Download as docx, pdf, or txt

You might also like

- Financial Accounting IFRS Student Mark Plan June 2019Document16 pagesFinancial Accounting IFRS Student Mark Plan June 2019scottNo ratings yet

- 2019 Vol 1 CH 5 AnswersDocument21 pages2019 Vol 1 CH 5 AnswersArkhie Davocol80% (5)

- Case 3Document13 pagesCase 3Prezi Toli100% (1)

- Problem: Andres Adi Putra S 43220110067 AKM2-Forum 6Document17 pagesProblem: Andres Adi Putra S 43220110067 AKM2-Forum 6tes doangNo ratings yet

- Workshop 2 Qs As Introduction To A FDocument18 pagesWorkshop 2 Qs As Introduction To A FYeoh Tze ShinNo ratings yet

- Applied Group Fin Reporting-Changes in Group Structure PDFDocument25 pagesApplied Group Fin Reporting-Changes in Group Structure PDFObey SitholeNo ratings yet

- Cashflow Analysis - Beta - GammaDocument14 pagesCashflow Analysis - Beta - Gammashahin selkarNo ratings yet

- 2016 December Financial Reporting L1 PDFDocument158 pages2016 December Financial Reporting L1 PDFDixie Cheelo100% (2)

- Basel II CheatsheetDocument8 pagesBasel II CheatsheetBhabaniParidaNo ratings yet

- Competency Exam Practice-211Document5 pagesCompetency Exam Practice-211marites yuNo ratings yet

- Half - Prime Bank 1st ICB AMCL Mutual Fund 10-11Document1 pageHalf - Prime Bank 1st ICB AMCL Mutual Fund 10-11Abrar FaisalNo ratings yet

- HKICPA QP Exam (Module A) Sep2008 Question PaperDocument9 pagesHKICPA QP Exam (Module A) Sep2008 Question Papercynthia tsui67% (3)

- Final Financial Reporting AssessmentDocument23 pagesFinal Financial Reporting Assessmentapi-413236814No ratings yet

- CH 1 Exhibit 1 Q 1-5Document6 pagesCH 1 Exhibit 1 Q 1-5ЭниЭ.No ratings yet

- 2019 Vol 1 CH 5 AnswersDocument23 pages2019 Vol 1 CH 5 AnswersDummy Number 2No ratings yet

- Compound Financial InstrumentDocument2 pagesCompound Financial Instrumenthae1234No ratings yet

- Review Accounting 1Document9 pagesReview Accounting 1jhouvanNo ratings yet

- Proposal Tanaman MelonDocument3 pagesProposal Tanaman Melondr walferNo ratings yet

- Running Head: Financial AccountingDocument9 pagesRunning Head: Financial AccountingKashémNo ratings yet

- NoneDocument1 pageNoneDonny EmanuelNo ratings yet

- Receipts and Payments AccountDocument2 pagesReceipts and Payments AccountUmapathi MNo ratings yet

- Bac 3 Review QNSDocument16 pagesBac 3 Review QNSsaidkhatib368No ratings yet

- 2021 - A2S2 Solution-OplossingDocument19 pages2021 - A2S2 Solution-OplossingmeghdyckNo ratings yet

- Statement of Cash Flows HandoutDocument17 pagesStatement of Cash Flows HandoutCharudatta MundeNo ratings yet

- Trading Securities and FA at FV Through OCI and FA at Amortized Cost (Prob 21-25)Document11 pagesTrading Securities and FA at FV Through OCI and FA at Amortized Cost (Prob 21-25)Lorence Patrick LapidezNo ratings yet

- Topic 4 Tutorial QuestionsDocument5 pagesTopic 4 Tutorial QuestionsAbigailNo ratings yet

- Chapter 17 In-Class Problems SolutionDocument6 pagesChapter 17 In-Class Problems Solutionliuxuhan3No ratings yet

- Plug (Parent) Spark (Subsidary) Lemon (Non Affiliate)Document25 pagesPlug (Parent) Spark (Subsidary) Lemon (Non Affiliate)Pasha HarahapNo ratings yet

- Problem 8-9 Akl 2Document4 pagesProblem 8-9 Akl 2andi nanaNo ratings yet

- 2023-Vol-1-Ch-3-Problems-Ans 3Document12 pages2023-Vol-1-Ch-3-Problems-Ans 3Glen ValdezcoNo ratings yet

