Download as pdf or txt

You might also like

- HR Report (LEON)Document12 pagesHR Report (LEON)ZeeNo ratings yet

- P&G SK-II Version 2Document2 pagesP&G SK-II Version 2Billy Jostar100% (2)

- Problems P 15-1 Apply Threshold Tests: Net Income Tax RateDocument2 pagesProblems P 15-1 Apply Threshold Tests: Net Income Tax Rateardi yansyahNo ratings yet

- COVID-19 Outbreak and Sectoral Performance of The Australian Stock Market: An Event Study AnalysisDocument15 pagesCOVID-19 Outbreak and Sectoral Performance of The Australian Stock Market: An Event Study AnalysisMd. Mahmudul AlamNo ratings yet

- Growth and Investment: 25000 5000 6000 7000 New Cases (7 Day MA) Total Deaths (RHS)Document16 pagesGrowth and Investment: 25000 5000 6000 7000 New Cases (7 Day MA) Total Deaths (RHS)Rk SunnyNo ratings yet

- Appraisal: Heraeus PreciousDocument4 pagesAppraisal: Heraeus PreciousdnikosdNo ratings yet

- South Korea Chart Book: An Improving Cycle Vulnerable To Trade WarsDocument8 pagesSouth Korea Chart Book: An Improving Cycle Vulnerable To Trade Warsbillroberts981No ratings yet

- China - Should We Worry About The Falling FDIDocument8 pagesChina - Should We Worry About The Falling FDISumanth GururajNo ratings yet

- AECOM Market Forecast Q2 2020 FINALDocument11 pagesAECOM Market Forecast Q2 2020 FINALMahmoud MoussaNo ratings yet

- MMF & RMG Update H1FY21: November 2020Document6 pagesMMF & RMG Update H1FY21: November 2020shahavNo ratings yet

- Corporate FinancialDocument15 pagesCorporate FinancialBenzon Agojo OndovillaNo ratings yet

- Engineering and Capital GoodsDocument44 pagesEngineering and Capital Goodsayusht7iNo ratings yet

- Indian Econ SnapshotDocument21 pagesIndian Econ SnapshotAshish JainNo ratings yet

- CH 1Document37 pagesCH 1Pablo ValdezNo ratings yet

- Navigating The RecoveriesDocument20 pagesNavigating The Recoveriesaw333No ratings yet

- DuyMinh Presentation 18th Oct-đã chuyển đổiDocument23 pagesDuyMinh Presentation 18th Oct-đã chuyển đổilearnit learnitNo ratings yet

- Global Outlook 2022: Five Key Questions For 2022Document26 pagesGlobal Outlook 2022: Five Key Questions For 2022Alfredo HutapeaNo ratings yet

- GDP and TrendsDocument3 pagesGDP and TrendsManish SatapathyNo ratings yet

- 06 Capital MarketsDocument16 pages06 Capital MarketsSadia AbidNo ratings yet

- OCBC NISP Market Outlook 2021 - Steven Yudha - AshmoreDocument16 pagesOCBC NISP Market Outlook 2021 - Steven Yudha - AshmoreNurul Meutia SalsabilaNo ratings yet

- UntitledDocument235 pagesUntitledQuynh VoNo ratings yet

- Goldman Sachs Russia Economic Activity and Policy Tracker - MayDocument5 pagesGoldman Sachs Russia Economic Activity and Policy Tracker - MayRoadtosuccessNo ratings yet

- The Appliance Market: Core MarketsDocument4 pagesThe Appliance Market: Core MarketsKatarzyna LipińskaNo ratings yet

- V. Marketing Plan: SWOT Analysis StrengthsDocument7 pagesV. Marketing Plan: SWOT Analysis StrengthsA cNo ratings yet

- Economic Update December 2021Document16 pagesEconomic Update December 2021shad.jawdNo ratings yet

- India Retail Report Aug 2022Document35 pagesIndia Retail Report Aug 2022Ravishankar SokkarNo ratings yet

- Indonesia Property Market Overview Recent Update in Transition Period 190920 01Document20 pagesIndonesia Property Market Overview Recent Update in Transition Period 190920 01rimuru samaNo ratings yet

- VIC - 4Q2023 - Earnings Presentation - VFDocument37 pagesVIC - 4Q2023 - Earnings Presentation - VFDương ChâuNo ratings yet

- ICICI Action Construction EquipmentDocument7 pagesICICI Action Construction Equipmentsuman sekhar dekaNo ratings yet

