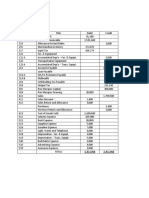

Neith: Trial Balance at 31 March 2020 Dr. CR

Neith: Trial Balance at 31 March 2020 Dr. CR

You might also like

- Assignment DFA6127Document3 pagesAssignment DFA6127parwez_0505No ratings yet

- Manufacturing Trial BalanceDocument3 pagesManufacturing Trial BalanceRechelleNo ratings yet

- 2nd Sem ProjectDocument49 pages2nd Sem ProjectNilesh Pawar100% (4)

- Solution To Q1 Summer 2022Document2 pagesSolution To Q1 Summer 2022dgornik021No ratings yet

- ADBM - FA - Questions CRADocument5 pagesADBM - FA - Questions CRAMahima SheromiNo ratings yet

- Batch 2-1Document2 pagesBatch 2-1kp7659165No ratings yet

- Solution Example 3Document2 pagesSolution Example 3ashish panwarNo ratings yet

- ACC2124 Mid-Term Test S2/17Document2 pagesACC2124 Mid-Term Test S2/17Niz IsmailNo ratings yet

- M.B.A (2021 Pattern)Document105 pagesM.B.A (2021 Pattern)Mayur HariyaniNo ratings yet

- Accounting Principles AbDocument36 pagesAccounting Principles Absamson mutukuNo ratings yet

- M.B.A. QPDocument184 pagesM.B.A. QPyogeshNo ratings yet

- Amanda D - Excel 2Document3 pagesAmanda D - Excel 2api-643373008No ratings yet

- DagohoyDocument6 pagesDagohoylinkin soyNo ratings yet

- Financial Accounting Assignment 1Document4 pagesFinancial Accounting Assignment 1jacklog600No ratings yet

- M.B.A (2019 Pattern)Document157 pagesM.B.A (2019 Pattern)girishpawarudgirkarNo ratings yet

- Financial Accounting hw1Document5 pagesFinancial Accounting hw1Jermaine M. SantoyoNo ratings yet

- Trial Balance and Final Accounts ProblemsDocument6 pagesTrial Balance and Final Accounts Problemsbhanu.chandu100% (1)

- Q No.1 Saleem Provided Following Trial Balance On December 31, 2015. Title of Accounts Debit CreditDocument4 pagesQ No.1 Saleem Provided Following Trial Balance On December 31, 2015. Title of Accounts Debit CreditNAFEES NASRUDDIN PATEL0% (1)

- Chapter 12 3 Bài DàiDocument6 pagesChapter 12 3 Bài DàiMai Lâm LêNo ratings yet

- 17 Financial Statements (With Adjustments)Document16 pages17 Financial Statements (With Adjustments)Dayaan ANo ratings yet

- Suggested Answer CAP I June 2011Document83 pagesSuggested Answer CAP I June 2011alchemistNo ratings yet

- Bba 122 Fai 11 AnswerDocument12 pagesBba 122 Fai 11 AnswerTomi Wayne Malenga100% (1)

- Financial Statement HandoutDocument5 pagesFinancial Statement Handoutmuzamilarshad31No ratings yet

- Assignment 2Document9 pagesAssignment 2Dư Trà MyNo ratings yet

- Accounting Principles Question Paper, Answers and Examiners CommentsDocument24 pagesAccounting Principles Question Paper, Answers and Examiners CommentsRyanNo ratings yet

- PT 2 and PT 3Document4 pagesPT 2 and PT 3Mariz Timario0% (2)

- 8447809Document11 pages8447809blackghostNo ratings yet

- MBA Accounting 4 Managers MSTDocument2 pagesMBA Accounting 4 Managers MSTrichadinrajNo ratings yet

- April 2022 (Fa4)Document7 pagesApril 2022 (Fa4)Amelia RahmawatiNo ratings yet

- Financial Statement2 (Work Sheet)Document6 pagesFinancial Statement2 (Work Sheet)Arham RajpootNo ratings yet

- Royal Escape LTD - Co Balance Sheet For The Month Ended, Dec.31,2020Document9 pagesRoyal Escape LTD - Co Balance Sheet For The Month Ended, Dec.31,2020KemerutNo ratings yet

