Download as pdf or txt

You might also like

- CFO Job Description DRAFTDocument3 pagesCFO Job Description DRAFTpatrickNo ratings yet

- A Report On Capital Structure of BHELDocument17 pagesA Report On Capital Structure of BHELRAVI RAUSHAN JHANo ratings yet

- BT GroupDocument14 pagesBT GroupAsif SafdarNo ratings yet

- Privatization in PakistanDocument4 pagesPrivatization in PakistanArshgee100% (1)

- Acknowledgemnt: Department of Management, BIT MesraDocument28 pagesAcknowledgemnt: Department of Management, BIT Mesraanuj191087No ratings yet

- MPRA Paper 116388Document56 pagesMPRA Paper 116388Hania ZafarNo ratings yet

- Mains July 2020Document69 pagesMains July 2020kela vinesNo ratings yet

- Privatization of PTCL. An Unforgotten Failure of Governance: A Public Management Case StudyDocument5 pagesPrivatization of PTCL. An Unforgotten Failure of Governance: A Public Management Case StudyImran SaddiqueNo ratings yet

- Infrastructure of Indian Economy: Power and Energy SectorDocument25 pagesInfrastructure of Indian Economy: Power and Energy SectorsanahbijlaniNo ratings yet

- Weekly CA - 2 JanDocument10 pagesWeekly CA - 2 JanNice YadavNo ratings yet

- Research Report "Privatization of PTCL": Business Research Methods Submitted To Group MembersDocument61 pagesResearch Report "Privatization of PTCL": Business Research Methods Submitted To Group MembersTanveer Hassan SiddiquiNo ratings yet

- This Content Downloaded From 14.139.123.52 On Sat, 13 Nov 2021 18:51:34 UTCDocument10 pagesThis Content Downloaded From 14.139.123.52 On Sat, 13 Nov 2021 18:51:34 UTCSanjana KoliNo ratings yet

- Competition in The Digital MarketplaceDocument8 pagesCompetition in The Digital MarketplaceTamara UrrutiaNo ratings yet

- Public Sector Enterprises ReformsDocument28 pagesPublic Sector Enterprises Reformsamit1234No ratings yet

- PrivatizationDocument12 pagesPrivatizationMahima GirdharNo ratings yet

- Managerial EconomicsDocument8 pagesManagerial EconomicsBishal RoyNo ratings yet

- Business and Environment - noPWDocument5 pagesBusiness and Environment - noPWcitizendenepal_77No ratings yet

- Looking To The Future PDFDocument8 pagesLooking To The Future PDFHadiBiesNo ratings yet

- Advantages For Centre From PSU Oil MergersDocument10 pagesAdvantages For Centre From PSU Oil Mergerstechnoconsulting4smbsNo ratings yet

- Privatization and Disinvestment: BY: Apala Gupta Garima Soni Minakshi Sinha Shraddha ChapekarDocument39 pagesPrivatization and Disinvestment: BY: Apala Gupta Garima Soni Minakshi Sinha Shraddha ChapekarvinodkumardasNo ratings yet

- KG Gas Scam - 1309510105Document3 pagesKG Gas Scam - 1309510105Kumar PrashantNo ratings yet

- Disinvestment and PrivatisationDocument30 pagesDisinvestment and PrivatisationSantosh MashalNo ratings yet

- Disinvestment and PrivatisationDocument40 pagesDisinvestment and Privatisationpiyush909No ratings yet

- Overview On Merger and AcquisitionDocument4 pagesOverview On Merger and AcquisitionraihanNo ratings yet

- Union Budget 2018-19Document17 pagesUnion Budget 2018-19InvesTrekkNo ratings yet

- Disinvestment Petrochemical Industry: Boon or A BaneDocument7 pagesDisinvestment Petrochemical Industry: Boon or A BanePrachi PawarNo ratings yet

