Download as docx, pdf, or txt

You might also like

- IFRS Simplified: A fast and easy-to-understand overview of the new International Financial Reporting StandardsFrom EverandIFRS Simplified: A fast and easy-to-understand overview of the new International Financial Reporting StandardsRating: 4 out of 5 stars4/5 (11)

- F3 Final File 2021-2022 ADocument147 pagesF3 Final File 2021-2022 AWWE Gaming0% (1)

- FA - Financial Accounting: Chapter 2 - Regulatory FrameworkDocument23 pagesFA - Financial Accounting: Chapter 2 - Regulatory FrameworkSumiya YousefNo ratings yet

- Chapter 1Document79 pagesChapter 1alemu desta100% (1)

- Tugas Akuntansi KeuanganDocument8 pagesTugas Akuntansi KeuanganꧾꧾNo ratings yet

- DipIFR TextbookDocument375 pagesDipIFR TextbookEmin SaftarovNo ratings yet

- Study Material of Corporate Reporting Practice and ASDocument57 pagesStudy Material of Corporate Reporting Practice and ASnidhi goel0% (1)

- CH 14Document22 pagesCH 14BensonChiuNo ratings yet

- E3 (1) - Further ExerciseDocument12 pagesE3 (1) - Further ExerciseansonNo ratings yet

- 004 - Chapter 02 - Financial Reporting FrameworksDocument10 pages004 - Chapter 02 - Financial Reporting FrameworksHaris ButtNo ratings yet

- Chapter 1 Introduction To Financial Reporting and FrameworksDocument45 pagesChapter 1 Introduction To Financial Reporting and FrameworksBantamkak FikaduNo ratings yet

- International Financial Reporting Standards (IFRS)Document74 pagesInternational Financial Reporting Standards (IFRS)Ashutosh GuptaNo ratings yet

- ACYFAR NOTES Standard Setting IAS 1 Conceptual FrameworkDocument34 pagesACYFAR NOTES Standard Setting IAS 1 Conceptual FrameworkFritzey Faye RomeronaNo ratings yet

- Unit 01 (8553)Document30 pagesUnit 01 (8553)naseer ahmedNo ratings yet

- Financial Reporting Standards GTSTDocument17 pagesFinancial Reporting Standards GTSTgaurav tiwariNo ratings yet

- Cfas ReviewerDocument2 pagesCfas ReviewerElaine Ü LubianoNo ratings yet

- AcFn 511-Ch II Ppt-LK-2020 - Part One-2Document110 pagesAcFn 511-Ch II Ppt-LK-2020 - Part One-2Chilot YihuneNo ratings yet

- ch6 IFRSDocument56 pagesch6 IFRSAnonymous 6aW7sZWdIL100% (1)

- Group 1Document8 pagesGroup 1Jason Leur BernabeNo ratings yet

- Notes 1Document6 pagesNotes 1sjayceelynNo ratings yet

- IFRS PresentationDocument49 pagesIFRS Presentationunni Krishnan100% (9)

- معايير المحاسبة الدوليةDocument38 pagesمعايير المحاسبة الدوليةcommander511No ratings yet

- FA2A - Study GuideDocument67 pagesFA2A - Study GuideHasan EvansNo ratings yet

- Lesson 1Document7 pagesLesson 1Ira Charisse BurlaosNo ratings yet

- Chapt 2.4Document15 pagesChapt 2.4volnakatya07No ratings yet

- Unit IVDocument16 pagesUnit IVOsm IdeasNo ratings yet

- Accounting Standards Tanmay AroraDocument133 pagesAccounting Standards Tanmay AroratanmayaroraNo ratings yet

- Bba Ca C1 - C4 FinalDocument61 pagesBba Ca C1 - C4 FinalFa DreamsNo ratings yet

- 2005 Model FsDocument72 pages2005 Model FsMuji1No ratings yet

- Adv. Accountancy Paper-1Document5 pagesAdv. Accountancy Paper-1Avadhut PaymalleNo ratings yet

- Financial ReportingDocument10 pagesFinancial Reportingrafiulbiz12No ratings yet

- International Financing Reporting Standards (Ifrs) International Financing Reporting Standards (Ifrs)Document15 pagesInternational Financing Reporting Standards (Ifrs) International Financing Reporting Standards (Ifrs)Sugufta ZehraNo ratings yet

- Introduction of IFRS-Issues and ChallengesDocument12 pagesIntroduction of IFRS-Issues and ChallengesAbhisshek GautamNo ratings yet