- Accounts Revision QuestionDocument1 pageAccounts Revision QuestionZaara AshfaqNo ratings yet

- Trial Balance February 28, 20X1Document3 pagesTrial Balance February 28, 20X1Angelica MaeNo ratings yet

- Answer Illustration 6Document4 pagesAnswer Illustration 6apokelloNo ratings yet

- Preparation of FSDocument1 pagePreparation of FSmarkjuan301993No ratings yet

- acctng-1-Quiz-FS Begino, Vanessa Jamila DDocument4 pagesacctng-1-Quiz-FS Begino, Vanessa Jamila DVanessa JamilaNo ratings yet

- Joyk-Excel 2 3 1Document4 pagesJoyk-Excel 2 3 1api-664350584No ratings yet

- Quiz - 2 - BAAB1014 - (Sept2022) AnswerDocument8 pagesQuiz - 2 - BAAB1014 - (Sept2022) AnswerTheresa AnneNo ratings yet

- Debit Credit: EGG SHERAN Corp. (Home Office) Unadjusted Trial Balance December 31,20x1Document6 pagesDebit Credit: EGG SHERAN Corp. (Home Office) Unadjusted Trial Balance December 31,20x1Riza Mae AlceNo ratings yet

- 2018 - Final Exam123key To StudentsDocument3 pages2018 - Final Exam123key To StudentsMinh ThưNo ratings yet

- Cash Flow Tutorial QnsDocument13 pagesCash Flow Tutorial QnsCristian Renatus100% (1)

- Begino, Vanessa Jamila D. Class No. 4Document3 pagesBegino, Vanessa Jamila D. Class No. 4Vanessa JamilaNo ratings yet

- The Following Trial Balance Was Extracted From The Books of Craz LTD As at 31 Dec 2014Document5 pagesThe Following Trial Balance Was Extracted From The Books of Craz LTD As at 31 Dec 2014Pham TrangNo ratings yet

- Answer Sheet Mock Test 23Document5 pagesAnswer Sheet Mock Test 23Nam Nguyễn HoàngNo ratings yet

- Retained Earning Opening Balance - Net Income For The Year Ended 2017 2370 Dividend Paid (2,500)Document21 pagesRetained Earning Opening Balance - Net Income For The Year Ended 2017 2370 Dividend Paid (2,500)Umar Razi QasimNo ratings yet

- ACCT 4200 Project Solution - Final Posting 2022Document15 pagesACCT 4200 Project Solution - Final Posting 2022Jaspal SinghNo ratings yet

- AccountingDocument5 pagesAccountingIhsan UllahNo ratings yet

- INCOTAXDocument4 pagesINCOTAXnicole bancoroNo ratings yet

- A211 MC 2 - StudentDocument6 pagesA211 MC 2 - StudentWon HaNo ratings yet

- Practice Set 5 Financial Statements of Sole ProprietorshipsDocument3 pagesPractice Set 5 Financial Statements of Sole ProprietorshipsBritney PetersNo ratings yet

- Finance AccountsDocument2 pagesFinance AccountsBalumahendran. P Balumahendran. PNo ratings yet

- Statement of Comprehensive Income ProblemsDocument2 pagesStatement of Comprehensive Income ProblemsDarlyn Dalida San PedroNo ratings yet

- Alkaline Comp. Multi Step QuestionDocument2 pagesAlkaline Comp. Multi Step QuestionhotfujNo ratings yet

- Adjusting Journal EntriesDocument3 pagesAdjusting Journal EntriesAmirahNo ratings yet

- Assignment BAAD2033 Feb 2017Document5 pagesAssignment BAAD2033 Feb 2017RubanNo ratings yet

- Prepare Profit & Loss Account and Balance Sheet With The Help of Information Given in The Trial BalanceDocument4 pagesPrepare Profit & Loss Account and Balance Sheet With The Help of Information Given in The Trial BalanceEntertainment StatusNo ratings yet

- SAmpior Final 3 BSLM1ADocument5 pagesSAmpior Final 3 BSLM1ARedge Jefferson SampiorNo ratings yet

