Download as pdf or txt

You might also like

- Lego Case Answers/ EssayDocument8 pagesLego Case Answers/ EssayRobert LongNo ratings yet

- Economics ProjectDocument39 pagesEconomics ProjectAnsh Bansal83% (6)

- Quiz - Investment, Part 2 ANSWERDocument4 pagesQuiz - Investment, Part 2 ANSWERJaylord Reyes100% (1)

- International Contract For Sale of Goods PDFDocument28 pagesInternational Contract For Sale of Goods PDFtienma19890% (1)

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Problem No. 1: Ap - 1Stpb - 05.07Document10 pagesProblem No. 1: Ap - 1Stpb - 05.07AnnNo ratings yet

- Chapter 13Document75 pagesChapter 13Anonymous rh4M7A100% (2)

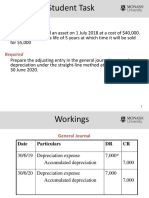

- Depriciation Methods 1Document26 pagesDepriciation Methods 1wasif ahmedNo ratings yet

- Applied Auditing Audit of Investment: Problem No. 1Document3 pagesApplied Auditing Audit of Investment: Problem No. 1JessicaNo ratings yet

- 5 DepDocument2 pages5 Depshreyash436No ratings yet

- Assignment On Session - 1: General Ledger's Name Group Op. Bal. Dr. / CRDocument18 pagesAssignment On Session - 1: General Ledger's Name Group Op. Bal. Dr. / CRcyber kci100% (1)

- Banking Company QuestionDocument11 pagesBanking Company QuestionOmkar VichareNo ratings yet

- Funds and Flow StatementDocument14 pagesFunds and Flow Statement75 SHWETA PATILNo ratings yet

- Chapter-1 (Additional Illustrations)Document20 pagesChapter-1 (Additional Illustrations)yashkumaryash11No ratings yet

- Accounts Compiler by Rahul Malkan Sir-73-98Document26 pagesAccounts Compiler by Rahul Malkan Sir-73-98sanketNo ratings yet

- Accounting For Investment in Variable Income Bearing Securities Lesson 27Document10 pagesAccounting For Investment in Variable Income Bearing Securities Lesson 27Sumantha SahaNo ratings yet

- DepreciationDocument3 pagesDepreciationSumanth KumarNo ratings yet

- Tutorial Letter 102/3/2014: Financial Accounting For Companies FAC2601Document57 pagesTutorial Letter 102/3/2014: Financial Accounting For Companies FAC2601Phebieon MukwenhaNo ratings yet

- 6a MTP Oct 2020Document13 pages6a MTP Oct 2020Bijay AgrawalNo ratings yet

- AP - Liabilities - FIN ACC AP - Liabilities - FIN ACCDocument5 pagesAP - Liabilities - FIN ACC AP - Liabilities - FIN ACCAina AguirreNo ratings yet

- 4.2 Answers and Solutions - Assignment On Materials and LaborDocument8 pages4.2 Answers and Solutions - Assignment On Materials and LaborRoselyn LumbaoNo ratings yet

- Quiz 2 PrE3Document13 pagesQuiz 2 PrE3Lyca MaeNo ratings yet

- AP Module 01 - Accounting Changes and ErrorsDocument10 pagesAP Module 01 - Accounting Changes and ErrorsjasfNo ratings yet

- Of Alabang Inc.: Prelim Examination Bsa 32E1Document16 pagesOf Alabang Inc.: Prelim Examination Bsa 32E1Genevieve VargasNo ratings yet

- Departmental Accounts PDFDocument10 pagesDepartmental Accounts PDFMINTU SARAFNo ratings yet

- 04 Assignments Practical Questions NEWDocument21 pages04 Assignments Practical Questions NEWBhupendra MendoleNo ratings yet

- SHT 031 AccountingDocument4 pagesSHT 031 Accountingnevil moraraNo ratings yet

- RM48,000 X 9% X 90/365Document4 pagesRM48,000 X 9% X 90/365Nurul SyakirinNo ratings yet

- Accounting INDIVIDUAL ASSIGNMENTDocument17 pagesAccounting INDIVIDUAL ASSIGNMENTHajara SaleethNo ratings yet

- Project Two. Process Financial Transactions and Prepare Financial The Accounts in The Ledger ofDocument11 pagesProject Two. Process Financial Transactions and Prepare Financial The Accounts in The Ledger ofGetahunNo ratings yet

- Rekon, Depreciation, and FifoDocument3 pagesRekon, Depreciation, and Fifom habiburrahman55No ratings yet

