Chapter 6 - Retained Earnings

Chapter 6 - Retained Earnings

You might also like

- Chapter 7 - Assignment 2Document9 pagesChapter 7 - Assignment 2Gwen Stefani DaugdaugNo ratings yet

- Problem #1 Shares Issuance For Cash: Name: Section: ProfessorDocument14 pagesProblem #1 Shares Issuance For Cash: Name: Section: Professorkakao0% (3)

- Collateral Management GuideDocument20 pagesCollateral Management Guidereggie1010100% (3)

- Argus CrudeDocument28 pagesArgus CrudeAziz SaputraNo ratings yet

- Corporations:Basic Considerations: Module 11-Chapter 14Document16 pagesCorporations:Basic Considerations: Module 11-Chapter 14kakaoNo ratings yet

- Problem 32 Retained Earnings ParcorDocument3 pagesProblem 32 Retained Earnings Parcornikki syNo ratings yet

- Chapter 5 - Corporation - Share TransactionsDocument14 pagesChapter 5 - Corporation - Share Transactionslou-924No ratings yet

- Module 5 - With SolutionsDocument12 pagesModule 5 - With SolutionsStella MarieNo ratings yet

- UM Panabo College 6th Examination Accounting 2a Test I - Multiple Choice Theory. No Erasures AllowedDocument2 pagesUM Panabo College 6th Examination Accounting 2a Test I - Multiple Choice Theory. No Erasures AllowedJessa BeloyNo ratings yet

- Corporation Problems-1Document18 pagesCorporation Problems-1Avia Chelsy DeangNo ratings yet

- Acctg 102 - True or False (Dissolution - Changes in Ownership) Flashcards - QuizletDocument4 pagesAcctg 102 - True or False (Dissolution - Changes in Ownership) Flashcards - QuizletBisag AsaNo ratings yet

- Corp. Retained EarningsDocument9 pagesCorp. Retained EarningshsjhsNo ratings yet

- CorpoDocument16 pagesCorpoErica JoannaNo ratings yet

- ParCor Chapter 5 - Hernandez - BSA 1-1 PDFDocument5 pagesParCor Chapter 5 - Hernandez - BSA 1-1 PDFBSA 1-1No ratings yet

- Partnership LiquidationDocument9 pagesPartnership LiquidationPeter PiperNo ratings yet

- Assignment Bsma 1a April 6Document27 pagesAssignment Bsma 1a April 6Maeca Angela SerranoNo ratings yet

- Cash Priority ProgramDocument1 pageCash Priority Programyela garcia0% (1)

- Chapter 3 ProblemshhhDocument15 pagesChapter 3 Problemshhhahmed arfanNo ratings yet

- Theories ProblemsDocument9 pagesTheories ProblemsKristine Esplana ToraldeNo ratings yet

- Partnership OperationDocument2 pagesPartnership OperationCjhay MarcosNo ratings yet

- CFAS Sample ProblemsDocument5 pagesCFAS Sample ProblemsChristian MartinNo ratings yet

- Retained EarningsDocument3 pagesRetained EarningsChristian Marvin VillanuevaNo ratings yet

- MCQ PartnershipDocument24 pagesMCQ Partnershiplou-924No ratings yet

- 5 2Document8 pages5 2Evelyn MorilloNo ratings yet

- Chpter 1.problem 7.mullesDocument11 pagesChpter 1.problem 7.mullesKim OlimbaNo ratings yet

- ACCTG122 Homework On Partnership LiquidationDocument2 pagesACCTG122 Homework On Partnership LiquidationJoana TrinidadNo ratings yet

- Chapter 11 SampleDocument6 pagesChapter 11 SamplePattraniteNo ratings yet

- Problem No. 1: Journal Entries PROBLEM NO. 5: JE and Statement of Financial Position Books of The Partnership Books of Fish R' UsDocument4 pagesProblem No. 1: Journal Entries PROBLEM NO. 5: JE and Statement of Financial Position Books of The Partnership Books of Fish R' UsJessa0% (1)