- Output No. 2 - PAS 1 Instruction: Write Your Answers On Long Bond PapersDocument2 pagesOutput No. 2 - PAS 1 Instruction: Write Your Answers On Long Bond Papersnmdl123No ratings yet

- Particulars Trial Balance Adjustments Adjusted Trial Balance DR CR DR CR DR CRDocument9 pagesParticulars Trial Balance Adjustments Adjusted Trial Balance DR CR DR CR DR CRasdfNo ratings yet

- Problem SolutionsDocument5 pagesProblem Solutionsmd nayonNo ratings yet

- 07 Activity 1 (24) .DocsDocument2 pages07 Activity 1 (24) .DocsNICOOR YOWWNo ratings yet

- Scope of Total Income and Residential StatusDocument3 pagesScope of Total Income and Residential StatusSandeep SinghNo ratings yet

- Income From House Property Solved Mcq's With PDF Download (Set-1)Document6 pagesIncome From House Property Solved Mcq's With PDF Download (Set-1)DevNo ratings yet

- Horizontal AnalysisDocument6 pagesHorizontal AnalysisjohhanaNo ratings yet

- Chapter-6 (Salary)Document53 pagesChapter-6 (Salary)BoRO TriAngLENo ratings yet

- Review of Financial Statement Preparation Analysis and Interpretation Pt.8Document6 pagesReview of Financial Statement Preparation Analysis and Interpretation Pt.8ADRIANO, Glecy C.No ratings yet

- Chapter 4 Economics of TourismDocument8 pagesChapter 4 Economics of TourismZeusNo ratings yet

- Act.4-8 Ae23Document6 pagesAct.4-8 Ae23Damian Sheila MaeNo ratings yet

- 2022 Accounting Grade 11 Project - ABDocument5 pages2022 Accounting Grade 11 Project - ABmishomabunda20No ratings yet

- Partner Ka Tax LagegaDocument16 pagesPartner Ka Tax LagegaVicky DNo ratings yet

- Brihanu - Research Paper-CommentsDocument20 pagesBrihanu - Research Paper-CommentsAddisu TeshomeNo ratings yet

- MTD YtdDocument350 pagesMTD YtdAmy Rose BotnandeNo ratings yet

- Alternative MeasuresDocument25 pagesAlternative MeasureslucaszayaNo ratings yet

- What Is AccountingDocument29 pagesWhat Is Accountingmule mulugetaNo ratings yet

- FN 200 - Financial Forecasting Seminar QuestionsDocument7 pagesFN 200 - Financial Forecasting Seminar QuestionskelvinizimburaNo ratings yet

- ch04 PDFDocument52 pagesch04 PDFerylpaez69% (13)

- T8 Homework Solutions-1Document15 pagesT8 Homework Solutions-1Anathi AnathiNo ratings yet

- Fatca - NSDL Non Ind. V. 21.3 (PG 1-4)Document4 pagesFatca - NSDL Non Ind. V. 21.3 (PG 1-4)digitaltarun99No ratings yet

- Social Accounting ModelsDocument19 pagesSocial Accounting ModelsSabrina Supti100% (1)

- How To Achieve Inclusive GrowthDocument901 pagesHow To Achieve Inclusive GrowthTAhmedNo ratings yet

- Human Capital in The Digital EconomyDocument6 pagesHuman Capital in The Digital EconomyalphathesisNo ratings yet

- PR - Asm 2 WawasanDocument4 pagesPR - Asm 2 WawasanCorrine TanNo ratings yet

- Diversion of IncomeDocument11 pagesDiversion of IncomeSrivathsan NambiraghavanNo ratings yet

- 3.2 Income Fro House Property AnswersDocument26 pages3.2 Income Fro House Property AnswersnairsulakshanaNo ratings yet

- Be Industrilization 2Document20 pagesBe Industrilization 2JAY SolankiNo ratings yet

- Jawaban Quiz 2Document2 pagesJawaban Quiz 2Muhammad IrvanNo ratings yet

- Chapters 3 and 4 Income TaxationDocument24 pagesChapters 3 and 4 Income TaxationJulie Ann BarcaNo ratings yet

- Income TaxDocument14 pagesIncome Taxanjuu2806No ratings yet

- Postemployment Benefits Wendy CompanyDocument6 pagesPostemployment Benefits Wendy CompanyArmelen DeloyNo ratings yet

