Download as pdf or txt

You might also like

- SIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)From EverandSIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2023 Edition)Rating: 5 out of 5 stars5/5 (1)

- CBRE Vietnam Market Outlook 2024 - ENDocument50 pagesCBRE Vietnam Market Outlook 2024 - ENtudanchuyNo ratings yet

- Intermediate Accounting 11th Edition Nikolai Test BankDocument47 pagesIntermediate Accounting 11th Edition Nikolai Test Bankheathernewtonedsxrcakbz100% (18)

- Test Bank For Financial and Managerial Accounting 15th Edition Jan WilliamsDocument78 pagesTest Bank For Financial and Managerial Accounting 15th Edition Jan WilliamsArnold Thompson100% (3)

- Audit ExamDocument29 pagesAudit Exam101bus85% (13)

- Fusionbanking Equation Swo PDFDocument12 pagesFusionbanking Equation Swo PDFJoseph Muzite0% (1)

- The Role of The Public Accountant in The American EconomyDocument22 pagesThe Role of The Public Accountant in The American EconomyShaika HaceenaNo ratings yet

- The Role of The Public Accountant in The American EconomyDocument53 pagesThe Role of The Public Accountant in The American EconomyJorecan Enad DacupNo ratings yet

- Principles of Auditing and Other Assurance Services Chap 001Document23 pagesPrinciples of Auditing and Other Assurance Services Chap 001vikkiNo ratings yet

- TB 1 - Mohammad MarufDocument10 pagesTB 1 - Mohammad MarufFalak EnayatNo ratings yet

- TBCH01Document6 pagesTBCH01Arnyl ReyesNo ratings yet

- CHAP 1.the Demand For Audit and Other Assurance ServicesDocument11 pagesCHAP 1.the Demand For Audit and Other Assurance ServicesNoroNo ratings yet

- Far Eastern University - Manila: Open Using Adobe Reader and PCDocument5 pagesFar Eastern University - Manila: Open Using Adobe Reader and PCKristine TiuNo ratings yet

- Questions and AnswersDocument20 pagesQuestions and AnswersJi YuNo ratings yet

- Chapter 1 Auditing IntegralDocument7 pagesChapter 1 Auditing IntegralAb CNo ratings yet

- ACCO 20063 Homework 3 Review of Conceptual FrameworkDocument8 pagesACCO 20063 Homework 3 Review of Conceptual FrameworkVincent Luigil AlceraNo ratings yet

- Old Batch Test-2Document6 pagesOld Batch Test-2Sanjida KhanNo ratings yet

- Multiple Choice Taller 2 Favor de Indicar Su NombreDocument4 pagesMultiple Choice Taller 2 Favor de Indicar Su NombrerafnellieNo ratings yet

- Chapter 1: The Demand For Audit and Other Assurance ServicesDocument32 pagesChapter 1: The Demand For Audit and Other Assurance Servicessamuel debebeNo ratings yet

- Audit ExamDocument29 pagesAudit Examthangdongquay152100% (2)

- Audit Assessment True or False and MCQ - CompressDocument8 pagesAudit Assessment True or False and MCQ - CompressHazel BawasantaNo ratings yet

- QB Introduction To FSADocument7 pagesQB Introduction To FSASarthak MalhotraNo ratings yet

- Comprehensive Reviewer Auditing TheoryDocument91 pagesComprehensive Reviewer Auditing TheoryMary Rose JuanNo ratings yet

- Audit Ch. 1 3 FlashcardsDocument20 pagesAudit Ch. 1 3 Flashcardst5nhakhobauNo ratings yet

- Test Bank For Auditing An InternationalDocument17 pagesTest Bank For Auditing An Internationalnevilalopariyahoo.comNo ratings yet

- Comprehensive Reviewer Auditing TheoryDocument54 pagesComprehensive Reviewer Auditing TheoryMc Bryan Barlizo100% (2)

- Basic AudDocument3 pagesBasic AudMary Rose JuanNo ratings yet

- 1 - Cfa-2018-Quest-Bank-R21-Financial-Statement-Analysis-An-Introduction-Q-BankDocument7 pages1 - Cfa-2018-Quest-Bank-R21-Financial-Statement-Analysis-An-Introduction-Q-BankQuyen Thanh NguyenNo ratings yet

