Exercises

Exercises

You might also like

- Tutorial Work With SolutionsDocument73 pagesTutorial Work With SolutionsAlison Mokla100% (1)

- The Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeFrom EverandThe Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeNo ratings yet

- Sun Brewing Case ExhibitsDocument26 pagesSun Brewing Case ExhibitsShshankNo ratings yet

- Basic Accounting Reviewer Step 1 To 3Document12 pagesBasic Accounting Reviewer Step 1 To 3Mary Gleyne100% (1)

- Problems in AccountingDocument4 pagesProblems in AccountingRaul Soriano CabantingNo ratings yet

- Bfjpia Cup 3 - Practical Accounting 2 Easy: Page 1 of 10Document10 pagesBfjpia Cup 3 - Practical Accounting 2 Easy: Page 1 of 10Arah OpalecNo ratings yet

- Quiz For Non-AccountantsDocument3 pagesQuiz For Non-AccountantsWycliffe Luther RosalesNo ratings yet

- UntitledDocument17 pagesUntitledJoshua Arjay V. ToveraNo ratings yet

- Name: Fernandez, Joriz O. Humss D Entrepreneurship - Quarter 2 - Module 8Document2 pagesName: Fernandez, Joriz O. Humss D Entrepreneurship - Quarter 2 - Module 8harley parsleyNo ratings yet

- Topic 10 - Practice ProblemsDocument2 pagesTopic 10 - Practice ProblemsAnna Mariyaahh DeblosanNo ratings yet

- Darantan, KC T. - FAR Module 6Document3 pagesDarantan, KC T. - FAR Module 6Li LiNo ratings yet

- Liquidation of CorporationDocument15 pagesLiquidation of CorporationMacie MenesesNo ratings yet

- Statement of AffairsDocument4 pagesStatement of AffairsCaliNo ratings yet

- Ex. 8.11 - B2 - A. Fuentes - Palacios - Lobangco - RonaCoDocument13 pagesEx. 8.11 - B2 - A. Fuentes - Palacios - Lobangco - RonaCoShwn Mchl SbynNo ratings yet

- Quiz 1 - Midterm ReviewerDocument4 pagesQuiz 1 - Midterm ReviewerJack HererNo ratings yet

- Doremi Partnership: Do, Capital (20%) Re, Capital (30%) Mi, Capital (50%)Document4 pagesDoremi Partnership: Do, Capital (20%) Re, Capital (30%) Mi, Capital (50%)Guiana WacasNo ratings yet

- Basic Accounting Final - QuestionDocument6 pagesBasic Accounting Final - QuestionEdaNo ratings yet

- Analysis of Business TransactionsDocument21 pagesAnalysis of Business TransactionsDan Gideon Cariaga100% (1)

- Accounting ConceptDocument1 pageAccounting ConceptNISHANTH P CHOYAL 2228512No ratings yet

- Paco Company: A. Accounting For Corporate LiquidationDocument3 pagesPaco Company: A. Accounting For Corporate LiquidationTine Griego100% (1)

- Chapter 1 Acctg Equation JournalizingDocument4 pagesChapter 1 Acctg Equation JournalizingNicole Marie Pontay BajadeNo ratings yet

- Business CombinationDocument1 pageBusiness CombinationNicki Salcedo0% (2)

- Module-Partnership-and-Corporation-Accounting - Lesson 1Document6 pagesModule-Partnership-and-Corporation-Accounting - Lesson 1Jay Lord GallardoNo ratings yet

- Las 6Document4 pagesLas 6Venus Abarico Banque-AbenionNo ratings yet

- BKP 9 Accounting EquationDocument16 pagesBKP 9 Accounting EquationPhilpNil8000No ratings yet

- Acc 1Document7 pagesAcc 1Taskeen AliNo ratings yet

- Tally Module 1 Assignment SolutionDocument6 pagesTally Module 1 Assignment Solutioncharu bishtNo ratings yet

- Chapter 4 - 5 ActivitiesDocument3 pagesChapter 4 - 5 ActivitiesJane Carla BorromeoNo ratings yet

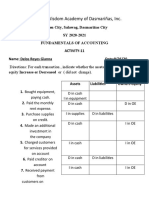

- Legacy of Wisdom Academy of Dasmariñas, IncDocument4 pagesLegacy of Wisdom Academy of Dasmariñas, InczavriaNo ratings yet

- Additional Questions On Financial Statements and Cash BookDocument5 pagesAdditional Questions On Financial Statements and Cash BookBoi NonoNo ratings yet

