Download as pdf or txt

You might also like

- Hi-Survey Road User Manual-EN-20200330Document276 pagesHi-Survey Road User Manual-EN-20200330Mauricio RuizNo ratings yet

- Ab Costing - ProblemsDocument8 pagesAb Costing - ProblemsMarcial VillegasNo ratings yet

- 38t GEI41047 PDocument28 pages38t GEI41047 PJorge DiazNo ratings yet

- Chapter 8 Solutions ExercisesDocument25 pagesChapter 8 Solutions Exerciseswajeeda awadNo ratings yet

- Chapter 6 HomeworkDocument10 pagesChapter 6 HomeworkAshy Lee0% (1)

- HW Session 5Document3 pagesHW Session 5Tiffany KimNo ratings yet

- Practice Questions - SolDocument8 pagesPractice Questions - SolNicholas LeeNo ratings yet

- Chapter 2 Cost Concepts and ClassificationDocument10 pagesChapter 2 Cost Concepts and ClassificationSteffany RoqueNo ratings yet

- Management Accounting Individual AssignmentDocument10 pagesManagement Accounting Individual AssignmentendalNo ratings yet

- Studi Kasus SCMDocument8 pagesStudi Kasus SCMMuflihul Khair0% (5)

- Solutions Ch. 7 ABCDocument11 pagesSolutions Ch. 7 ABCThanawat PHURISIRUNGROJNo ratings yet

- Ab Costing CathDocument5 pagesAb Costing CathRoy Mitz Aggabao Bautista VNo ratings yet

- Solutions 1Document4 pagesSolutions 1Markus H.No ratings yet

- ABC MethodDocument6 pagesABC MethodPrincess RapisuraNo ratings yet

- Key Chapter 2 & 3Document9 pagesKey Chapter 2 & 3bxp9b56xv4No ratings yet

- Chapter 8-SolutiondocxDocument17 pagesChapter 8-Solutiondocxevani1998No ratings yet

- Session 16 PGPDocument10 pagesSession 16 PGPtanvi gargNo ratings yet

- CH 12Document15 pagesCH 12Firas HamadNo ratings yet

- Cornerstone Exercises Cornerstone Exercise 17.1Document30 pagesCornerstone Exercises Cornerstone Exercise 17.1Nirwana PuriNo ratings yet

- CH 3Document12 pagesCH 3Firas HamadNo ratings yet

- ManaktugasDocument7 pagesManaktugasNimas KartikaNo ratings yet

- ADMS 2510 Week 13 SolutionsDocument20 pagesADMS 2510 Week 13 Solutionsadms examzNo ratings yet

- ANSWERS TO PRACTICE MIDTERM (Multiple Choice) : RequiredDocument5 pagesANSWERS TO PRACTICE MIDTERM (Multiple Choice) : RequiredGwendolyn Chloe PurnamaNo ratings yet

- AF2110 Management Accounting 1 Assignment 05 Suggested Solutions Exercise 6-13 (20 Minutes)Document12 pagesAF2110 Management Accounting 1 Assignment 05 Suggested Solutions Exercise 6-13 (20 Minutes)Shadow IpNo ratings yet

- Kerjakan 4-12 Dan 4 - 17: 1. "Plantwide"Document4 pagesKerjakan 4-12 Dan 4 - 17: 1. "Plantwide"natan. lieNo ratings yet

- A Chp6 TUTDocument11 pagesA Chp6 TUTYong Jing YinNo ratings yet

- 201B Exam 3 PracticeDocument16 pages201B Exam 3 PracticeChanel NguyenNo ratings yet

- Answer To Assignment #2 - Variable Costing PDFDocument14 pagesAnswer To Assignment #2 - Variable Costing PDFVivienne Rozenn LaytoNo ratings yet

- Solution P5 - 4656Document5 pagesSolution P5 - 4656HO JING YI MBS221190No ratings yet

- Prof. VG CMA Practice Problems With SolutionsDocument6 pagesProf. VG CMA Practice Problems With SolutionssudiptakrNo ratings yet

- Solution To Questions On Decision MakingDocument27 pagesSolution To Questions On Decision Makingdanishbashir786No ratings yet

- Chapter 8 Solutions - Inclass ExercisesDocument8 pagesChapter 8 Solutions - Inclass ExercisesSummerNo ratings yet