- Disinvestment NeelamDocument39 pagesDisinvestment NeelamvaidwaraNo ratings yet

- Restructuring of The Nigerian Electricity Industry: A Partial Equilibrium AnalysisDocument20 pagesRestructuring of The Nigerian Electricity Industry: A Partial Equilibrium Analysisadwa_anj89No ratings yet

- Does Privatization Effect PerformanceDocument12 pagesDoes Privatization Effect PerformanceWaseem ShahNo ratings yet

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDocument15 pagesPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamNo ratings yet

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDocument15 pagesPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamNo ratings yet

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDocument15 pagesPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamNo ratings yet

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDocument15 pagesPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamNo ratings yet

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDocument15 pagesPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamNo ratings yet

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDocument15 pagesPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamNo ratings yet

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDocument15 pagesPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamNo ratings yet

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDocument15 pagesPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamNo ratings yet

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDocument15 pagesPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamNo ratings yet

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDocument15 pagesPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamNo ratings yet

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDocument15 pagesPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamNo ratings yet

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDocument15 pagesPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamNo ratings yet

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDocument15 pagesPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamNo ratings yet

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDocument15 pagesPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamNo ratings yet

- Potential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractDocument15 pagesPotential Petroleum Revenues For The Government of Kenya: Implications of The Proposed 2015 Model Production Sharing ContractOxfamNo ratings yet

- 17 KoreaDocument5 pages17 KoreaGabriel PotarcaNo ratings yet

- Muhammad Reza Adi - Assignment 5BDocument6 pagesMuhammad Reza Adi - Assignment 5BReza AdiNo ratings yet

- Bharat Petroleum Corporation LTDDocument15 pagesBharat Petroleum Corporation LTDsagunkumarNo ratings yet

- Indian Power IndustryDocument10 pagesIndian Power IndustryuttamrungtaNo ratings yet

- Bhel Divestment Strategy AnalysisDocument9 pagesBhel Divestment Strategy AnalysisHimanshu JoshiNo ratings yet

- Economic Survey 2019-20Document22 pagesEconomic Survey 2019-20Akash SherryNo ratings yet

- British PetroleumDocument6 pagesBritish PetroleumtejaNo ratings yet

- What Future Pfi PPPDocument38 pagesWhat Future Pfi PPPasdf789456123No ratings yet

- M&A Submission2Document3 pagesM&A Submission2Shikhar AroraNo ratings yet

- Wage Determination in The Irish EconomyDocument15 pagesWage Determination in The Irish EconomyBerliana CristinNo ratings yet

- A Ril 22 ProjectDocument13 pagesA Ril 22 ProjectAKANSHAm mGUPTANo ratings yet

- BPs Office of The Chief Technology Officer ADocument14 pagesBPs Office of The Chief Technology Officer AArnold TampubolonNo ratings yet

- Test 9 - Economics - II-ANSKEY - FinalDocument16 pagesTest 9 - Economics - II-ANSKEY - FinalsachinstinNo ratings yet

- National Monetization PipelineDocument4 pagesNational Monetization PipelinemouliNo ratings yet

- Global Reform Oview Epw 066A02 PDFDocument24 pagesGlobal Reform Oview Epw 066A02 PDFsuderNo ratings yet

- The Regulatory Environment: Part Two of The Investors' Guide to the United Kingdom 2015/16From EverandThe Regulatory Environment: Part Two of The Investors' Guide to the United Kingdom 2015/16No ratings yet

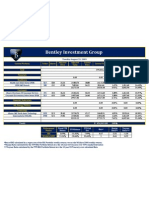

- Bentley Investment Group: Tuesday August 25, 2009Document1 pageBentley Investment Group: Tuesday August 25, 2009bentleyinvestmentgroupNo ratings yet

- ECE8803 Syllabus Sp2015Document2 pagesECE8803 Syllabus Sp2015Saad MuftahNo ratings yet