- (Fabm 2) - m1 - Lolo-GatesDocument6 pages(Fabm 2) - m1 - Lolo-GatesCriestefiel LoloNo ratings yet

- Corporate LiquidationDocument6 pagesCorporate LiquidationAngelieNo ratings yet

- AFST Practice Set 04 Corporate LiquidationDocument4 pagesAFST Practice Set 04 Corporate LiquidationAlain CopperNo ratings yet

- Acctg 1Document3 pagesAcctg 1HoneyzelOmandamPonceNo ratings yet

- Module 6 AccountingDocument2 pagesModule 6 AccountingJesther Nasa-anNo ratings yet

- Seatwork 2Document8 pagesSeatwork 2Nasiba M. AbdulcaderNo ratings yet

- Advact PrelimDocument10 pagesAdvact PrelimSano ManjiroNo ratings yet

- Accounting 1 QuizDocument2 pagesAccounting 1 QuizGringo KodetaNo ratings yet

- BFJPIA Cup Level 4 P2Document9 pagesBFJPIA Cup Level 4 P2Blessy Zedlav LacbainNo ratings yet

- Topic 6.Document5 pagesTopic 6.Ernie AbeNo ratings yet

- Unit 1 JournalizingDocument9 pagesUnit 1 JournalizingAnore, Anton NikolaiNo ratings yet

- Analysis of Business TransactionsDocument2 pagesAnalysis of Business Transactionskianna aquino100% (1)

- S1-Accounting: Soal 23Document12 pagesS1-Accounting: Soal 23Anggi Fauzia RamadhaniNo ratings yet

- Module 3 - Caragan, Adriane Ronn B. (CORRESPONDENCE)Document8 pagesModule 3 - Caragan, Adriane Ronn B. (CORRESPONDENCE)WonnNo ratings yet

- Prac 2Document10 pagesPrac 2Fery AnnNo ratings yet

- Unit IV Corporate Liquidation PDFDocument20 pagesUnit IV Corporate Liquidation PDFLeslie Mae Vargas ZafeNo ratings yet

- ACCO Module 2Document5 pagesACCO Module 2Lala BoraNo ratings yet

- Multiple Choices QuestionsDocument7 pagesMultiple Choices QuestionsrenoNo ratings yet

- Advacc1 Accounting For Special Transactions (Advanced Accounting 1)Document24 pagesAdvacc1 Accounting For Special Transactions (Advanced Accounting 1)Dzulija Talipan100% (1)

- Course Name 9Document6 pagesCourse Name 9Revise PastralisNo ratings yet

- SUMMER REVIEW SESSION NO.5 QUESTIONNAIRES (F1 and F2 ONLY)Document6 pagesSUMMER REVIEW SESSION NO.5 QUESTIONNAIRES (F1 and F2 ONLY)Aileen TorresNo ratings yet

- 2ND Term S3 Financial AccountDocument24 pages2ND Term S3 Financial Accountsaidu musaNo ratings yet

- Answer Key POD Cup Jr. Final RoundDocument6 pagesAnswer Key POD Cup Jr. Final RoundRitsNo ratings yet

- Mid Term Exam POA 2023 - Đề 2Document5 pagesMid Term Exam POA 2023 - Đề 2Anh Nguyễn MaiNo ratings yet

- Class Exercises - Accounting Equation 2 - AnswersDocument8 pagesClass Exercises - Accounting Equation 2 - AnswerseshakaurNo ratings yet

- CombinepdfDocument30 pagesCombinepdfDavid BermudezNo ratings yet

- JOint CorpDocument7 pagesJOint CorpNhel AlvaroNo ratings yet

- BKP 9 Accounting EquationDocument13 pagesBKP 9 Accounting EquationPhilpNil8000No ratings yet

- Getting Started in Real Estate Investment TrustsFrom EverandGetting Started in Real Estate Investment TrustsRating: 3 out of 5 stars3/5 (1)

- ComicDocument2 pagesComicJohn Daniel BerdosNo ratings yet

- Solving Problems Involving Kinds of Propotion StudentDocument18 pagesSolving Problems Involving Kinds of Propotion StudentJohn Daniel BerdosNo ratings yet

- SCRIPTTTTTTTTDocument2 pagesSCRIPTTTTTTTTJohn Daniel BerdosNo ratings yet

- POVERTYDocument5 pagesPOVERTYJohn Daniel BerdosNo ratings yet

- ETHICSDocument3 pagesETHICSJohn Daniel BerdosNo ratings yet

- ISA 706 (Revised)Document19 pagesISA 706 (Revised)karnanNo ratings yet

- Week 3-Fringe Benefit TaxDocument51 pagesWeek 3-Fringe Benefit TaxMARCIAL, Althea Kate A.No ratings yet

