Using Data Analytics To Ask and Answer Accounting Questions: A Look at This Chapter

Using Data Analytics To Ask and Answer Accounting Questions: A Look at This Chapter

You might also like

- KELOMPOK 7 Materi Bahasa Inggris Buku VernonDocument142 pagesKELOMPOK 7 Materi Bahasa Inggris Buku VernonmelvinNo ratings yet

- Strategic Analytics: Advancing Strategy Execution and Organizational EffectivenessFrom EverandStrategic Analytics: Advancing Strategy Execution and Organizational EffectivenessNo ratings yet

- As9100 As9120Document2 pagesAs9100 As9120Innovia100% (1)

- Chapter 1Document36 pagesChapter 1CharleneKronstedtNo ratings yet

- Level 7 Sports v. University of Utah Et Al.Document25 pagesLevel 7 Sports v. University of Utah Et Al.The Salt Lake TribuneNo ratings yet

- MODAUD2 - Unit 3 - Audit of Accounts and Notes Payable - T31516 - FINALDocument4 pagesMODAUD2 - Unit 3 - Audit of Accounts and Notes Payable - T31516 - FINALmimi96No ratings yet

- Operational RiskDocument26 pagesOperational RiskmmkattaNo ratings yet

- Master The Data: An Introduction To Accounting Data: A Look BackDocument81 pagesMaster The Data: An Introduction To Accounting Data: A Look Backsalsabila.rafy-2021No ratings yet

- (Simkin, Rose y Norman, 2012, Pp. 4-9) Core Concepts of AISDocument6 pages(Simkin, Rose y Norman, 2012, Pp. 4-9) Core Concepts of AISCristian MsbNo ratings yet

- Business Analytics II, Mid TermDocument9 pagesBusiness Analytics II, Mid TermAman SinghNo ratings yet

- SpringboardDataAnalyticsforBusinessSyllabus 2Document6 pagesSpringboardDataAnalyticsforBusinessSyllabus 2uchiha_rhenzaki0% (1)

- Chapter 1Document31 pagesChapter 1Brenda MuseNo ratings yet

- Revisiting Ackoffs Management Misinformation SystemsDocument7 pagesRevisiting Ackoffs Management Misinformation SystemsPaulo Kirschner JrNo ratings yet

- English TestDocument3 pagesEnglish TestGiofher UrciaNo ratings yet

- Literature Review On Accounting Information SystemDocument8 pagesLiterature Review On Accounting Information SystemafdtzwlzdNo ratings yet

- Management Accounting ThesisDocument8 pagesManagement Accounting Thesisafkogsfea100% (2)

- 1.2 Rapid Change in Accountantâ ™s RoleDocument13 pages1.2 Rapid Change in Accountantâ ™s RoleelinaNo ratings yet

- Cashiering System ThesisDocument7 pagesCashiering System Thesisjacquelinethomascleveland100% (2)

- Analisis de NegociosDocument1,177 pagesAnalisis de Negociosspiplatium100% (1)

- ISPFL9 Module1Document22 pagesISPFL9 Module1Rose Ann BalladaresNo ratings yet

- The Role of Visual AnalysisDocument13 pagesThe Role of Visual AnalysisAngie Marcela Marulanda Meneses100% (2)

- Dissertation On Accounting Information SystemDocument7 pagesDissertation On Accounting Information SystemBuyCustomPaperCanada100% (1)

- Research Paper of Management AccountingDocument5 pagesResearch Paper of Management Accountingskpcijbkf100% (1)

- Module 2 - Fund. of Business AnalyticsDocument26 pagesModule 2 - Fund. of Business AnalyticsnicaapcinaNo ratings yet

- Big Data Analytics Opportunity or Threat PDFDocument39 pagesBig Data Analytics Opportunity or Threat PDFYenny ChandraNo ratings yet

- 2015-07-2320151626cokins JCAF Accounting TaxonomyDocument12 pages2015-07-2320151626cokins JCAF Accounting TaxonomyLaura Francisca Carril CancinoNo ratings yet

- Using Analytics To Reduce DsoDocument8 pagesUsing Analytics To Reduce DsoTony KayNo ratings yet

- Fundamentals of Business Analytics ModuleDocument5 pagesFundamentals of Business Analytics Modulesarah.sardonNo ratings yet

