limited Mobile: 93514 - 68666 Phone: 7821821250 / 51 / 52 / 53 / 54Document9 pagesVidya Sagar Career Institute Limited Mobile: 93514 - 68666 Phone: 7821821250 / 51 / 52 / 53 / 54shrenik bhuratNo ratings yet

- Suggested CAP II Group I June 2023Document43 pagesSuggested CAP II Group I June 2023pratyushmudbhari340No ratings yet

- FR MTP 2Document8 pagesFR MTP 2gaurav gargNo ratings yet

- 78018bos62659 c13 TykDocument38 pages78018bos62659 c13 TykHirak PatelNo ratings yet

- TPP PP 2024Document225 pagesTPP PP 2024AminaNo ratings yet

- Lecture No. 2 - Financial Statements & Illustrative ProblemDocument6 pagesLecture No. 2 - Financial Statements & Illustrative ProblemJA LAYUG100% (1)

- Nov22 Final gp1Document108 pagesNov22 Final gp1navin kumarNo ratings yet

- 64746bos51938 Fnew p4Document21 pages64746bos51938 Fnew p4AagamNo ratings yet

- 69587bos55533-P1.pdf 2Document46 pages69587bos55533-P1.pdf 2pittujb2002No ratings yet

- Banking QaDocument10 pagesBanking QaBijay AgrawalNo ratings yet

- CA FINAL (May 2019 - New Course) Paper - 1 (Financial Reporting)Document32 pagesCA FINAL (May 2019 - New Course) Paper - 1 (Financial Reporting)Upasana NimjeNo ratings yet

- Numericals Schedule 3Document4 pagesNumericals Schedule 3Achyut AwasthiNo ratings yet

- FE QUESTION FIN 2224 Sept2021Document6 pagesFE QUESTION FIN 2224 Sept2021Tabish HyderNo ratings yet

- Financial Accounting WorkbookDocument4 pagesFinancial Accounting WorkbookZiyaad SolomonNo ratings yet

- Inp 2205 - Advance Accounting - Question PaperDocument10 pagesInp 2205 - Advance Accounting - Question PaperAnshit BahediaNo ratings yet

- RTP June 19 QnsDocument15 pagesRTP June 19 QnsbinuNo ratings yet

- June 2019Document182 pagesJune 2019shankar k.c.No ratings yet

- Calculation of Rebate: Particular Dr. CRDocument12 pagesCalculation of Rebate: Particular Dr. CRDennis BijuNo ratings yet

- Paper - 1: Financial Reporting: AssetsDocument43 pagesPaper - 1: Financial Reporting: AssetsTisha AggarwalNo ratings yet

- Unit IV Corporate Liquidation PDFDocument20 pagesUnit IV Corporate Liquidation PDFLeslie Mae Vargas ZafeNo ratings yet

- PDF 04Document7 pagesPDF 04Hiruni LakshaniNo ratings yet

- CA Inter Law Suggested Answer Nov 2022Document20 pagesCA Inter Law Suggested Answer Nov 2022V DHARSHININo ratings yet

- Advanced AccountingDocument39 pagesAdvanced AccountingHemanth Singh RajpurohitNo ratings yet

- Statement Of: Financial PositionDocument22 pagesStatement Of: Financial PositionZyriece Camille CentenoNo ratings yet

- Ga PP Module 3 Dec2022Document125 pagesGa PP Module 3 Dec2022preethi alNo ratings yet

- CAP-III SA Group-I Dec2021 FinalDocument79 pagesCAP-III SA Group-I Dec2021 FinalSanjay AryalNo ratings yet

- © The Institute of Chartered Accountants of India: TH STDocument46 pages© The Institute of Chartered Accountants of India: TH STheikNo ratings yet

- Test 4Document8 pagesTest 4govarthan1976No ratings yet

- Super 50 Cma Final Dt June 2024Document52 pagesSuper 50 Cma Final Dt June 2024Raja MunagalaNo ratings yet

- C 20: C C F: Hapter Onsolidation ASH LowsDocument1 pageC 20: C C F: Hapter Onsolidation ASH Lows.No ratings yet

