Download as pdf or txt

You might also like

- The Ultimate UKCAT Guide: 1250 Practice QuestionsFrom EverandThe Ultimate UKCAT Guide: 1250 Practice QuestionsRating: 5 out of 5 stars5/5 (1)

- 4995628Document5 pages4995628mohitgaba19100% (1)

- Ia@uclan Ac UkDocument2 pagesIa@uclan Ac UkJap KhambholiyaNo ratings yet

- Rejo Coventry CLOADocument5 pagesRejo Coventry CLOAChinmaya SekharNo ratings yet

- SARS Comprehensive Guide To The ITR12 Return For IndividualsDocument102 pagesSARS Comprehensive Guide To The ITR12 Return For IndividualsNick BesterNo ratings yet

- ADIT Prospectus 2018Document40 pagesADIT Prospectus 2018Alan HgNo ratings yet

- Final Jnu IbDocument93 pagesFinal Jnu IbMONEY WEALTH HUBNo ratings yet

- Final Jnu IbDocument93 pagesFinal Jnu IbSima DeyNo ratings yet

- 07412.May2017.Exam PaperDocument13 pages07412.May2017.Exam PaperSasidharan RajendranNo ratings yet

- College Development PresentationDocument64 pagesCollege Development PresentationPrabhdeep Singh DhanjalNo ratings yet

- AI & Data Science Degree - Sep' 2024Document2 pagesAI & Data Science Degree - Sep' 2024Asterix ObelixNo ratings yet

- Mbarara University Fees PolicyDocument19 pagesMbarara University Fees PolicyRaymond Alinetu100% (1)

- ADIT Prospectus 2016Document28 pagesADIT Prospectus 2016zenofiaNo ratings yet

- Vikash Offer LetterDocument5 pagesVikash Offer LetterabhayjiktlNo ratings yet

- CUCoM JOINING 2022 2023Document9 pagesCUCoM JOINING 2022 2023ABDULSWAMADU KARIMUNo ratings yet

- Registration GuideDocument13 pagesRegistration Guidenzuliana.majidNo ratings yet

- Internship Training in Noida Metro Rail Corporation (NMRC) : YEAR - 2022Document6 pagesInternship Training in Noida Metro Rail Corporation (NMRC) : YEAR - 2022SAI Charan GoudNo ratings yet

- Conditional OfferLetter 31410 31410 20228285916Document6 pagesConditional OfferLetter 31410 31410 20228285916Md ZainNo ratings yet

- 9Th Jamia National Moot Court Competition, 2022Document17 pages9Th Jamia National Moot Court Competition, 2022Anshu kumarNo ratings yet

- Academic Session 2022-23 Offer of Admission To Bachelor of Technology in Electrical and Computer EngineeringDocument4 pagesAcademic Session 2022-23 Offer of Admission To Bachelor of Technology in Electrical and Computer EngineeringHacking TimeNo ratings yet

- 1st CCI PU Moot RulesDocument19 pages1st CCI PU Moot RulesSHIVAM SHARMANo ratings yet

- 1st CCI PU Moot RulesDocument19 pages1st CCI PU Moot RulesSHIVAM SHARMANo ratings yet

- Dry Van Container Exam Information BulletinDocument12 pagesDry Van Container Exam Information Bulletinsahil josephNo ratings yet

- 9th JNMCC 2022 BrochureDocument17 pages9th JNMCC 2022 BrochureKunwarbir Singh lohatNo ratings yet

- Nwadike Elochukwumarcel Offer Letter 220630 171641Document3 pagesNwadike Elochukwumarcel Offer Letter 220630 171641k9phcfsj8vNo ratings yet

- B.SC GeneralDocument76 pagesB.SC Generalme.sarveshpathakNo ratings yet

- Fees Policy: Date First Approved: Date of Effect: Date Last Amended: Date of Next ReviewDocument30 pagesFees Policy: Date First Approved: Date of Effect: Date Last Amended: Date of Next ReviewNadia Tul JannatNo ratings yet

- MCCQE Part I Medical Council of CanadaDocument1 pageMCCQE Part I Medical Council of Canadasara borjianNo ratings yet

- MBBS Batch 8 1 1Document1 pageMBBS Batch 8 1 1Syed HassanNo ratings yet

- De-220609-193936-Exam Notification For B Tech B.pharm IV-II Reg - Supply IV-I Supply June-2022Document12 pagesDe-220609-193936-Exam Notification For B Tech B.pharm IV-II Reg - Supply IV-I Supply June-2022R N D GIPSNo ratings yet

- Cbe Joining Instruction For Diploma 1 September Intake 2023-2024 Jif2Document10 pagesCbe Joining Instruction For Diploma 1 September Intake 2023-2024 Jif2Daniel EudesNo ratings yet