Download as xlsx, pdf, or txt

You might also like

- Assignment DFA6127Document3 pagesAssignment DFA6127parwez_0505No ratings yet

- Manufacturing Trial BalanceDocument3 pagesManufacturing Trial BalanceRechelleNo ratings yet

- 2nd Sem ProjectDocument49 pages2nd Sem ProjectNilesh Pawar100% (4)

- Solution To Q1 Summer 2022Document2 pagesSolution To Q1 Summer 2022dgornik021No ratings yet

- ADBM - FA - Questions CRADocument5 pagesADBM - FA - Questions CRAMahima SheromiNo ratings yet

- Batch 2-1Document2 pagesBatch 2-1kp7659165No ratings yet

- Solution Example 3Document2 pagesSolution Example 3ashish panwarNo ratings yet

- ACC2124 Mid-Term Test S2/17Document2 pagesACC2124 Mid-Term Test S2/17Niz IsmailNo ratings yet

- M.B.A (2021 Pattern)Document105 pagesM.B.A (2021 Pattern)Mayur HariyaniNo ratings yet

- Accounting Principles AbDocument36 pagesAccounting Principles Absamson mutukuNo ratings yet

- M.B.A. QPDocument184 pagesM.B.A. QPyogeshNo ratings yet

- Amanda D - Excel 2Document3 pagesAmanda D - Excel 2api-643373008No ratings yet

- DagohoyDocument6 pagesDagohoylinkin soyNo ratings yet

- Financial Accounting Assignment 1Document4 pagesFinancial Accounting Assignment 1jacklog600No ratings yet

- M.B.A (2019 Pattern)Document157 pagesM.B.A (2019 Pattern)girishpawarudgirkarNo ratings yet

- Financial Accounting hw1Document5 pagesFinancial Accounting hw1Jermaine M. SantoyoNo ratings yet

- Trial Balance and Final Accounts ProblemsDocument6 pagesTrial Balance and Final Accounts Problemsbhanu.chandu100% (1)

- Q No.1 Saleem Provided Following Trial Balance On December 31, 2015. Title of Accounts Debit CreditDocument4 pagesQ No.1 Saleem Provided Following Trial Balance On December 31, 2015. Title of Accounts Debit CreditNAFEES NASRUDDIN PATEL0% (1)

- Chapter 12 3 Bài DàiDocument6 pagesChapter 12 3 Bài DàiMai Lâm LêNo ratings yet

- 17 Financial Statements (With Adjustments)Document16 pages17 Financial Statements (With Adjustments)Dayaan ANo ratings yet

- Suggested Answer CAP I June 2011Document83 pagesSuggested Answer CAP I June 2011alchemistNo ratings yet

- Bba 122 Fai 11 AnswerDocument12 pagesBba 122 Fai 11 AnswerTomi Wayne Malenga100% (1)

- Financial Statement HandoutDocument5 pagesFinancial Statement Handoutmuzamilarshad31No ratings yet

- Assignment 2Document9 pagesAssignment 2Dư Trà MyNo ratings yet

- Accounting Principles Question Paper, Answers and Examiners CommentsDocument24 pagesAccounting Principles Question Paper, Answers and Examiners CommentsRyanNo ratings yet

- PT 2 and PT 3Document4 pagesPT 2 and PT 3Mariz Timario0% (2)

- 8447809Document11 pages8447809blackghostNo ratings yet

- MBA Accounting 4 Managers MSTDocument2 pagesMBA Accounting 4 Managers MSTrichadinrajNo ratings yet

- April 2022 (Fa4)Document7 pagesApril 2022 (Fa4)Amelia RahmawatiNo ratings yet

- Financial Statement2 (Work Sheet)Document6 pagesFinancial Statement2 (Work Sheet)Arham RajpootNo ratings yet

- Royal Escape LTD - Co Balance Sheet For The Month Ended, Dec.31,2020Document9 pagesRoyal Escape LTD - Co Balance Sheet For The Month Ended, Dec.31,2020KemerutNo ratings yet

- Accounts Revision QuestionDocument1 pageAccounts Revision QuestionZaara AshfaqNo ratings yet