- Far320 Capital Reduction ExercisesDocument7 pagesFar320 Capital Reduction ExercisesALIA MAISARA MD AKHIRNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- AP.3501 Audit of InventoriesDocument7 pagesAP.3501 Audit of InventoriesMarinoNo ratings yet

- CFIA Sample Exam Questions and Instructions - 2024Document12 pagesCFIA Sample Exam Questions and Instructions - 2024martin.rosNo ratings yet

- 2 Just For FEET Case Analysis REWRITEDocument7 pages2 Just For FEET Case Analysis REWRITEJuris Renier MendozaNo ratings yet

- Finals - II. Deductions & ExemptionsDocument13 pagesFinals - II. Deductions & ExemptionsJovince Daño DoceNo ratings yet

- Kasneb Examinations Information BookletDocument58 pagesKasneb Examinations Information BookletCollins OgiloNo ratings yet

- Assignment in Financial ManagementDocument6 pagesAssignment in Financial ManagementEricaNo ratings yet

- 119 Jasmine Tirkey PDFDocument30 pages119 Jasmine Tirkey PDFDinki ChouhanNo ratings yet

- Chapter 3 (Accounting - What The Numbers Mean 10e)Document17 pagesChapter 3 (Accounting - What The Numbers Mean 10e)Nguyen Dac ThichNo ratings yet

- TATA CONSULTANCY SERVICES ValautionDocument3 pagesTATA CONSULTANCY SERVICES ValautionRohit Kumar 4170No ratings yet

- Management Accounting Notes 20.02.2024Document11 pagesManagement Accounting Notes 20.02.2024damienmugabo3No ratings yet

- 01 Mar 2023 To 31 Mar 2023 FCMB StatementDocument2 pages01 Mar 2023 To 31 Mar 2023 FCMB StatementMoses Iyekekpolor OtaborNo ratings yet

- Fundamentals 2024 PDF SPCCDocument82 pagesFundamentals 2024 PDF SPCCJeetalal GadaNo ratings yet

- Endnotes 1 AA Atkinson and GA FelthamDocument4 pagesEndnotes 1 AA Atkinson and GA FelthamLina JapNo ratings yet

- SM 06Document73 pagesSM 06Mai Anh ĐàoNo ratings yet

- GMD FICC Sales (New)Document1 pageGMD FICC Sales (New)Ritik BaliNo ratings yet

- Incoterms 2020 Chart 2023Document1 pageIncoterms 2020 Chart 2023dc-183159No ratings yet

- NOTES G RCCP Stocks, StockholdersDocument3 pagesNOTES G RCCP Stocks, StockholdersMelissa Kayla ManiulitNo ratings yet

- WCM of Cipla LTDDocument53 pagesWCM of Cipla LTDChanderNo ratings yet

- ACC 610 Final Project SubmissionDocument26 pagesACC 610 Final Project SubmissionvincentNo ratings yet

- Audit of LedgersDocument28 pagesAudit of LedgersShahbaz NoorNo ratings yet

- Analysis On Combating Hostile TakeoverDocument14 pagesAnalysis On Combating Hostile TakeoverLAW MANTRA100% (1)

- Corporate Finance - Teaching Plan - 2019-21Document18 pagesCorporate Finance - Teaching Plan - 2019-21Dimpy KatharNo ratings yet

- Factsheet Nifty100 Alpha30Document2 pagesFactsheet Nifty100 Alpha30sumonNo ratings yet

- FM & Eco Grand Test 3Document9 pagesFM & Eco Grand Test 3moniNo ratings yet

- Chapter 16 Advanced Accounting Solution ManualDocument119 pagesChapter 16 Advanced Accounting Solution ManualAsuncion BarquerosNo ratings yet

- Resume Chapter 11Document2 pagesResume Chapter 11dwiNo ratings yet

- Topic: Introduction To Financial Statements K W LDocument3 pagesTopic: Introduction To Financial Statements K W Lfatima waqar100% (1)