- MMR 2024-04 enDocument32 pagesMMR 2024-04 enVMNo ratings yet

- Top 100 CompaniiDocument34 pagesTop 100 CompaniiDan MarianNo ratings yet

- The Economist Global Economic Outlook 2022, Explaining The Main Drags On Global Growth 2022Document9 pagesThe Economist Global Economic Outlook 2022, Explaining The Main Drags On Global Growth 2022SergioNo ratings yet

- China and India in The Global Economy: A Cooperative Knowledge-Based A Cooperative Knowledge Based Development StrategyDocument23 pagesChina and India in The Global Economy: A Cooperative Knowledge-Based A Cooperative Knowledge Based Development Strategyguysmart08No ratings yet

- Valuations Amidst The COVID-19 Pandemic & Significant Economic UncertaintiesDocument19 pagesValuations Amidst The COVID-19 Pandemic & Significant Economic Uncertaintiesikhan809No ratings yet

- Food Sector - Fruits & VegetablesDocument17 pagesFood Sector - Fruits & Vegetablesgaurav khatriNo ratings yet

- Indonesia Trade Policies and UpdatesDocument27 pagesIndonesia Trade Policies and UpdateskennydoggyuNo ratings yet

- WP5: Scenario & Market Strategies (Energy) : Med-Csp Concentrating Solar Power For The Mediterranean RegionDocument44 pagesWP5: Scenario & Market Strategies (Energy) : Med-Csp Concentrating Solar Power For The Mediterranean Regionknowledge3736 jNo ratings yet

- Retail August 2023Document35 pagesRetail August 2023Avishkar PNo ratings yet

- Unctad Oecd2023d30 enDocument23 pagesUnctad Oecd2023d30 enVikram VermaNo ratings yet

- 2nd Quarter 2020 GIPC Investment ReportDocument9 pages2nd Quarter 2020 GIPC Investment ReportFuaad DodooNo ratings yet

- Pharmaceutical Industry - CDPDocument20 pagesPharmaceutical Industry - CDPhasnain114No ratings yet

- Chapter 3.figure 3.2. Business and Public Investment Have Expanded Global Research Capacity Version 1 - Last Updated: 06-Oct-2016Document10 pagesChapter 3.figure 3.2. Business and Public Investment Have Expanded Global Research Capacity Version 1 - Last Updated: 06-Oct-2016ana mariaNo ratings yet

- Course Title: Principles of Macroeconomics Course Code: ECON 2013 Assignment NoDocument6 pagesCourse Title: Principles of Macroeconomics Course Code: ECON 2013 Assignment Nohania sheikhNo ratings yet

- 2018 Eurobank Market ReportDocument24 pages2018 Eurobank Market ReportDeva RajaNo ratings yet

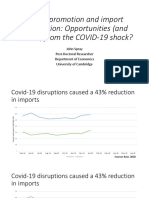

- 3 1 Spray Export Promotion and Import SubstitutionDocument15 pages3 1 Spray Export Promotion and Import SubstitutionHarsh MehtaNo ratings yet

- Gulshan PolyolsDocument41 pagesGulshan Polyolssachinmittal.nitkNo ratings yet

- Desktop KPI PromoterDocument14 pagesDesktop KPI PromoterGatot SentonoNo ratings yet

- Hong Kong Monetary AuthorityDocument62 pagesHong Kong Monetary Authoritygcsblue stacksNo ratings yet

- January 2021Document20 pagesJanuary 2021Panache ZNo ratings yet

- FalconDocument15 pagesFalconJoseph EffiongNo ratings yet

- AOFM Investor Insights Issue 9 December 2021Document9 pagesAOFM Investor Insights Issue 9 December 2021Rodrigo FujimotoNo ratings yet

- Weekly Epi Update 19Document21 pagesWeekly Epi Update 19hanifahNo ratings yet

- Euro China Investment Report 2013/2014: The Antwerp Forum 26.09.2013Document69 pagesEuro China Investment Report 2013/2014: The Antwerp Forum 26.09.2013guo_georgeNo ratings yet

- Oxford Economics Global Economic Outlook On The Cusp of ADocument10 pagesOxford Economics Global Economic Outlook On The Cusp of ABrainNo ratings yet

- India Chartbook July 2019Document63 pagesIndia Chartbook July 2019Himesh ShahNo ratings yet

- Retail July 2021Document35 pagesRetail July 2021digen parikhNo ratings yet

- EU Energy Crisis Sparked by Ukraine War To Create Blackouts in Poor Countries - BloombergDocument8 pagesEU Energy Crisis Sparked by Ukraine War To Create Blackouts in Poor Countries - BloombergShivam BoseNo ratings yet

- Assignment 2 CoronaDocument2 pagesAssignment 2 CoronasumeetkantkaulNo ratings yet