- Trial Balance February 28, 20X1Document3 pagesTrial Balance February 28, 20X1Angelica MaeNo ratings yet

- Answer Illustration 6Document4 pagesAnswer Illustration 6apokelloNo ratings yet

- Preparation of FSDocument1 pagePreparation of FSmarkjuan301993No ratings yet

- acctng-1-Quiz-FS Begino, Vanessa Jamila DDocument4 pagesacctng-1-Quiz-FS Begino, Vanessa Jamila DVanessa JamilaNo ratings yet

- Joyk-Excel 2 3 1Document4 pagesJoyk-Excel 2 3 1api-664350584No ratings yet

- Quiz - 2 - BAAB1014 - (Sept2022) AnswerDocument8 pagesQuiz - 2 - BAAB1014 - (Sept2022) AnswerTheresa AnneNo ratings yet

- Debit Credit: EGG SHERAN Corp. (Home Office) Unadjusted Trial Balance December 31,20x1Document6 pagesDebit Credit: EGG SHERAN Corp. (Home Office) Unadjusted Trial Balance December 31,20x1Riza Mae AlceNo ratings yet

- 2018 - Final Exam123key To StudentsDocument3 pages2018 - Final Exam123key To StudentsMinh ThưNo ratings yet

- Cash Flow Tutorial QnsDocument13 pagesCash Flow Tutorial QnsCristian Renatus100% (1)

- Begino, Vanessa Jamila D. Class No. 4Document3 pagesBegino, Vanessa Jamila D. Class No. 4Vanessa JamilaNo ratings yet

- The Following Trial Balance Was Extracted From The Books of Craz LTD As at 31 Dec 2014Document5 pagesThe Following Trial Balance Was Extracted From The Books of Craz LTD As at 31 Dec 2014Pham TrangNo ratings yet

- Answer Sheet Mock Test 23Document5 pagesAnswer Sheet Mock Test 23Nam Nguyễn HoàngNo ratings yet

- Retained Earning Opening Balance - Net Income For The Year Ended 2017 2370 Dividend Paid (2,500)Document21 pagesRetained Earning Opening Balance - Net Income For The Year Ended 2017 2370 Dividend Paid (2,500)Umar Razi QasimNo ratings yet

- ACCT 4200 Project Solution - Final Posting 2022Document15 pagesACCT 4200 Project Solution - Final Posting 2022Jaspal SinghNo ratings yet

- AccountingDocument5 pagesAccountingIhsan UllahNo ratings yet

- INCOTAXDocument4 pagesINCOTAXnicole bancoroNo ratings yet

- A211 MC 2 - StudentDocument6 pagesA211 MC 2 - StudentWon HaNo ratings yet

- Practice Set 5 Financial Statements of Sole ProprietorshipsDocument3 pagesPractice Set 5 Financial Statements of Sole ProprietorshipsBritney PetersNo ratings yet

- Finance AccountsDocument2 pagesFinance AccountsBalumahendran. P Balumahendran. PNo ratings yet

- Statement of Comprehensive Income ProblemsDocument2 pagesStatement of Comprehensive Income ProblemsDarlyn Dalida San PedroNo ratings yet

- Alkaline Comp. Multi Step QuestionDocument2 pagesAlkaline Comp. Multi Step QuestionhotfujNo ratings yet

- Adjusting Journal EntriesDocument3 pagesAdjusting Journal EntriesAmirahNo ratings yet

- Assignment BAAD2033 Feb 2017Document5 pagesAssignment BAAD2033 Feb 2017RubanNo ratings yet

- Prepare Profit & Loss Account and Balance Sheet With The Help of Information Given in The Trial BalanceDocument4 pagesPrepare Profit & Loss Account and Balance Sheet With The Help of Information Given in The Trial BalanceEntertainment StatusNo ratings yet

- SAmpior Final 3 BSLM1ADocument5 pagesSAmpior Final 3 BSLM1ARedge Jefferson SampiorNo ratings yet

- Output No. 2 - PAS 1 Instruction: Write Your Answers On Long Bond PapersDocument2 pagesOutput No. 2 - PAS 1 Instruction: Write Your Answers On Long Bond Papersnmdl123No ratings yet