- AIS Course OutlineDocument6 pagesAIS Course OutlineRajivManochaNo ratings yet

- Chapter 01Document25 pagesChapter 01Frank Lee50% (2)

- Accounting Information System CH 1 - Systems An OverviewDocument49 pagesAccounting Information System CH 1 - Systems An OverviewfyramadhanNo ratings yet

- The Effects of Using Business Intelligence Systems On An Excellence Management and Decision-Making Process by Start-Up Companies: A Case StudyDocument11 pagesThe Effects of Using Business Intelligence Systems On An Excellence Management and Decision-Making Process by Start-Up Companies: A Case StudyLuttpiNo ratings yet

- Learning Guide: Accounts and Budget ServiceDocument110 pagesLearning Guide: Accounts and Budget ServicerameNo ratings yet

- UNIT 1 PPDocument16 pagesUNIT 1 PPPrince RathoreNo ratings yet

- Sample Solution: Midterm Exam - 300 PointsDocument4 pagesSample Solution: Midterm Exam - 300 PointsYusuf HusseinNo ratings yet

- Lecture Notes 1Document5 pagesLecture Notes 1Cynthia del CorroNo ratings yet

- Learning Guide: Accounts and Budget SupportDocument100 pagesLearning Guide: Accounts and Budget Supportmac video teachingNo ratings yet

- Data AnalysisDocument17 pagesData Analysisolabisiesther83No ratings yet

- 3 MBA E-BusinessDocument8 pages3 MBA E-BusinessKapil SenNo ratings yet

- Lecture Notes-Chapter 1Document3 pagesLecture Notes-Chapter 1nayna_taraviyaNo ratings yet

- 11e Chp1-IMDocument14 pages11e Chp1-IMManila JohnNo ratings yet

- Your Modern Business Guide To Data AnalysisDocument22 pagesYour Modern Business Guide To Data AnalysisDrJd ChandrapalNo ratings yet

- Full Download Solution Manual For Core Concepts of Accounting Information Systems 14th by Simkin PDF Full ChapterDocument36 pagesFull Download Solution Manual For Core Concepts of Accounting Information Systems 14th by Simkin PDF Full Chapterhebraizelathyos6cae100% (24)

- Research Paper Topics For Accounting Information SystemsDocument6 pagesResearch Paper Topics For Accounting Information Systemslinudyt0lov2100% (1)

- Ashak Anowar MahiDocument6 pagesAshak Anowar MahiAshak Anowar MahiNo ratings yet

- How Business Analytics Applications Works in Financial ActivitiesDocument12 pagesHow Business Analytics Applications Works in Financial ActivitiesMostak100% (1)

- Reference 3Document12 pagesReference 3Jhersey ManzanoNo ratings yet

- What Are The Skills Required To Be A Business Analyst?Document4 pagesWhat Are The Skills Required To Be A Business Analyst?Ravi Kumar DubeyNo ratings yet

- Business Intelligence Literature ReviewDocument7 pagesBusiness Intelligence Literature Reviewmgpwfubnd100% (1)

- Accounting Information System Term PaperDocument5 pagesAccounting Information System Term Paperafdtuwxrb100% (1)

- Sargent PPDocument41 pagesSargent PPNabeel MughalNo ratings yet

- Business Analytics: Vicky Grade3 Class B 2019.04Document20 pagesBusiness Analytics: Vicky Grade3 Class B 2019.04shaneNo ratings yet

- Data Mining For Financial Statement AnalysisDocument4 pagesData Mining For Financial Statement Analysisalokkhode100% (1)

- The LAMP FrameworkDocument13 pagesThe LAMP FrameworkGrace RuthNo ratings yet

- Oracle HR AnalyticsDocument21 pagesOracle HR AnalyticslijinowalNo ratings yet

- 6 Management Reporting Best Practices To Create Effective Reports PDFDocument12 pages6 Management Reporting Best Practices To Create Effective Reports PDFAnang FakhruddinNo ratings yet

- Accounting Information System DissertationDocument6 pagesAccounting Information System DissertationDltkCustomWritingPaperMurfreesboro100% (1)

- Business Intelligence and Its Applications To The Public AdministrationDocument10 pagesBusiness Intelligence and Its Applications To The Public AdministrationprofetaabrahamNo ratings yet