- ASG 3 Soloist PDFDocument4 pagesASG 3 Soloist PDFJohnsen PratamaNo ratings yet

- Akuntansi BiayaDocument4 pagesAkuntansi BiayaIntan Bella YuspramanaNo ratings yet

- Review Problem: Differential Analysis: RequiredDocument17 pagesReview Problem: Differential Analysis: RequiredBảo Anh Phạm100% (1)

- Problem 1.: Beginnin G EndingDocument3 pagesProblem 1.: Beginnin G EndingMarsha Zhafira ANo ratings yet

- Chapter 2Document16 pagesChapter 2Manish SadhuNo ratings yet

- Revision Week 1. Questions. Question 1. Cost of Goods Manufactured, Cost of Goods Sold, Income Statement. (A)Document5 pagesRevision Week 1. Questions. Question 1. Cost of Goods Manufactured, Cost of Goods Sold, Income Statement. (A)Sujib BarmanNo ratings yet

- MA Mids Muneeb Ahmed 10180Document11 pagesMA Mids Muneeb Ahmed 10180zainNo ratings yet

- ACC 213 Exercise 6Document3 pagesACC 213 Exercise 6rechell obusaNo ratings yet

- Problem 2Document3 pagesProblem 2Mohammed Al ArmaliNo ratings yet

- Sol ch15Document4 pagesSol ch15Julian PoerwanjanaNo ratings yet

- Latihan Soal Week 8Document6 pagesLatihan Soal Week 8Natasya Prashta WidyadhariNo ratings yet

- Abc RemedialDocument6 pagesAbc RemedialMinie KimNo ratings yet

- Exercise MADocument7 pagesExercise MAthanhntt21No ratings yet

- Solutions To Self-Study QuestionsDocument47 pagesSolutions To Self-Study QuestionsChristina ZhangNo ratings yet

- Answer - Case 1Document10 pagesAnswer - Case 1EVI MARIA SIBUEANo ratings yet

- MGT Acc SolutionsDocument34 pagesMGT Acc Solutionsshamsirarefin275285No ratings yet

- Relevant Cost Exercise SolutionDocument14 pagesRelevant Cost Exercise SolutionHimadri DeyNo ratings yet

- Example-2 With SolutionDocument4 pagesExample-2 With SolutionDeepNo ratings yet

- Ch7 Variable Absoorption Extra ExcersisesDocument7 pagesCh7 Variable Absoorption Extra ExcersisesSarah Al MuallaNo ratings yet

- COSMAN ASSIGNMENT 21 32 Answers CheggDocument8 pagesCOSMAN ASSIGNMENT 21 32 Answers CheggwalsondevNo ratings yet

- Chapter 1 2 SolutionsDocument10 pagesChapter 1 2 SolutionsShiv AchariNo ratings yet

- T5 - Activity-Based Costing - Open Book TeamDocument3 pagesT5 - Activity-Based Costing - Open Book TeamSujib BarmanNo ratings yet

- Service Department Cost Allocation: Solutions To Exercises and ProblemsDocument27 pagesService Department Cost Allocation: Solutions To Exercises and ProblemsMafi De LeonNo ratings yet

- Flexible Budget and VarianceDocument8 pagesFlexible Budget and VarianceLhorene Hope DueñasNo ratings yet

- CASE Limiting FactorsDocument2 pagesCASE Limiting FactorsEhrom SaidovNo ratings yet

- Practice Test E 1: Xercise (Ron Chemicals) 1. Physical Units Method Product: A-1 B-3 C-2 Q-9 TotalDocument2 pagesPractice Test E 1: Xercise (Ron Chemicals) 1. Physical Units Method Product: A-1 B-3 C-2 Q-9 TotalKaren Joyce SinsayNo ratings yet

- Problem10 18 and 10 20Document10 pagesProblem10 18 and 10 20roseNo ratings yet

- Ch05 SolutionsDocument12 pagesCh05 SolutionsHạnh Đỗ Thị ThanhNo ratings yet

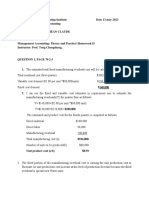

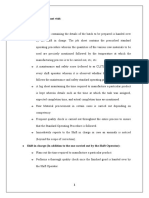

- m80221012-Kanyabwira Jean Claude - 基因 - Ass2Document10 pagesm80221012-Kanyabwira Jean Claude - 基因 - Ass2UKURI TV7No ratings yet

