Download as pdf or txt

You might also like

- Estmt - 2023 02 17Document6 pagesEstmt - 2023 02 17allan tu50% (2)

- Wilkerson Case SolutionDocument4 pagesWilkerson Case Solutionishan.gandhi1No ratings yet

- Case Study Polyproducts IncorporatedDocument7 pagesCase Study Polyproducts IncorporatedNayyerShah0% (8)

- Airbnb Etsy UberDocument15 pagesAirbnb Etsy UberParag PardhiNo ratings yet

- The Nespresso Case: Value Articulation - A Framework For The Strategic Management of Intellectual PropertyDocument6 pagesThe Nespresso Case: Value Articulation - A Framework For The Strategic Management of Intellectual PropertyAna SiqueiraNo ratings yet

- University of NottinghamDocument2 pagesUniversity of NottinghamdineshNo ratings yet

- CA Inter Paper 4Document1 pageCA Inter Paper 4ap.quatrroNo ratings yet

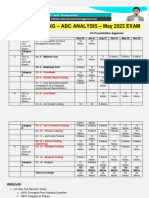

- CA Inter Top 5 Chapters Cover 80 Marks in May 2023 ABC Analysis PDFDocument4 pagesCA Inter Top 5 Chapters Cover 80 Marks in May 2023 ABC Analysis PDFSonu KalwarNo ratings yet

- Ca Inter Abc AnalysisDocument12 pagesCa Inter Abc AnalysisAbhu ArNo ratings yet

- CA Inter Top 5 Chapters To Cover 60 Marks in May 2022Document4 pagesCA Inter Top 5 Chapters To Cover 60 Marks in May 2022Dainika ShettyNo ratings yet

- Rambaan CostDocument433 pagesRambaan CostSanjana SharmaNo ratings yet

- Accounting CA Inter Paper AnalysisDocument10 pagesAccounting CA Inter Paper AnalysiszzxrssyNo ratings yet

- Introduction To SubjectDocument2 pagesIntroduction To SubjectsarmadaliaquariusNo ratings yet

- L1 PDFDocument16 pagesL1 PDFprogamerqwerty1122No ratings yet

- Assignment #1: Cumulative Earned ValueDocument5 pagesAssignment #1: Cumulative Earned ValueSheenan R. MedfordNo ratings yet

- Merged File Lectue 1 To 104Document202 pagesMerged File Lectue 1 To 104Mehwish NazNo ratings yet

- CA Final SCMPE Top 5 Chapters - Cover 75 Marks in May 2022Document3 pagesCA Final SCMPE Top 5 Chapters - Cover 75 Marks in May 2022Manogna PNo ratings yet

- SCM DJB-Birds Eye View July21Document2 pagesSCM DJB-Birds Eye View July21law classNo ratings yet

- CAF - Accounting - Past Exam Analysis - IL - 03012022 - PDFDocument9 pagesCAF - Accounting - Past Exam Analysis - IL - 03012022 - PDFRAHUL CHOUHANNo ratings yet

- Evaluation Matrix 250 BHS PDFDocument2 pagesEvaluation Matrix 250 BHS PDFKhurram ShahzadNo ratings yet

- EV Simulator R1 TrainerDocument16 pagesEV Simulator R1 TrainerSarinNo ratings yet

- P6A FM CA Inter NotesDocument275 pagesP6A FM CA Inter NotesnazcomputersitsNo ratings yet

- Strategy To Clear CA Inter May 2022Document41 pagesStrategy To Clear CA Inter May 2022Manas NaikNo ratings yet

- Strategy To Clear CA Inter May 2023 PDFDocument57 pagesStrategy To Clear CA Inter May 2023 PDFParag RaiyaniNo ratings yet

- SCMPE Brahamashtra For May 2022Document495 pagesSCMPE Brahamashtra For May 2022denakarNo ratings yet

- E&CDocument25 pagesE&CtejasNo ratings yet

- Unit I - Total Quality ManagementDocument17 pagesUnit I - Total Quality ManagementsudhaaNo ratings yet

- KIA Balance Score CardDocument49 pagesKIA Balance Score Cardthathathatha1973No ratings yet

- CAF - ACC - Past Exam AnalysisDocument6 pagesCAF - ACC - Past Exam AnalysisTheophras academyNo ratings yet

- UntitledDocument44 pagesUntitledRafay AnwarNo ratings yet

- Strategy To Clear CA Inter May'23 Final PDFDocument50 pagesStrategy To Clear CA Inter May'23 Final PDFXyzNo ratings yet