- Unit 1Document13 pagesUnit 1abhimanyu chauhanNo ratings yet

- Ais CH - 1Document14 pagesAis CH - 1zinabuassefa3524No ratings yet

- Accounting & Data Analytics - What You Need To Know - Franklin UniversityDocument10 pagesAccounting & Data Analytics - What You Need To Know - Franklin UniversityAntônio DuarteNo ratings yet

- Business Analytics: Leveraging Data for Insights and Competitive AdvantageFrom EverandBusiness Analytics: Leveraging Data for Insights and Competitive AdvantageNo ratings yet

- MU1 Practice ExamDocument20 pagesMU1 Practice ExamCGASTUFFNo ratings yet

- Aui4861 2020 TL 202 Assignment AnswersDocument6 pagesAui4861 2020 TL 202 Assignment AnswersDennis MasipaNo ratings yet

- Business Form Report ChecklistDocument2 pagesBusiness Form Report ChecklistcaplusincNo ratings yet

- Curriculum Vitae: Educational Background Formal EducationDocument5 pagesCurriculum Vitae: Educational Background Formal EducationrianNo ratings yet

- AUD NOTES 2011/2012 (12 Pages) Shared By: Biggs: To Help You Pass, Prepare Your Own NotesDocument7 pagesAUD NOTES 2011/2012 (12 Pages) Shared By: Biggs: To Help You Pass, Prepare Your Own Notesjklein2588No ratings yet

- Process FlowsDocument76 pagesProcess FlowsRaj KumarNo ratings yet

- US v. McGrawDocument6 pagesUS v. McGrawJustin OkunNo ratings yet

- Registration Document 2018: Including The Annual Fi Nancial ReportDocument352 pagesRegistration Document 2018: Including The Annual Fi Nancial ReportRomain DelplancqNo ratings yet

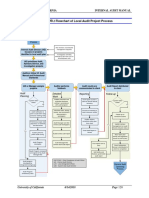

- 6000 Appendix 6000.: 2 Flowchart of Local Audit Project ProcessDocument1 page6000 Appendix 6000.: 2 Flowchart of Local Audit Project ProcessNiken RindasariNo ratings yet

- ABN AMRO Annual Report 2005Document241 pagesABN AMRO Annual Report 2005andrea_baffoNo ratings yet

- (2023794491) Habiba KashifDocument5 pages(2023794491) Habiba KashifHabiba KashifNo ratings yet

- New Syllabus For BCOM Semester Wise 2018-19Document22 pagesNew Syllabus For BCOM Semester Wise 2018-19Ashutosh AgarwalNo ratings yet

- IRCA Application RequirementsDocument58 pagesIRCA Application RequirementsLuis Gustavo PachecoNo ratings yet

- Company Vs LLP Vs FirmDocument6 pagesCompany Vs LLP Vs FirmVipul DesaiNo ratings yet

- Audit Firms On SBP PannelDocument6 pagesAudit Firms On SBP PannelOmer ArifNo ratings yet

- Pakistan: Semester-5Document2 pagesPakistan: Semester-5Muhammad Zahid FaridNo ratings yet

- TDS Late Fee (Or GST Late Fee) Is An Allowable ExpenditureDocument5 pagesTDS Late Fee (Or GST Late Fee) Is An Allowable ExpenditureDivyaNo ratings yet

- CamiguinProv2018 Audit ReportDocument159 pagesCamiguinProv2018 Audit ReporthazelNo ratings yet

- Summary CH 6 (Audit Evidence)Document10 pagesSummary CH 6 (Audit Evidence)bernadetteNo ratings yet

- Internship ReportDocument33 pagesInternship ReportPriyanka A SNo ratings yet

- Project On Airlines IndiaDocument48 pagesProject On Airlines IndiaVikram SinghNo ratings yet

- MHRD Two Year Full Time Programme Course Structure and SyllabusDocument59 pagesMHRD Two Year Full Time Programme Course Structure and SyllabusPriyank JainNo ratings yet

- UG Annual Examination Time Table March 2016Document6 pagesUG Annual Examination Time Table March 2016Lakshmi Prasad CNo ratings yet

- Measurement Theory Sesi #5 Dr. Zaroni: Godfrey Hodgson Holmes TarcaDocument27 pagesMeasurement Theory Sesi #5 Dr. Zaroni: Godfrey Hodgson Holmes TarcaFELIX PANDIKANo ratings yet

- Buhary Maharoop Ali (Mahrouf)Document4 pagesBuhary Maharoop Ali (Mahrouf)Bm AliNo ratings yet