- Iowa Federation of Animal Owners - 9724 - DR2 - SummaryDocument1 pageIowa Federation of Animal Owners - 9724 - DR2 - SummaryZach EdwardsNo ratings yet

- Money and Interest Rates: © 2013 Pearson Education, Inc. All Rights Reserved. 3-1Document55 pagesMoney and Interest Rates: © 2013 Pearson Education, Inc. All Rights Reserved. 3-1Lân ÀaNo ratings yet

- Match Each Annual Report Section With Its Description Annual ReportDocument1 pageMatch Each Annual Report Section With Its Description Annual ReportLet's Talk With HassanNo ratings yet

- Full Download Test Bank For Strategic Management 10th Edition by Hitt PDF Full ChapterDocument36 pagesFull Download Test Bank For Strategic Management 10th Edition by Hitt PDF Full Chapterempyesis.princockijlde4100% (22)

- Case 1: Stocks Knowing The Philippine Stock Exchange 1. What Is The Philippine Stock Exchange, Inc.?Document27 pagesCase 1: Stocks Knowing The Philippine Stock Exchange 1. What Is The Philippine Stock Exchange, Inc.?AyuguNo ratings yet

- LOF Lloyds FinalDocument284 pagesLOF Lloyds FinalDhameemAnsariNo ratings yet

- What Is Funds Management?Document2 pagesWhat Is Funds Management?KidMonkey2299No ratings yet

- 2010.08.01 TRENDadvisor Basket of StocksDocument16 pages2010.08.01 TRENDadvisor Basket of Stocksclis338460No ratings yet

- 0000 TEMPLATE Written Consent FormDocument2 pages0000 TEMPLATE Written Consent FormRose Cano-AmbuloNo ratings yet

- 04192010assign RedactedDocument1 page04192010assign RedactedWalter HackettNo ratings yet

- Executive Summary: Analysis: - Banking"Document57 pagesExecutive Summary: Analysis: - Banking"vivekbalvirNo ratings yet

- Module 3 - PAS10 and PAS24Document6 pagesModule 3 - PAS10 and PAS24Roen Jasper EviaNo ratings yet

- Comprehensive Car Insurance PolicyDocument1 pageComprehensive Car Insurance PolicyMehul KumarNo ratings yet

- Financial Statement As of February 2018Document12 pagesFinancial Statement As of February 2018Jaijai Travel and ToursNo ratings yet

- Preliminary Exam FIN 2 - SampleDocument3 pagesPreliminary Exam FIN 2 - SampleEumell Alexis PaleNo ratings yet

- Legal Forms Letter of Demand For Full PaymentDocument2 pagesLegal Forms Letter of Demand For Full PaymentIris Pauline TaganasNo ratings yet

- VOPAK Jaarverslag2010 PDFDocument180 pagesVOPAK Jaarverslag2010 PDFJasper Laarmans Teixeira de MattosNo ratings yet

- Taxn 1000 First Term Exam Sy 2021-2022 QuestionsDocument8 pagesTaxn 1000 First Term Exam Sy 2021-2022 QuestionsLAIJANIE CLAIRE ALVAREZNo ratings yet

- Aoc 4Document20 pagesAoc 4Sameer DhumaleNo ratings yet

- Symbol Last Trend Quote Trend Net CHNG Bid AskDocument17 pagesSymbol Last Trend Quote Trend Net CHNG Bid AskMax LiNo ratings yet

- Governmental Operating Statement Accounts Budgetary AccountingDocument38 pagesGovernmental Operating Statement Accounts Budgetary AccountingshimelisNo ratings yet

- Brockhaus-Long ApproximationDocument8 pagesBrockhaus-Long Approximationmainak.chatterjee03No ratings yet

- Unit I EntrepreneurshipDocument67 pagesUnit I EntrepreneurshipRica ArtajoNo ratings yet

- Reserve Bank of IndiaDocument10 pagesReserve Bank of IndiasardeepanwitaNo ratings yet

- Refund Request FormDocument1 pageRefund Request FormIris100% (1)

- Tugas Kelompok Manajemen Keuangan Semester 3Document5 pagesTugas Kelompok Manajemen Keuangan Semester 3IdaNo ratings yet

