Download as pdf or txt

You might also like

- Strategic Planning and Capital BudgetingDocument32 pagesStrategic Planning and Capital BudgetingKeeiiiyyttt Joie100% (5)

- Managerial Accounting Excel Project 2Document8 pagesManagerial Accounting Excel Project 2John GuerreroNo ratings yet

- Intermediate Accounting 1: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 1: a QuickStudy Digital Reference GuideNo ratings yet

- Value-based financial management: Towards a Systematic Process for Financial Decision - MakingFrom EverandValue-based financial management: Towards a Systematic Process for Financial Decision - MakingNo ratings yet

- Financial Reporting PDFDocument67 pagesFinancial Reporting PDFlukamasia93% (15)

- Other AssignmentsDocument27 pagesOther AssignmentsAli AhmedNo ratings yet

- Framework of Financial AnalysisDocument7 pagesFramework of Financial AnalysismkhanmajlisNo ratings yet

- Management Acctg. Qualitative Characteristics of Financial StatementsDocument71 pagesManagement Acctg. Qualitative Characteristics of Financial StatementsasiegrainenicoleNo ratings yet

- Financial ReportingDocument133 pagesFinancial ReportingJOHN KAMANDANo ratings yet

- Fsa Notes 2023Document44 pagesFsa Notes 2023Kiptoon CollinsNo ratings yet

- Conceptual Framework of AccountingDocument3 pagesConceptual Framework of AccountingJoanna Phaye VilbarNo ratings yet

- Financial ReportingDocument133 pagesFinancial ReportingClerry SamuelNo ratings yet

- Contemporary Ch2 NotesDocument3 pagesContemporary Ch2 NotesdhfbbbbbbbbbbbbbbbbbhNo ratings yet

- F. Understanding The Financial Statement and Its Components Sahid P.ADocument10 pagesF. Understanding The Financial Statement and Its Components Sahid P.Aantonette.escobia17No ratings yet

- Financial StatementsDocument49 pagesFinancial Statementsfietha67% (3)

- M1 Handout 4 Conceptual Framework of AccountingDocument9 pagesM1 Handout 4 Conceptual Framework of AccountingAmelia TaylorNo ratings yet

- Graded Forum - 070921 Financial Statement ReportingDocument3 pagesGraded Forum - 070921 Financial Statement ReportingheyNo ratings yet

- Module 2 Conceptual Framework For Financial ReportingDocument9 pagesModule 2 Conceptual Framework For Financial ReportingVivo V27No ratings yet

- Financial Statements Analyses and Their Implications To ManagementDocument9 pagesFinancial Statements Analyses and Their Implications To ManagementMarie Frances SaysonNo ratings yet

- #02 Conceptual FrameworkDocument5 pages#02 Conceptual FrameworkZaaavnn VannnnnNo ratings yet

- The Objective of General Purpose Financial ReportingDocument86 pagesThe Objective of General Purpose Financial ReportingAlex liaoNo ratings yet

- Jawaban Assigment CH 1Document5 pagesJawaban Assigment CH 1AjiwNo ratings yet

- PWC Understanding Financial Statement AuditDocument18 pagesPWC Understanding Financial Statement AuditAries BautistaNo ratings yet

- FR & FasDocument195 pagesFR & FasPrerana SharmaNo ratings yet

- Financial Statement Analysis: Assignment OnDocument6 pagesFinancial Statement Analysis: Assignment OnMd Ohidur RahmanNo ratings yet

- Introduction To Financial Statement AuditDocument63 pagesIntroduction To Financial Statement AuditRica RegorisNo ratings yet

- AC201 Notes PART 1Document25 pagesAC201 Notes PART 1mollymgonigle1No ratings yet

- Financial Analysis of Wipro LTD PDFDocument25 pagesFinancial Analysis of Wipro LTD PDFMridul sharda100% (2)

- Chapter 1 - AACA P1Document7 pagesChapter 1 - AACA P1Toni Rose Hernandez LualhatiNo ratings yet

- CH 6 TADocument47 pagesCH 6 TAVera NitaNo ratings yet

- Unit Four: Audit Responsibilities and ObjectivesDocument44 pagesUnit Four: Audit Responsibilities and ObjectiveseferemNo ratings yet

- Group 1 Chapter 1 The Demand For Auditing and Assurance ServicesDocument23 pagesGroup 1 Chapter 1 The Demand For Auditing and Assurance ServicestristahmncdldyNo ratings yet

- The Conceptual Framework For Financial ReportingDocument32 pagesThe Conceptual Framework For Financial ReportingDINIE RUZAINI BINTI MOH ZAINUDINNo ratings yet