- Ms ConsultancyDocument3 pagesMs Consultancynda0403No ratings yet

Download as pdf or txt

You might also like

- KELOMPOK 7 Materi Bahasa Inggris Buku VernonDocument142 pagesKELOMPOK 7 Materi Bahasa Inggris Buku VernonmelvinNo ratings yet

- Strategic Analytics: Advancing Strategy Execution and Organizational EffectivenessFrom EverandStrategic Analytics: Advancing Strategy Execution and Organizational EffectivenessNo ratings yet

- As9100 As9120Document2 pagesAs9100 As9120Innovia100% (1)

- Chapter 1Document36 pagesChapter 1CharleneKronstedtNo ratings yet

- Level 7 Sports v. University of Utah Et Al.Document25 pagesLevel 7 Sports v. University of Utah Et Al.The Salt Lake TribuneNo ratings yet

- MODAUD2 - Unit 3 - Audit of Accounts and Notes Payable - T31516 - FINALDocument4 pagesMODAUD2 - Unit 3 - Audit of Accounts and Notes Payable - T31516 - FINALmimi96No ratings yet

- Operational RiskDocument26 pagesOperational RiskmmkattaNo ratings yet

- Master The Data: An Introduction To Accounting Data: A Look BackDocument81 pagesMaster The Data: An Introduction To Accounting Data: A Look Backsalsabila.rafy-2021No ratings yet

- (Simkin, Rose y Norman, 2012, Pp. 4-9) Core Concepts of AISDocument6 pages(Simkin, Rose y Norman, 2012, Pp. 4-9) Core Concepts of AISCristian MsbNo ratings yet

- Business Analytics II, Mid TermDocument9 pagesBusiness Analytics II, Mid TermAman SinghNo ratings yet

- SpringboardDataAnalyticsforBusinessSyllabus 2Document6 pagesSpringboardDataAnalyticsforBusinessSyllabus 2uchiha_rhenzaki0% (1)

- Chapter 1Document31 pagesChapter 1Brenda MuseNo ratings yet

- Revisiting Ackoffs Management Misinformation SystemsDocument7 pagesRevisiting Ackoffs Management Misinformation SystemsPaulo Kirschner JrNo ratings yet

- English TestDocument3 pagesEnglish TestGiofher UrciaNo ratings yet

- Literature Review On Accounting Information SystemDocument8 pagesLiterature Review On Accounting Information SystemafdtzwlzdNo ratings yet

- Management Accounting ThesisDocument8 pagesManagement Accounting Thesisafkogsfea100% (2)

- 1.2 Rapid Change in Accountantâ ™s RoleDocument13 pages1.2 Rapid Change in Accountantâ ™s RoleelinaNo ratings yet

- Cashiering System ThesisDocument7 pagesCashiering System Thesisjacquelinethomascleveland100% (2)

- Analisis de NegociosDocument1,177 pagesAnalisis de Negociosspiplatium100% (1)

- ISPFL9 Module1Document22 pagesISPFL9 Module1Rose Ann BalladaresNo ratings yet

- The Role of Visual AnalysisDocument13 pagesThe Role of Visual AnalysisAngie Marcela Marulanda Meneses100% (2)

- Dissertation On Accounting Information SystemDocument7 pagesDissertation On Accounting Information SystemBuyCustomPaperCanada100% (1)

- Research Paper of Management AccountingDocument5 pagesResearch Paper of Management Accountingskpcijbkf100% (1)

- Module 2 - Fund. of Business AnalyticsDocument26 pagesModule 2 - Fund. of Business AnalyticsnicaapcinaNo ratings yet

- Big Data Analytics Opportunity or Threat PDFDocument39 pagesBig Data Analytics Opportunity or Threat PDFYenny ChandraNo ratings yet

- 2015-07-2320151626cokins JCAF Accounting TaxonomyDocument12 pages2015-07-2320151626cokins JCAF Accounting TaxonomyLaura Francisca Carril CancinoNo ratings yet

- Using Analytics To Reduce DsoDocument8 pagesUsing Analytics To Reduce DsoTony KayNo ratings yet

- Fundamentals of Business Analytics ModuleDocument5 pagesFundamentals of Business Analytics Modulesarah.sardonNo ratings yet