- Accounts FinalDocument5 pagesAccounts FinalGujju GamerNo ratings yet

Download as docx, pdf, or txt

You might also like

- Tutorial Work With SolutionsDocument73 pagesTutorial Work With SolutionsAlison Mokla100% (1)

- The Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeFrom EverandThe Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeNo ratings yet

- Sun Brewing Case ExhibitsDocument26 pagesSun Brewing Case ExhibitsShshankNo ratings yet

- Basic Accounting Reviewer Step 1 To 3Document12 pagesBasic Accounting Reviewer Step 1 To 3Mary Gleyne100% (1)

- Problems in AccountingDocument4 pagesProblems in AccountingRaul Soriano CabantingNo ratings yet

- Bfjpia Cup 3 - Practical Accounting 2 Easy: Page 1 of 10Document10 pagesBfjpia Cup 3 - Practical Accounting 2 Easy: Page 1 of 10Arah OpalecNo ratings yet

- Quiz For Non-AccountantsDocument3 pagesQuiz For Non-AccountantsWycliffe Luther RosalesNo ratings yet

- UntitledDocument17 pagesUntitledJoshua Arjay V. ToveraNo ratings yet

- Name: Fernandez, Joriz O. Humss D Entrepreneurship - Quarter 2 - Module 8Document2 pagesName: Fernandez, Joriz O. Humss D Entrepreneurship - Quarter 2 - Module 8harley parsleyNo ratings yet

- Topic 10 - Practice ProblemsDocument2 pagesTopic 10 - Practice ProblemsAnna Mariyaahh DeblosanNo ratings yet

- Darantan, KC T. - FAR Module 6Document3 pagesDarantan, KC T. - FAR Module 6Li LiNo ratings yet

- Liquidation of CorporationDocument15 pagesLiquidation of CorporationMacie MenesesNo ratings yet

- Statement of AffairsDocument4 pagesStatement of AffairsCaliNo ratings yet

- Ex. 8.11 - B2 - A. Fuentes - Palacios - Lobangco - RonaCoDocument13 pagesEx. 8.11 - B2 - A. Fuentes - Palacios - Lobangco - RonaCoShwn Mchl SbynNo ratings yet

- Quiz 1 - Midterm ReviewerDocument4 pagesQuiz 1 - Midterm ReviewerJack HererNo ratings yet

- Doremi Partnership: Do, Capital (20%) Re, Capital (30%) Mi, Capital (50%)Document4 pagesDoremi Partnership: Do, Capital (20%) Re, Capital (30%) Mi, Capital (50%)Guiana WacasNo ratings yet

- Basic Accounting Final - QuestionDocument6 pagesBasic Accounting Final - QuestionEdaNo ratings yet

- Analysis of Business TransactionsDocument21 pagesAnalysis of Business TransactionsDan Gideon Cariaga100% (1)

- Accounting ConceptDocument1 pageAccounting ConceptNISHANTH P CHOYAL 2228512No ratings yet

- Paco Company: A. Accounting For Corporate LiquidationDocument3 pagesPaco Company: A. Accounting For Corporate LiquidationTine Griego100% (1)

- Chapter 1 Acctg Equation JournalizingDocument4 pagesChapter 1 Acctg Equation JournalizingNicole Marie Pontay BajadeNo ratings yet

- Business CombinationDocument1 pageBusiness CombinationNicki Salcedo0% (2)

- Module-Partnership-and-Corporation-Accounting - Lesson 1Document6 pagesModule-Partnership-and-Corporation-Accounting - Lesson 1Jay Lord GallardoNo ratings yet

- Las 6Document4 pagesLas 6Venus Abarico Banque-AbenionNo ratings yet

- BKP 9 Accounting EquationDocument16 pagesBKP 9 Accounting EquationPhilpNil8000No ratings yet

- Acc 1Document7 pagesAcc 1Taskeen AliNo ratings yet

- Tally Module 1 Assignment SolutionDocument6 pagesTally Module 1 Assignment Solutioncharu bishtNo ratings yet

- Chapter 4 - 5 ActivitiesDocument3 pagesChapter 4 - 5 ActivitiesJane Carla BorromeoNo ratings yet

- Legacy of Wisdom Academy of Dasmariñas, IncDocument4 pagesLegacy of Wisdom Academy of Dasmariñas, InczavriaNo ratings yet

- Additional Questions On Financial Statements and Cash BookDocument5 pagesAdditional Questions On Financial Statements and Cash BookBoi NonoNo ratings yet