- Jawaban Soal UTS Akuntansi Keu - MenengahDocument4 pagesJawaban Soal UTS Akuntansi Keu - MenengahJessinthaNo ratings yet

- Pascal Mosa Ananda W - Latihan KP Financial Accounting 2Document14 pagesPascal Mosa Ananda W - Latihan KP Financial Accounting 2Brenda FreitasNo ratings yet

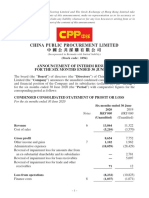

- China Public Procurement Limited 中 國 公 共 採 購 有 限 公 司Document37 pagesChina Public Procurement Limited 中 國 公 共 採 購 有 限 公 司in resNo ratings yet

- 21 Problems - and - Answers - Reclassification - of - Financial - AssetDocument30 pages21 Problems - and - Answers - Reclassification - of - Financial - AssetSheila Grace BajaNo ratings yet

- Trident, Inc. Consolidated Balance Sheets: Execonline - Mastering Finance FundamentalsDocument3 pagesTrident, Inc. Consolidated Balance Sheets: Execonline - Mastering Finance Fundamentalschemicalchouhan9303No ratings yet

- Section B:: 1. Are The Following Balance Sheet Items (A) Assets, (L) Liabilities, or (E) Stockholders' Equity?Document11 pagesSection B:: 1. Are The Following Balance Sheet Items (A) Assets, (L) Liabilities, or (E) Stockholders' Equity?18071369 Nguyễn ThànhNo ratings yet

- Exercises Chapter 4 Group 4Document5 pagesExercises Chapter 4 Group 4Phạm Ngọc Uyên NhiNo ratings yet

- The Examiner's Answers F2 - Financial Management March 2013: Section ADocument18 pagesThe Examiner's Answers F2 - Financial Management March 2013: Section Amd salehinNo ratings yet

- What A ProblemDocument4 pagesWhat A ProblemEleazar SalazarNo ratings yet

- 2019 Vol 1 CH 3 AnswersDocument14 pages2019 Vol 1 CH 3 AnswersMarjorie NepomucenoNo ratings yet

- HR Welfare Society 13-10-13Document11 pagesHR Welfare Society 13-10-13WazedZayedNo ratings yet

- 2-8 - Solutions To Practice Questions (Amended For TXT Update)Document3 pages2-8 - Solutions To Practice Questions (Amended For TXT Update)PatNo ratings yet

- Investments in Debt SecuritiesDocument34 pagesInvestments in Debt SecuritiesNobu NobuNo ratings yet

- Prepare Statements of FinancialDocument5 pagesPrepare Statements of FinancialNguyễn Ngọc HàNo ratings yet

- Investment in Associate ExercisesDocument7 pagesInvestment in Associate ExercisesJo KeNo ratings yet

- Intermediate Accounting CH 8 Vol 1 2012 AnswersDocument6 pagesIntermediate Accounting CH 8 Vol 1 2012 AnswersPrincessAngelaDeLeon100% (5)

- Chapter 9 Intercompany Bond Holdings and Miscellaneous Topics-Consolidated Financial StatementsDocument45 pagesChapter 9 Intercompany Bond Holdings and Miscellaneous Topics-Consolidated Financial StatementsAchmad RizalNo ratings yet

- Bishop Group (IAS-21 + Cashflow) : Cfap 1: A A F RDocument1 pageBishop Group (IAS-21 + Cashflow) : Cfap 1: A A F R.No ratings yet

- Psaf Revision Day 3 May 2023Document8 pagesPsaf Revision Day 3 May 2023Esther AkpanNo ratings yet

- Statement of Cash Flows Lecture Questions and AnswersDocument9 pagesStatement of Cash Flows Lecture Questions and AnswersSaaniya AbbasiNo ratings yet

- Accounting IAS (Malaysia) Model Answers Series 2 2005 Old SyllabusDocument20 pagesAccounting IAS (Malaysia) Model Answers Series 2 2005 Old SyllabusAung Zaw HtweNo ratings yet

- Gmernacej W5C5 AssigmentOLDDocument6 pagesGmernacej W5C5 AssigmentOLDalmaNo ratings yet

- Prob 7Document1 pageProb 7Angelia TNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Securities Brokerage Revenues World Summary: Market Values & Financials by CountryFrom EverandSecurities Brokerage Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Using Economic Indicators to Improve Investment AnalysisFrom EverandUsing Economic Indicators to Improve Investment AnalysisRating: 3.5 out of 5 stars3.5/5 (1)