- Conceptual Framework Accounting SystemDocument13 pagesConceptual Framework Accounting SystemYes ChannelNo ratings yet

- Accounting StandardsDocument109 pagesAccounting StandardsJugal Shah100% (1)

- Accounting Standard Setting Bodies LectureDocument34 pagesAccounting Standard Setting Bodies LectureozobokemeoyintareNo ratings yet

- Accounting Standards S.ClementDocument109 pagesAccounting Standards S.Clementabhi_chess22No ratings yet

- ACC702 Course Material Study GuideDocument78 pagesACC702 Course Material Study Guidethùy TrầnNo ratings yet

- Conceptual Famework FASB IASBDocument36 pagesConceptual Famework FASB IASBMusab AhmedNo ratings yet

- Advanced Financial Management: Corporate Finance: Laurent BARTHE CetiaDocument76 pagesAdvanced Financial Management: Corporate Finance: Laurent BARTHE CetiaHo Nguyen Nhat TanNo ratings yet

- Acc Cap1 PresentationDocument30 pagesAcc Cap1 PresentationtafsirmhinNo ratings yet

- IAS ALL ChapterDocument23 pagesIAS ALL Chapterchethan9353605265No ratings yet

- Actuarial Practices Relating To Accounting For Insurance Pursuant To International Financial Reporting StandardsDocument39 pagesActuarial Practices Relating To Accounting For Insurance Pursuant To International Financial Reporting StandardsIvana TodorovNo ratings yet

- BABE1 Reviewer 1Document13 pagesBABE1 Reviewer 1James Ryan AlzonaNo ratings yet

- Unit 2 - GAAP and IFRSDocument15 pagesUnit 2 - GAAP and IFRSKanak RathoreNo ratings yet

- Afa Ipsas and Adoption of Ipsas in NigeriaDocument25 pagesAfa Ipsas and Adoption of Ipsas in Nigeriat4fgmwcb2kNo ratings yet

- A - Intro To IASBDocument4 pagesA - Intro To IASBKaryl FailmaNo ratings yet

- BSBFIN401 Assessment 2Document10 pagesBSBFIN401 Assessment 2Kitpipoj PornnongsaenNo ratings yet

- Lesson 2: Financial Reporting StandardsDocument25 pagesLesson 2: Financial Reporting StandardsQuyen Thanh NguyenNo ratings yet

- Lesson 1Document11 pagesLesson 1shadowlord468No ratings yet

- 19, International Financial Reporting Standards-I Paper: 02, Accounting & Financial AnalysisDocument13 pages19, International Financial Reporting Standards-I Paper: 02, Accounting & Financial AnalysisMohit RanaNo ratings yet

- 1 Ifrs Ias 1-AccaDocument265 pages1 Ifrs Ias 1-AccaSabrina Aeni100% (1)

- ACCG835 International AccountingDocument41 pagesACCG835 International AccountingSophie DaoNo ratings yet

- Contemporary Issues - IFRS, HR, CSR EtcDocument38 pagesContemporary Issues - IFRS, HR, CSR Etckaltim.iu.m.ma.h78No ratings yet

- 2 The Regulatory Framework - PPSXDocument13 pages2 The Regulatory Framework - PPSXAbdelwahab Ahmed IbrahimNo ratings yet

- Assignment Intermediate Accounting CH 123Document5 pagesAssignment Intermediate Accounting CH 123NELVA QABLINANo ratings yet

- Ch1-2 The Regulation FrameworkDocument14 pagesCh1-2 The Regulation Frameworkxu lNo ratings yet

- Lecture 2 - Financial Statements and AnalysisDocument58 pagesLecture 2 - Financial Statements and AnalysisMegat AlifNo ratings yet

- Reviewer (CFAS) - Chapter 1-13Document26 pagesReviewer (CFAS) - Chapter 1-13pilingat23-1851No ratings yet

- 6 International Financial StandardsDocument11 pages6 International Financial StandardsKanika GuptaNo ratings yet

- Ifrs Unit 5Document12 pagesIfrs Unit 5Deven LadNo ratings yet

- CFAS Notes Unit1Document2 pagesCFAS Notes Unit1BabeEbab AndreiNo ratings yet

- International Financial Statement AnalysisFrom EverandInternational Financial Statement AnalysisRating: 1 out of 5 stars1/5 (1)

- Managerial and Financial AccountingDocument42 pagesManagerial and Financial AccountingRodrigo de Oliveira LeiteNo ratings yet

- Ch.8 New Ventr DevpDocument18 pagesCh.8 New Ventr DevpRitik MishraNo ratings yet