- Chap 3 and 4 - ParcorDocument4 pagesChap 3 and 4 - ParcorAnne Gwynneth RadaNo ratings yet

- Solved The Partnership of Angel Investors Began Operations On January 1... - Course HeroDocument2 pagesSolved The Partnership of Angel Investors Began Operations On January 1... - Course HeroeannetiyabNo ratings yet

- Par CorDocument27 pagesPar CorPam LlanetaNo ratings yet

- Win Ballada Parcor Chapter 4 ProblemDocument2 pagesWin Ballada Parcor Chapter 4 ProblemKrngyx100% (1)

- Bam 040 ReviewerDocument7 pagesBam 040 ReviewerAndrea Vila VelascoNo ratings yet

- TOPIC EconDocument44 pagesTOPIC EconChristy HabelNo ratings yet

- CAlAMBA AND SANTIAGO - TUGOTDocument2 pagesCAlAMBA AND SANTIAGO - TUGOTAndrea Tugot100% (1)

- Problem 5Document4 pagesProblem 5Reana ReyesNo ratings yet

- Baral, Malaluan, CastroDocument2 pagesBaral, Malaluan, CastroAndrea TugotNo ratings yet

- Acctg Problem 2-9Document4 pagesAcctg Problem 2-9Honeybunch before100% (1)

- Parcor Proj (Version 1)Document45 pagesParcor Proj (Version 1)Jwhll MaeNo ratings yet

- Accounting Quizzes Answer KeyDocument11 pagesAccounting Quizzes Answer KeyRae SlaughterNo ratings yet

- ParCor Chapter 3 - Hernandez - BSA 1-1 PDFDocument11 pagesParCor Chapter 3 - Hernandez - BSA 1-1 PDFBSA 1-1No ratings yet

- Hi Tech Gen. LedgerDocument14 pagesHi Tech Gen. LedgerjhienellNo ratings yet

- Conceptual Framework and Accounting Standards - Chapter 2 - NotesDocument5 pagesConceptual Framework and Accounting Standards - Chapter 2 - NotesKhey KheyNo ratings yet

- Admission and Retirement of PartnersDocument3 pagesAdmission and Retirement of PartnersJohn Eric MacallaNo ratings yet

- EXAM. MIDTERM. April 20, 2022Document15 pagesEXAM. MIDTERM. April 20, 2022Raziel Angelo AnsusNo ratings yet

- PARCORDocument5 pagesPARCORjelai anselmoNo ratings yet

- Accbp100 2nd Exam Part 1Document2 pagesAccbp100 2nd Exam Part 1emem resuento100% (1)

- Classifications of PartnershipDocument3 pagesClassifications of PartnershipFely MaataNo ratings yet

- Win Ballada Parcor Chapter 4 ProblemDocument2 pagesWin Ballada Parcor Chapter 4 ProblemKrngyxNo ratings yet

- Chapter 2 Problem 9 in Win Ballada ParcorDocument4 pagesChapter 2 Problem 9 in Win Ballada ParcorKatrina PetracheNo ratings yet

- ParCor Chapter 4 - Hernandez - BSA 1-1 PDFDocument7 pagesParCor Chapter 4 - Hernandez - BSA 1-1 PDFBSA 1-1No ratings yet

- ACCOUNTING 2 ReviewDocument4 pagesACCOUNTING 2 ReviewAhnJello100% (1)

- Guide Questions For Chapter 2Document5 pagesGuide Questions For Chapter 2Kathleen Mangual0% (1)

- Win Ballada Parcor Chapter 4 ProblemDocument2 pagesWin Ballada Parcor Chapter 4 ProblemKrngyx0% (1)

- Cfas Theories QuizletDocument4 pagesCfas Theories Quizletagm25No ratings yet

- Chapter 3 ParcorDocument6 pagesChapter 3 ParcorJwhll MaeNo ratings yet

- Par CorDocument11 pagesPar CorIts meh Sushi100% (1)

- Chapter 02Document25 pagesChapter 02Mendoza KlariseNo ratings yet

- 6 Corporation - Share Capital ProblemsDocument2 pages6 Corporation - Share Capital Problemslou-924No ratings yet