- AIS Course OutlineDocument6 pagesAIS Course OutlineRajivManochaNo ratings yet

- Chapter 01Document25 pagesChapter 01Frank Lee50% (2)

- Accounting Information System CH 1 - Systems An OverviewDocument49 pagesAccounting Information System CH 1 - Systems An OverviewfyramadhanNo ratings yet

- The Effects of Using Business Intelligence Systems On An Excellence Management and Decision-Making Process by Start-Up Companies: A Case StudyDocument11 pagesThe Effects of Using Business Intelligence Systems On An Excellence Management and Decision-Making Process by Start-Up Companies: A Case StudyLuttpiNo ratings yet

- Learning Guide: Accounts and Budget ServiceDocument110 pagesLearning Guide: Accounts and Budget ServicerameNo ratings yet

- UNIT 1 PPDocument16 pagesUNIT 1 PPPrince RathoreNo ratings yet

- Sample Solution: Midterm Exam - 300 PointsDocument4 pagesSample Solution: Midterm Exam - 300 PointsYusuf HusseinNo ratings yet

- Lecture Notes 1Document5 pagesLecture Notes 1Cynthia del CorroNo ratings yet

- Learning Guide: Accounts and Budget SupportDocument100 pagesLearning Guide: Accounts and Budget Supportmac video teachingNo ratings yet

- Data AnalysisDocument17 pagesData Analysisolabisiesther83No ratings yet

- 3 MBA E-BusinessDocument8 pages3 MBA E-BusinessKapil SenNo ratings yet

- Lecture Notes-Chapter 1Document3 pagesLecture Notes-Chapter 1nayna_taraviyaNo ratings yet

- 11e Chp1-IMDocument14 pages11e Chp1-IMManila JohnNo ratings yet

- Your Modern Business Guide To Data AnalysisDocument22 pagesYour Modern Business Guide To Data AnalysisDrJd ChandrapalNo ratings yet

- Full Download Solution Manual For Core Concepts of Accounting Information Systems 14th by Simkin PDF Full ChapterDocument36 pagesFull Download Solution Manual For Core Concepts of Accounting Information Systems 14th by Simkin PDF Full Chapterhebraizelathyos6cae100% (24)

- Research Paper Topics For Accounting Information SystemsDocument6 pagesResearch Paper Topics For Accounting Information Systemslinudyt0lov2100% (1)

- Ashak Anowar MahiDocument6 pagesAshak Anowar MahiAshak Anowar MahiNo ratings yet

- How Business Analytics Applications Works in Financial ActivitiesDocument12 pagesHow Business Analytics Applications Works in Financial ActivitiesMostak100% (1)

- Reference 3Document12 pagesReference 3Jhersey ManzanoNo ratings yet

- What Are The Skills Required To Be A Business Analyst?Document4 pagesWhat Are The Skills Required To Be A Business Analyst?Ravi Kumar DubeyNo ratings yet

- Business Intelligence Literature ReviewDocument7 pagesBusiness Intelligence Literature Reviewmgpwfubnd100% (1)

- Accounting Information System Term PaperDocument5 pagesAccounting Information System Term Paperafdtuwxrb100% (1)

- Sargent PPDocument41 pagesSargent PPNabeel MughalNo ratings yet

- Business Analytics: Vicky Grade3 Class B 2019.04Document20 pagesBusiness Analytics: Vicky Grade3 Class B 2019.04shaneNo ratings yet

- Data Mining For Financial Statement AnalysisDocument4 pagesData Mining For Financial Statement Analysisalokkhode100% (1)

- The LAMP FrameworkDocument13 pagesThe LAMP FrameworkGrace RuthNo ratings yet

- Oracle HR AnalyticsDocument21 pagesOracle HR AnalyticslijinowalNo ratings yet

- 6 Management Reporting Best Practices To Create Effective Reports PDFDocument12 pages6 Management Reporting Best Practices To Create Effective Reports PDFAnang FakhruddinNo ratings yet

- Accounting Information System DissertationDocument6 pagesAccounting Information System DissertationDltkCustomWritingPaperMurfreesboro100% (1)

- Business Intelligence and Its Applications To The Public AdministrationDocument10 pagesBusiness Intelligence and Its Applications To The Public AdministrationprofetaabrahamNo ratings yet