- Particulars Trial Balance Adjustments Adjusted Trial Balance DR CR DR CR DR CRDocument9 pagesParticulars Trial Balance Adjustments Adjusted Trial Balance DR CR DR CR DR CRasdfNo ratings yet

- Problem SolutionsDocument5 pagesProblem Solutionsmd nayonNo ratings yet

- 07 Activity 1 (24) .DocsDocument2 pages07 Activity 1 (24) .DocsNICOOR YOWWNo ratings yet

- Scope of Total Income and Residential StatusDocument3 pagesScope of Total Income and Residential StatusSandeep SinghNo ratings yet

- Income From House Property Solved Mcq's With PDF Download (Set-1)Document6 pagesIncome From House Property Solved Mcq's With PDF Download (Set-1)DevNo ratings yet

- Horizontal AnalysisDocument6 pagesHorizontal AnalysisjohhanaNo ratings yet

- Chapter-6 (Salary)Document53 pagesChapter-6 (Salary)BoRO TriAngLENo ratings yet

- Review of Financial Statement Preparation Analysis and Interpretation Pt.8Document6 pagesReview of Financial Statement Preparation Analysis and Interpretation Pt.8ADRIANO, Glecy C.No ratings yet

- Chapter 4 Economics of TourismDocument8 pagesChapter 4 Economics of TourismZeusNo ratings yet

- Act.4-8 Ae23Document6 pagesAct.4-8 Ae23Damian Sheila MaeNo ratings yet

- 2022 Accounting Grade 11 Project - ABDocument5 pages2022 Accounting Grade 11 Project - ABmishomabunda20No ratings yet

- Partner Ka Tax LagegaDocument16 pagesPartner Ka Tax LagegaVicky DNo ratings yet

- Brihanu - Research Paper-CommentsDocument20 pagesBrihanu - Research Paper-CommentsAddisu TeshomeNo ratings yet

- MTD YtdDocument350 pagesMTD YtdAmy Rose BotnandeNo ratings yet

- Alternative MeasuresDocument25 pagesAlternative MeasureslucaszayaNo ratings yet

- What Is AccountingDocument29 pagesWhat Is Accountingmule mulugetaNo ratings yet

- FN 200 - Financial Forecasting Seminar QuestionsDocument7 pagesFN 200 - Financial Forecasting Seminar QuestionskelvinizimburaNo ratings yet

- ch04 PDFDocument52 pagesch04 PDFerylpaez69% (13)

- T8 Homework Solutions-1Document15 pagesT8 Homework Solutions-1Anathi AnathiNo ratings yet

- Fatca - NSDL Non Ind. V. 21.3 (PG 1-4)Document4 pagesFatca - NSDL Non Ind. V. 21.3 (PG 1-4)digitaltarun99No ratings yet

- Social Accounting ModelsDocument19 pagesSocial Accounting ModelsSabrina Supti100% (1)

- How To Achieve Inclusive GrowthDocument901 pagesHow To Achieve Inclusive GrowthTAhmedNo ratings yet

- Human Capital in The Digital EconomyDocument6 pagesHuman Capital in The Digital EconomyalphathesisNo ratings yet

- PR - Asm 2 WawasanDocument4 pagesPR - Asm 2 WawasanCorrine TanNo ratings yet

- Diversion of IncomeDocument11 pagesDiversion of IncomeSrivathsan NambiraghavanNo ratings yet

- 3.2 Income Fro House Property AnswersDocument26 pages3.2 Income Fro House Property AnswersnairsulakshanaNo ratings yet

- Be Industrilization 2Document20 pagesBe Industrilization 2JAY SolankiNo ratings yet

- Jawaban Quiz 2Document2 pagesJawaban Quiz 2Muhammad IrvanNo ratings yet

- Chapters 3 and 4 Income TaxationDocument24 pagesChapters 3 and 4 Income TaxationJulie Ann BarcaNo ratings yet

- Income TaxDocument14 pagesIncome Taxanjuu2806No ratings yet

- Postemployment Benefits Wendy CompanyDocument6 pagesPostemployment Benefits Wendy CompanyArmelen DeloyNo ratings yet