Download as pdf or txt

You might also like

- The Sugarcube Sc-1 Mini: SweetvinylDocument2 pagesThe Sugarcube Sc-1 Mini: SweetvinylTaeMinKimNo ratings yet

- Drilling Fluids ManualDocument486 pagesDrilling Fluids ManualParaZzzit100% (12)

- 26 - LCCI L3 AC - Sep 2019 - ASE 20104 - MSDocument15 pages26 - LCCI L3 AC - Sep 2019 - ASE 20104 - MSKhin Zaw Htwe100% (6)

- Administrator's Guide To Portal Capabilities For Microsoft Dynamics 365 PDFDocument328 pagesAdministrator's Guide To Portal Capabilities For Microsoft Dynamics 365 PDFJohn DrewNo ratings yet

- Accounting StandardsDocument21 pagesAccounting Standardscontact.mvypNo ratings yet

- Accounting StandardsDocument816 pagesAccounting StandardsPavan KocherlakotaNo ratings yet

- Appendix 1Document16 pagesAppendix 1Chandan KumarNo ratings yet

- Accounting Standards Grp-1 Accounts by Accounts ManDocument52 pagesAccounting Standards Grp-1 Accounts by Accounts ManAlankritaNo ratings yet

- Unit 2Document30 pagesUnit 2Dibyansu KumarNo ratings yet

- Applicability of Accounting StandardsDocument151 pagesApplicability of Accounting StandardsSoum JaiswalNo ratings yet

- As Applicability For Non-CorporatesDocument9 pagesAs Applicability For Non-CorporatesAryan HateNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument12 pages© The Institute of Chartered Accountants of Indiajanardhan CA,CSNo ratings yet

- Applicability of Accounting Standards To Non CA. (DR.) S.B.ZawareDocument8 pagesApplicability of Accounting Standards To Non CA. (DR.) S.B.Zawarepramodmurkya13No ratings yet

- Financial Statement Analysis and Ratio AnalysisDocument29 pagesFinancial Statement Analysis and Ratio AnalysisNayana GoswamiNo ratings yet

- Accounting Standard MainDocument20 pagesAccounting Standard MainsweetektaNo ratings yet

- Accounting Standards 32Document91 pagesAccounting Standards 32bathinisridhar100% (3)

- Accounting Standard2Document24 pagesAccounting Standard2shajiNo ratings yet

- 62A Introduction of ASDocument3 pages62A Introduction of ASjoyboyishehereNo ratings yet

- Nestle Project - AccountsDocument31 pagesNestle Project - AccountsNishant Shah75% (4)

- Accounting Standard LLP - 05.11.2023Document10 pagesAccounting Standard LLP - 05.11.2023Mustafa MisriNo ratings yet

- AS-29 (Prov For CDocument25 pagesAS-29 (Prov For Capi-3828505No ratings yet

- Accounting Standard 170417Document32 pagesAccounting Standard 170417selvam sNo ratings yet

- Level II Entities Level III Entities Level IV EntitiesDocument1 pageLevel II Entities Level III Entities Level IV EntitiesNEHA NAYAKNo ratings yet

- CH 1Document42 pagesCH 1asah.201103No ratings yet

- Amity Business School: NoidaDocument10 pagesAmity Business School: NoidaMansi VermaNo ratings yet

- Accounting Standard (AS) 32: Financial Instruments: DisclosuresDocument31 pagesAccounting Standard (AS) 32: Financial Instruments: DisclosuresDesaraju Seshagiri RaoNo ratings yet

- Glimpse of Accounting Standards Group 1Document52 pagesGlimpse of Accounting Standards Group 1Rajesh Mahesh BohraNo ratings yet

- Rev CMA Topic 10 ASDocument35 pagesRev CMA Topic 10 ASPrakhar BalyanNo ratings yet

- Companies (Auditor's Report) Order, 2020: Companies Specifically Excluded From Its PurviewDocument4 pagesCompanies (Auditor's Report) Order, 2020: Companies Specifically Excluded From Its PurviewABINASHNo ratings yet

- Accounting Standard For MNCEDocument122 pagesAccounting Standard For MNCENithin KumarNo ratings yet

