Download as pdf or txt

You might also like

- SAP Enterprise Structure Concept and Configuration Guide: A Case StudyFrom EverandSAP Enterprise Structure Concept and Configuration Guide: A Case StudyRating: 5 out of 5 stars5/5 (3)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Understanding Financial Statements (Review and Analysis of Straub's Book)From EverandUnderstanding Financial Statements (Review and Analysis of Straub's Book)Rating: 5 out of 5 stars5/5 (5)

- SAP FICO MaterialDocument24 pagesSAP FICO MaterialNeelam Singh100% (1)

- Sap Fico Questions&AnswersDocument46 pagesSap Fico Questions&AnswersNeeraj Melayil100% (2)

- Sap Fi Co ModuleDocument384 pagesSap Fi Co ModuleAnupam BaliNo ratings yet

- Kiran Kumar: Sap Fico Interview Questions & AnswersDocument46 pagesKiran Kumar: Sap Fico Interview Questions & AnswerspavankalluriNo ratings yet

- Sap Fico Basic SetttingsDocument3 pagesSap Fico Basic SetttingssrinivasNo ratings yet

- Enterprise Structure:: Basic SettingsDocument62 pagesEnterprise Structure:: Basic SettingspawanhegdeNo ratings yet

- Enterprise Structure SAPDocument31 pagesEnterprise Structure SAPLafidan Rizata FebiolaNo ratings yet

- Financials ERP For BeginnersDocument120 pagesFinancials ERP For BeginnersEryx LetzNo ratings yet

- Sap DocmentDocument8 pagesSap DocmentVineela DevarakondaNo ratings yet

- 1.what Is SAP Finance? What Business Requirement Is Fulfilled in This Module?Document163 pages1.what Is SAP Finance? What Business Requirement Is Fulfilled in This Module?sudhakarNo ratings yet

- SAP MM - Organizational Structure Interview Questions and AnswersDocument4 pagesSAP MM - Organizational Structure Interview Questions and AnswersSambit MohantyNo ratings yet

- BasicDocument3 pagesBasicvenkatreddyNo ratings yet

- SAP FICO Interview QuestionsDocument4 pagesSAP FICO Interview Questionsnagasuresh nNo ratings yet

- Sap Fico BeginnersDocument710 pagesSap Fico Beginnersprincereddy100% (3)

- Sap Intro Functional Fi 14nov2007Document4 pagesSap Intro Functional Fi 14nov2007Jose Luis GonzalezNo ratings yet

- Fi Asap Q&aDocument22 pagesFi Asap Q&ahwidjaja88No ratings yet

- Notes 1Document12 pagesNotes 1Aniruddha ChakrabortyNo ratings yet

- Company Code: Accounting Component. The Business Transactions Relevant For Financial Accounting Are EnteredDocument2 pagesCompany Code: Accounting Component. The Business Transactions Relevant For Financial Accounting Are EnteredTeja SaiNo ratings yet

- Tugas RangkumanDocument18 pagesTugas RangkumaniqbalNo ratings yet

- Fi Creation StepsDocument42 pagesFi Creation StepsGowtham Naidu BNo ratings yet

- BP in GLDocument35 pagesBP in GLMohammed Al SaaidiNo ratings yet

- Qustion AnsDocument23 pagesQustion Ansjay koshtiNo ratings yet

- SFBDocument712 pagesSFBVinay PrasanthNo ratings yet

- Chapter Five: Setting Up General Ledger: Session 5 2/14/16Document10 pagesChapter Five: Setting Up General Ledger: Session 5 2/14/16barber bobNo ratings yet

- Top 25 Fi: 1. What Are The Options in SAP For Fiscal Years?Document5 pagesTop 25 Fi: 1. What Are The Options in SAP For Fiscal Years?Manjunathreddy SeshadriNo ratings yet

- Presales FICO QuestDocument27 pagesPresales FICO QuestKrishnaNo ratings yet

- Project Class Day 3Document7 pagesProject Class Day 3y421997No ratings yet

- FI and New GL OverviewDocument39 pagesFI and New GL OverviewUday Bhaskar GurralaNo ratings yet