- MaterialityDocument7 pagesMaterialityRogers256No ratings yet

- Dwnload Full Financial Reporting and Analysis 5th Edition Revsine Solutions Manual PDFDocument35 pagesDwnload Full Financial Reporting and Analysis 5th Edition Revsine Solutions Manual PDFinactionwantwit.a8i0100% (16)

- Document 7Document12 pagesDocument 7Ram PagongNo ratings yet

- Case Study - 1Document5 pagesCase Study - 1Jordan BimandamaNo ratings yet

- Financial Statement I: The Income StatementDocument46 pagesFinancial Statement I: The Income StatementYousef ShahwanNo ratings yet

- Chapter One An Overview of AuditingDocument9 pagesChapter One An Overview of AuditingMulatu LombamoNo ratings yet

- ACCOUNTING - FOR - LAWYERS: Source DocumentsDocument45 pagesACCOUNTING - FOR - LAWYERS: Source DocumentsWHATSAPPs VIDEOS STATUSNo ratings yet

- IASB Conceptual FrameworkDocument26 pagesIASB Conceptual FrameworkALEXERIK23100% (4)

- Test 1Document4 pagesTest 1Leslie CarrollNo ratings yet

- Financial Statement AnalysisDocument27 pagesFinancial Statement AnalysisJayvee Balino100% (1)

- Chapter 1: The Objective of General Purpose Financial ReportingDocument22 pagesChapter 1: The Objective of General Purpose Financial ReportingSteven TanNo ratings yet

- Conceptual Framework2Document2 pagesConceptual Framework2iamivanbasas100% (1)

- Aas 16 Going ConcernDocument5 pagesAas 16 Going ConcernRishabh GuptaNo ratings yet

- Review Na Sa Conceptual FrameworkDocument5 pagesReview Na Sa Conceptual FrameworkMARY ROSENo ratings yet

- Sap 1012Document30 pagesSap 1012AndreiNo ratings yet

- Isa 550 & Isa 570Document56 pagesIsa 550 & Isa 570sajida mohdNo ratings yet

- ISA 550 & 570 - PresentationDocument25 pagesISA 550 & 570 - Presentationsajida mohdNo ratings yet

- Accounting Conventions: Monetary MeasurementDocument5 pagesAccounting Conventions: Monetary MeasurementAli HaiderNo ratings yet

- Accounting For Lawyers by Solicitor KatuDocument45 pagesAccounting For Lawyers by Solicitor KatuFrancisco Hagai GeorgeNo ratings yet

- 01 - ASC FrameworkDocument8 pages01 - ASC FrameworkralphalonzoNo ratings yet

- Narrative - Assumptions and ISFDocument10 pagesNarrative - Assumptions and ISFKatrizia FauniNo ratings yet

- UntitledDocument42 pagesUntitledKara Sophia BatucanNo ratings yet

- UntitledDocument35 pagesUntitledKara Sophia BatucanNo ratings yet

- Babe OyeDocument4 pagesBabe Oyejashanvipan1290No ratings yet

- Seminar AuditDocument7 pagesSeminar AuditMichael BusuiocNo ratings yet

- Audit Risk Alert: General Accounting and Auditing Developments, 2017/18From EverandAudit Risk Alert: General Accounting and Auditing Developments, 2017/18No ratings yet

- Finance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersFrom EverandFinance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersNo ratings yet

- Transparency in Financial Reporting: A concise comparison of IFRS and US GAAPFrom EverandTransparency in Financial Reporting: A concise comparison of IFRS and US GAAPRating: 4.5 out of 5 stars4.5/5 (3)

- Master BudgetDocument27 pagesMaster BudgetDawn Juliana AranNo ratings yet

- FM Vs MaDocument1 pageFM Vs MaDawn Juliana AranNo ratings yet

- B Mathweek3Document1 pageB Mathweek3Dawn Juliana AranNo ratings yet

- Capital-Budgeting (Managerial Accounting)Document12 pagesCapital-Budgeting (Managerial Accounting)Dawn Juliana AranNo ratings yet

- Module 3 Quality ReportsDocument1 pageModule 3 Quality ReportsDawn Juliana AranNo ratings yet

- CPAweek 1Document4 pagesCPAweek 1Dawn Juliana AranNo ratings yet

- Math 1 Module 4Document58 pagesMath 1 Module 4Dawn Juliana AranNo ratings yet

- Module 6 Business MeetingsDocument16 pagesModule 6 Business MeetingsDawn Juliana Aran100% (1)

- Purposive Communication ReviewerDocument19 pagesPurposive Communication ReviewerDawn Juliana AranNo ratings yet

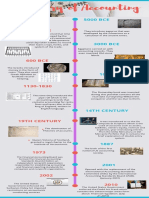

- Accounting HistoryDocument1 pageAccounting HistoryDawn Juliana AranNo ratings yet