- Silo - Tips - Acca Paper f5 Performance Management PDFDocument57 pagesSilo - Tips - Acca Paper f5 Performance Management PDFSashauna GrahamNo ratings yet

- Ca InterDocument48 pagesCa InterVANSHNo ratings yet

- 9707 Business Studies: MARK SCHEME For The May/June 2011 Question Paper For The Guidance of TeachersDocument9 pages9707 Business Studies: MARK SCHEME For The May/June 2011 Question Paper For The Guidance of TeachersrumbidzayichatambararaNo ratings yet

- Introduction To: Cost of UalityDocument29 pagesIntroduction To: Cost of UalitySaad ParachaNo ratings yet

- VIDYA SAGAR Analysis-COSTDocument2 pagesVIDYA SAGAR Analysis-COSTap.quatrroNo ratings yet

- BLK320 October2022 TestDocument6 pagesBLK320 October2022 TestfezbutiNo ratings yet

- Welcome To All Chapters and Their Juries To Case Study Evaluation System For CCQC-2020Document11 pagesWelcome To All Chapters and Their Juries To Case Study Evaluation System For CCQC-2020Bibhudutta MishraNo ratings yet

- VIDYA SAGAR Analysis-COST For Nov 2022Document2 pagesVIDYA SAGAR Analysis-COST For Nov 2022MH DESKNo ratings yet

- BudgetingDocument62 pagesBudgetingkalamabikoko01No ratings yet

- Production Cost Analysis (Short Run)Document6 pagesProduction Cost Analysis (Short Run)Mystica BayaniNo ratings yet

- Lec-5 - COST ANALYSISDocument16 pagesLec-5 - COST ANALYSISvsvsasasNo ratings yet

- For Evaluation CriteriaDocument10 pagesFor Evaluation CriteriaMahesh GatadeNo ratings yet

- 348 - Master of Commerce Part 1 M.Com GernarelDocument36 pages348 - Master of Commerce Part 1 M.Com GernarelAmisha Singh VishenNo ratings yet

- Assignment 3Document15 pagesAssignment 3Muhammad Nur HelmyNo ratings yet

- Software Engineering 1 - Assignment 4: Q1 Q2 Q3 Q4 Q5 Q6 Q7 Q8 CostsDocument5 pagesSoftware Engineering 1 - Assignment 4: Q1 Q2 Q3 Q4 Q5 Q6 Q7 Q8 CostsElzbethyNo ratings yet

- CAInter - FM - Paper Analysis - IL..Document7 pagesCAInter - FM - Paper Analysis - IL..babuvenkatesh566No ratings yet

- AUTUMN 2019: Cost and Management Accounting CAF-8 Past Paper AnalysisDocument1 pageAUTUMN 2019: Cost and Management Accounting CAF-8 Past Paper Analysissidra awanNo ratings yet

- SCMPE ABC Analysis For May 2022 by CA Purushottam AggarwalDocument3 pagesSCMPE ABC Analysis For May 2022 by CA Purushottam AggarwalAneek JainNo ratings yet

- 04 Theory of Production and Cost FinalDocument21 pages04 Theory of Production and Cost FinalNeushinth HettiarachchiNo ratings yet

- ScyallabuseDocument127 pagesScyallabuseAanshu SinghNo ratings yet

- Past TrendDocument2 pagesPast TrendSurendra RangwaniNo ratings yet

- Inventory Management Organization: RIL (VMD) : Submitted By: Hemang Prashnani Roll No.45Document30 pagesInventory Management Organization: RIL (VMD) : Submitted By: Hemang Prashnani Roll No.45hemangjp868629No ratings yet

- Economic Principles - Tutorial 4 Semester 1 AnswersDocument19 pagesEconomic Principles - Tutorial 4 Semester 1 Answersmad EYESNo ratings yet

- F5 Mapit Workbook Questions PDFDocument88 pagesF5 Mapit Workbook Questions PDFalvin1deosaranNo ratings yet

- Realisasi KPIDocument3 pagesRealisasi KPIryen putraNo ratings yet

- 2.2016 Syllabus Paper-15-Oct-2020 Strategic Cost Management - Decision Making Study NotesDocument392 pages2.2016 Syllabus Paper-15-Oct-2020 Strategic Cost Management - Decision Making Study NotesRadhakrishnaraja Ramesh100% (1)