- FICA1Document8 pagesFICA1alexisNo ratings yet

- SAP FICO Interview Question and Answers Series OneDocument67 pagesSAP FICO Interview Question and Answers Series OneSAP allmoduleNo ratings yet

- Accounts Imp Interview QustionsDocument14 pagesAccounts Imp Interview QustionsNandan DNo ratings yet

- BOK Parallel AccountingDocument8 pagesBOK Parallel AccountingPiyush DubeNo ratings yet

- Sapficointerviewquestions 121004024409 Phpapp01Document38 pagesSapficointerviewquestions 121004024409 Phpapp01Manas Kumar Sahoo100% (1)

- SEM BCS Key Design Considerations For Integration With SAP ECCDocument14 pagesSEM BCS Key Design Considerations For Integration With SAP ECCGanesh ShankarNo ratings yet

- SAP - ERP Financials and Controlling - Financial Accounting OverviewDocument25 pagesSAP - ERP Financials and Controlling - Financial Accounting Overviewwillie.adeleNo ratings yet

- Sap Fico Interview Questions & Answers: How To Clear Each and Every Interview You Give-100 % Success AssuredDocument71 pagesSap Fico Interview Questions & Answers: How To Clear Each and Every Interview You Give-100 % Success Assuredkrishna1427100% (1)

- Organization Structure in SAP Client SCC4: (Rcomp)Document18 pagesOrganization Structure in SAP Client SCC4: (Rcomp)Sambit MohantyNo ratings yet

- Business Area: Tcode: Ox03: Whether A Single Business Area Can Be Used by Two or More Company Codes?Document41 pagesBusiness Area: Tcode: Ox03: Whether A Single Business Area Can Be Used by Two or More Company Codes?fharooksNo ratings yet

- SAP FI Related DefinitionsDocument2 pagesSAP FI Related Definitionskirangitam7454No ratings yet

- Sap Fico BeginnersDocument384 pagesSap Fico BeginnersIrfan KNo ratings yet

- ErpDocument2 pagesErpyoungpaulus0No ratings yet

- Sap FicoDocument3 pagesSap FicoinsaneNo ratings yet

- GL TheoryDocument6 pagesGL TheoryKolusu GopirajuNo ratings yet

- Sap Fico Interview QuestionsDocument28 pagesSap Fico Interview QuestionsNeelesh KumarNo ratings yet

- Sap Fico Interview Questions & Answers: How To Clear Each and Every Interview You Give-100 % Success AssuredDocument72 pagesSap Fico Interview Questions & Answers: How To Clear Each and Every Interview You Give-100 % Success AssuredAkshay GodhamgaonkarNo ratings yet

- End User DocumentDocument5 pagesEnd User DocumentShivangii SharmaNo ratings yet

- Tally Interview Questions: 1. Define Tally. Where Does It Find Its Application?Document5 pagesTally Interview Questions: 1. Define Tally. Where Does It Find Its Application?prince2venkatNo ratings yet

- Student Hand Book: On Tally - ERPDocument33 pagesStudent Hand Book: On Tally - ERPRia MakkarNo ratings yet

- Sap Fico Enterprice StructureDocument11 pagesSap Fico Enterprice StructureRajashekar ReddyNo ratings yet

- What Is The Relation Between A Controlling Areas and A Company CodeDocument27 pagesWhat Is The Relation Between A Controlling Areas and A Company CodeManjunathreddy SeshadriNo ratings yet

- Basic Configuration Settings For Implementing Asset Accounting in SAP 6.0Document5 pagesBasic Configuration Settings For Implementing Asset Accounting in SAP 6.0Jyotiraditya BanerjeeNo ratings yet

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- Financing Your New VentureDocument33 pagesFinancing Your New Venturetytry56565No ratings yet

- Outlook Money PDFDocument68 pagesOutlook Money PDFKumar Pranay100% (1)

- (20240101) BlackRock's 2024 Private Markets OutlookDocument27 pages(20240101) BlackRock's 2024 Private Markets Outlook施詠柔No ratings yet