- Unit 1Document13 pagesUnit 1abhimanyu chauhanNo ratings yet

- Ais CH - 1Document14 pagesAis CH - 1zinabuassefa3524No ratings yet

- Accounting & Data Analytics - What You Need To Know - Franklin UniversityDocument10 pagesAccounting & Data Analytics - What You Need To Know - Franklin UniversityAntônio DuarteNo ratings yet

- Business Analytics: Leveraging Data for Insights and Competitive AdvantageFrom EverandBusiness Analytics: Leveraging Data for Insights and Competitive AdvantageNo ratings yet

- MU1 Practice ExamDocument20 pagesMU1 Practice ExamCGASTUFFNo ratings yet

- Aui4861 2020 TL 202 Assignment AnswersDocument6 pagesAui4861 2020 TL 202 Assignment AnswersDennis MasipaNo ratings yet

- Business Form Report ChecklistDocument2 pagesBusiness Form Report ChecklistcaplusincNo ratings yet

- Curriculum Vitae: Educational Background Formal EducationDocument5 pagesCurriculum Vitae: Educational Background Formal EducationrianNo ratings yet

- AUD NOTES 2011/2012 (12 Pages) Shared By: Biggs: To Help You Pass, Prepare Your Own NotesDocument7 pagesAUD NOTES 2011/2012 (12 Pages) Shared By: Biggs: To Help You Pass, Prepare Your Own Notesjklein2588No ratings yet

- Process FlowsDocument76 pagesProcess FlowsRaj KumarNo ratings yet

- US v. McGrawDocument6 pagesUS v. McGrawJustin OkunNo ratings yet

- Registration Document 2018: Including The Annual Fi Nancial ReportDocument352 pagesRegistration Document 2018: Including The Annual Fi Nancial ReportRomain DelplancqNo ratings yet

- 6000 Appendix 6000.: 2 Flowchart of Local Audit Project ProcessDocument1 page6000 Appendix 6000.: 2 Flowchart of Local Audit Project ProcessNiken RindasariNo ratings yet

- ABN AMRO Annual Report 2005Document241 pagesABN AMRO Annual Report 2005andrea_baffoNo ratings yet

- (2023794491) Habiba KashifDocument5 pages(2023794491) Habiba KashifHabiba KashifNo ratings yet

- New Syllabus For BCOM Semester Wise 2018-19Document22 pagesNew Syllabus For BCOM Semester Wise 2018-19Ashutosh AgarwalNo ratings yet

- IRCA Application RequirementsDocument58 pagesIRCA Application RequirementsLuis Gustavo PachecoNo ratings yet

- Company Vs LLP Vs FirmDocument6 pagesCompany Vs LLP Vs FirmVipul DesaiNo ratings yet

- Audit Firms On SBP PannelDocument6 pagesAudit Firms On SBP PannelOmer ArifNo ratings yet

- Pakistan: Semester-5Document2 pagesPakistan: Semester-5Muhammad Zahid FaridNo ratings yet

- TDS Late Fee (Or GST Late Fee) Is An Allowable ExpenditureDocument5 pagesTDS Late Fee (Or GST Late Fee) Is An Allowable ExpenditureDivyaNo ratings yet

- CamiguinProv2018 Audit ReportDocument159 pagesCamiguinProv2018 Audit ReporthazelNo ratings yet

- Summary CH 6 (Audit Evidence)Document10 pagesSummary CH 6 (Audit Evidence)bernadetteNo ratings yet

- Internship ReportDocument33 pagesInternship ReportPriyanka A SNo ratings yet

- Project On Airlines IndiaDocument48 pagesProject On Airlines IndiaVikram SinghNo ratings yet

- MHRD Two Year Full Time Programme Course Structure and SyllabusDocument59 pagesMHRD Two Year Full Time Programme Course Structure and SyllabusPriyank JainNo ratings yet

- UG Annual Examination Time Table March 2016Document6 pagesUG Annual Examination Time Table March 2016Lakshmi Prasad CNo ratings yet

- Measurement Theory Sesi #5 Dr. Zaroni: Godfrey Hodgson Holmes TarcaDocument27 pagesMeasurement Theory Sesi #5 Dr. Zaroni: Godfrey Hodgson Holmes TarcaFELIX PANDIKANo ratings yet

- Buhary Maharoop Ali (Mahrouf)Document4 pagesBuhary Maharoop Ali (Mahrouf)Bm AliNo ratings yet

- Ms ConsultancyDocument3 pagesMs Consultancynda0403No ratings yet