- Fee Information: Staffordshire University ProgrammeDocument1 pageFee Information: Staffordshire University ProgrammeLương TrầnNo ratings yet

- Deferral CLoO - Mohammed Miraj - 4021615 GCB+MIB Feb22Document17 pagesDeferral CLoO - Mohammed Miraj - 4021615 GCB+MIB Feb22mr copy xeroxNo ratings yet

- Notification AIOAT 2022Document2 pagesNotification AIOAT 2022pritam kumarNo ratings yet

- Cbe Joining Instructions For Post Graduate Programmes September 2023-2024Document12 pagesCbe Joining Instructions For Post Graduate Programmes September 2023-2024Daniel EudesNo ratings yet

- Admission Notice DBTDocument2 pagesAdmission Notice DBTwebiisNo ratings yet

- Ict ADocument40 pagesIct ALufreyNo ratings yet

- Brochure-Int-MTech-2023-24-Copy 22-02-2023Document12 pagesBrochure-Int-MTech-2023-24-Copy 22-02-2023Pratyush AnandNo ratings yet

- Tamkang University in Taiwan Handbook 2020 Latest InformationDocument58 pagesTamkang University in Taiwan Handbook 2020 Latest InformationFadilah KamilahNo ratings yet

- The Tamil Nadu Dr. Ambedkar Law University: "Poompozhil", 5, Dr. D.G.S. Dinakaran Salai, Chennai - 600 028Document1 pageThe Tamil Nadu Dr. Ambedkar Law University: "Poompozhil", 5, Dr. D.G.S. Dinakaran Salai, Chennai - 600 028Anbarasi ThenuNo ratings yet

- Education Prices 202223 Institute of Chartered ShipbrokersDocument1 pageEducation Prices 202223 Institute of Chartered ShipbrokersBhanu Pratap RathoreNo ratings yet

- 1 NS CG K2CDocument9 pages1 NS CG K2Cxiaoya zhaiNo ratings yet

- Pearson Edexcel Ear On 23Document2 pagesPearson Edexcel Ear On 23Nazia EnayetNo ratings yet

- Provisional Selection List - M ComDocument3 pagesProvisional Selection List - M ComAachal SinghNo ratings yet

- MSC Info Security Feeschedule 2022 2023Document4 pagesMSC Info Security Feeschedule 2022 2023moonwaince8No ratings yet

- Conditional OfferDocument12 pagesConditional Offer6249kcgqvcNo ratings yet

- Conditional Offer Letter - Mr. Syed Ali - LGSiDP - Class of 2025Document2 pagesConditional Offer Letter - Mr. Syed Ali - LGSiDP - Class of 2025ALI Qasim FitnessNo ratings yet

- CPA Students Brochure NewDocument8 pagesCPA Students Brochure NewTunone Julius100% (1)

- CIOTDocument34 pagesCIOTLukas CNo ratings yet

- International Business Feeschedule 2019 20 PDFDocument3 pagesInternational Business Feeschedule 2019 20 PDFAndrea Gonzalez MercadoNo ratings yet

- TRANTuanDat BIT LetterofOfferDocument9 pagesTRANTuanDat BIT LetterofOfferTrang Tran ThuNo ratings yet

- De-221221-133508-Notification For IV I BTech BPharm and IV I MinorDegree Jan2023 ExamsDocument11 pagesDe-221221-133508-Notification For IV I BTech BPharm and IV I MinorDegree Jan2023 ExamsBollam Pragnya 518No ratings yet

- LLM Feeschedule 2021 2022Document3 pagesLLM Feeschedule 2021 2022Naroz AliNo ratings yet

- UK Bases Becas Master ENDocument7 pagesUK Bases Becas Master ENoklllNo ratings yet

- Information BulletinDocument87 pagesInformation BulletinGulshan ShahNo ratings yet

- Graduate Diploma Programme - Fee: A. Fee Payable To ISBFDocument2 pagesGraduate Diploma Programme - Fee: A. Fee Payable To ISBFrajni chaturvediNo ratings yet

- Anjum Ahitan Conditional Offer 2760762Document5 pagesAnjum Ahitan Conditional Offer 2760762abhayjiktlNo ratings yet

- Registration Guide: MAY 2021 SemesterDocument11 pagesRegistration Guide: MAY 2021 Semesterfaiza yusufNo ratings yet

- ADIT Principles of International Taxation Module BrochureDocument4 pagesADIT Principles of International Taxation Module BrochureLady Campos BallartaNo ratings yet

- Ashwani MBA Business Management (UOB) - Conditional Offer Letter April 2023Document2 pagesAshwani MBA Business Management (UOB) - Conditional Offer Letter April 2023akashNo ratings yet

- Information Brochure: Ph.D. Admissions 2018Document5 pagesInformation Brochure: Ph.D. Admissions 2018Anonymous Zec5hjG9fNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- Guidelines - Piggery - NMPS (2012-13) 2Document6 pagesGuidelines - Piggery - NMPS (2012-13) 2Ravi KumarNo ratings yet