- Torrent Downloaded FromDocument4 pagesTorrent Downloaded FromJULIUS L. LEVENNo ratings yet

- ParCor Corpo EQ Set ADocument3 pagesParCor Corpo EQ Set AMara LacsamanaNo ratings yet

- Audit of Shareholders EquityDocument2 pagesAudit of Shareholders EquityGwyneth TorrefloresNo ratings yet

- Quiz - Leases and FSDocument12 pagesQuiz - Leases and FSlou-924No ratings yet

- Cost Accounting-2018-Guerrero-Chapter-3Document21 pagesCost Accounting-2018-Guerrero-Chapter-3lou-924No ratings yet

- GOVACC Final ExaminationDocument10 pagesGOVACC Final Examinationlou-924No ratings yet

- Chapter 13 LeasesDocument13 pagesChapter 13 Leaseslou-924No ratings yet

- Chapter 16 Non Profit OrganizationsDocument28 pagesChapter 16 Non Profit Organizationslou-924No ratings yet

- Cost Accounting-2018-Guerrero-Chapter-1Document83 pagesCost Accounting-2018-Guerrero-Chapter-1lou-924No ratings yet

- Quiz - Intagibles and LiabilitiesDocument6 pagesQuiz - Intagibles and Liabilitieslou-924No ratings yet

- Chapter 12 LiabilitiesDocument19 pagesChapter 12 Liabilitieslou-924No ratings yet

- Cost Accounting-2018-Guerrero-Chapter-2Document32 pagesCost Accounting-2018-Guerrero-Chapter-2lou-924No ratings yet

- MCQ PartnershipDocument24 pagesMCQ Partnershiplou-924No ratings yet

- Partnerships - Formation, Operations, and Changes in Ownership InterestsDocument43 pagesPartnerships - Formation, Operations, and Changes in Ownership Interestslou-924No ratings yet

- Quiz - Merchandising TheoryDocument1 pageQuiz - Merchandising Theorylou-924No ratings yet

- 3 - Partnership DissolutionDocument11 pages3 - Partnership Dissolutionlou-924No ratings yet

- Accounting - Basic ConceptsDocument35 pagesAccounting - Basic Conceptslou-924No ratings yet

- PartnershipsDocument4 pagesPartnershipslou-924No ratings yet

- Questionnaire Evaluation With Factor Analysis and Cronbach's AlphaDocument12 pagesQuestionnaire Evaluation With Factor Analysis and Cronbach's Alphalou-924No ratings yet

- A-Health Medical ClinicDocument2 pagesA-Health Medical Cliniclou-924No ratings yet

- Peer Influence On Risk Taking, Risk Preference, and Risky Decision Making in Adolescence and Adulthood: An Experimental StudyDocument5 pagesPeer Influence On Risk Taking, Risk Preference, and Risky Decision Making in Adolescence and Adulthood: An Experimental Studylou-924No ratings yet

- My Observations On The Journal Article "A Quasi-Experimental Study On Management Coaching Effectiveness"Document6 pagesMy Observations On The Journal Article "A Quasi-Experimental Study On Management Coaching Effectiveness"lou-924No ratings yet

- My Observations On The Journal Article "A Study On The Correlation Between Self Efficacy and Foreign Language Learning Anxiety"Document8 pagesMy Observations On The Journal Article "A Study On The Correlation Between Self Efficacy and Foreign Language Learning Anxiety"lou-924No ratings yet

- My Observations On The Journal Article "A Structural Equation Model of Predictors For Effective Online Learning"Document1 pageMy Observations On The Journal Article "A Structural Equation Model of Predictors For Effective Online Learning"lou-924No ratings yet

- Teachers Make A Difference, What Is The Research Evidence?Document11 pagesTeachers Make A Difference, What Is The Research Evidence?lou-924No ratings yet

- An Exploratory Factor Analysis and Reliability Analysis of The Student Online Learning Readiness (SOLR) InstrumentDocument1 pageAn Exploratory Factor Analysis and Reliability Analysis of The Student Online Learning Readiness (SOLR) Instrumentlou-924No ratings yet