- Retail November 2021Document35 pagesRetail November 2021AyazNo ratings yet

- 66339e4aaf770 Case Study OpsDocument2 pages66339e4aaf770 Case Study Opspriyansh sharma 8053No ratings yet

- Economic Indicators for Southeast Asia and the Pacific: Input–Output TablesFrom EverandEconomic Indicators for Southeast Asia and the Pacific: Input–Output TablesNo ratings yet

- Resources and Energy Quarterly March 2021Document171 pagesResources and Energy Quarterly March 2021JarodNo ratings yet

- Sheet Prices Move Lower Across Key Markets: April 2013Document21 pagesSheet Prices Move Lower Across Key Markets: April 2013musehopeNo ratings yet

- Shanzhai Case Study DocumentDocument7 pagesShanzhai Case Study Documentthomas_joseph_18No ratings yet

- Johnson & Johnson: Caring For People, Worldwide: Nilanjan Sengupta & Mousumi SenguptaDocument40 pagesJohnson & Johnson: Caring For People, Worldwide: Nilanjan Sengupta & Mousumi SenguptaRaavananNo ratings yet

- CAS Report SitharaDocument7 pagesCAS Report SitharaNAVYA PNo ratings yet

- V Textiles 2015-16 ArDocument100 pagesV Textiles 2015-16 ArThe Himalayas 360No ratings yet

- GBS - Mid T Exam 16-99599-3Document11 pagesGBS - Mid T Exam 16-99599-3Likhon RahmanNo ratings yet

- Advancing Climate Resilience in ASEAN: MARCH 2020Document36 pagesAdvancing Climate Resilience in ASEAN: MARCH 2020Lutfi ZaidanNo ratings yet

- SHTGDocument7 pagesSHTGBarby WoohooNo ratings yet

- Global Weekly Economic Update - Deloitte InsightsDocument34 pagesGlobal Weekly Economic Update - Deloitte InsightsGANGULYABHILASHANo ratings yet

- Alternative Centres of PowerDocument40 pagesAlternative Centres of PowerJigyasa Atreya0% (2)

- World ForecastDocument607 pagesWorld ForecastThalia SandersNo ratings yet

- Bill Gates PortfolioDocument33 pagesBill Gates PortfolioCarlCord100% (1)

- Ritmurile LuniiDocument161 pagesRitmurile Luniimonica_vasilescu2008No ratings yet

- Pak-China Relations Through CPECDocument24 pagesPak-China Relations Through CPECFatimaNo ratings yet

- Basic Characteristics of Chinese CultureDocument27 pagesBasic Characteristics of Chinese CultureShikha SinghNo ratings yet

- Advertising Strategy in ChinaDocument33 pagesAdvertising Strategy in ChinaVineet Kumar ANo ratings yet

- International Marketing - ChinaDocument10 pagesInternational Marketing - ChinaNaijalegendNo ratings yet

- KNL Report - IIM IndoreDocument24 pagesKNL Report - IIM Indoredearssameer6270No ratings yet

- Fanuc Dual Check Safety: The TheDocument32 pagesFanuc Dual Check Safety: The TheWazabi MooNo ratings yet

- Ford in ChinaDocument4 pagesFord in ChinaDaud SulaimanNo ratings yet

- Beijing Cuts Interest Rates in Bid To Revive Economy: Three Headaches Sleeping Beauty The Big RetreatDocument26 pagesBeijing Cuts Interest Rates in Bid To Revive Economy: Three Headaches Sleeping Beauty The Big RetreatstefanoNo ratings yet

- Decoding China Cross-Cultural Strategies For Successful Business With The ChineseDocument116 pagesDecoding China Cross-Cultural Strategies For Successful Business With The Chinese卡卡No ratings yet

- Chapter 3: Industrialisation: Table of Contents: Industrialisation/Global EconomyDocument25 pagesChapter 3: Industrialisation: Table of Contents: Industrialisation/Global EconomyErvin LimNo ratings yet

- ShopDocument272 pagesShopBoyi EnebinelsonNo ratings yet

- Consumer Credits and Economic Growth in China: The Chinese EconomyDocument11 pagesConsumer Credits and Economic Growth in China: The Chinese EconomyFadel MuhammadNo ratings yet

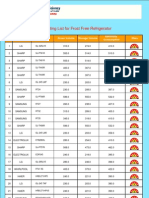

- 7 BEE FrostFree Refrigerator ListDocument13 pages7 BEE FrostFree Refrigerator ListPunit ShethNo ratings yet

- Economics Real Life ExamplesDocument22 pagesEconomics Real Life ExamplesachinthaNo ratings yet