- Auditing Chapter 1Document3 pagesAuditing Chapter 1Mark Anthony Casuga SiotingNo ratings yet

- Reviewer Auditing TheoryDocument59 pagesReviewer Auditing Theoryunexpected thingsNo ratings yet

- Financial Accounting 11th Edition Albrecht Test BankDocument20 pagesFinancial Accounting 11th Edition Albrecht Test BankBeckyCareyranxj100% (11)

- 111年會考 審計學題庫 kiem toan can ban engDocument17 pages111年會考 審計學題庫 kiem toan can ban engphannhi1632004No ratings yet

- DescriptionDocument32 pagesDescriptionShiko TharwatNo ratings yet

- Exam 1 Review SheetDocument12 pagesExam 1 Review SheetjhouvanNo ratings yet

- TestbankDocument93 pagesTestbankMack Ray O. Paredes100% (1)

- Exercise Ch1Document4 pagesExercise Ch1MayadaNo ratings yet

- Auditing and Assurance Services An Applied Approach 1st Edition Stuart Test BankDocument81 pagesAuditing and Assurance Services An Applied Approach 1st Edition Stuart Test BankMichaelMasseyfsmpxNo ratings yet

- Auditing Theory - 1Document9 pagesAuditing Theory - 1Kageyama HinataNo ratings yet

- Revision Chapter 1Document6 pagesRevision Chapter 1ahmed shebl100% (1)

- Auditing Theory Answer Key 5Document3 pagesAuditing Theory Answer Key 5Jasper GicaNo ratings yet

- Chapter 1Document14 pagesChapter 1ANH NGUYEN THI THUYNo ratings yet

- Audit Test Bank Chap10Document27 pagesAudit Test Bank Chap10Yen0% (1)

- Prehensive Review-Auditing TheoryDocument71 pagesPrehensive Review-Auditing TheoryemmanvillafuerteNo ratings yet

- Audit TheoryDocument17 pagesAudit TheoryFrancis Martin100% (2)

- 111年會考 審計學題庫Document15 pages111年會考 審計學題庫張巧薇No ratings yet

- AT PrelimDocument32 pagesAT Prelimfer maNo ratings yet

- Audit Mcqs Ricchiute Test BankDocument30 pagesAudit Mcqs Ricchiute Test BankjpbluejnNo ratings yet

- Exercise AuditingDocument3 pagesExercise Auditingkris mNo ratings yet

- Chapter 01 - Accounting: Information For Decision MakingDocument89 pagesChapter 01 - Accounting: Information For Decision Makingyujia ZhaiNo ratings yet

- AT QuizDocument15 pagesAT QuizClydeNo ratings yet

- RicchiuteGroup2 Ch1 20Document89 pagesRicchiuteGroup2 Ch1 20Gabriel OrolfoNo ratings yet

- Financial and Managerial Accounting Information For Decision MakingDocument77 pagesFinancial and Managerial Accounting Information For Decision Makingsat satw100% (1)

- True / False QuestionsDocument19 pagesTrue / False QuestionsRizza OmalinNo ratings yet

- RicchiuteGroup2 Ch1 20Document93 pagesRicchiuteGroup2 Ch1 20Sherine Lois QuiambaoNo ratings yet

- Auditing Multiple ChoiceDocument11 pagesAuditing Multiple Choiceunique_vn100% (1)

- Auditing A Business Risk Approach 8th Edition Rittenberg Test BankDocument39 pagesAuditing A Business Risk Approach 8th Edition Rittenberg Test BankWilliamMcphersonmifzjNo ratings yet

- Internal ControlDocument4 pagesInternal ControlShaira Mikaela CasiñoNo ratings yet

- Louwers - Auditing and Assurance Services 4eDocument74 pagesLouwers - Auditing and Assurance Services 4eChristian Ray DetranNo ratings yet

- Audit Risk Alert: General Accounting and Auditing Developments 2018/19From EverandAudit Risk Alert: General Accounting and Auditing Developments 2018/19No ratings yet

- Audit Risk Alert: General Accounting and Auditing Developments, 2017/18From EverandAudit Risk Alert: General Accounting and Auditing Developments, 2017/18No ratings yet