- MCCPDocument4 pagesMCCPSrujan ReddyNo ratings yet

- Daily Equity Market Report - 22.03.2022Document1 pageDaily Equity Market Report - 22.03.2022Fuaad DodooNo ratings yet

- Dividend - UPDATEDDocument83 pagesDividend - UPDATEDAbhishek SinhaNo ratings yet

- How To Handle Your MoneyDocument7 pagesHow To Handle Your Moneypjs150% (1)

- Mflrig 1208160004405181Document2 pagesMflrig 1208160004405181Spam SuhasNo ratings yet

- Procter Gamble v. Bankers TrustDocument22 pagesProcter Gamble v. Bankers Trustthman.workingNo ratings yet

- FD Internal Assessment PaperDocument2 pagesFD Internal Assessment PaperAAKIB HAMDANINo ratings yet

- Russell Indexes Performance: Best PerformingDocument2 pagesRussell Indexes Performance: Best PerformingWilliam HuachisacaNo ratings yet

- Chapter 10 PresentationDocument26 pagesChapter 10 PresentationMega_ImranNo ratings yet

- IIFL - India Info Line - FUNCTION'S OF STOCK MARKET IN INDIA (WITH RESPECT TO LEVEL OF CUSTOMER ADocument88 pagesIIFL - India Info Line - FUNCTION'S OF STOCK MARKET IN INDIA (WITH RESPECT TO LEVEL OF CUSTOMER AVajir BajiNo ratings yet

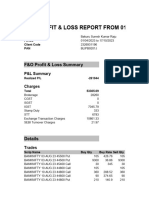

- F&O P&L Report.Document8 pagesF&O P&L Report.Suresh KumarNo ratings yet

- Yhoo 20110908 SC13D 0Document17 pagesYhoo 20110908 SC13D 0Kara SwisherNo ratings yet

- Suggested Solutions To Chapter 8 Problems: NswerDocument5 pagesSuggested Solutions To Chapter 8 Problems: NsweremilyNo ratings yet

- Chapter 1 - Role of Financial Markets and InstitutionsDocument33 pagesChapter 1 - Role of Financial Markets and InstitutionsJenniferNo ratings yet

- Drago Indjic On Liquidity and Replicators at London Business SchoolDocument31 pagesDrago Indjic On Liquidity and Replicators at London Business SchoolDrago IndjicNo ratings yet

- SEBI Revisits The Concept of Promoter & Promoter GroupDocument10 pagesSEBI Revisits The Concept of Promoter & Promoter GroupAngela JohnNo ratings yet

- Redemption of Preference SharesDocument11 pagesRedemption of Preference SharesRiya SawantNo ratings yet

- Keene, Andrew - Ichimoku Cloud, World's Best Technical IndicatorDocument17 pagesKeene, Andrew - Ichimoku Cloud, World's Best Technical IndicatorihaiNo ratings yet

- Exchange Traded FundDocument2 pagesExchange Traded FundarmailgmNo ratings yet

- CH 20Document22 pagesCH 20sumihosaNo ratings yet

- Mutual Fund DataDocument194 pagesMutual Fund DatashreyaNo ratings yet

- Consistent Profits Through Option Selling 28 12 19 WebinarDocument50 pagesConsistent Profits Through Option Selling 28 12 19 WebinarRahul67% (3)

- Amisignals - ULTIMATEDocument11 pagesAmisignals - ULTIMATEpndymrigankarkaNo ratings yet

- Management CoempensationDocument5 pagesManagement CoempensationSufia Nur KamilaNo ratings yet

- Confirmation: Unit Price Net Debit Security No. of Shares R/R Extension CommissionDocument1 pageConfirmation: Unit Price Net Debit Security No. of Shares R/R Extension CommissionDrw ArcyNo ratings yet

- Dividend Policy Question and AnswerDocument7 pagesDividend Policy Question and AnswerBella CynthiaNo ratings yet