- (Fabm 2) - m1 - Lolo-GatesDocument6 pages(Fabm 2) - m1 - Lolo-GatesCriestefiel LoloNo ratings yet

- Corporate LiquidationDocument6 pagesCorporate LiquidationAngelieNo ratings yet

- AFST Practice Set 04 Corporate LiquidationDocument4 pagesAFST Practice Set 04 Corporate LiquidationAlain CopperNo ratings yet

- Acctg 1Document3 pagesAcctg 1HoneyzelOmandamPonceNo ratings yet

- Module 6 AccountingDocument2 pagesModule 6 AccountingJesther Nasa-anNo ratings yet

- Seatwork 2Document8 pagesSeatwork 2Nasiba M. AbdulcaderNo ratings yet

- Advact PrelimDocument10 pagesAdvact PrelimSano ManjiroNo ratings yet

- Accounting 1 QuizDocument2 pagesAccounting 1 QuizGringo KodetaNo ratings yet

- BFJPIA Cup Level 4 P2Document9 pagesBFJPIA Cup Level 4 P2Blessy Zedlav LacbainNo ratings yet

- Topic 6.Document5 pagesTopic 6.Ernie AbeNo ratings yet

- Unit 1 JournalizingDocument9 pagesUnit 1 JournalizingAnore, Anton NikolaiNo ratings yet

- Analysis of Business TransactionsDocument2 pagesAnalysis of Business Transactionskianna aquino100% (1)

- S1-Accounting: Soal 23Document12 pagesS1-Accounting: Soal 23Anggi Fauzia RamadhaniNo ratings yet

- Module 3 - Caragan, Adriane Ronn B. (CORRESPONDENCE)Document8 pagesModule 3 - Caragan, Adriane Ronn B. (CORRESPONDENCE)WonnNo ratings yet

- Prac 2Document10 pagesPrac 2Fery AnnNo ratings yet

- Unit IV Corporate Liquidation PDFDocument20 pagesUnit IV Corporate Liquidation PDFLeslie Mae Vargas ZafeNo ratings yet

- ACCO Module 2Document5 pagesACCO Module 2Lala BoraNo ratings yet

- Multiple Choices QuestionsDocument7 pagesMultiple Choices QuestionsrenoNo ratings yet

- Advacc1 Accounting For Special Transactions (Advanced Accounting 1)Document24 pagesAdvacc1 Accounting For Special Transactions (Advanced Accounting 1)Dzulija Talipan100% (1)

- Course Name 9Document6 pagesCourse Name 9Revise PastralisNo ratings yet

- SUMMER REVIEW SESSION NO.5 QUESTIONNAIRES (F1 and F2 ONLY)Document6 pagesSUMMER REVIEW SESSION NO.5 QUESTIONNAIRES (F1 and F2 ONLY)Aileen TorresNo ratings yet

- 2ND Term S3 Financial AccountDocument24 pages2ND Term S3 Financial Accountsaidu musaNo ratings yet

- Answer Key POD Cup Jr. Final RoundDocument6 pagesAnswer Key POD Cup Jr. Final RoundRitsNo ratings yet

- Mid Term Exam POA 2023 - Đề 2Document5 pagesMid Term Exam POA 2023 - Đề 2Anh Nguyễn MaiNo ratings yet

- Class Exercises - Accounting Equation 2 - AnswersDocument8 pagesClass Exercises - Accounting Equation 2 - AnswerseshakaurNo ratings yet

- CombinepdfDocument30 pagesCombinepdfDavid BermudezNo ratings yet

- JOint CorpDocument7 pagesJOint CorpNhel AlvaroNo ratings yet

- BKP 9 Accounting EquationDocument13 pagesBKP 9 Accounting EquationPhilpNil8000No ratings yet

- Getting Started in Real Estate Investment TrustsFrom EverandGetting Started in Real Estate Investment TrustsRating: 3 out of 5 stars3/5 (1)

- ComicDocument2 pagesComicJohn Daniel BerdosNo ratings yet

- Solving Problems Involving Kinds of Propotion StudentDocument18 pagesSolving Problems Involving Kinds of Propotion StudentJohn Daniel BerdosNo ratings yet

- SCRIPTTTTTTTTDocument2 pagesSCRIPTTTTTTTTJohn Daniel BerdosNo ratings yet

- POVERTYDocument5 pagesPOVERTYJohn Daniel BerdosNo ratings yet

- ETHICSDocument3 pagesETHICSJohn Daniel BerdosNo ratings yet

- ISA 706 (Revised)Document19 pagesISA 706 (Revised)karnanNo ratings yet

- Week 3-Fringe Benefit TaxDocument51 pagesWeek 3-Fringe Benefit TaxMARCIAL, Althea Kate A.No ratings yet