- Audit Risk Alert: Government Auditing Standards and Single Audit Developments: Strengthening Audit Integrity 2018/19From EverandAudit Risk Alert: Government Auditing Standards and Single Audit Developments: Strengthening Audit Integrity 2018/19No ratings yet

- Payment ReceiptDocument1 pagePayment ReceiptRISHABHNo ratings yet

- Doing Business With WillScotDocument7 pagesDoing Business With WillScotWilliamsNo ratings yet

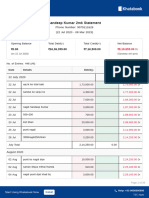

- Khatabook-Customer-Transactions-09 12 2023-04 45 01 PMDocument26 pagesKhatabook-Customer-Transactions-09 12 2023-04 45 01 PMPawan NayakNo ratings yet

- Understanding Media Extra QuestionsDocument3 pagesUnderstanding Media Extra QuestionsRishit SinhaNo ratings yet

- Internship Report: University of DhakaDocument45 pagesInternship Report: University of Dhakaketan dontamsettiNo ratings yet

- Insurance Company in SylhetDocument7 pagesInsurance Company in SylhetAhmed Al MasudNo ratings yet

- NakakaxDocument3 pagesNakakaxPaula Villarubia100% (1)

- TCC234Document1 pageTCC234Hardik ShahNo ratings yet

- Introduction and Web Development Strategies / Web TeamDocument3 pagesIntroduction and Web Development Strategies / Web TeamlalithaNo ratings yet

- Brinda Project FinalDocument94 pagesBrinda Project FinalChaithra M100% (1)

- Banking Products and Sevices FinalDocument17 pagesBanking Products and Sevices Finaljevesh9No ratings yet

- Name: Venkata Naga Jagadeesh Appana Client Code: 57995415 Pan No: Bcfpa6131A Pin: 533125Document3 pagesName: Venkata Naga Jagadeesh Appana Client Code: 57995415 Pan No: Bcfpa6131A Pin: 533125sagar lovzNo ratings yet

- Level of ServiceDocument3 pagesLevel of ServicesateeshNo ratings yet

- Supply Chain Network of CampinaDocument2 pagesSupply Chain Network of CampinaTri BebeNo ratings yet

- BANK RECONCILIATION EXERCISE - Sheet1Document3 pagesBANK RECONCILIATION EXERCISE - Sheet1shayndelamagaNo ratings yet

- ADC PresentationDocument16 pagesADC PresentationNusha TabassumNo ratings yet

- Memecoin White PaperDocument26 pagesMemecoin White PaperKago KhachanaNo ratings yet

- TLTA Associates Directory: Company County City Member TypeDocument31 pagesTLTA Associates Directory: Company County City Member Typeranjith123No ratings yet

- الهجمات السيبرانية على القطاع البنكي التهديدات والحلول - فادي الأسوديDocument16 pagesالهجمات السيبرانية على القطاع البنكي التهديدات والحلول - فادي الأسوديikuytrfNo ratings yet

- MicrosoftDocument2 pagesMicrosoftKrisi MartinezNo ratings yet

- Definition of Distribution Logistics From The Producer To The CustomerDocument2 pagesDefinition of Distribution Logistics From The Producer To The CustomerAndrean MaulanaNo ratings yet

- Quansheng Uv k5 Two Way RadioDocument12 pagesQuansheng Uv k5 Two Way Radioairbus75No ratings yet

- Nokia Flexi Zone Pico Product DescriptionDocument59 pagesNokia Flexi Zone Pico Product DescriptionhoquangNo ratings yet

- 2017 Franchise Operations Manual-1-160Document160 pages2017 Franchise Operations Manual-1-160merkaberototalNo ratings yet

- Form SL-C: Claims Must Be Submitted Within 3 Months of Incurred Expenses With All Receipts and Proof of AttendanceDocument1 pageForm SL-C: Claims Must Be Submitted Within 3 Months of Incurred Expenses With All Receipts and Proof of AttendancedrakeNo ratings yet

- ACT502 Assignment - Sem 2 - 2018Document5 pagesACT502 Assignment - Sem 2 - 2018tgmn4kssd2No ratings yet

- EUR Statement: Account SummaryDocument2 pagesEUR Statement: Account SummarySW ProjectNo ratings yet

- Account Closure RequestDocument1 pageAccount Closure Requestanilmourya5No ratings yet