- Cik ListDocument8 pagesCik ListStaurt AttkinsNo ratings yet

- Shruti OberoiDocument4 pagesShruti OberoiManuj OberoiNo ratings yet

Download as pdf or txt

You might also like

- Chapter 7 - Assignment 2Document9 pagesChapter 7 - Assignment 2Gwen Stefani DaugdaugNo ratings yet

- Problem #1 Shares Issuance For Cash: Name: Section: ProfessorDocument14 pagesProblem #1 Shares Issuance For Cash: Name: Section: Professorkakao0% (3)

- Collateral Management GuideDocument20 pagesCollateral Management Guidereggie1010100% (3)

- Argus CrudeDocument28 pagesArgus CrudeAziz SaputraNo ratings yet

- Corporations:Basic Considerations: Module 11-Chapter 14Document16 pagesCorporations:Basic Considerations: Module 11-Chapter 14kakaoNo ratings yet

- Problem 32 Retained Earnings ParcorDocument3 pagesProblem 32 Retained Earnings Parcornikki syNo ratings yet

- Chapter 5 - Corporation - Share TransactionsDocument14 pagesChapter 5 - Corporation - Share Transactionslou-924No ratings yet

- Module 5 - With SolutionsDocument12 pagesModule 5 - With SolutionsStella MarieNo ratings yet

- UM Panabo College 6th Examination Accounting 2a Test I - Multiple Choice Theory. No Erasures AllowedDocument2 pagesUM Panabo College 6th Examination Accounting 2a Test I - Multiple Choice Theory. No Erasures AllowedJessa BeloyNo ratings yet

- Corporation Problems-1Document18 pagesCorporation Problems-1Avia Chelsy DeangNo ratings yet

- Acctg 102 - True or False (Dissolution - Changes in Ownership) Flashcards - QuizletDocument4 pagesAcctg 102 - True or False (Dissolution - Changes in Ownership) Flashcards - QuizletBisag AsaNo ratings yet

- Corp. Retained EarningsDocument9 pagesCorp. Retained EarningshsjhsNo ratings yet

- CorpoDocument16 pagesCorpoErica JoannaNo ratings yet

- ParCor Chapter 5 - Hernandez - BSA 1-1 PDFDocument5 pagesParCor Chapter 5 - Hernandez - BSA 1-1 PDFBSA 1-1No ratings yet

- Partnership LiquidationDocument9 pagesPartnership LiquidationPeter PiperNo ratings yet

- Assignment Bsma 1a April 6Document27 pagesAssignment Bsma 1a April 6Maeca Angela SerranoNo ratings yet

- Cash Priority ProgramDocument1 pageCash Priority Programyela garcia0% (1)

- Chapter 3 ProblemshhhDocument15 pagesChapter 3 Problemshhhahmed arfanNo ratings yet

- Theories ProblemsDocument9 pagesTheories ProblemsKristine Esplana ToraldeNo ratings yet

- Partnership OperationDocument2 pagesPartnership OperationCjhay MarcosNo ratings yet

- CFAS Sample ProblemsDocument5 pagesCFAS Sample ProblemsChristian MartinNo ratings yet

- Retained EarningsDocument3 pagesRetained EarningsChristian Marvin VillanuevaNo ratings yet

- MCQ PartnershipDocument24 pagesMCQ Partnershiplou-924No ratings yet

- 5 2Document8 pages5 2Evelyn MorilloNo ratings yet

- Chpter 1.problem 7.mullesDocument11 pagesChpter 1.problem 7.mullesKim OlimbaNo ratings yet

- ACCTG122 Homework On Partnership LiquidationDocument2 pagesACCTG122 Homework On Partnership LiquidationJoana TrinidadNo ratings yet

- Chapter 11 SampleDocument6 pagesChapter 11 SamplePattraniteNo ratings yet

- Problem No. 1: Journal Entries PROBLEM NO. 5: JE and Statement of Financial Position Books of The Partnership Books of Fish R' UsDocument4 pagesProblem No. 1: Journal Entries PROBLEM NO. 5: JE and Statement of Financial Position Books of The Partnership Books of Fish R' UsJessa0% (1)