- ch01R StudentDocument70 pagesch01R StudentChuan ShihNo ratings yet

- Receivables and Revenue RecognitionDocument21 pagesReceivables and Revenue RecognitionLu CasNo ratings yet

- Financial Statement Analysis: Mcgraw-Hill/IrwinDocument42 pagesFinancial Statement Analysis: Mcgraw-Hill/IrwinDiana Fernandez MagnoNo ratings yet

- Mago Et AlDocument4 pagesMago Et AlSonia PortugaleteNo ratings yet

- Investments Chapter 1 Powerpoint SlideDocument11 pagesInvestments Chapter 1 Powerpoint SlideDénise RafaëlNo ratings yet

- M A PlaybookDocument24 pagesM A PlaybookDwayne JohnsonNo ratings yet

- Howden Capabilities Oct 2017 ScreenDocument68 pagesHowden Capabilities Oct 2017 ScreenukdealsNo ratings yet

- Sarah Lowthian.: Hello My Name IsDocument3 pagesSarah Lowthian.: Hello My Name Isapi-225679366No ratings yet

- Lesson 2 Career OpportunitiesDocument24 pagesLesson 2 Career OpportunitiesQueen AzurNo ratings yet

- CIPFA Diploma in Contract Management 11 2019Document5 pagesCIPFA Diploma in Contract Management 11 2019kaafiNo ratings yet

- Business Ethics/ Social Responsibility/ Environmental SustainabilityDocument28 pagesBusiness Ethics/ Social Responsibility/ Environmental SustainabilityEnnAoeihG PajarinNo ratings yet

- Ronald Shone - An Introduction To Economic Dynamics (2001, Cambridge University Press) PDFDocument235 pagesRonald Shone - An Introduction To Economic Dynamics (2001, Cambridge University Press) PDFPedro Camargo100% (1)

- EU Food and Drink IndustryDocument9 pagesEU Food and Drink IndustryMuhammad HarisNo ratings yet

- Expansion of The Menu Option DescriptionDocument57 pagesExpansion of The Menu Option DescriptionGeraldine NkankumeNo ratings yet

- Exercises 20.4A Bad DebtsDocument1 pageExercises 20.4A Bad DebtsCarolnesa Dorie Tan Kar MeanNo ratings yet

- 1530266570ECO P11 M28 E-TextDocument12 pages1530266570ECO P11 M28 E-TextMonika SainiNo ratings yet

- Session 10 Simulation QuestionsDocument6 pagesSession 10 Simulation QuestionsireneNo ratings yet

- Assignment - Banking & InsuranceDocument4 pagesAssignment - Banking & Insurancesandeep_kadam_7No ratings yet

- Implementation of Tax Regulations On Internet-Based Business Activity Case Study: Google'S Tax Avoidance in IndonesiaDocument11 pagesImplementation of Tax Regulations On Internet-Based Business Activity Case Study: Google'S Tax Avoidance in IndonesiagilangNo ratings yet

- Chapter 5 Job Order Costing.Document6 pagesChapter 5 Job Order Costing.hafiz100% (1)

- Acculi Labs' Lyfas PDFDocument8 pagesAcculi Labs' Lyfas PDFHbNo ratings yet

- Caiib Study PlanDocument17 pagesCaiib Study PlanPrabhat KrNo ratings yet

- ECO720 Global and Regional Economic Development FinalsDocument13 pagesECO720 Global and Regional Economic Development FinalsJohn TanNo ratings yet

- Most Important Reports & Indexes 2024Document1 pageMost Important Reports & Indexes 2024mail2saadmisbahNo ratings yet

- Case SPMDocument4 pagesCase SPMainiNo ratings yet

- Entrepreneurship 31 PDF FreeDocument19 pagesEntrepreneurship 31 PDF FreeLovern Kaye RonquilloNo ratings yet

- BBA 1st Financial AccountingDocument3 pagesBBA 1st Financial AccountingAbbas Sky50% (4)