- Food Safety Audit Working Paper SANSDocument99 pagesFood Safety Audit Working Paper SANSRavi KumarNo ratings yet

- ANB StartupsDocument12 pagesANB StartupsRavi KumarNo ratings yet

- Project Liquid GlassDocument19 pagesProject Liquid GlassRavi KumarNo ratings yet

- SOFC - FY22 SOFC Peer Review Overview Report - 03232022Document25 pagesSOFC - FY22 SOFC Peer Review Overview Report - 03232022Ravi KumarNo ratings yet

- Note 6 Situs (Sources) of IncomeDocument3 pagesNote 6 Situs (Sources) of IncomeJason Robert MendozaNo ratings yet

- Employee Master File Creation Form: Form: Pay01 (Applicable For Both Payroll and GP Fund)Document3 pagesEmployee Master File Creation Form: Form: Pay01 (Applicable For Both Payroll and GP Fund)Hameed TerichNo ratings yet

- BillDocument1 pageBillSowmya DNo ratings yet

- Tax Invoice / Bill of SupplyDocument2 pagesTax Invoice / Bill of SupplySiddharth DasNo ratings yet

- Tax-May 8Document1 pageTax-May 8Ella Apelo100% (1)

- Mahaveer Enterprises: Tax InvoiceDocument1 pageMahaveer Enterprises: Tax InvoiceAyush SrivastavNo ratings yet

- Financial Accounting Volume ThreeDocument32 pagesFinancial Accounting Volume ThreeJennybabe PetaNo ratings yet

- Accounting VoucherDocument1 pageAccounting VoucherAnonymous eKt1FCDNo ratings yet

- Cori Preftakes Cash Flow Analysis ToolDocument6 pagesCori Preftakes Cash Flow Analysis ToolcpreftakesNo ratings yet

- Confirmation For Booking ID # 694245897 SarathDocument1 pageConfirmation For Booking ID # 694245897 Sarathbindu mathaiNo ratings yet

- Tc-2421green Power SolutionDocument1 pageTc-2421green Power SolutionHussain ShaikhNo ratings yet

- 3 - BAF - Direct Tax IDocument3 pages3 - BAF - Direct Tax Isid pjNo ratings yet

- International JVs Feb 2010Document96 pagesInternational JVs Feb 2010International Tax Magazine; David Greenberg PhD, MSA, EA, CPA; Tax Group International; 646-705-2910No ratings yet

- E-Return Acknowledgment Receipt: Personal Information and Return Filing DetailsDocument1 pageE-Return Acknowledgment Receipt: Personal Information and Return Filing DetailsSTAR BOYNo ratings yet

- To Be Discussed Final ExaminationDocument11 pagesTo Be Discussed Final ExaminationRenz CastroNo ratings yet

- TAX Invoice: Meqte Sales & Services PVT LTDDocument2 pagesTAX Invoice: Meqte Sales & Services PVT LTDVicky KumarNo ratings yet

- CIR v. Estate of Benigno Toda, 438 SCRA 290, 2004Document8 pagesCIR v. Estate of Benigno Toda, 438 SCRA 290, 2004JMae MagatNo ratings yet

- Liddell & Co DigestDocument2 pagesLiddell & Co DigestJoey PastranaNo ratings yet

- US Internal Revenue Service: I1040aDocument80 pagesUS Internal Revenue Service: I1040aIRS100% (1)

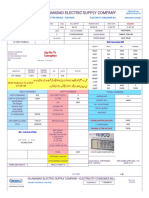

- Iesco Online BillDocument1 pageIesco Online BillURDU BHAINo ratings yet

- A Systematic Literature Review On Tax Amnesty in 9 Asian - Countries (#354229) - 365354Document6 pagesA Systematic Literature Review On Tax Amnesty in 9 Asian - Countries (#354229) - 365354tiger4i17No ratings yet

- Polyplex AR 2021Document237 pagesPolyplex AR 2021Abhishek JaiswalNo ratings yet

- Business and Transfer Taxation - T or FDocument3 pagesBusiness and Transfer Taxation - T or FEuli Mae SomeraNo ratings yet

- Trial Balance Setelah PenyesuaianDocument1 pageTrial Balance Setelah Penyesuaianimam hanapiNo ratings yet

- Accounting 11 Activity 1Document1 pageAccounting 11 Activity 1Ma Trixia Alexandra CuevasNo ratings yet

- 002WZ3744Document3 pages002WZ3744DrVarsha Priya SinghNo ratings yet

- CashDocument3 pagesCashDahirNo ratings yet

- Chapter 06 Sample Test SDocument4 pagesChapter 06 Sample Test SRohan GopalNo ratings yet