- Correction Handbook ABS For OPM ProjectDocument36 pagesCorrection Handbook ABS For OPM ProjectDrishti KudosNo ratings yet

- 19 06 27 Facilities KpisDocument18 pages19 06 27 Facilities KpisPhu, Le HuuNo ratings yet

- ActivityDocument8 pagesActivityKim James AguinaldoNo ratings yet

- Tracking KPI HO Ytd Mar 2021 - Infra Workshop Rev 2Document475 pagesTracking KPI HO Ytd Mar 2021 - Infra Workshop Rev 2daniel siahaanNo ratings yet

- Kromatic Template - Financial Modeling Spreadsheet - SHAREDDocument61 pagesKromatic Template - Financial Modeling Spreadsheet - SHAREDmicheleNo ratings yet

- Falcon FX Journal & Performance Analyser (V2)Document43 pagesFalcon FX Journal & Performance Analyser (V2)Villaca KeneteNo ratings yet

- Marketing & Retail Analytics - Report - Part ADocument18 pagesMarketing & Retail Analytics - Report - Part AAshish Agrawal100% (2)

- Benefits of Performance Measurement For Construction Project Organizations A Norwegian Case StudyDocument11 pagesBenefits of Performance Measurement For Construction Project Organizations A Norwegian Case StudykleinNo ratings yet

- Backlonk Sites ListsDocument7 pagesBacklonk Sites Listsmohit kumarNo ratings yet

- Cvs Health Financial AnalysisDocument12 pagesCvs Health Financial Analysisapi-643481686No ratings yet

- Wipo Pub 480 PDFDocument69 pagesWipo Pub 480 PDFFerry TimothyNo ratings yet

- The Large Marketplace Comparison GuideDocument43 pagesThe Large Marketplace Comparison GuidegencmetohuNo ratings yet

- Statement of Account - 22!28!39Document4 pagesStatement of Account - 22!28!39babybera770No ratings yet

- Mba580 Act2Document3 pagesMba580 Act2ashsimeon2020No ratings yet

- LSSBB - Sample Test Paper With AnswerDocument10 pagesLSSBB - Sample Test Paper With AnswerRanjith RanaNo ratings yet

- Resume LayoutDocument3 pagesResume LayoutJere Mae MarananNo ratings yet

- Maintenance of Medical EquipmentDocument33 pagesMaintenance of Medical EquipmentAbe CyberCrewPlusDotmy100% (1)

- WCC DefinitionDocument16 pagesWCC Definitionutsa sarkarNo ratings yet

- ApqpDocument1 pageApqpJatin PopliNo ratings yet

- Foundations in TurkeyDocument25 pagesFoundations in TurkeyOlcay Sanem SipahioğluNo ratings yet

- BRS Ca FoundationDocument9 pagesBRS Ca FoundationJunaid Iqbal MastoiNo ratings yet

- Chapter 4 - Organizational and Managerial Issues in Logistics PDFDocument65 pagesChapter 4 - Organizational and Managerial Issues in Logistics PDFTrey HoltonNo ratings yet

- Maths ContentDocument67 pagesMaths Contentrubinaqureshi1997No ratings yet

- Accounting Concepts and Qualitative CharacteristicsDocument2 pagesAccounting Concepts and Qualitative CharacteristicsElyse Burns-HillNo ratings yet

- Electiva 1 - Exam First Half - Units 1, 2, 3 Intelligent BusinessDocument4 pagesElectiva 1 - Exam First Half - Units 1, 2, 3 Intelligent BusinessYURLI ROANo ratings yet

- United States District Court Central District of California Case No: Cv08-01908 DSF (CTX)Document12 pagesUnited States District Court Central District of California Case No: Cv08-01908 DSF (CTX)twebster321100% (1)

- MANG6134 Risk Attitude and Utility Analysis STUDENT OHPS - 2021Document52 pagesMANG6134 Risk Attitude and Utility Analysis STUDENT OHPS - 2021dikshaNo ratings yet

- Complaint Against Macho Sports PDFDocument59 pagesComplaint Against Macho Sports PDFMartín Hidalgo BustamanteNo ratings yet

- VRTXDocument27 pagesVRTXJeypee De GeeNo ratings yet

- Project Report On Lakme PDFDocument66 pagesProject Report On Lakme PDFMithun Konjath30% (10)

- Mba Project On Recruitment Selection PDFDocument100 pagesMba Project On Recruitment Selection PDFsumanNo ratings yet