- Iowa Federation of Animal Owners - 9724 - DR2 - SummaryDocument1 pageIowa Federation of Animal Owners - 9724 - DR2 - SummaryZach EdwardsNo ratings yet

- Money and Interest Rates: © 2013 Pearson Education, Inc. All Rights Reserved. 3-1Document55 pagesMoney and Interest Rates: © 2013 Pearson Education, Inc. All Rights Reserved. 3-1Lân ÀaNo ratings yet

- Match Each Annual Report Section With Its Description Annual ReportDocument1 pageMatch Each Annual Report Section With Its Description Annual ReportLet's Talk With HassanNo ratings yet

- Full Download Test Bank For Strategic Management 10th Edition by Hitt PDF Full ChapterDocument36 pagesFull Download Test Bank For Strategic Management 10th Edition by Hitt PDF Full Chapterempyesis.princockijlde4100% (22)

- Case 1: Stocks Knowing The Philippine Stock Exchange 1. What Is The Philippine Stock Exchange, Inc.?Document27 pagesCase 1: Stocks Knowing The Philippine Stock Exchange 1. What Is The Philippine Stock Exchange, Inc.?AyuguNo ratings yet

- LOF Lloyds FinalDocument284 pagesLOF Lloyds FinalDhameemAnsariNo ratings yet

- What Is Funds Management?Document2 pagesWhat Is Funds Management?KidMonkey2299No ratings yet

- 2010.08.01 TRENDadvisor Basket of StocksDocument16 pages2010.08.01 TRENDadvisor Basket of Stocksclis338460No ratings yet

- 0000 TEMPLATE Written Consent FormDocument2 pages0000 TEMPLATE Written Consent FormRose Cano-AmbuloNo ratings yet

- 04192010assign RedactedDocument1 page04192010assign RedactedWalter HackettNo ratings yet

- Executive Summary: Analysis: - Banking"Document57 pagesExecutive Summary: Analysis: - Banking"vivekbalvirNo ratings yet

- Module 3 - PAS10 and PAS24Document6 pagesModule 3 - PAS10 and PAS24Roen Jasper EviaNo ratings yet

- Comprehensive Car Insurance PolicyDocument1 pageComprehensive Car Insurance PolicyMehul KumarNo ratings yet

- Financial Statement As of February 2018Document12 pagesFinancial Statement As of February 2018Jaijai Travel and ToursNo ratings yet

- Preliminary Exam FIN 2 - SampleDocument3 pagesPreliminary Exam FIN 2 - SampleEumell Alexis PaleNo ratings yet

- Legal Forms Letter of Demand For Full PaymentDocument2 pagesLegal Forms Letter of Demand For Full PaymentIris Pauline TaganasNo ratings yet

- VOPAK Jaarverslag2010 PDFDocument180 pagesVOPAK Jaarverslag2010 PDFJasper Laarmans Teixeira de MattosNo ratings yet

- Taxn 1000 First Term Exam Sy 2021-2022 QuestionsDocument8 pagesTaxn 1000 First Term Exam Sy 2021-2022 QuestionsLAIJANIE CLAIRE ALVAREZNo ratings yet

- Aoc 4Document20 pagesAoc 4Sameer DhumaleNo ratings yet

- Symbol Last Trend Quote Trend Net CHNG Bid AskDocument17 pagesSymbol Last Trend Quote Trend Net CHNG Bid AskMax LiNo ratings yet

- Governmental Operating Statement Accounts Budgetary AccountingDocument38 pagesGovernmental Operating Statement Accounts Budgetary AccountingshimelisNo ratings yet

- Brockhaus-Long ApproximationDocument8 pagesBrockhaus-Long Approximationmainak.chatterjee03No ratings yet

- Unit I EntrepreneurshipDocument67 pagesUnit I EntrepreneurshipRica ArtajoNo ratings yet

- Reserve Bank of IndiaDocument10 pagesReserve Bank of IndiasardeepanwitaNo ratings yet

- Refund Request FormDocument1 pageRefund Request FormIris100% (1)

- Tugas Kelompok Manajemen Keuangan Semester 3Document5 pagesTugas Kelompok Manajemen Keuangan Semester 3IdaNo ratings yet

- Accounts FinalDocument5 pagesAccounts FinalGujju GamerNo ratings yet