- Chap 3 and 4 - ParcorDocument4 pagesChap 3 and 4 - ParcorAnne Gwynneth RadaNo ratings yet

- Solved The Partnership of Angel Investors Began Operations On January 1... - Course HeroDocument2 pagesSolved The Partnership of Angel Investors Began Operations On January 1... - Course HeroeannetiyabNo ratings yet

- Par CorDocument27 pagesPar CorPam LlanetaNo ratings yet

- Win Ballada Parcor Chapter 4 ProblemDocument2 pagesWin Ballada Parcor Chapter 4 ProblemKrngyx100% (1)

- Bam 040 ReviewerDocument7 pagesBam 040 ReviewerAndrea Vila VelascoNo ratings yet

- TOPIC EconDocument44 pagesTOPIC EconChristy HabelNo ratings yet

- CAlAMBA AND SANTIAGO - TUGOTDocument2 pagesCAlAMBA AND SANTIAGO - TUGOTAndrea Tugot100% (1)

- Problem 5Document4 pagesProblem 5Reana ReyesNo ratings yet

- Baral, Malaluan, CastroDocument2 pagesBaral, Malaluan, CastroAndrea TugotNo ratings yet

- Acctg Problem 2-9Document4 pagesAcctg Problem 2-9Honeybunch before100% (1)

- Parcor Proj (Version 1)Document45 pagesParcor Proj (Version 1)Jwhll MaeNo ratings yet

- Accounting Quizzes Answer KeyDocument11 pagesAccounting Quizzes Answer KeyRae SlaughterNo ratings yet

- ParCor Chapter 3 - Hernandez - BSA 1-1 PDFDocument11 pagesParCor Chapter 3 - Hernandez - BSA 1-1 PDFBSA 1-1No ratings yet

- Hi Tech Gen. LedgerDocument14 pagesHi Tech Gen. LedgerjhienellNo ratings yet

- Conceptual Framework and Accounting Standards - Chapter 2 - NotesDocument5 pagesConceptual Framework and Accounting Standards - Chapter 2 - NotesKhey KheyNo ratings yet

- Admission and Retirement of PartnersDocument3 pagesAdmission and Retirement of PartnersJohn Eric MacallaNo ratings yet

- EXAM. MIDTERM. April 20, 2022Document15 pagesEXAM. MIDTERM. April 20, 2022Raziel Angelo AnsusNo ratings yet

- PARCORDocument5 pagesPARCORjelai anselmoNo ratings yet

- Accbp100 2nd Exam Part 1Document2 pagesAccbp100 2nd Exam Part 1emem resuento100% (1)

- Classifications of PartnershipDocument3 pagesClassifications of PartnershipFely MaataNo ratings yet

- Win Ballada Parcor Chapter 4 ProblemDocument2 pagesWin Ballada Parcor Chapter 4 ProblemKrngyxNo ratings yet

- Chapter 2 Problem 9 in Win Ballada ParcorDocument4 pagesChapter 2 Problem 9 in Win Ballada ParcorKatrina PetracheNo ratings yet

- ParCor Chapter 4 - Hernandez - BSA 1-1 PDFDocument7 pagesParCor Chapter 4 - Hernandez - BSA 1-1 PDFBSA 1-1No ratings yet

- ACCOUNTING 2 ReviewDocument4 pagesACCOUNTING 2 ReviewAhnJello100% (1)

- Guide Questions For Chapter 2Document5 pagesGuide Questions For Chapter 2Kathleen Mangual0% (1)

- Win Ballada Parcor Chapter 4 ProblemDocument2 pagesWin Ballada Parcor Chapter 4 ProblemKrngyx0% (1)

- Cfas Theories QuizletDocument4 pagesCfas Theories Quizletagm25No ratings yet

- Chapter 3 ParcorDocument6 pagesChapter 3 ParcorJwhll MaeNo ratings yet

- Par CorDocument11 pagesPar CorIts meh Sushi100% (1)

- Chapter 02Document25 pagesChapter 02Mendoza KlariseNo ratings yet

- 6 Corporation - Share Capital ProblemsDocument2 pages6 Corporation - Share Capital Problemslou-924No ratings yet