- Financial Reporting Disclosure Practices in Selected Small and Medium Enterprises (Smes) Listed On National Stock Exchange of IndiaDocument16 pagesFinancial Reporting Disclosure Practices in Selected Small and Medium Enterprises (Smes) Listed On National Stock Exchange of IndiaRajat RajatNo ratings yet

- FR NotesDocument83 pagesFR Noteskalyan.nNo ratings yet

- As 17 Segment ReportingDocument5 pagesAs 17 Segment ReportingcalvinroarNo ratings yet

- Paper 18Document153 pagesPaper 18ahmedNo ratings yet

- Ind AS 101Document114 pagesInd AS 101Manisha DeyNo ratings yet

- Analysis of Accounting Standards IFRS and IND ASDocument13 pagesAnalysis of Accounting Standards IFRS and IND ASEditor IJTSRDNo ratings yet

- Ind AS 1 & 8Document78 pagesInd AS 1 & 8Ajay JangirNo ratings yet

- Segment Reporting: Accounting Standard (AS) 17Document37 pagesSegment Reporting: Accounting Standard (AS) 17ca_amit_jainNo ratings yet

- 2.caro For Company AuditDocument43 pages2.caro For Company AuditchariNo ratings yet

- Quick Guide To Ind AsDocument39 pagesQuick Guide To Ind AsGayathri NathanNo ratings yet

- 74847bos60515 IntermediateDocument21 pages74847bos60515 IntermediateShubhamNo ratings yet

- CA Ajay Rathi Accounts BookDocument449 pagesCA Ajay Rathi Accounts BookNkume Irene100% (1)

- Indian Accounting Standards (Ind AS) : Basic ConceptsDocument18 pagesIndian Accounting Standards (Ind AS) : Basic ConceptsSivasankariNo ratings yet

- 74883bos60524 cp1Document42 pages74883bos60524 cp1cofinab795No ratings yet

- Accounting StandardDocument128 pagesAccounting StandardIndu GuptaNo ratings yet

- Introduction To Ind AsDocument24 pagesIntroduction To Ind AsRicha AgarwalNo ratings yet

- WRK Model Financial Statements SMEs PDFDocument86 pagesWRK Model Financial Statements SMEs PDFChaudhury Ahmed HabibNo ratings yet

- Related Party Disclosures: Accounting Standard (AS) 18Document13 pagesRelated Party Disclosures: Accounting Standard (AS) 18Prakash SivaNo ratings yet

- COVID 19 Finance Relief Application BR1 PDFDocument5 pagesCOVID 19 Finance Relief Application BR1 PDFThembinkosi Mthimkhulu ZakweNo ratings yet

- IND As Vs As ComparisonDocument42 pagesIND As Vs As ComparisonGeetikaNo ratings yet

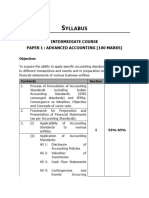

- SyllabusDocument2 pagesSyllabusdeepaksangwan1612No ratings yet

- 76830bos61899 InterDocument35 pages76830bos61899 InterShailesh BapnaNo ratings yet

- Compliances: Overview of Year End Under Companies Act, 2013Document89 pagesCompliances: Overview of Year End Under Companies Act, 2013Vijay MelwaniNo ratings yet

- Sample Chapter For WebDocument4 pagesSample Chapter For WebRizwan AkhtarNo ratings yet

- Discontinuing Operations: Accounting Standard (AS) 24Document22 pagesDiscontinuing Operations: Accounting Standard (AS) 24Sujit ChakrabortyNo ratings yet

- Company Accounting Australia New Zealand 5th Edition Jubb Solutions ManualDocument21 pagesCompany Accounting Australia New Zealand 5th Edition Jubb Solutions Manualjubasticky.vlvus2100% (24)

- SFRS For SE Statement of Applicability (2017)Document6 pagesSFRS For SE Statement of Applicability (2017)dgajudoNo ratings yet

- Weightages of CA Inter Group - 1Document35 pagesWeightages of CA Inter Group - 1Rohit PaulNo ratings yet

- CA Final Audit AmendmentDocument8 pagesCA Final Audit AmendmentSandesh LaddhaNo ratings yet