- INVESTMENT PROJECTS TO GENERATE POSITIVE RATES OF RETURN in CONDITIONS OF NEAR ZERO or NEGATIVE INTEREST RATESFrom EverandINVESTMENT PROJECTS TO GENERATE POSITIVE RATES OF RETURN in CONDITIONS OF NEAR ZERO or NEGATIVE INTEREST RATESNo ratings yet

- 2011 Accounting: For Office Use Only Attach Sace Registration Number Label To This BoxDocument33 pages2011 Accounting: For Office Use Only Attach Sace Registration Number Label To This BoxRaymond RayNo ratings yet

- Capital Market Review and Outlook: AnnualDocument20 pagesCapital Market Review and Outlook: AnnualbigaNo ratings yet

- Mutual Fund Pass4sureDocument394 pagesMutual Fund Pass4surerohini.flyasiaNo ratings yet

- Rental Investment ReportDocument5 pagesRental Investment ReportTuba TunaNo ratings yet

- InvoiceDocument1 pageInvoiceDaya shankarNo ratings yet

- Stages of Dtec Application - Jan 2019Document1 pageStages of Dtec Application - Jan 2019Sami AlasadNo ratings yet

- Optimal Capital StructureDocument13 pagesOptimal Capital StructureScarlet SalongaNo ratings yet

- Altisource IIM A JDDocument2 pagesAltisource IIM A JDBipin Bansal AgarwalNo ratings yet

- Summary International Accounting Chap 4Document2 pagesSummary International Accounting Chap 4RisantiNo ratings yet

- Chapter 1 - 1 IFMDocument24 pagesChapter 1 - 1 IFMVaibhav PandeyNo ratings yet

- FM Chap 1Document12 pagesFM Chap 1Mubarek AsefaNo ratings yet

- 1 LifeInsur-E311-2022-10-9ED (001-044)Document44 pages1 LifeInsur-E311-2022-10-9ED (001-044)bruno.dematteisk47No ratings yet

- Capital Budgeting Assignment QuestionsDocument3 pagesCapital Budgeting Assignment QuestionsNgaiza3No ratings yet

- DMMR CVP MathDocument2 pagesDMMR CVP MathSabbir ZamanNo ratings yet

- Government of Andhra Pradesh Police Department:: Appco: M E N UDocument1 pageGovernment of Andhra Pradesh Police Department:: Appco: M E N U5532024 SAI KRISHNA.CHNo ratings yet

- Business Accounting Standard - LithuaniaDocument9 pagesBusiness Accounting Standard - Lithuaniafleur de VieNo ratings yet

- Level I of The CFA ProgramDocument8 pagesLevel I of The CFA ProgramSachinNo ratings yet

- Bestbuy Turn Around StrategyDocument13 pagesBestbuy Turn Around StrategyRajendra Yadav100% (1)

- 1st Term s1 Financial AccountDocument21 pages1st Term s1 Financial AccountAsabia OmoniyiNo ratings yet

- Message 1Document7 pagesMessage 1Zyad UziNo ratings yet

- Business Law MCQDocument4 pagesBusiness Law MCQPoonam PraveenNo ratings yet

- Lease vs. Purchase Analysis: Fast Tools & ResourcesDocument11 pagesLease vs. Purchase Analysis: Fast Tools & ResourcesTom ReillyNo ratings yet

- Annual Administration Report ProfarmaDocument4 pagesAnnual Administration Report ProfarmacherryprasaadNo ratings yet

- Systematic Risk Vs Unsystematic RiskDocument2 pagesSystematic Risk Vs Unsystematic RiskJayesh PatelNo ratings yet

- Acc 106 - Sas 2Document13 pagesAcc 106 - Sas 2bakdbdkNo ratings yet

- 10 Funds Flow StatementDocument13 pages10 Funds Flow Statementankush sardanaNo ratings yet

- Treasury Yield Curve RatesDocument34 pagesTreasury Yield Curve RatesmatthyllandNo ratings yet

- Sample Paperpre Board II Acct 2324-2Document10 pagesSample Paperpre Board II Acct 2324-2kanakchauhan206No ratings yet

- Blue Ridge Bank 2017 Annual ReportDocument48 pagesBlue Ridge Bank 2017 Annual ReportFauquier NowNo ratings yet