- Torrent Downloaded FromDocument4 pagesTorrent Downloaded FromJULIUS L. LEVENNo ratings yet

- ParCor Corpo EQ Set ADocument3 pagesParCor Corpo EQ Set AMara LacsamanaNo ratings yet

- Audit of Shareholders EquityDocument2 pagesAudit of Shareholders EquityGwyneth TorrefloresNo ratings yet

- Quiz - Leases and FSDocument12 pagesQuiz - Leases and FSlou-924No ratings yet

- Cost Accounting-2018-Guerrero-Chapter-3Document21 pagesCost Accounting-2018-Guerrero-Chapter-3lou-924No ratings yet

- GOVACC Final ExaminationDocument10 pagesGOVACC Final Examinationlou-924No ratings yet

- Chapter 13 LeasesDocument13 pagesChapter 13 Leaseslou-924No ratings yet

- Chapter 16 Non Profit OrganizationsDocument28 pagesChapter 16 Non Profit Organizationslou-924No ratings yet

- Cost Accounting-2018-Guerrero-Chapter-1Document83 pagesCost Accounting-2018-Guerrero-Chapter-1lou-924No ratings yet

- Quiz - Intagibles and LiabilitiesDocument6 pagesQuiz - Intagibles and Liabilitieslou-924No ratings yet

- Chapter 12 LiabilitiesDocument19 pagesChapter 12 Liabilitieslou-924No ratings yet

- Cost Accounting-2018-Guerrero-Chapter-2Document32 pagesCost Accounting-2018-Guerrero-Chapter-2lou-924No ratings yet

- MCQ PartnershipDocument24 pagesMCQ Partnershiplou-924No ratings yet

- Partnerships - Formation, Operations, and Changes in Ownership InterestsDocument43 pagesPartnerships - Formation, Operations, and Changes in Ownership Interestslou-924No ratings yet

- Quiz - Merchandising TheoryDocument1 pageQuiz - Merchandising Theorylou-924No ratings yet

- 3 - Partnership DissolutionDocument11 pages3 - Partnership Dissolutionlou-924No ratings yet

- Accounting - Basic ConceptsDocument35 pagesAccounting - Basic Conceptslou-924No ratings yet

- PartnershipsDocument4 pagesPartnershipslou-924No ratings yet

- Questionnaire Evaluation With Factor Analysis and Cronbach's AlphaDocument12 pagesQuestionnaire Evaluation With Factor Analysis and Cronbach's Alphalou-924No ratings yet

- A-Health Medical ClinicDocument2 pagesA-Health Medical Cliniclou-924No ratings yet

- Peer Influence On Risk Taking, Risk Preference, and Risky Decision Making in Adolescence and Adulthood: An Experimental StudyDocument5 pagesPeer Influence On Risk Taking, Risk Preference, and Risky Decision Making in Adolescence and Adulthood: An Experimental Studylou-924No ratings yet

- My Observations On The Journal Article "A Quasi-Experimental Study On Management Coaching Effectiveness"Document6 pagesMy Observations On The Journal Article "A Quasi-Experimental Study On Management Coaching Effectiveness"lou-924No ratings yet

- My Observations On The Journal Article "A Study On The Correlation Between Self Efficacy and Foreign Language Learning Anxiety"Document8 pagesMy Observations On The Journal Article "A Study On The Correlation Between Self Efficacy and Foreign Language Learning Anxiety"lou-924No ratings yet

- My Observations On The Journal Article "A Structural Equation Model of Predictors For Effective Online Learning"Document1 pageMy Observations On The Journal Article "A Structural Equation Model of Predictors For Effective Online Learning"lou-924No ratings yet

- Teachers Make A Difference, What Is The Research Evidence?Document11 pagesTeachers Make A Difference, What Is The Research Evidence?lou-924No ratings yet

- An Exploratory Factor Analysis and Reliability Analysis of The Student Online Learning Readiness (SOLR) InstrumentDocument1 pageAn Exploratory Factor Analysis and Reliability Analysis of The Student Online Learning Readiness (SOLR) Instrumentlou-924No ratings yet