- AC 100 Aug2006 MSDocument6 pagesAC 100 Aug2006 MSERICK MLINGWANo ratings yet

- 2019 Vol 1 CH 3 AnswersDocument14 pages2019 Vol 1 CH 3 AnswersMarjorie NepomucenoNo ratings yet

- Quiz - Assignment 03.06.2021Document3 pagesQuiz - Assignment 03.06.2021Thricia Lou OpialaNo ratings yet

- Business Accounting and Analysis249 8MHDyx07qXDocument3 pagesBusiness Accounting and Analysis249 8MHDyx07qXShikha GargNo ratings yet

- Additional Illustratiions 2Document14 pagesAdditional Illustratiions 2Naman ChotiaNo ratings yet

- Suggested Answer CAP II June 2018Document128 pagesSuggested Answer CAP II June 2018Pradeep Bhattarai67% (3)

- Master of Business Administration (M.B.A.) Semester-I (C.B.C.S.) Examination Accounting For Managers Compulsory Paper-3 (Elective)Document6 pagesMaster of Business Administration (M.B.A.) Semester-I (C.B.C.S.) Examination Accounting For Managers Compulsory Paper-3 (Elective)Namrata RamgadeNo ratings yet

- CorporateAccounting Costing October2019 B B A WithCredits RegularJune-2017PatternSecondYearB B A F96AA255Document3 pagesCorporateAccounting Costing October2019 B B A WithCredits RegularJune-2017PatternSecondYearB B A F96AA255Mubin Shaikh NooruNo ratings yet

- 5.3 Depreciation Soln To Practice QuestionsDocument18 pages5.3 Depreciation Soln To Practice Questionsdivya shindeNo ratings yet

- AP PPE QuizDocument3 pagesAP PPE QuizjomsNo ratings yet

- Unit 2 - Accountingformanager - AnanduDocument52 pagesUnit 2 - Accountingformanager - Ananducraziestidiot31No ratings yet

- Level 03Document19 pagesLevel 03Abbas WazeerNo ratings yet

- Chapter 13 - Sh. Based PaymentsDocument4 pagesChapter 13 - Sh. Based PaymentsXiena75% (4)

- 5 6305198873144984587 PDFDocument112 pages5 6305198873144984587 PDFNbut ddgfNo ratings yet

- Bact 310topic Four Accounting For Long Term Investments-2Document22 pagesBact 310topic Four Accounting For Long Term Investments-2Pa HabbakukNo ratings yet

- 5 6188442313212035099Document19 pages5 6188442313212035099JamieNo ratings yet

- Acc q2 SANSDocument11 pagesAcc q2 SANSTanvir AnjumNo ratings yet

- Advanced Accounting - NCG Pre Final Question PaperDocument4 pagesAdvanced Accounting - NCG Pre Final Question PaperKarthikeya PeddhaboinaNo ratings yet

- Reconciliation NSM DGN ABC & Clinic 2008Document2 pagesReconciliation NSM DGN ABC & Clinic 2008July SimbolonNo ratings yet

- AFU 08501 - Tutorial Set-2021 - DemosntrationDocument5 pagesAFU 08501 - Tutorial Set-2021 - DemosntrationCunningham LazzNo ratings yet

- PPE Investments Working PaperDocument15 pagesPPE Investments Working PaperMarriel Fate CullanoNo ratings yet

- Investment Accounts-Master Mind Answers PDFDocument7 pagesInvestment Accounts-Master Mind Answers PDFRam IyerNo ratings yet

- Quit 2 SolutionsDocument2 pagesQuit 2 Solutions賴昱宏No ratings yet

- Mayor AnaliticoDocument68 pagesMayor Analiticopaola vicentNo ratings yet

- Insurance Contracts UploadDocument2 pagesInsurance Contracts UploadRafael BarbinNo ratings yet

- Om Ganesh 2020-21Document11 pagesOm Ganesh 2020-21coorameshNo ratings yet

- Suggested Answers-Partnership-3Document4 pagesSuggested Answers-Partnership-3Pulkit MarwahNo ratings yet

- Chartered Accountancy Professional Ii (CAP-II) : Education Division The Institute of Chartered Accountants of NepalDocument81 pagesChartered Accountancy Professional Ii (CAP-II) : Education Division The Institute of Chartered Accountants of NepalPrashant Sagar GautamNo ratings yet

- RTP Dec 2020 QnsDocument13 pagesRTP Dec 2020 QnsbinuNo ratings yet

- PT Tiga Cahaya PutraDocument78 pagesPT Tiga Cahaya PutraBambang RisNo ratings yet