- 2011-Innovprstrstrat Change201011102011Document11 pages2011-Innovprstrstrat Change201011102011wienna1987No ratings yet

- Test 5 Mutual Fund Nismtop500.in-1Document51 pagesTest 5 Mutual Fund Nismtop500.in-1अभिजीत आखाडेNo ratings yet

- Adjust Your Perspective.: Bloomberg Professional ServicesDocument8 pagesAdjust Your Perspective.: Bloomberg Professional ServicesGonzalo Ramírez VargasNo ratings yet

- Assessment of The Level of Financial Literacy Among Microentrepreneurs in Relation To Their Business GrowthDocument74 pagesAssessment of The Level of Financial Literacy Among Microentrepreneurs in Relation To Their Business Growthjovina dimacaleNo ratings yet

- Week 5Document6 pagesWeek 5Jeth Irah CostanNo ratings yet

- Specifications Guide: Asia Pacific and Middle East Crude OilDocument22 pagesSpecifications Guide: Asia Pacific and Middle East Crude OilAMANo ratings yet

- Kok Kok Mini Workshop - IB Presentation - 20230410Document10 pagesKok Kok Mini Workshop - IB Presentation - 20230410paxy sengoudoneNo ratings yet

- Maple Leaf Cement CompanyDocument35 pagesMaple Leaf Cement CompanyHira Mustafa ShahNo ratings yet

- Portfolio Construction Using Sharpe Index Model With Special Reference To Pharmaceutical, Banking, Construction, FMCG, and Oil&Gas SectorsDocument20 pagesPortfolio Construction Using Sharpe Index Model With Special Reference To Pharmaceutical, Banking, Construction, FMCG, and Oil&Gas SectorsHari VijayaNo ratings yet

- Pro Forma Models - StudentsDocument9 pagesPro Forma Models - Studentsshanker23scribd100% (1)

- Volume Discount PDFDocument1 pageVolume Discount PDFGrecia Loza CaballleroNo ratings yet

- Econ 101E (Hand-Out 3) 2019 - Basic Economy Study MethodsDocument7 pagesEcon 101E (Hand-Out 3) 2019 - Basic Economy Study MethodsFrancisco CarbonNo ratings yet

- University of Mauritius: Faculty of Law and ManagementDocument9 pagesUniversity of Mauritius: Faculty of Law and ManagementMîñåk ŞhïïNo ratings yet

- Golden Points of Options Flavour : Clarifications About Batman StrategyDocument5 pagesGolden Points of Options Flavour : Clarifications About Batman StrategyRohit NijampurkarNo ratings yet

- Dividend Discount Model: AssumptionsDocument27 pagesDividend Discount Model: AssumptionsSairam GovarthananNo ratings yet

- Finance Cheat Sheet - Formulas and Concepts - RM NISPEROSDocument27 pagesFinance Cheat Sheet - Formulas and Concepts - RM NISPEROSCHANDAN C KAMATHNo ratings yet

- Angel Broking LTD Project 03Document53 pagesAngel Broking LTD Project 03King Nitin AgnihotriNo ratings yet

- Order in The Respect of Shamken Multifab Limited and OrsDocument15 pagesOrder in The Respect of Shamken Multifab Limited and OrsShyam SunderNo ratings yet

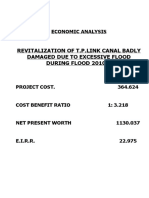

- Revitalization of T.P.Link Canal Badly Damaged Due To Excessive Flood During Flood 2010"Document4 pagesRevitalization of T.P.Link Canal Badly Damaged Due To Excessive Flood During Flood 2010"Xshf AkNo ratings yet

- Stock Loan MarketDocument45 pagesStock Loan MarketjoniakomNo ratings yet

- Statement of Cost of Good Sold (Aquino)Document9 pagesStatement of Cost of Good Sold (Aquino)John cookNo ratings yet

- Retail and Franchising: Simulation Presentation: Group 3Document10 pagesRetail and Franchising: Simulation Presentation: Group 3Aditya AnandNo ratings yet

- What Is Share Capital?: Company Receives Through Their Equity FinancingDocument6 pagesWhat Is Share Capital?: Company Receives Through Their Equity FinancingDominique B. PeronillaNo ratings yet

- Chapter 9 Cash Flow Analysis To Make Investment DecisionsDocument6 pagesChapter 9 Cash Flow Analysis To Make Investment DecisionstyNo ratings yet

- CAIIB-BFM Practice Que Set-1Document5 pagesCAIIB-BFM Practice Que Set-1Surya PillaNo ratings yet