- MCCPDocument4 pagesMCCPSrujan ReddyNo ratings yet

- Daily Equity Market Report - 22.03.2022Document1 pageDaily Equity Market Report - 22.03.2022Fuaad DodooNo ratings yet

- Dividend - UPDATEDDocument83 pagesDividend - UPDATEDAbhishek SinhaNo ratings yet

- How To Handle Your MoneyDocument7 pagesHow To Handle Your Moneypjs150% (1)

- Mflrig 1208160004405181Document2 pagesMflrig 1208160004405181Spam SuhasNo ratings yet

- Procter Gamble v. Bankers TrustDocument22 pagesProcter Gamble v. Bankers Trustthman.workingNo ratings yet

- FD Internal Assessment PaperDocument2 pagesFD Internal Assessment PaperAAKIB HAMDANINo ratings yet

- Russell Indexes Performance: Best PerformingDocument2 pagesRussell Indexes Performance: Best PerformingWilliam HuachisacaNo ratings yet

- Chapter 10 PresentationDocument26 pagesChapter 10 PresentationMega_ImranNo ratings yet

- IIFL - India Info Line - FUNCTION'S OF STOCK MARKET IN INDIA (WITH RESPECT TO LEVEL OF CUSTOMER ADocument88 pagesIIFL - India Info Line - FUNCTION'S OF STOCK MARKET IN INDIA (WITH RESPECT TO LEVEL OF CUSTOMER AVajir BajiNo ratings yet

- F&O P&L Report.Document8 pagesF&O P&L Report.Suresh KumarNo ratings yet

- Yhoo 20110908 SC13D 0Document17 pagesYhoo 20110908 SC13D 0Kara SwisherNo ratings yet

- Suggested Solutions To Chapter 8 Problems: NswerDocument5 pagesSuggested Solutions To Chapter 8 Problems: NsweremilyNo ratings yet

- Chapter 1 - Role of Financial Markets and InstitutionsDocument33 pagesChapter 1 - Role of Financial Markets and InstitutionsJenniferNo ratings yet

- Drago Indjic On Liquidity and Replicators at London Business SchoolDocument31 pagesDrago Indjic On Liquidity and Replicators at London Business SchoolDrago IndjicNo ratings yet

- SEBI Revisits The Concept of Promoter & Promoter GroupDocument10 pagesSEBI Revisits The Concept of Promoter & Promoter GroupAngela JohnNo ratings yet

- Redemption of Preference SharesDocument11 pagesRedemption of Preference SharesRiya SawantNo ratings yet

- Keene, Andrew - Ichimoku Cloud, World's Best Technical IndicatorDocument17 pagesKeene, Andrew - Ichimoku Cloud, World's Best Technical IndicatorihaiNo ratings yet

- Exchange Traded FundDocument2 pagesExchange Traded FundarmailgmNo ratings yet

- CH 20Document22 pagesCH 20sumihosaNo ratings yet

- Mutual Fund DataDocument194 pagesMutual Fund DatashreyaNo ratings yet

- Consistent Profits Through Option Selling 28 12 19 WebinarDocument50 pagesConsistent Profits Through Option Selling 28 12 19 WebinarRahul67% (3)

- Amisignals - ULTIMATEDocument11 pagesAmisignals - ULTIMATEpndymrigankarkaNo ratings yet

- Management CoempensationDocument5 pagesManagement CoempensationSufia Nur KamilaNo ratings yet

- Confirmation: Unit Price Net Debit Security No. of Shares R/R Extension CommissionDocument1 pageConfirmation: Unit Price Net Debit Security No. of Shares R/R Extension CommissionDrw ArcyNo ratings yet

- Dividend Policy Question and AnswerDocument7 pagesDividend Policy Question and AnswerBella CynthiaNo ratings yet

- Cik ListDocument8 pagesCik ListStaurt AttkinsNo ratings yet

- Shruti OberoiDocument4 pagesShruti OberoiManuj OberoiNo ratings yet