- Audit of LiabilitiesDocument6 pagesAudit of LiabilitiesEdmar HalogNo ratings yet

- Zoom SlidesDocument10 pagesZoom SlidesTuấn Kiệt NguyễnNo ratings yet

- Tugas Responsi (Individu 2) AKT - Keuangan Ramelinium Purba (190120144)Document5 pagesTugas Responsi (Individu 2) AKT - Keuangan Ramelinium Purba (190120144)Ramelinium PurbaNo ratings yet

- Management Accounting - Chapter 05 - Flexible Budget Overhead Cost VariancesDocument34 pagesManagement Accounting - Chapter 05 - Flexible Budget Overhead Cost VariancesHuyền MaiNo ratings yet

- Coffee in Peru Analysis EUROMONITORDocument2 pagesCoffee in Peru Analysis EUROMONITORJaime Marcelo Tello PalominoNo ratings yet

- Economic Crimes: Philippines PerspectiveDocument8 pagesEconomic Crimes: Philippines Perspectivejollina dawaNo ratings yet

- Second Installment Payment Relief - MBAMSc - 2021Document9 pagesSecond Installment Payment Relief - MBAMSc - 2021Chalitha DhananjaniNo ratings yet

- Realizing The Full Potential of Safety Nets PDFDocument421 pagesRealizing The Full Potential of Safety Nets PDFMwawiNo ratings yet

- FS Analysis Part 2 Drill OnlineDocument3 pagesFS Analysis Part 2 Drill OnlineDRIXLER RIVERANo ratings yet

- Motiwalla Esm2e PP 01Document50 pagesMotiwalla Esm2e PP 01lockbit3065No ratings yet

- Index of BC Regulations - March 31, 2017 PDFDocument151 pagesIndex of BC Regulations - March 31, 2017 PDFneodvx-1No ratings yet

- Risk Management ChecklistDocument2 pagesRisk Management ChecklistStefan LucaciNo ratings yet

- Black Scholes BSOP-VaR PDFDocument25 pagesBlack Scholes BSOP-VaR PDFkuttan1000No ratings yet

- Fund RaisingDocument22 pagesFund RaisingPratyush GuptaNo ratings yet

- Investors Perception Towards The Mutual Funds - Reliance SecuritiesDocument83 pagesInvestors Perception Towards The Mutual Funds - Reliance Securitiesorsashok100% (2)

- Module Outline SEM 1 2023-2024 FIN (1) (1) Updated Aug 28 2023 (4) FiinnnDocument5 pagesModule Outline SEM 1 2023-2024 FIN (1) (1) Updated Aug 28 2023 (4) FiinnnKristianNo ratings yet

- Process of 26QBDocument15 pagesProcess of 26QBthetrilight2023No ratings yet

- Term Paper (PRAN Food and Beverage)Document16 pagesTerm Paper (PRAN Food and Beverage)Chowdhury Farsad AurangzebNo ratings yet

- 5903 18966 2 PBDocument20 pages5903 18966 2 PBBerliana PrahestiNo ratings yet

- 5 6075592202128459141Document22 pages5 6075592202128459141vippala gopalreddyNo ratings yet

- Central Bank Digital Currency and Monetary Policy - A Literature ReviewDocument12 pagesCentral Bank Digital Currency and Monetary Policy - A Literature ReviewJessyNo ratings yet

- Chapter 2-Market and Market SegmentationDocument25 pagesChapter 2-Market and Market SegmentationMA ValdezNo ratings yet

- Chapter 6 - Brief Exercises - SolutionsDocument4 pagesChapter 6 - Brief Exercises - SolutionsQuynh Nguyen Huong100% (1)

- Opt Toc DBRDocument29 pagesOpt Toc DBRFischer SnapNo ratings yet

- Chapter 16 - Taxes On Consumption and SaleDocument22 pagesChapter 16 - Taxes On Consumption and Salewatts1No ratings yet

- Numerical Reasoning Test1 SolutionsDocument32 pagesNumerical Reasoning Test1 SolutionsJonson CaoNo ratings yet

- (505 (B) ) Analysis of Financial Statemnets BB223039 Shirke Kartiki RatnadeepDocument26 pages(505 (B) ) Analysis of Financial Statemnets BB223039 Shirke Kartiki RatnadeepRohan KashidNo ratings yet

- Books of Prime EntryDocument22 pagesBooks of Prime EntryRakiya ZainabNo ratings yet