- Accounting StandardsDocument6 pagesAccounting StandardsJohnsonNo ratings yet

- 44AD As and What NotDocument82 pages44AD As and What NotParikshitNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- Maria Margaretha: Personal DetailDocument3 pagesMaria Margaretha: Personal DetailncocikaNo ratings yet

- Thời gian làm bài 120 phút, không kể thời gian giao đềDocument9 pagesThời gian làm bài 120 phút, không kể thời gian giao đềĐỗ Hoàng DũngNo ratings yet

- Chapter 4 Manual Assembly LinesDocument49 pagesChapter 4 Manual Assembly LinesRohit WadhwaniNo ratings yet

- Othello Final Summative Assessment Jessica ContrerasDocument3 pagesOthello Final Summative Assessment Jessica Contrerasapi-412495462No ratings yet

- Industry 40 PDFDocument5 pagesIndustry 40 PDFDonRafee RNo ratings yet

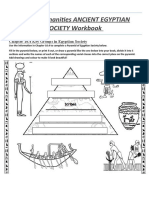

- ANCIENT EGYPTIAN SOCIETY WorkbookDocument7 pagesANCIENT EGYPTIAN SOCIETY WorkbookRick BartNo ratings yet

- Crating Web Forms Applications: by Ms. Madhura KutreDocument47 pagesCrating Web Forms Applications: by Ms. Madhura KutreAjit PatilNo ratings yet

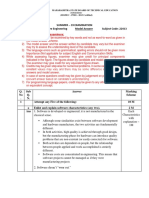

- 2019 Summer Model Answer Paper (Msbte Study Resources)Document34 pages2019 Summer Model Answer Paper (Msbte Study Resources)arvi.sardarNo ratings yet

- Topic Review Question and Case Study TopDocument6 pagesTopic Review Question and Case Study TopNorainah Abdul GaniNo ratings yet

- 4thh Quarter Pre TestDocument1 page4thh Quarter Pre TestAlona Camino100% (2)

- Air Brake 100D1 PDFDocument117 pagesAir Brake 100D1 PDFmarsauto2No ratings yet

- Nokia MEC in 5G White Paper enDocument13 pagesNokia MEC in 5G White Paper enarushi sharmaNo ratings yet

- Case Study in Safety ManagementDocument37 pagesCase Study in Safety ManagementVernie SorianoNo ratings yet

- World Religions-WPS OfficeDocument15 pagesWorld Religions-WPS OfficeZ Delante TamayoNo ratings yet

- Charles Keeping - Beowulf - PDFDocument16 pagesCharles Keeping - Beowulf - PDFra ayNo ratings yet

- Sap fb08 Amp f80 Tutorial Document ReversalDocument16 pagesSap fb08 Amp f80 Tutorial Document Reversalsaeedawais47No ratings yet

- Jacques Berlinerblau's CVDocument17 pagesJacques Berlinerblau's CVjdb75100% (1)

- CAPNOGRAPHYDocument10 pagesCAPNOGRAPHYJessica GuzmanNo ratings yet

- 15 3 16 - p.325 331 PDFDocument7 pages15 3 16 - p.325 331 PDFbeatcookNo ratings yet

- Proverbs 18-24 Ronnie LoudermilkDocument1 pageProverbs 18-24 Ronnie LoudermilkKeneth Chris NamocNo ratings yet

- Recruitment and Selection Kamini-200Document98 pagesRecruitment and Selection Kamini-200Mohammad ShoebNo ratings yet

- Stability of Floating BodiesDocument6 pagesStability of Floating Bodieskharry8davidNo ratings yet

- TR - Dressmaking NC IIDocument60 pagesTR - Dressmaking NC IIMR. CHRISTIAN DACORONNo ratings yet

- Stylistics Book For Bs7thDocument276 pagesStylistics Book For Bs7thKB BalochNo ratings yet

- Development and Use of Non-Digital and Conventional Instructional MaterialsDocument17 pagesDevelopment and Use of Non-Digital and Conventional Instructional MaterialsAmy Apelado ApigoNo ratings yet

- 45ACP Hollow PointDocument5 pages45ACP Hollow PointTactic Otd ArgNo ratings yet