- Brief Principles of Macroeconomics 7th Edition Gregory Mankiw Test Bank DownloadDocument263 pagesBrief Principles of Macroeconomics 7th Edition Gregory Mankiw Test Bank DownloadAnn Siewers100% (17)

- Project On Derivative Market by Sanjay Gupta - IssuuDocument16 pagesProject On Derivative Market by Sanjay Gupta - IssuuAshishNo ratings yet

- Chapter 1 Accounting in ActionDocument42 pagesChapter 1 Accounting in ActionShihab AhmedNo ratings yet

- A Study On Financial Analysis of Punjab National BankDocument11 pagesA Study On Financial Analysis of Punjab National BankJitesh LadgeNo ratings yet

- Synopsis On: Corporate Debt Ratings: An Analysis of Methodologies and Practices by Select Credit Rating Agencies in IndiaDocument39 pagesSynopsis On: Corporate Debt Ratings: An Analysis of Methodologies and Practices by Select Credit Rating Agencies in IndiaNihit SrivastavaNo ratings yet

- AFAR 8918. Business Combination-Date of AcquisitionDocument4 pagesAFAR 8918. Business Combination-Date of AcquisitionTineNo ratings yet

- Downloaded From Testpapers - Co.zaDocument16 pagesDownloaded From Testpapers - Co.zapaci chaviNo ratings yet

- Distributive Bargaining CalculationDocument2 pagesDistributive Bargaining CalculationNurul NajwaNo ratings yet

- Oscillator PDFDocument2 pagesOscillator PDFSandeep MishraNo ratings yet

- Final FSE ReportDocument113 pagesFinal FSE Reportgetachewasnake481No ratings yet

- Beta Saham 20210506 enDocument14 pagesBeta Saham 20210506 enRalian AlbarNo ratings yet

- Raising Capital (Ch15)Document22 pagesRaising Capital (Ch15)Spidy BondNo ratings yet

- Consolidated Statements of Financial Position Debts & CashDocument4 pagesConsolidated Statements of Financial Position Debts & CashMuhammad Desca Nur RabbaniNo ratings yet

- Capital Budgeting Cibg.Document36 pagesCapital Budgeting Cibg.Frederick Gbli100% (1)

- Best Buy Team PresentationDocument10 pagesBest Buy Team PresentationSandra Medina-CortesNo ratings yet

- ICT - Short Term Trading PlanDocument11 pagesICT - Short Term Trading PlanAzize MohammedNo ratings yet

- Complex Investment DecisionsDocument36 pagesComplex Investment DecisionsAmir Siddiqui100% (1)

- Finance MCQDocument27 pagesFinance MCQravi kangneNo ratings yet

- RoutledgeHandbooks 9780203713303 Chapter1Document5 pagesRoutledgeHandbooks 9780203713303 Chapter1samyghallabNo ratings yet

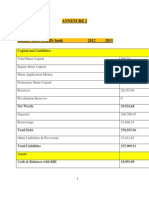

- Annexure 2Document13 pagesAnnexure 2Shalini SrivastavNo ratings yet

- P20ADocument604 pagesP20AAashish Garg100% (1)

- Open Statement Decjan-2023 2Document9 pagesOpen Statement Decjan-2023 2raheemtimo1No ratings yet

- Finec 2Document11 pagesFinec 2nurulnatasha sinclairaquariusNo ratings yet

- Entrep12 q2 m8 Computation of Gross Profits 2Document22 pagesEntrep12 q2 m8 Computation of Gross Profits 2Gerald PatolotNo ratings yet

- Brealey Fundamentals of Corporate Finance 10e Ch08 PPT 2022Document25 pagesBrealey Fundamentals of Corporate Finance 10e Ch08 PPT 2022farroohaahmedNo ratings yet

- Imt 59 Question 5 Assignmwnet SolDocument26 pagesImt 59 Question 5 Assignmwnet SolamitNo ratings yet

- New-Silibus Bwff2013 Mqa-StudentDocument8 pagesNew-Silibus Bwff2013 Mqa-StudentBlack Fish FishNo ratings yet