- Module 8 - Simple Interest and Compound InterestDocument11 pagesModule 8 - Simple Interest and Compound InterestDawn Juliana AranNo ratings yet

- Philippine RevolutionDocument24 pagesPhilippine RevolutionDawn Juliana AranNo ratings yet

- Case Study-ABAKADA CompanyDocument3 pagesCase Study-ABAKADA CompanyDawn Juliana Aran100% (1)

- Module 1 HistDocument27 pagesModule 1 HistDawn Juliana AranNo ratings yet

- Case Study: Guide QuestionsDocument1 pageCase Study: Guide QuestionsDawn Juliana AranNo ratings yet

- A Study Applying DCF Technique For Valuing Indian IPO's Case Studies of CCDDocument11 pagesA Study Applying DCF Technique For Valuing Indian IPO's Case Studies of CCDarcherselevators100% (1)

- NCC Bank RatiosDocument20 pagesNCC Bank RatiosRahnoma Bilkis NavaidNo ratings yet

- BSTDB Financial Statements For 2020Document72 pagesBSTDB Financial Statements For 2020Isabela VelicariaNo ratings yet

- The Dark Side of Valuation (Slides)Document98 pagesThe Dark Side of Valuation (Slides)Johnathan Fitz KennedyNo ratings yet

- Question 1Document29 pagesQuestion 1Fierdzz XieeraNo ratings yet

- Fischer - Pship LiquiDocument7 pagesFischer - Pship LiquiShawn Michael DoluntapNo ratings yet

- Quiz DepletionDocument5 pagesQuiz Depletionhoneyjoy salapantanNo ratings yet

- Chapter 2-Test Material 2 1Document7 pagesChapter 2-Test Material 2 1Marcus MonocayNo ratings yet

- CHUMISMITA DAS - DTP & Xerox ShopDocument15 pagesCHUMISMITA DAS - DTP & Xerox Shophiranyadas611No ratings yet

- Ipsas 12 and Ipsas 27Document14 pagesIpsas 12 and Ipsas 27Kidanu Taye TerfaNo ratings yet

- Chapter 2 StudentDocument76 pagesChapter 2 StudentKiều PhươngNo ratings yet

- 2008 HSBC Annual Report and Accounts EnglishDocument34 pages2008 HSBC Annual Report and Accounts EnglishigharieebNo ratings yet

- Topic 2 Installment Sales Module Part 1Document5 pagesTopic 2 Installment Sales Module Part 1Maricel Ann BaccayNo ratings yet

- ProFormaDivisionProfitability Q2Document2 pagesProFormaDivisionProfitability Q2drashteeNo ratings yet

- Theories FAR - Special TopicsDocument17 pagesTheories FAR - Special TopicsLuiNo ratings yet

- Asian Paints Ltd. (India) : SourceDocument6 pagesAsian Paints Ltd. (India) : SourceDivyagarapatiNo ratings yet

- C V P AnalysisDocument8 pagesC V P AnalysisDinesh PantNo ratings yet

- Applied Auditing Audit of Intangibles and Correction of ErrorsDocument2 pagesApplied Auditing Audit of Intangibles and Correction of ErrorsCar Mae La67% (3)

- Exam 2 Practice Problems AnswersDocument6 pagesExam 2 Practice Problems Answersoizys131No ratings yet

- Ud WirastriDocument18 pagesUd WirastriyumamhrnptrNo ratings yet

- Finma 4 Prelim ResearchDocument10 pagesFinma 4 Prelim Researchfrescy mosterNo ratings yet

- CFAS Quiz Questions AddedDocument2 pagesCFAS Quiz Questions AddedSaeym SegoviaNo ratings yet

- CMA5E01Document12 pagesCMA5E01Rafael GarciaNo ratings yet

- Beximco PHARMACEUTICALS LTD ISDocument2 pagesBeximco PHARMACEUTICALS LTD ISSuny ChowdhuryNo ratings yet

- Ultralift Corp Manufactures Chain Hoists The Raw Materials Inventories OnDocument3 pagesUltralift Corp Manufactures Chain Hoists The Raw Materials Inventories OnAmit PandeyNo ratings yet

- CHP 1 & 3 QuestionsDocument3 pagesCHP 1 & 3 QuestionschengNo ratings yet

- Valuation Concepts and Methods EssayDocument2 pagesValuation Concepts and Methods EssayChristine MadecNo ratings yet

- CAF-1 Over All Lecture Notes of Pre Batch (Without Basics)Document35 pagesCAF-1 Over All Lecture Notes of Pre Batch (Without Basics)Bushra AsgharNo ratings yet