- Job Order Costing QuizbowlDocument27 pagesJob Order Costing QuizbowlsarahbeeNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Elphos Erald: Police Chief Clarifies Child's ID Kit UsageDocument10 pagesElphos Erald: Police Chief Clarifies Child's ID Kit UsageThe Delphos HeraldNo ratings yet

- Observations From The Plant VisitDocument2 pagesObservations From The Plant VisitAniket ShrivastavaNo ratings yet

- Valorisation of Spent Coffee Grounds Production of Biodiesel Via Enzimatic Catalisis With Ethanol and Co-SolventDocument14 pagesValorisation of Spent Coffee Grounds Production of Biodiesel Via Enzimatic Catalisis With Ethanol and Co-SolventAline GonçalvesNo ratings yet

- Fil-Chin Engineering: To: Limketkai Attn: Mr. Eduard Oh Re: Heat ExchangerDocument6 pagesFil-Chin Engineering: To: Limketkai Attn: Mr. Eduard Oh Re: Heat ExchangerKeith Henrich M. ChuaNo ratings yet

- Daftar Harga 2021 (Abjad)Document9 pagesDaftar Harga 2021 (Abjad)Arahmaniansyah HenkzNo ratings yet

- Circuito Integrado BA05STDocument10 pagesCircuito Integrado BA05STEstefano EspinozaNo ratings yet

- Open Web Floor Trusses - MiTek IncDocument7 pagesOpen Web Floor Trusses - MiTek IncinfoNo ratings yet

- EN ISO 13503-2 (2006) (E) CodifiedDocument8 pagesEN ISO 13503-2 (2006) (E) CodifiedEzgi PelitNo ratings yet

- Apple Serial Number Info - Decode Your Mac's Serial Number!Document1 pageApple Serial Number Info - Decode Your Mac's Serial Number!edp8 malsbyNo ratings yet

- Individual Development WorkoutDocument3 pagesIndividual Development WorkoutmichelleNo ratings yet

- Parts Catalog ARDFDocument30 pagesParts Catalog ARDFUlmanu ValentinNo ratings yet

- Cryolite JM File 2011Document5 pagesCryolite JM File 2011mutemuNo ratings yet

- Min Pin Sweater Paradise - Autumn Stripes Crochet Min Pin SweaterDocument6 pagesMin Pin Sweater Paradise - Autumn Stripes Crochet Min Pin SweaterNathalyaNo ratings yet

- Pressure Relief Valve, Pilot-OperatedDocument52 pagesPressure Relief Valve, Pilot-OperatedAlvaro YépezNo ratings yet

- Fourth Quarter Exam in TLE Grade SevenDocument5 pagesFourth Quarter Exam in TLE Grade SevenShabby Gay Trogani83% (12)

- Essay Types Character Analysis EssayDocument7 pagesEssay Types Character Analysis EssayFatihNo ratings yet

- Agile ManufacturingDocument17 pagesAgile Manufacturingkaushalsingh20No ratings yet

- Direction TestDocument3 pagesDirection TestprascribdNo ratings yet

- IGNITE CIB 24 February 2024Document4 pagesIGNITE CIB 24 February 2024jigarNo ratings yet

- Guia 5Document2 pagesGuia 5Luz Analía Valdez CandiaNo ratings yet

- Lesson Plan Format (Acad)Document4 pagesLesson Plan Format (Acad)Aienna Lacaya MatabalanNo ratings yet

- P2 Chp2 Section 2.1ADocument3 pagesP2 Chp2 Section 2.1APaing Khant KyawNo ratings yet

- Product Data: Order Tracking Analyzer - Type 2145Document8 pagesProduct Data: Order Tracking Analyzer - Type 2145jhon vargasNo ratings yet

- Ingersoll Rand Ingersoll Rand Compressor 39880984 Interstage Pressure SwitchDocument1 pageIngersoll Rand Ingersoll Rand Compressor 39880984 Interstage Pressure Switchbara putranta fahdliNo ratings yet

- Assignment2 NamocDocument5 pagesAssignment2 NamocHenry Darius NamocNo ratings yet

- PPP-Eclipse-E05 Module 05 IDUsDocument11 pagesPPP-Eclipse-E05 Module 05 IDUsJervy SegarraNo ratings yet